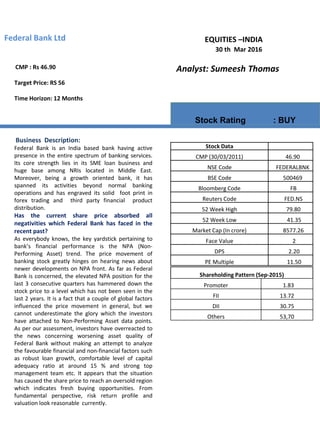

1. EQUITIES –INDIA

Analyst: Sumeesh Thomas

Stock Rating : BUY

Federal Bank Ltd

30 th Mar 2016

Business Description:

Federal Bank is an India based bank having active

presence in the entire spectrum of banking services.

Its core strength lies in its SME loan business and

huge base among NRIs located in Middle East.

Moreover, being a growth oriented bank, it has

spanned its activities beyond normal banking

operations and has engraved its solid foot print in

forex trading and third party financial product

distribution.

Has the current share price absorbed all

negativities which Federal Bank has faced in the

recent past?

As everybody knows, the key yardstick pertaining to

bank’s financial performance is the NPA (Non-

Performing Asset) trend. The price movement of

banking stock greatly hinges on hearing news about

newer developments on NPA front. As far as Federal

Bank is concerned, the elevated NPA position for the

last 3 consecutive quarters has hammered down the

stock price to a level which has not been seen in the

last 2 years. It is a fact that a couple of global factors

influenced the price movement in general, but we

cannot underestimate the glory which the investors

have attached to Non-Performing Asset data points.

As per our assessment, investors have overreacted to

the news concerning worsening asset quality of

Federal Bank without making an attempt to analyze

the favourable financial and non-financial factors such

as robust loan growth, comfortable level of capital

adequacy ratio at around 15 % and strong top

management team etc. It appears that the situation

has caused the share price to reach an oversold region

which indicates fresh buying opportunities. From

fundamental perspective, risk return profile and

valuation look reasonable currently.

CMP : Rs 46.90

Target Price: RS 56

Time Horizon: 12 Months

Shareholding Pattern (Sep-2015)

Promoter 1.83

FII 13.72

DII 30.75

Others 53,70

Stock Data

CMP (30/03/2011) 46.90

NSE Code FEDERALBNK

BSE Code 500469

Bloomberg Code FB

Reuters Code FED.NS

52 Week High 79.80

52 Week Low 41.35

Market Cap (In crore) 8577.26

Face Value 2

DPS 2.20

PE Multiple 11.50

2. Federal Bank Ltd

Mar 2016

Management’s reorientation towards growth:

Management has turned its attention on making the top management formidable in order to

equip them to deal with fast changing banking business environment. Federal Bank had some

recent high profile head count additions towards this end.

Acknowledging the significance of digitalisation, bank has converged major chunk of its efforts

towards rolling out new facilities to render enhanced banking experience for the tech-savvy

customers.

Management has identified that the era of aggressive branch expansion has come to an end and

the banks needs to generate more return in terms of increased productivity from the existing

branches and through branch optimisation efforts by means of relocation of less productive

braches to a different place.

Hitherto, the bank had not mined aggressively big ticket corporate loan market. Ever since the

management recognized the faster pace of corporate loan growth as pillar of banking business

uptick, it has taken steps to achieve this. Federal Bank can now boast of a network of relationship

managers across different geographies to cater to this loan segment.

Bank’s Loan Mix:

Bank maintains an excellent portfolio of loan with emphasis on its traditional stronghold SME

business . Below chart depicts the weightage of each loan vertical relative to its overall business

16392

13876

6137

15272

Loan mix as on Sep '16‘ (Amount in Crores)

Retail

SME

Agri

Corporate

3. Mar 2016

Federal Bank Ltd

Corporate loan segment registered a de-growth of 5 % in 2016 Q2 YOY. In order to address this issue,

there has been a renewed focus and conscious efforts on the part of top management to stimulate

growth by building a team relationship managers who will deal with pipe line and converts.

Acknowledging this as a positive development, we expect a strong credit off take in the next 2 to 3

quarters. As regards SME advances, Federal Bank has witnessed a growth rate of 17 % during the last

2 quarters. This is a very encouraging trend . Management is hopeful that the same will be sustained in

the next few quarters as well. The two factors which may turn in favour of loan growth as a whole will

be the continued low interest rate regime and the expected spending boost consequent to the

implementation of 7 th Central Pay Commission.

