Idea cellular investor rationale

•Download as DOCX, PDF•

0 likes•239 views

Investor Rationale for Idea Cellular (2014)

Recommended

More Related Content

What's hot

What's hot (18)

Similar to Idea cellular investor rationale

Similar to Idea cellular investor rationale (20)

Recently uploaded

Recently uploaded (20)

Idea cellular investor rationale

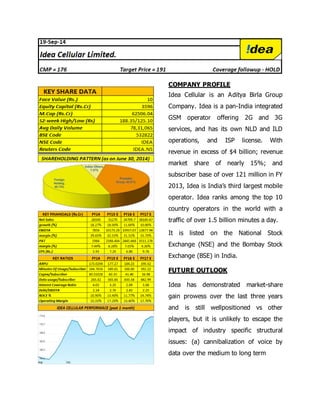

- 1. COMPANY PROFILE Idea Cellular is an Aditya Birla Group Company. Idea is a pan-India integrated GSM operator offering 2G and 3G services, and has its own NLD and ILD operations, and ISP license. With revenue in excess of $4 billion; revenue market share of nearly 15%; and subscriber base of over 121 million in FY 2013, Idea is India’s third largest mobile operator. Idea ranks among the top 10 country operators in the world with a traffic of over 1.5 billion minutes a day. It is listed on the National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE) in India. FUTURE OUTLOOK Idea has demonstrated market-share gain prowess over the last three years and is still wellpositioned vs other players, but it is unlikely to escape the impact of industry specific structural issues: (a) cannibalization of voice by data over the medium to long term

- 2. (b) Licence renewal in crucial 900 MHz band which is up for auction in FY15, and (c) Impact of the imminent entry of Reliance Jio. Licence Renewal: Idea enters a crucial period over the next 12‐18 months as it seeks to renew nine licenses in the crucial 900MHz band even as FY14 performance and recent fund raising gives us confidence about its renewal capabilities. Idea ticked all the right Boxes in the year gone by with 18% revenue growth, 29% EBIDTA margin and a ARPU of 173. Operating cash flow jumped ~86% YoY on doubling of pre-tax profit and easing of working capital cycle. However spectrum purchases in Feb auctions plus FY14 capex led to negative free cash flow for the year. Overall license renewals remain the key near term risk but we remain optimist on Idea’s ability to fund spectrum purchases. Overall Outlook: The company has reported strong RPM expansion on both Voice and Data but we believe part of the growth is attributable to election led spending. In our view although voice growth would moderate in ensuing quarters, we expect the data revenue to rise considerably at a CAGR of 18% upto 2019. Launch of R-Jio would continue to remain an overhang on the telecom sector as we strongly believe R-Jio would launch data services with huge price disruption. This would lead to slowdown in subscriber acquisition post R-Jio enters the market affecting growth in Net Sales. We expect the sales to grow at a CAGR of 10% upto 2019. Further, Idea’s 9 circles are coming up for renewal, which contribute 79% of revenue so it will have to retain majority of 900 MHz spectrum holding. Given the strong operating traction in wireless business and recent fund raising, we remain confident of Idea’s capability to fund the spectrum purchases although we note that competition in the 900MHz band could lead to higher than expected renewal payouts. Recommendation: We maintain a ‘HOLD’ rating on the stock with the 9-12 month target price of Rs.191 per share, a 9% rise from the current market price of Rs. 176.

- 4. KEY CONCERNS 900 MHz auctions coming up next year contribute to 79% of Idea Cellular’s revenue. Being unable to retain even one of the 9 circles up for auction can severely impact revenue and profitability Launch of Reliance Jio in 2016 is a major threat due to the expected huge price disruption in services offered. Subscriber growth and revenue can be impacted further Unforeseen disputes with TRAI regarding tower sharing can be an issue Further reduction in pricing to stay competitive in the market can also affect revenue margin FIANANCIAL PERFORMANCE: (CONSOLIDATED)

- 6. KEY RATIOS