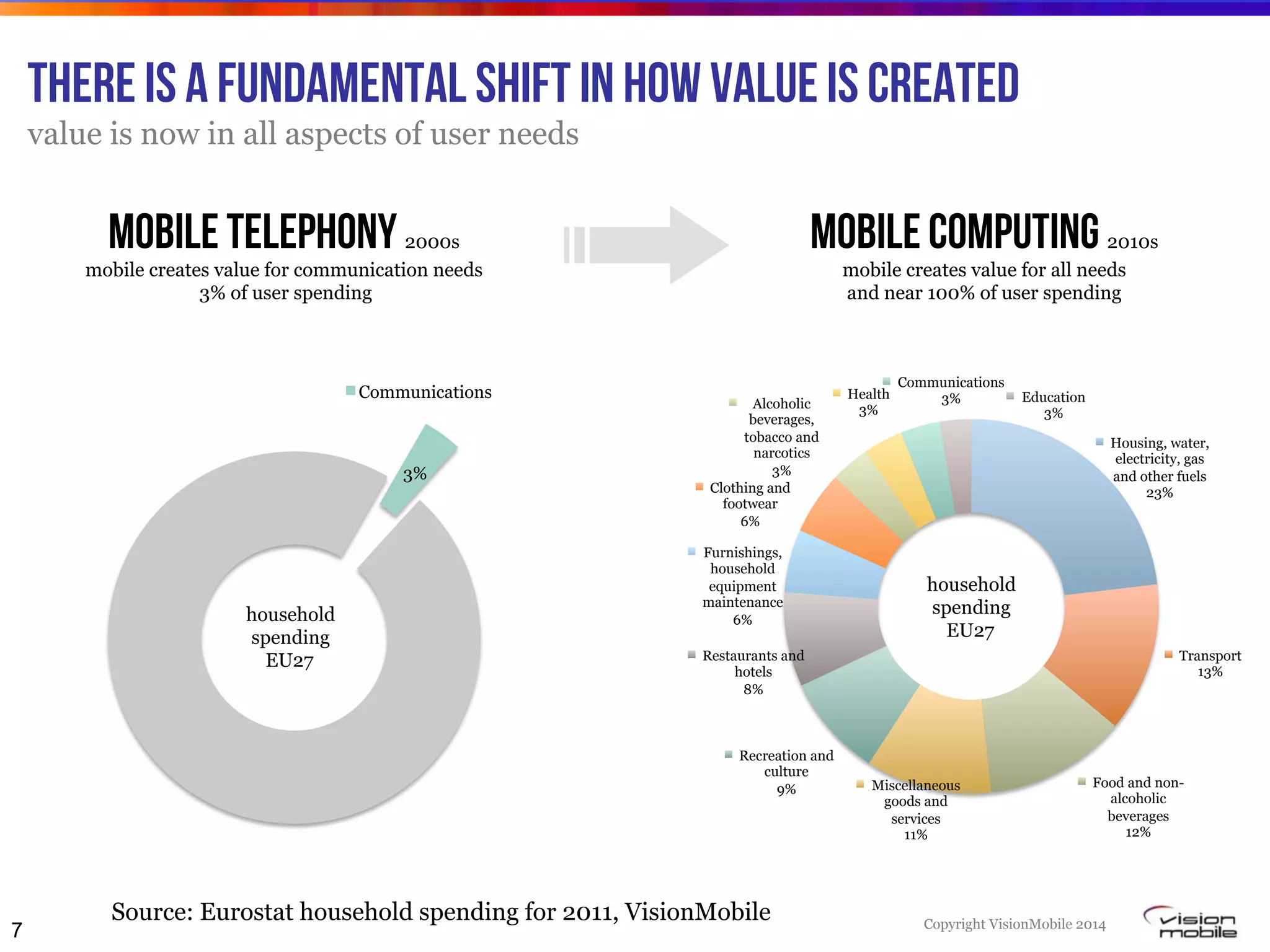

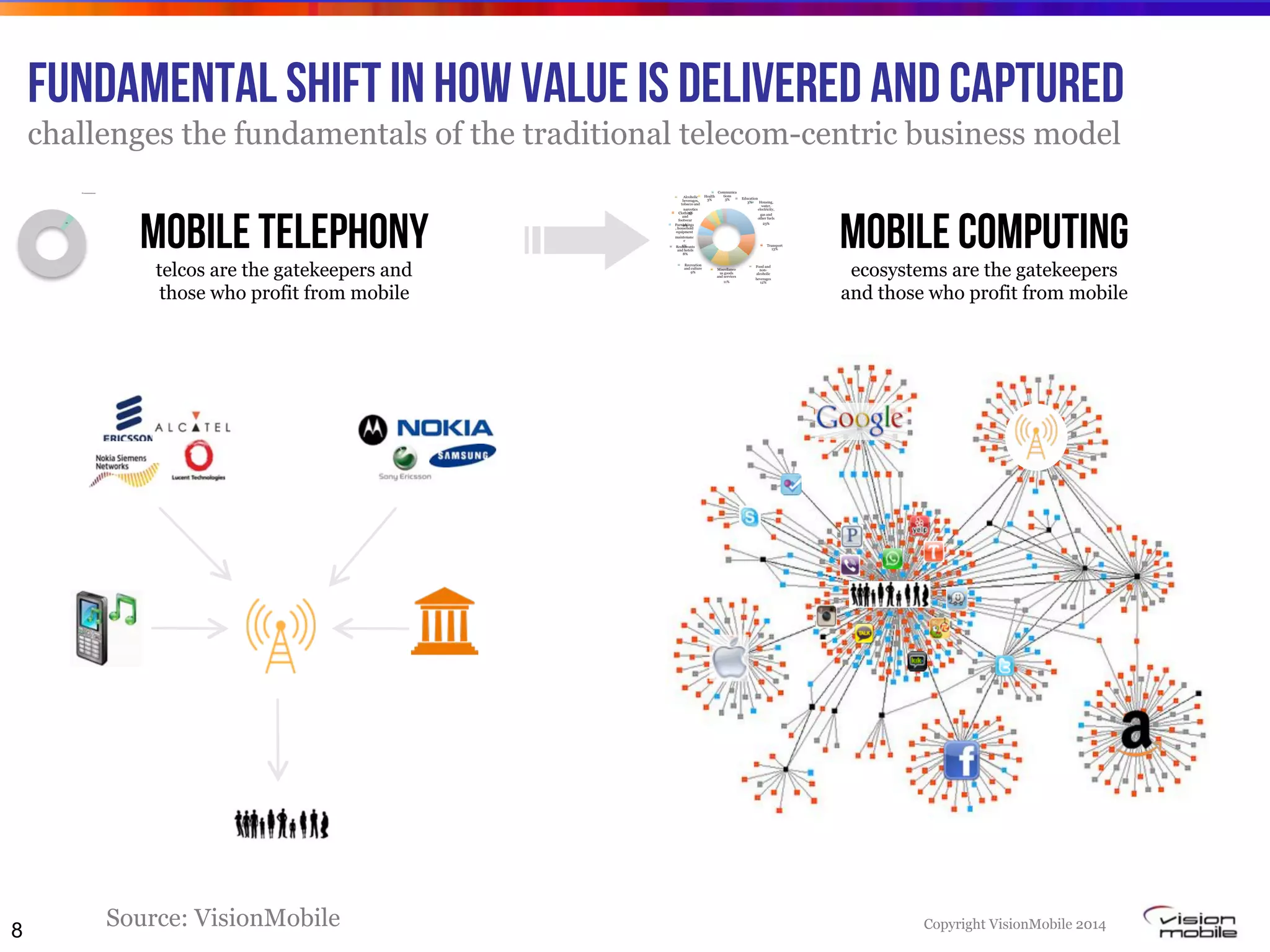

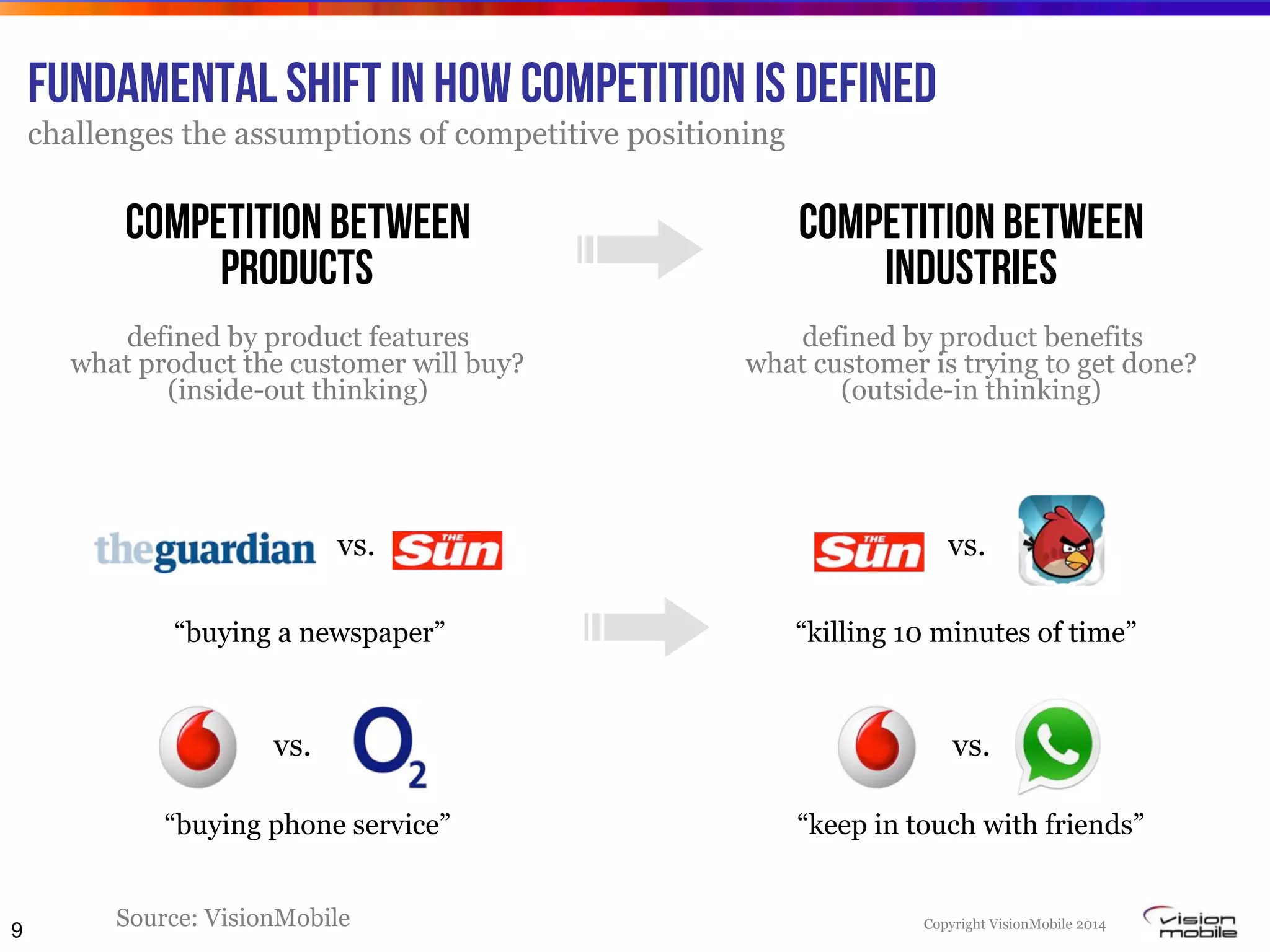

