VIP Call Girl Jamshedpur Aashi 8250192130 Independent Escort Service Jamshedpur

LL 455

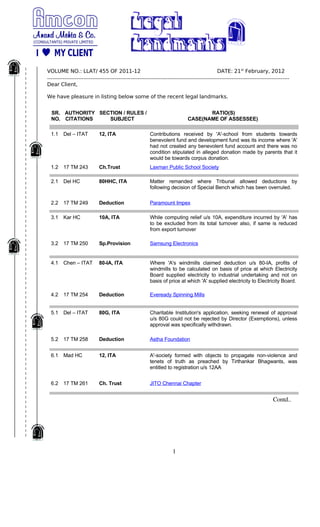

1. VOLUME NO.: LLAT/ 455 OF 2011-12 DATE: 21st February, 2012

Dear Client,

We have pleasure in listing below some of the recent legal landmarks.

SR. AUTHORITY SECTION / RULES / RATIO(S)

NO. CITATIONS SUBJECT CASE(NAME OF ASSESSEE)

1.1 Del – ITAT 12, ITA Contributions received by 'A'-school from students towards

benevolent fund and development fund was its income where 'A'

had not created any benevolent fund account and there was no

condition stipulated in alleged donation made by parents that it

would be towards corpus donation.

1.2 17 TM 243 Ch.Trust Laxman Public School Society

2.1 Del HC 80HHC, ITA Matter remanded where Tribunal allowed deductions by

following decision of Special Bench which has been overruled.

2.2 17 TM 249 Deduction Paramount Impex

3.1 Kar HC 10A, ITA While computing relief u/s 10A, expenditure incurred by 'A' has

to be excluded from its total turnover also, if same is reduced

from export turnover

3.2 17 TM 250 Sp.Provision Samsung Electronics

4.1 Chen – ITAT 80-IA, ITA Where 'A's windmills claimed deduction u/s 80-IA, profits of

windmills to be calculated on basis of price at which Electricity

Board supplied electricity to industrial undertaking and not on

basis of price at which 'A' supplied electricity to Electricity Board.

4.2 17 TM 254 Deduction Eveready Spinning Mills

5.1 Del – ITAT 80G, ITA Charitable Institution's application, seeking renewal of approval

u/s 80G could not be rejected by Director (Exemptions), unless

approval was specifically withdrawn.

5.2 17 TM 258 Deduction Astha Foundation

6.1 Mad HC 12, ITA A'-society formed with objects to propagate non-violence and

tenets of truth as preached by Tirthankar Bhagwants, was

entitled to registration u/s 12AA

6.2 17 TM 261 Ch. Trust JITO Chennai Chapter

Contd..

1

2. VOLUME NO.: LLAT/ 455 OF 2011-12 DATE: 21st February, 2012

SR. AUTHORITY SECTION / RULES / RATIO(S)

NO. CITATIONS SUBJECT CASE(NAME OF ASSESSEE)

7.1 Kar HC 10A, ITA While computing relief u/s 10A, expenditure incurred by 'A' has

to be excluded from total turnover if same is reduced from

export turnover

7.2 17 TM 263 Sp. Provision Himatsingka Seide

8.1 Del – ITAT 92C, ITA The only one price has been determined notwithstanding the

fact that two comparables were used. Therefore, on the plain

language of the provision, the adjustment as sought is not

admissible.

8.2 2012-TII-08 ALP Vipin Enterprises

Please let us know if you need any further information on these.

Thanking you and assuring you of our best services at all times.

Yours Faithfully,

For Anand Mehta & Co .,

(CONSULTANTS) PVT. LTD.

Anand V. Mehta

DIRECTOR

A mind of a consultant with a heart of a friend.

Mumbai Office- 334, Mulratna 1st Floor Narshi Natha Street Masjid (W) Mumbai 40009

Tel -022- 23400882 • Fax-022-23420195 • E-mail: amcon.mumbai@amcount.com

Pune Office –B/5 Shardaram Park, 34, Sasson Road, Near Jehangir Hospital, Pune - 411

001

Tel-020 6401 3124 • Fax 020- 30521223•E-mail: amcon.pune@amcount.com

Gram-MATERPLAN <--> MASTERPLAY

Website:www.amcount.com

2