NPA movement:

Since Gross & Net NPA and Provision Coverage ratio data were observed to have some degree of

correlation, we have drawn up a comparison chart to gauge the growth trend of these 3 key

parameters during the last 5 quarters. As per the below chart, it is obvious that Gross and Net NPA

have spiked in the first quarter of FY 2016. Hence, since the bank which had already built up a

comfortable PCR during low interest period, it began using the provision coverage as a tool to stem the

huge erosion in net profit. The encouraging facet of the NPA trend is that the spike which was

witnessed during 2016 Q1 has not accelerated further, instead it began showing the sign of retreat

-10%

0%

10%

20%

30%

40%

2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3

Gross NPAs (%)

Net NPAs (%)

Provision Coverage Ratio

0

0.5

1

1.5

2

2.5

3

3.5

2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3

Gross NPAs (%)

Net NPAs (%)

4. Federal Bank Ltd- Fundamental Report

PCR diagram indicates that the bank

maintained the highest PCR to the

tune of 85 % during the period of low

NPA and started scaling down the

provision coverage as and when the

asset quality is getting worse. PCR is

hovering around the border of 70 % in

the latest available quarter.

60

65

70

75

80

85

90

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

Provision Coverage Ratio

Provision Coverage

Ratio

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Retail SME Agri Corporate

Segment wise Gross NPA as on Sep ‘2015’

Segment wise NPA

SME segment topped in the NPA

Category scoring 4.3 % level.

Corporate segment is not far behind

with a 3.58 % score on NPA front.

Out of slippage of Rs. 405 Crores

recorded in 2016 Q2, Large

corporate and SME have contributed

Rs. 170 Crores and 155 Crores of

NPAs respectively. During Q3 FY

2016, three NPA accounts were sold

to ARCs (Asset Reconstruction

Company) . The amounts were Rs.

225, Rs. 109 and Rs. 70 (all in Crores).

It is related to one shipping and 2

metal accounts.

Loan restructuring

Loan restructuring is an essential part of banking operation. Banks resort to loan restructuring as part of 5/25

or Corporate Debt Restructuring (CDR) schemes . It entails easing original terms and conditions of loan like

extending repayment period or reduction in interest rate etc. Major sectors covered are Infrastructure, Power

and Metal. Most of the NPA origination is linked to restructured category for most of the bank . Federal Bank is

also no exception.

While publishing quarterly results, analysts in general are eager to know the amount of fresh restructuring

occurred during the quarter. As regards Federal Bank, it is heartening to note that the fresh rescheduled

category of loan amount came to just 80 Lacks during the past 6 months However, there are a three accounts

for which moratorium on restructuring will be ending in the next 3 quarters. It is a cause of concern for the

bank. As on September 30th last year, bank’s standard restructured loan amount was Rs. 2200 Crores. SEBs

(State Electricity Boards) have 37 % exposure in Standard Restructured loan while Infrastructure and Airline

also had substantial contribution towards loan restructuring exercise.

5. Federal Bank- Fundamental Report

Deposit Profile:

Large chunk of deposits from NRI segment is the differentiating factor for Federal Bank. It appears that NRI

deposit growth reached at its peak to the tune of 27 % during the bygone quarter. However the bank is

cautiously optimistic over the sustained high deposit flow in this segment due to the impending recessionary

fears in the Middle East Countries as a result of crude oil price crash.

29.5

30

30.5

31

31.5

32

32.5

2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3

CASA (%) growth

CASA (%)

With regard to CASA proportion to overall

deposit, it is registering a steady and

sturdy pace of growth as depicted in the

chart.

Operational Efficiency:

Cost to Income ratio is the one of the main indicators of operational efficiency of the bank. There is a direct

relationship between NPA and Cost to Income Ratio. During the periods of rising NPA, cost to income proportion

will generally shoot up for banks, thanks to non-recognition of income from NPA accounts. In the below chart,

it is obvious that between Annual result of FY 2015 and 2016 Q1 quarterly result, cost to income ratio zoomed

in by around 7 %. On the expenditure side, we can see that era of branch expansion is over and the bank

currently focuses on extracting more productivity from the existing braches, hence we do not see a dramatic rise

in operational expenditure in terms of incremental man power and branch maintenance expenditure Hence

NPA largely accounts for the spike in the ratio. Based on this hypothesis, we have drawn another Cost to Income

ratio projection chart (in next slide)

0%

2%

4%

6%

8%

10%

12%

14%

2012 2013 2014 2015 2016 Q1 2016 Q2

Cost to Income growth (in %)

Cost to Income

6. Federal Bank Ltd – Fundamental Report

We hope that the bank will come

clean most of its NPA woes by FY

2017E. In such a situation, we project

that cost to income ratio will come

down significantly.