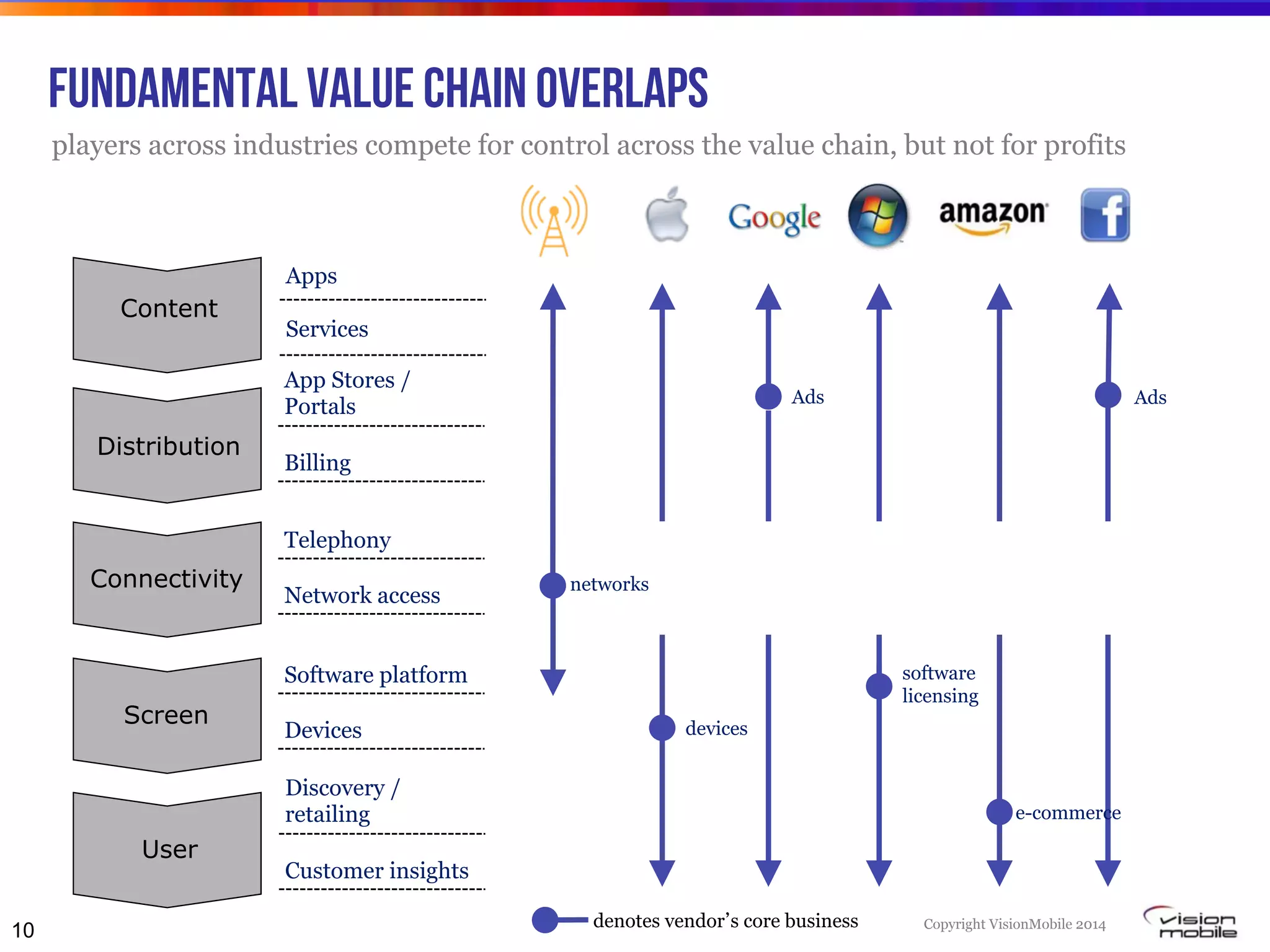

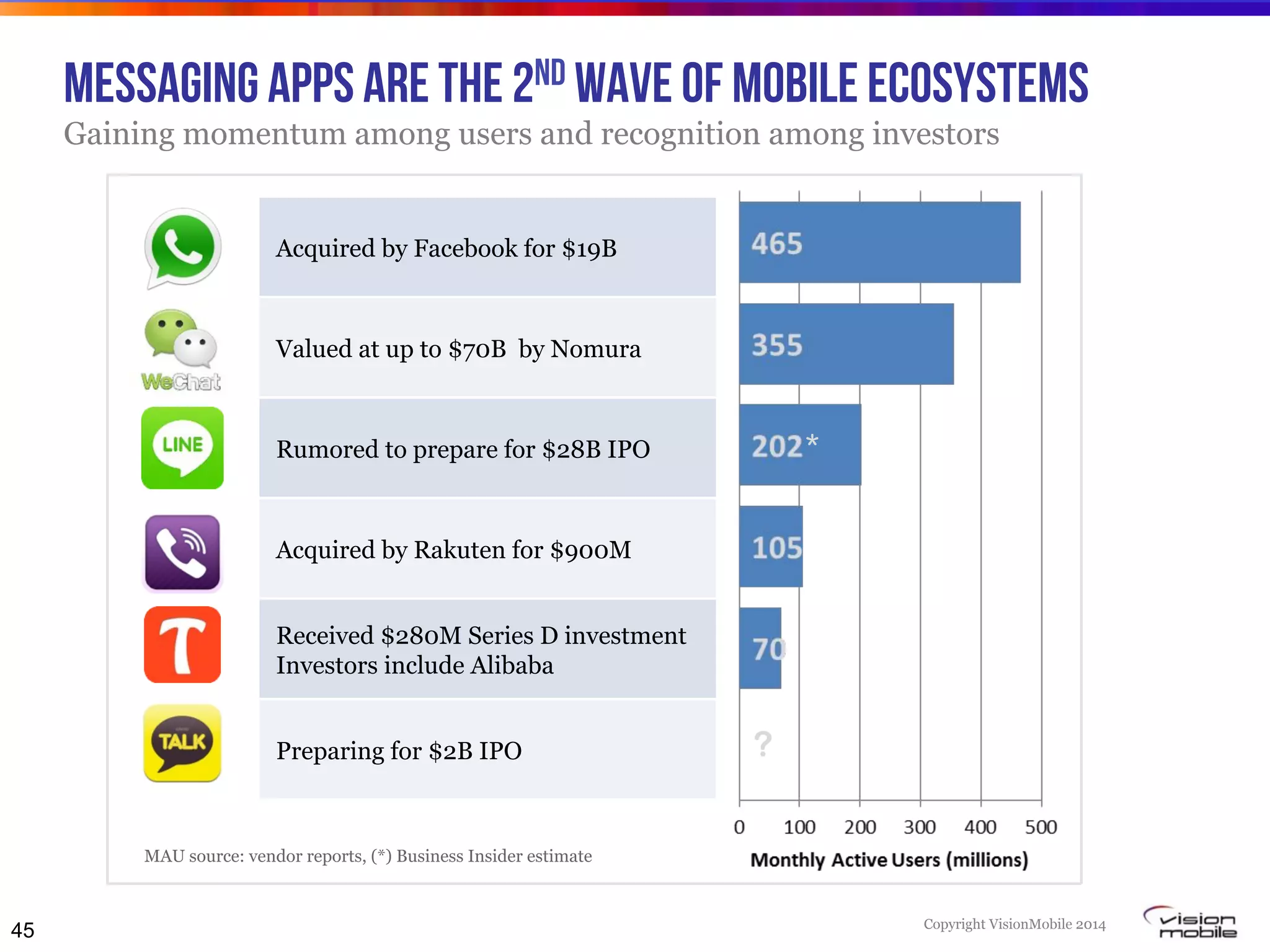

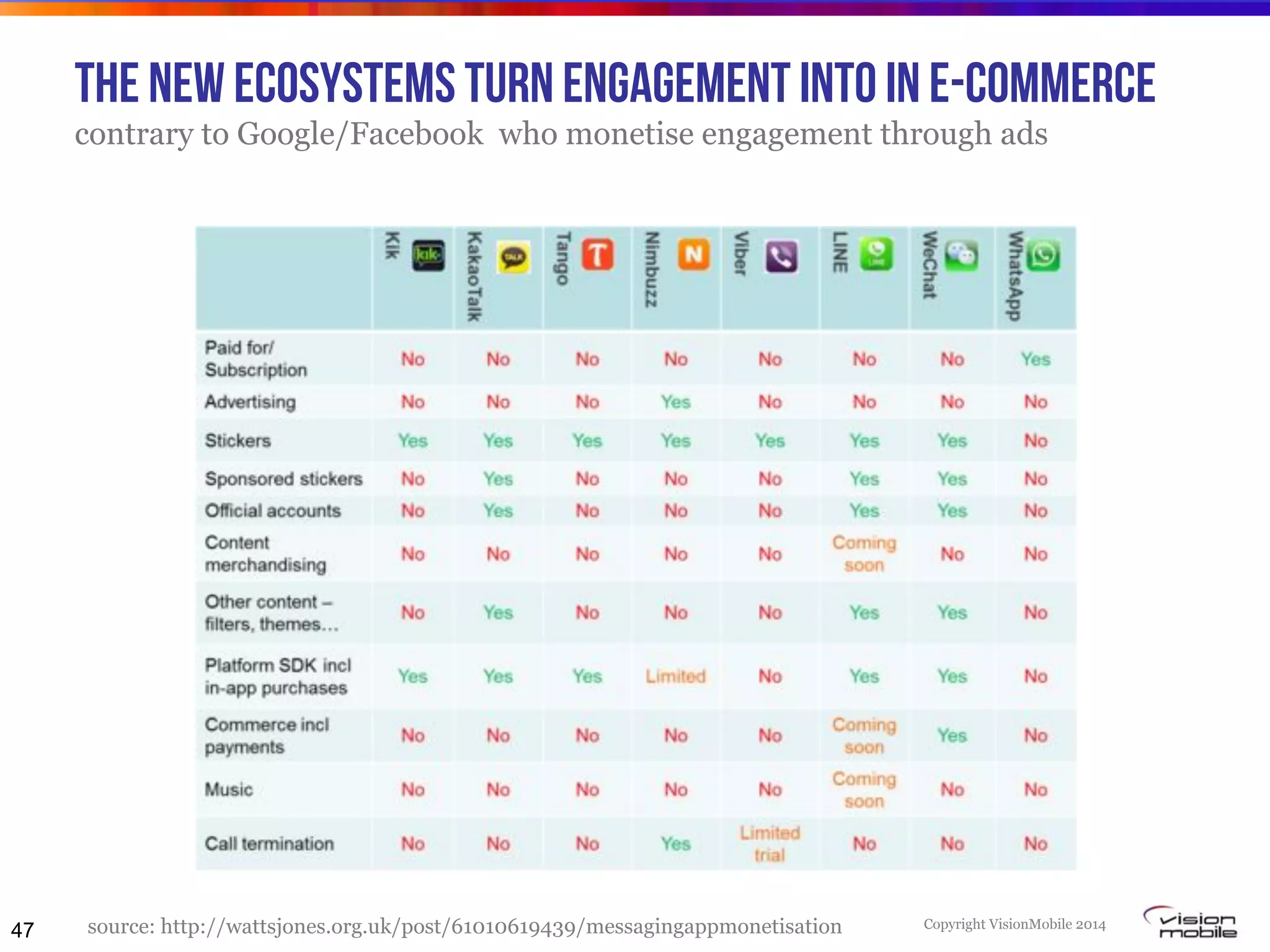

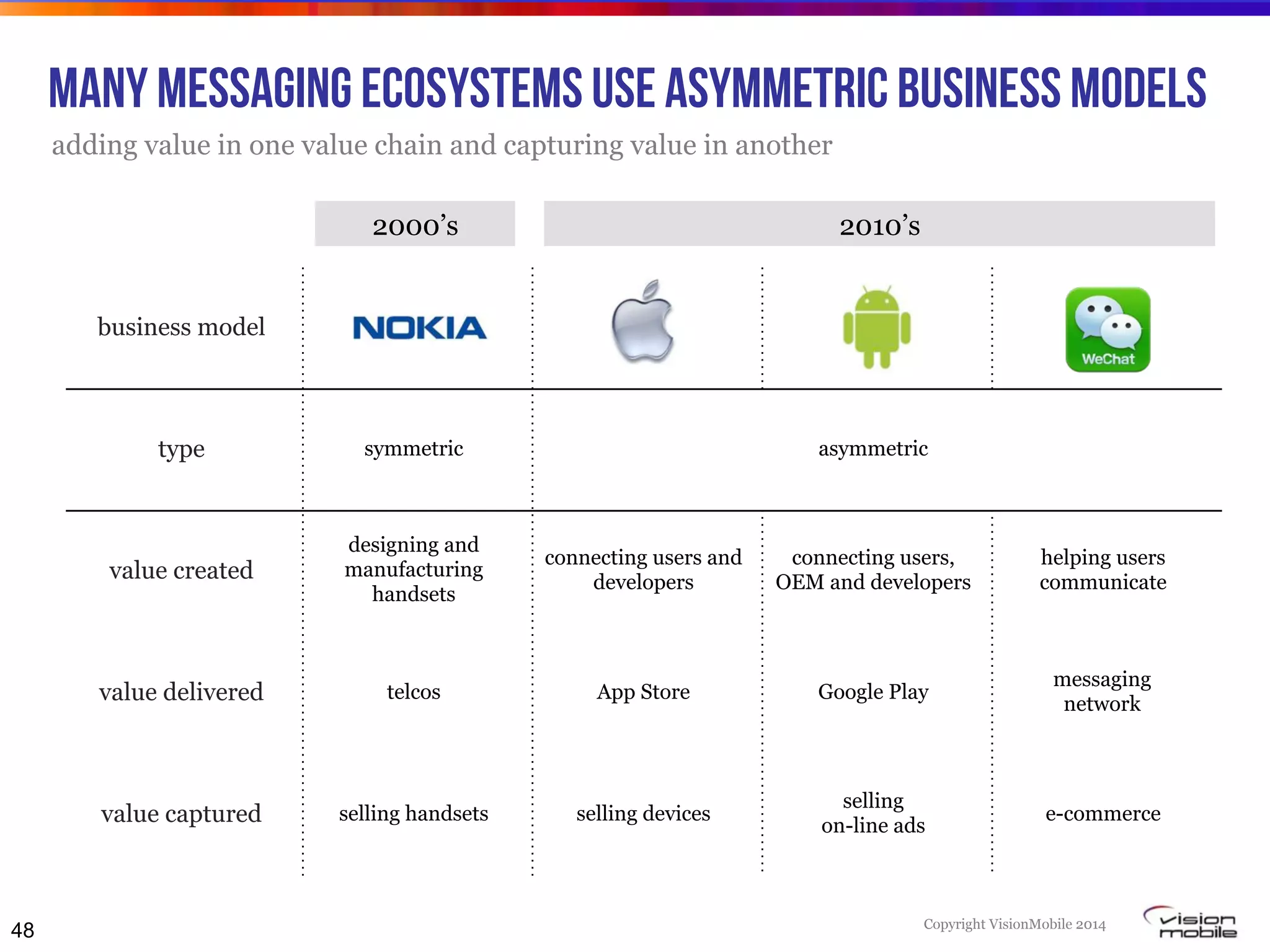

