More Related Content

Similar to LHTSI_Edition-1-2016

Similar to LHTSI_Edition-1-2016 (20)

LHTSI_Edition-1-2016

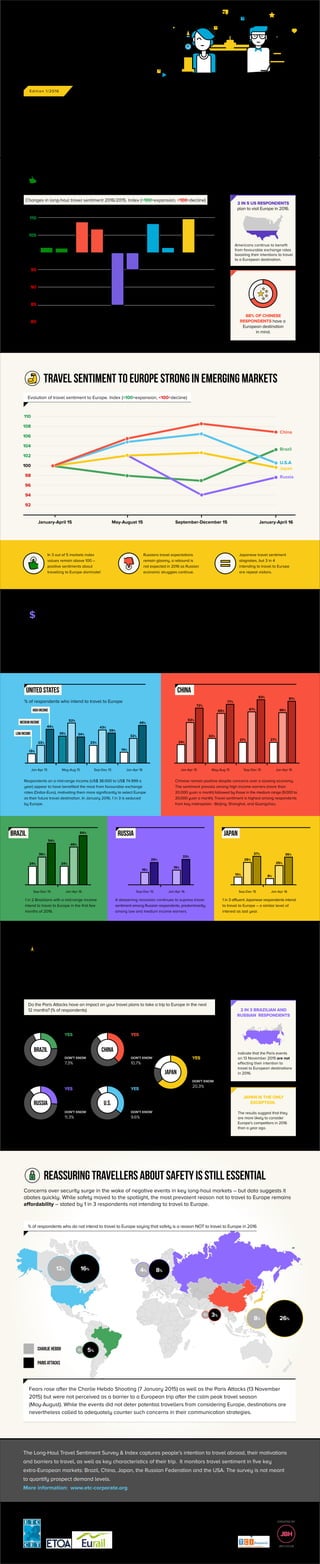

- 1. In 3 out of 5 markets index

values remain above 100 –

positive sentiments about

travelling to Europe dominate!

Russians travel expectations

remain gloomy, a rebound is

not expected in 2016 as Russian

economic struggles continue.

Japanese travel sentiment

stagnates, but 3 in 4

intending to travel to Europe

are repeat visitors.

Travel sentiment to Europe strong in emerging markets

Evolution of travel sentiment to Europe. Index (>100=expansion, <100=decline)

92

94

96

98

100

102

104

106

108

110

January-April 15 May-August 15 September-December 15 January-April 16

China

Brazil

U.S.A

Japan

Russia

The Long-Haul Travel Sentiment Survey & Index captures people’s intention to travel abroad, their motivations

and barriers to travel, as well as key characteristics of their trip. It monitors travel sentiment in five key

extra-European markets: Brazil, China, Japan, the Russian Federation and the USA. The survey is not meant

to quantify prospect demand levels.

More information: www.etc-corporate.org

The findings are brought to you by the European Travel Commission

etc-corporate.org, European Tourism Association etoa.org and Eurail

Group G.I.E. eurailgroup.org, realised by TCI Research

tci-research.com. © European Travel Commission. All rights reserved.

CREATED BY

JBH.CO.UK

Changes in long-haul travel sentiment 2016/2015. Index (>100=expansion, <100=decline)

DESTINATION

EUROPE

Optimistic outlook for long-haul travel from key markets

Long-haul travel markets are a significant source of growth for

European tourism. In 2015, China and the United States were at

the forefront, having contributed positively to Europe’s +5% in

international tourist arrivals. However, what are the expectations

for Europe’s key long-haul markets in the near future?

Measuring travel sentiment sheds light on potential

travellers’ dreams.

For Europe, the future looks promising in the majority of key

markets under scrutiny. Among the highest volume long-haul

markets, Chinese and American respondents are keener to travel to

European destinations than a year ago. But competition is at their

heels. 2016 will show if Europe can reap the positive effects of its

established image and joint marketing efforts in key markets.

Americans continue to benefit

from favourable exchange rates

boosting their intentions to travel

to a European destination.

2 IN 5 US RESPONDENTS

plan to visit Europe in 2016.

68% OF CHINESE

RESPONDENTS have a

European destination

in mind.

