Basics of accounting

•Download as PPTX, PDF•

3 likes•503 views

Basics of accounting for induction of MBA students

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Basics of accounting

Similar to Basics of accounting (20)

Recently uploaded

Recently uploaded (20)

Basics of accounting

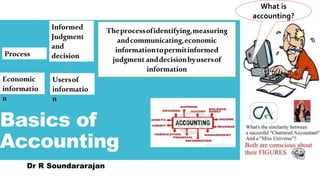

- 1. Basics of Accounting Dr R Soundararajan Theprocessofidentifying,measuring andcommunicating,economic informationtopermitinformed judgmentanddecisionbyusersof information Process Economic informatio n Informed Judgment and decision Usersof informatio n What is accounting?

- 2. Career CA

- 5. USERS InternalExternal Owners/ Investors Management Employees Decision Making Profit Which Investment buy/sell Stability/ Profitability 1. Lenders – their money Safe? 2. Suppliers – Amount owned would be paid? 3. Government / Regulators-Tax, Governance 4. Customers- How much to buy? 5. Public – trends 6. Research Scholars- Who are the users?

- 6. Book Keeping : is the art of recording business transactions in a systematic manner Accounting is the design of system of records, preparation of reports, Classifying and summarizing data, communicating the results to the interested party Can you differentiate book keeping and accounting Refers to business dealing or event Which can be measurable in terms of money or business worth Cash transaction CreditTransaction

- 7. Basic Terminologies Goods Commodities, articles, products or things Purchase Commodities bought Sales Goods sold Purchase Return Return outwards Sales Return Return inwards

- 8. Basic Terminol ogies Stock Goods lying with business unsold Closing Stock Lying with business unsold at the end of accounting period Opening Stock Lying with business unsold at the beginning of accounting period Assets Due to it by othersLiabilities Owes to others 1. Accuracy can be tested by trial balance 2. Income statement to ascertain profit 3. Financial position by balance sheet 4. Ready information available for decision making 5. Tax for government Double entry debit and credit Each transaction involves exchange of benefits and expense/ loss Doubleentry system

- 9. Basic Terminologies Capital It refers to the money or money’s worth introduced or invested by proprietor Drawing Value of goods or cash withdrawn by the proprietor Debtor Who owns money to the business as he received some benefits from the business Creditors To whom the business owe moneyEquity All claims against a firm . It denotes liability Solvent Trader is solvent if he is able to pay

- 11. Branches of Accounting 1. Record 2. Prepare Financial statement 3. AscertainP/L 4. Communicate tousers Financial Accounting 1. Costofthe products services ascertain 2. ControlCost 3. Budget, Standard Costing, Marginal costing Cost Accounting Costaccounting methodsapplied fordecision makingand policy formulation Management Accounting

- 12. Limitations of Accounting Measuremonetary valuesonly Recordhistorical data Preparation of accounts fora particular period Actualcostonly recorded Notusefulforcost control Failstofixpricesas costisknownafter incurring

- 13. Accounting Concepts BusinessEntity Separate and distinct from person supply capital GoingConcern Business Concern will exist up to foreseeable Future [ IAS-1] Moneymeasurement Only transaction involving money or money equivalent will be recorded Matching Accounting Concept Cost Cost concept assumes that the price to acquire an asset is the basis for subsequent accounting DualAspect Every business transaction has two aspects Asset= Capital + liabilities AccountingPeriod Accounting Period Realization The revenue is matched for the same period Revenue is recognized when a sale is made

- 14. Accounting Convention Accounting convention Revenue is recognized when a sale is made Conservation – safe guard asset – anticipate no profit and provide for all losses Full disclosure all material information to be revealed Consistency-Accounting policy to be same year to year Materiality: Only important material details and avoid insignificant details 1 2 3 4

- 15. GAAP Rules and principles set for presenting financial information Which economic resources and obligations should be recorded Which changes of assets and liabilities should be recorded ? How the changes of assets and liabilities measured Which financial statement to be prepared? What accounting policies to be adopted? In India Accounting Standards Board[ ASB] Institute of chartered Accountants of India[ ICAI] Department of Company affairs[ DCA] SEBI ICWAI ICS Cash system Entries only when cash is received or paid No entry when receipt or payment due. Mercantile system When become due for payment or receipt Transaction when occurred. Followed by all merchants trade and industry What does an accountant say when boarding a train? 'Mind the GAAP'.

- 16. FirstStep in book keeping 1.All transaction are recorded in journal called book of prime entry 2.Daily record 3.Information for an item may not be in one place 4,It is called Journalizing 1.Ledger is a book of final entry 2.Posting from journal to ledger done periodically 3.Information for an item at one place 4. It is called posting Trial Balance 1.From ledger nominal accounts Dr balances posted in Dr Column and Cr Balance in Cr Column 2.It is the summary of various accounts 3. Ensure arithmetical accuracy 4. Facilitate preparation of final accounts What is journal? Journal has Date Particulars Ledger folio- later the journal is posted in ledger Dr Cr Journal Ledger Trial Balance

- 17. Types of accounts and rules PersonalAccounts • Accounts of persons with whom business deals • Debit Receiver • Credit Giver RealAccounts • Tangible Intangible • Related to things - assets • Debit what comes in • Credit what goes out NominalAccounts • Transactions • Expenses, loses • Income, gain • Debit all expenses, and losses Credit all income and gains