0

20

40

60

2015 2016E 2017E 2018E

Projected Cost to Income Ratio

Cost to Income

Non-Interest Income:

Regarding its non-interest income, Forex trading business was impacted due to slow down in Middle

East. However GIFT city initiatives and growth on retail loan front, have boosted fees income. Hence,

we scaled down our expectations on non-interest income and estimated some degree of de-growth in

FY 2016E.Hnowever we forecast that the growth momentum will be restored in full scale in FY 2017E

aided by fee income and third party financial product distribution.

Profitability:

Bank’s bottom line growth depends on the growth in advances, non-interest income and level of NPA.

Spike in NPA witnessed during the first quarter of the Current Financial Year has impacted the interest

income and necessitated higher provisioning, leading to lower profit.NPA level has remained sticky

during the successive 2 quarters as well. In view of these facts, we estimated that in FY 2016, Federal

Bank will register dip in net profit after witnessing a CAGR growth of 17.40 % over the last 5 years.

We are optimistic that bottom line growth will be revived in FY 2017E, buoyed by impressive uptick in

corporate , SME and housing loan growth. We also hope that bank’s NPA overhang will be turned

around by then.

0

500

1000

1500

2000

2011 2012 2013 2014 2015 2016 E 2017 E 2018 E

Projected Net Profit Growth in Crores

Net Profit

7. Federal Bank Ltd- Fundamental Report

0

1

2

3

4

2011 2012 2013 2014 2015 2016E 2017E 2018E

Net Interest Margin

Net Interest

Margin

Net Interest Margin (NIM) is one o the

Key Performance Indicators (KPIs) of the

bank.NIM gives an idea as to how much

net income a bank generates from its

core business. As per our assessment,

Net Interest Margin has hit the rock

bottom in the CY and is poised to rise in

the coming Financial Years. Falling cost

of deposit and rising CASA proportion

will be acting in favour of Net Interest

Margin and make an overall picture

about Federal bank rosy in the near

term.

Share Holder’s wealth:

Maximizing shareholder’s wealth is the core objectives behind existence of every business entities. In

order to gauge the accretion to the wealth, we have ratios like Earning Per Share, Return on Equity, Book

Value Per Share etc.

0

10

20

30

40

50

60

2012 2013 2014 2015 2016 E 2017E 2018E

Book Value Per Share

Book Value Per Share

Book Value per

share has been

steadily rising and

as per our

estimate ,it is

likely to cross Rs.

50 in FY 2018

8. Federal Bank Ltd– Fundamental Report

0.00

5.00

10.00

15.00

20.00

2011 2012 2013 2014 2015 2016 E 2017 E 2018 E

Return on Equity

Return on Net Worth

Liabilities 2011 2012 2013 14 2015 2016 E 2017E 2018 E

Share Capital 171.05 171.05 171.06 171.06 171.33 343.34 344.67 345.2

Total Reserves 4846.65 5421.25 6092.86 6689.65 7528.94 7825 8021.17 8716.61

Shareholder's Funds 5017.7 5592.29 6263.92 6860.71 7700.27 8168.34 8365.84 9061.81

Deposits 42988.45 48934.73 57611.17 59729.04 70822.69 76810.78 83614 93097

Borrowings 1888.36 4266.04 5239.05 5767.54 2392.98 3018 2927 3517

Other Liabilities & Provisions 1448.33 1751.17 1878.82 2287.55 1992.35 2340 2510 2617

Total Liabilities 51343 60544 70993 74645 82908 90337 97417 108292.81

Assets

Cash and Balance with Reserve Bank of

India 2936.35 2429.68 2748.86 3108.37 3381.98 3710 3935 4416

Balances with Banks and Money at Call 813.25 1108.7 977.67 1425.81 1402.46 1812 2216 2357

Investments 14407.9 17102.02 20854.49 23838.59 24189.81 26616 28014 33023

Advances 31957.81 37945.85 44327.42 43703.81 51529.19 55457 60422.03 65117

Net Block 292.92 337.03 412.08 413.84 446.1 471.12 515.81 562.8

Other Assets 934.61 1620.96 1670.03 2131.8 1932.16 2271 2314 2817.01

Total Assets 51343 60544 70993 74645 82908 90337 97417 108292.81

As per our estimate ,barring 2016E, return on equity will be on the path of steady rise . NPA woes and slow

down in non-interest income are likely to cause some amount of erosion in the return generated to Equity

share holders.