Long-Haul Travel Barometer

Edition 1/2016

Brazil

TravelSentimentIndex

China Russia United States Japan

80

85

90

95

100

105

110

Long-haul

destinations

Europe Long-haul

destinations

Europe Long-haul

destinations

Europe Long-haul

destinations

Europe Long-haul

destinations

Europe

Where to?

Respondents on a mid-range income (US$ 38.000 to US$ 74.999 a

year) appear to have benefited the most from favourable exchange

rates (Dollar-Euro), motivating them more significantly to select Europe

as their future travel destination. In January 2016, 1 in 3 is seduced

by Europe.

Chinese remain positive despite concerns over a slowing economy.

The sentiment prevails among high income earners (more than

20.000 yuan a month) followed by those in the medium range (9.000 to

20.000 yuan a month). Travel sentiment is highest among respondents

from key metropoles - Beijing, Shanghai, and Guangzhou.

Naturally available disposable income plays a significant role in having the opportunity to invest in long-haul

travel. Throughout the past months, the volatile economic environment has had a significant impact on the

evolution of respondents’ intention to travel in very diverse ways.

1 in 2 Brazilians with a mid-range income

intend to travel to Europe in the first few

months of 2016.

A deepening recession continues to supress travel

sentiment among Russian respondents, predominantly

among low and medium income earners.

1 in 3 affluent Japanese respondents intend

to travel to Europe – a similar level of

interest as last year.

Middleandhighincomegroupsmostinterestedina

triptoEurope

Jan-Apr 15

13%

24%

53%

72%

32%

65%

77%

27%

67%

83%

27%

66%

81%

23%

44%

35%

52%

34%

23%

43%

39%

14%

32%

49%

May-Aug 15 Sep-Dec 15 Jan-Apr 16 Jan-Apr 15 May-Aug 15 Sep-Dec 15 Jan-Apr 16

24%

36%

54%

24%

49%

64%

Sep-Dec 15 Jan-Apr 16

16%

29%

19%

33%

Sep-Dec 15 Jan-Apr 16

10%

29%

37%

8%

25%

36%

Sep-Dec 15 Jan-Apr 16

Brazil

UnitedStates

LOWINCOME

MEDIUMINCOME

HIGHINCOME

RuSSIA JAPAN

CHINA

Do the Paris Attacks have an impact on your travel plans to take a trip to Europe in the next

12 months? (% of respondents)

For the majority of survey respondents the Paris Attacks did not have an impact on their intention to travel to

Europe in the course of 2016. As seen above, travel sentiment to Europe remains positive indicating that

respondents would rather change their destination and activities than cancelling a trip to Europe altogether.

The(perceived)impactoftheParisAttackson

travelsentiment

indicate that the Paris events

on 13 November 2015 are not

effecting their intention to

travel to European destinations

in 2016.

2 IN 3 BRAZILIAN AND

RUSSIAN RESPONDENTS

The results suggest that they

are more likely to consider

Europe’s competitors in 2016

than a year ago.

JAPAN IS THE ONLY

EXCEPTION.

YES

23.9%

NO

68.8%

DON’T KNOW

7.3%

Brazil

RuSSIA

JAPAN

U.S.

DON’T KNOW

10.7%

YES

38.8%

NO

50.5%CHINA

DON’T KNOW

20.3%

YES

63.9%

NO

15.8%

DON’T KNOW

9.6%

YES

35.8%

NO

54.6%

DON’T KNOW

11.3%

YES

26.3%

NO

62.3%

12% 16% 8%4%

0%

0%

5%

3%

26%8%

Concerns over security surge in the wake of negative events in key long-haul markets – but data suggests it

abates quickly. While safety moved to the spotlight, the most prevalent reason not to travel to Europe remains

affordability – stated by 1 in 3 respondents not intending to travel to Europe.

Reassuringtravellersaboutsafetyisstillessential

% of respondents who do not intend to travel to Europe saying that safety is a reason NOT to travel to Europe in 2016

Fears rose after the Charlie Hebdo Shooting (7 January 2015) as well as the Paris Attacks (13 November

2015) but were not perceived as a barrier to a European trip after the calm peak travel season

(May-August). While the events did not deter potential travellers from considering Europe, destinations are

nevertheless called to adequately counter such concerns in their communication strategies.

CHARLIE HEBDO

paris attacks

% of respondents who intend to travel to Europe