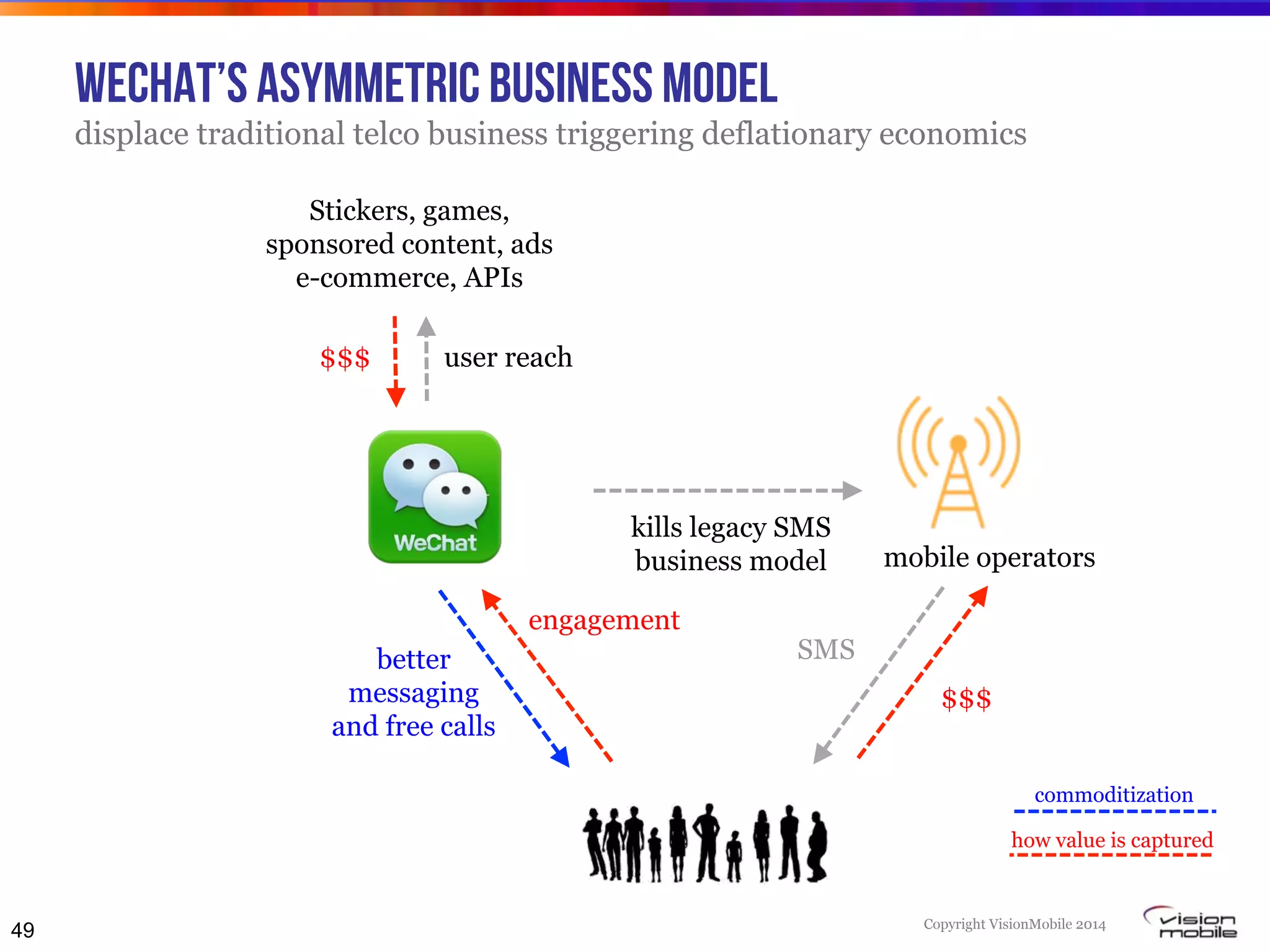

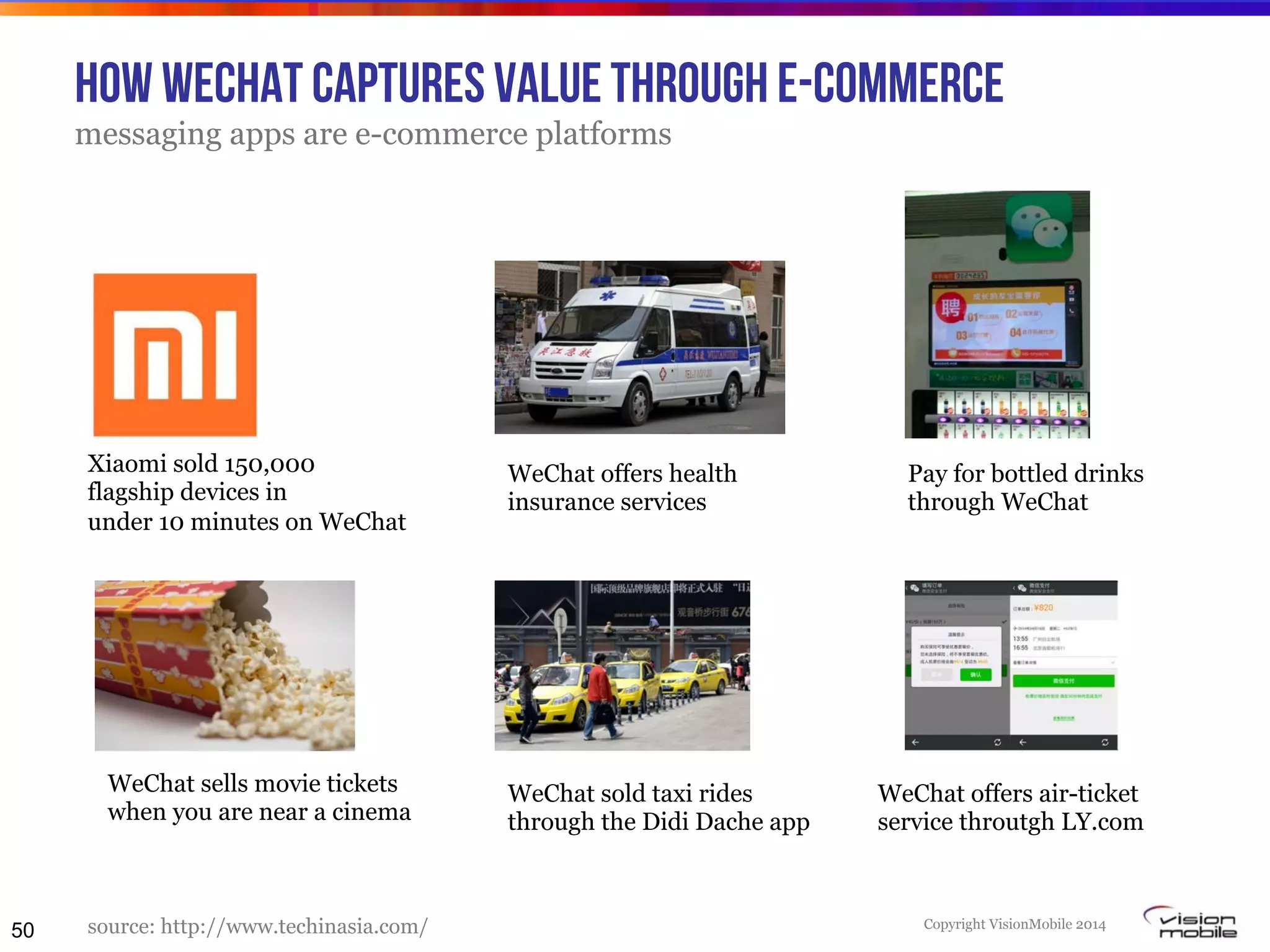

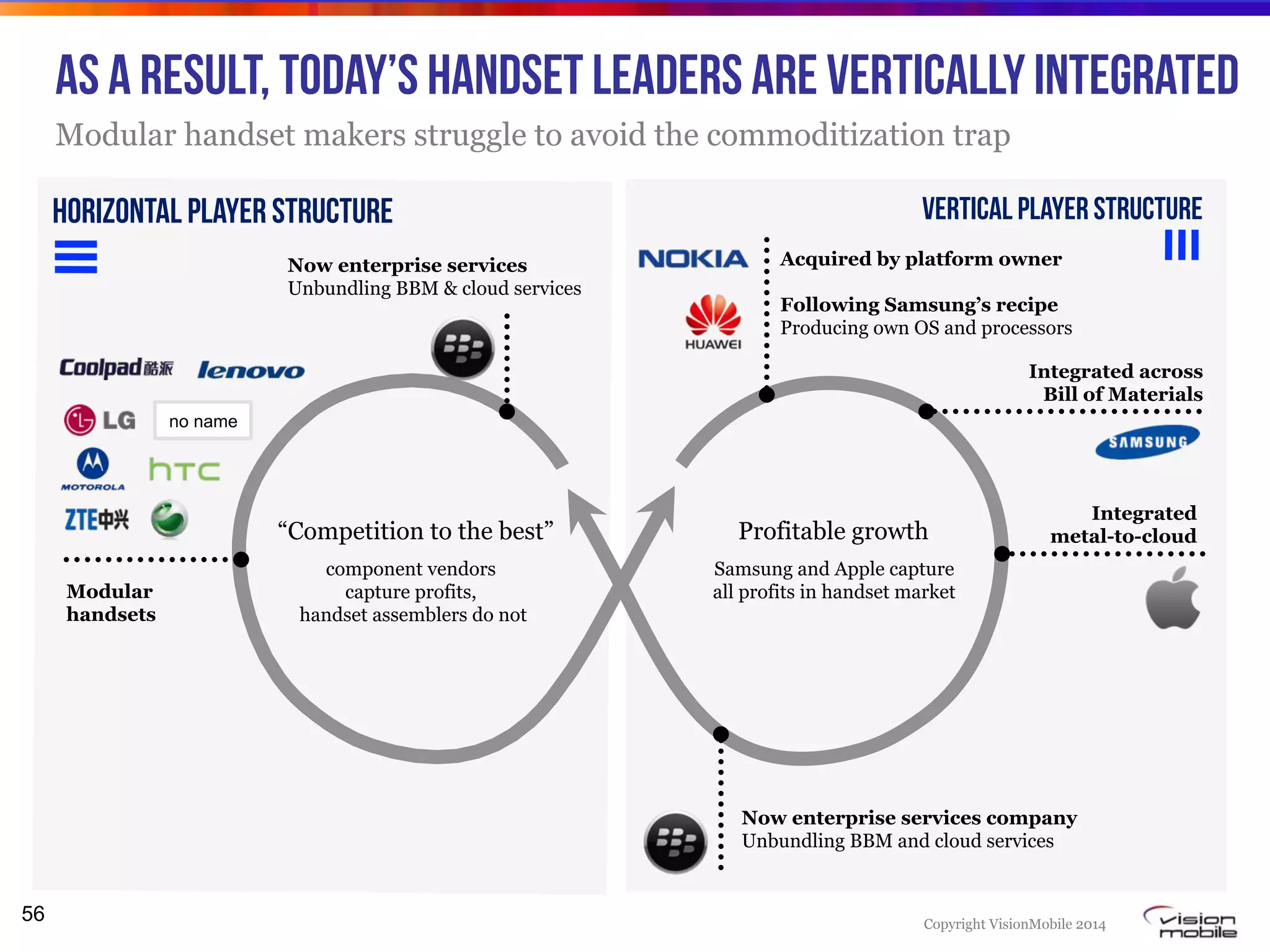