Financial Statements Rs. In Crores

9. Federal Bank Ltd– Fundamental Report

Financial Year 2011 2012 2013 2014 2015 2016 E 2017 E 2018 E

Interest Earned 4052.03 5581.72 6246.32 7005.7 7487.77 7633.17 8396.487 9152.171

Interest Expended 2304.49 3606.67 4208.94 4727.76 5056.33 5199.87 5459.864 5808.276

Net Interest Income 1747.54 1975.05 2037.38 2277.94 2431.44 2433.3 2936.624 3343.895

Other Income 518.33 532.2 664.64 685.18 878.54 746.52 903.2892 921.355

Operating Expenses 836.54 1008.06 1228.59 1493.5 1675.21 1718.56 1804.488 1894.712

Provisions and Contingencies 525.44 334.89 263.54 267.87 105.2 343.49 195.2062 235.6642

Profit before Tax 903.89 1164.3 1209.89 1201.75 1529.57 1117.77 1840.219 2134.874

Tax 315.42 392.79 359.68 372.83 517.48 338.38 588.8699 683.1595

Profit after Tax 588.47 771.51 850.21 828.92 1012.09 779.39 1251.349 1451.714

Share of Associate -32 -17.78 2.45 20.83 45.72 54.25 71 86

Consolidated Profit 556.47 753.73 852.66 849.75 1057.81 833.64 1322.349 1537.714

2016 Q3 2016 Q2 2016 Q1 2015 Q4 2015 Q3

Interest Earned 1902.76 1902.26 1913.15 1908.28 1870.1

Interest Expended 1297.56 1293.92 1308.39 1285.05 1282.94

Net Interest Income 605.2 608.34 604.76 623.23 587.16

Other Income 183.31 182.27 193.94 306 219.91

Operating Expenses 463.03 454.04 431.49 460.08 409.72

Provisions and Contingencies 75.11 87.28 153.1 39.78 -0.82

PBT 250.37 249.29 214.11 429.37 398.17

Tax 87.65 88.01 72.72 148.84 133.48

Profit after Tax 162.72 161.28 141.39 280.53 264.69

Quarterly results

Outlook and Valuation:

Banking Industry is going through its worst phase in terms of stressed assets at its peak. The most recent

quarterly financial result of banks unearthed huge amount of bad loan which is far above what industry and

street had expected. Asset quality review which is being conducted by RBI appears to have vowed to clean up

the balance sheet of banks by FY 2017 by flushing out the spiraling NPAs. Global growth concerns and

commodity route have increased stress level in the balance sheet of companies due to weakening realization

and decreased cash flow. These domestic and global scenario have posed huge challenge to Federal Bank

although its exposure to the most stressed iron and steel sector is insignificant. As far as Federal Bank is

concerned, the abrupt surge in bad loan during the current Financial Year has sent a shock wave to investors.

As we come closer to this Financial Year, we can see that bank has not yet been relieved from the grip of bad

loan woes. However, management exudes confidence that worst is behind now and bank is well prepared to

alleviate the concerns of its stakeholders through concerted efforts of the reinforced top management to

address NPA issues, renewed focus on loan growth ,digitalization and branch optimization etc.

10. Federal Bank Ltd-Fundamental

Our target price of Rs. 56 is based on the Gordon multi-stage growth model where we have applied

Residual Income Method of valuation. Our cost of equity is 12.54 % .We have applied a persistency factor

of 0.80 to arrive at a continuing residual value. Key hypothesis used while forecasting the financial

statement is that by FY 2017, the bank will get rid of most of its NPA worries and improve bottom line.

Similarly a sturdy pace of loan growth and a revival in growth momentum on non-banking operations

front will boost the top line.

Investors can accumulate the stock of Federal Bank Ltd on every dip and exit their investment when the

stock price reaches Rs. 56 with a holding period of 1 year.

Risks to Investment:

Below are the probable risk factors which investors have to bear in mind while buying stocks of Federal

Bank

Slower than expected corporate loan growth will impact top line growth which is expected to pick up in

FY 2017

Further slow down in Middle East economies will affect deposit flow from NRI segment and is likely to

cause dip in CASA proportion to over all deposit. This will erode Net Interest Margin of bank

Likelihood of more number of NBFCs obtaining bank license will intensify the competitive landscape

in banking sector. Moreover, the advent of payment banks is likely to pose challenges as far as current

and saving deposit space is concerned

Analyst's Disclaimer: This report reflects my personal opinion based on an in-depth study on some primary reports which

are available in public domain. Please do not make any investment decision purely based on this report. Please read it along

with other reports and make any investment decision after consulting your financial advisor. I will not be responsible in case

any one incurs any loss due to this report