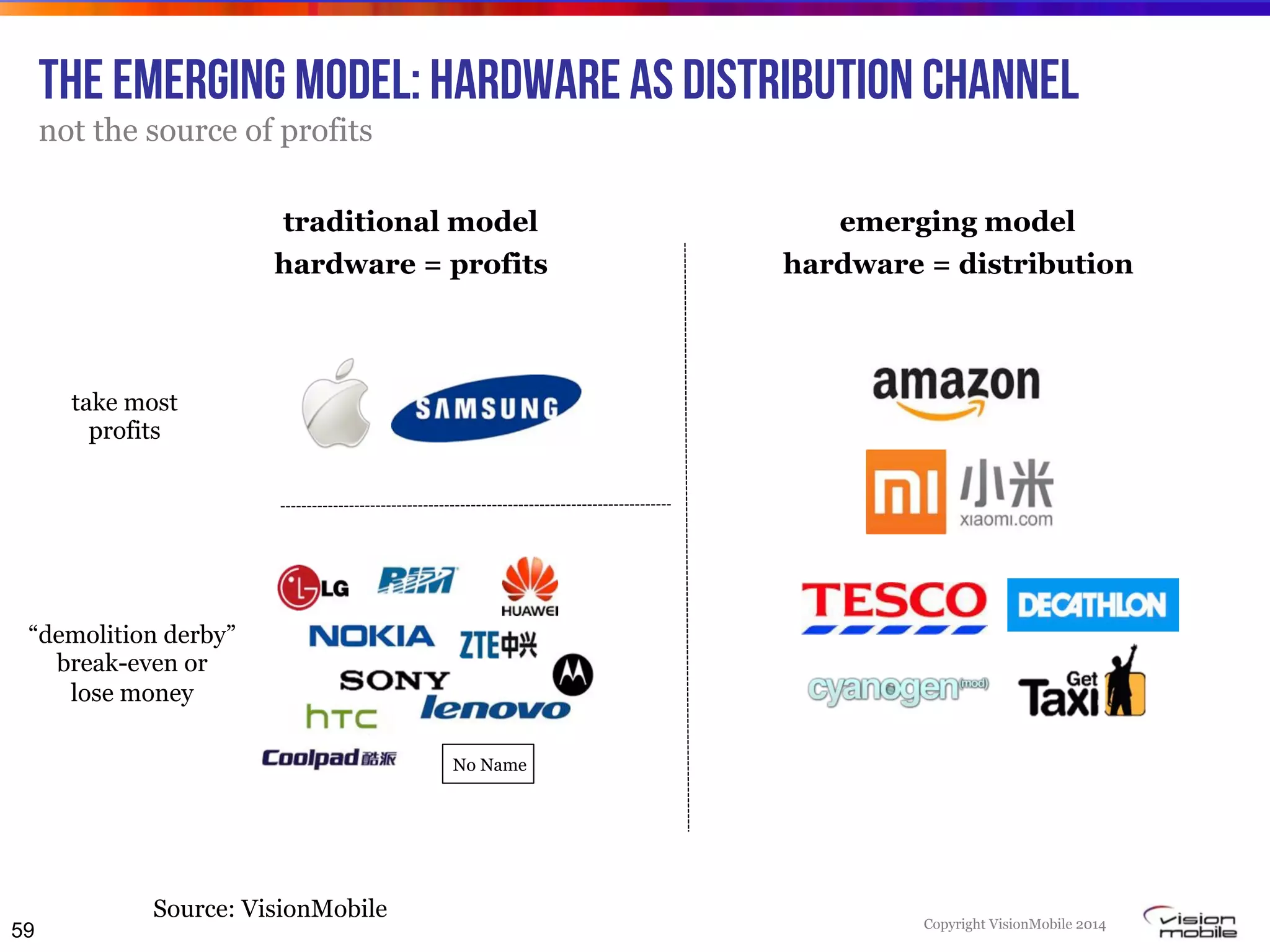

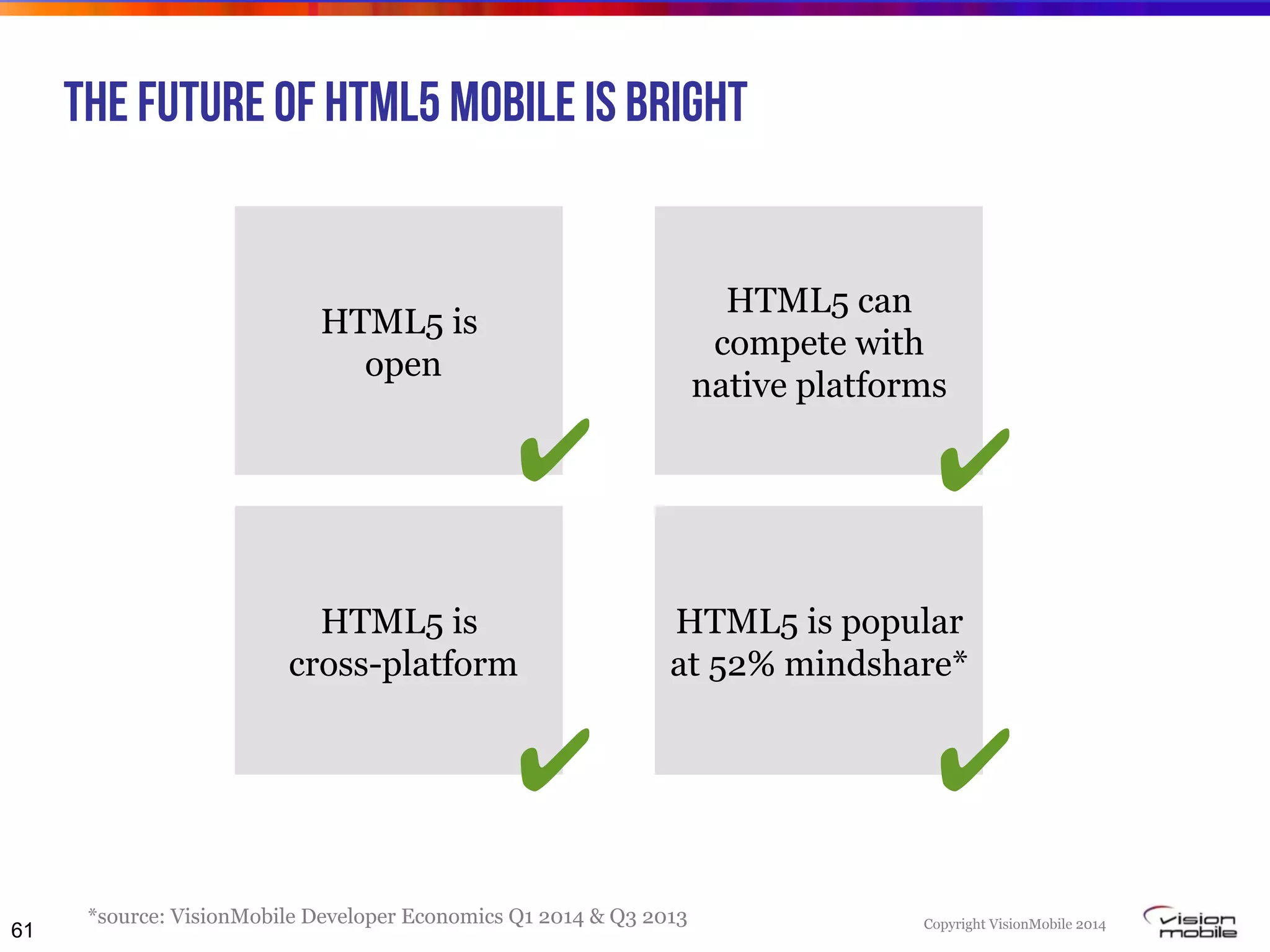

The document outlines the evolution and current landscape of mobile app ecosystems, highlighting how platforms like iOS and Android dominate the market and how they create significant economic value. It discusses the competitive challenges faced by traditional telecom models and the emergence of messaging apps as new powerful ecosystems transforming engagement into e-commerce opportunities. Furthermore, it emphasizes the need for new players to innovate and compete in an increasingly interconnected mobile environment where hardware is shifting towards being a distribution channel rather than a profit center.