QNBFS Daily Market Report June 15, 2021

•

0 likes•41 views

The QE Index rose 0.7% to close at 10,811.2. Gains were led by the Industrials and Banks & Financial Services indices, gaining 1.1% and 0.7%, respectively.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to QNBFS Daily Market Report June 15, 2021

Similar to QNBFS Daily Market Report June 15, 2021 (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

QNBFS Daily Market Report June 15, 2021

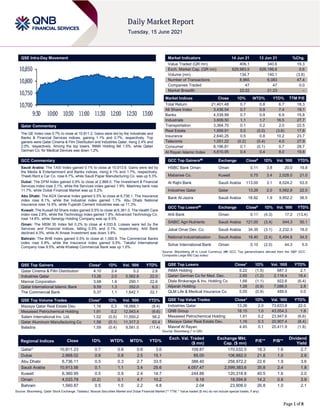

- 1. Page 1 of 8 QSE Intra-Day Movement Qatar Commentary The QE Index rose 0.7% to close at 10,811.2. Gains were led by the Industrials and Banks & Financial Services indices, gaining 1.1% and 0.7%, respectively. Top gainers were Qatar Cinema & Film Distribution and Industries Qatar, rising 2.4% and 2.0%, respectively. Among the top losers, INMA Holding fell 1.5%, while Qatari German Co. for Medical Devices was down 1.2%. GCC Commentary Saudi Arabia: The TASI Index gained 0.1% to close at 10,913.6. Gains were led by the Media & Entertainment and Banks indices, rising 4.1% and 1.7%, respectively. Theeb Rent a Car Co. rose 6.7%, while Saudi Paper Manufacturing Co. was up 5.3%. Dubai: The DFM Index gained 0.9% to close at 2,868.0. The Investment & Financial Services index rose 2.1%, while the Services index gained 1.9%. Mashreq bank rose 11.7%, while Dubai Financial Market was up 5.2%. Abu Dhabi: The ADX General Index gained 0.5% to close at 6,736.1. The Insurance index rose 6.1%, while the Industrial index gained 1.7%. Abu Dhabi National Insurance rose 14.5%, while Fujairah Cement Industries was up 11.3%. Kuwait: The Kuwait All Share Index gained 0.5% to close at 6,361.0. The Health Care index rose 2.8%, while the Technology index gained 1.8%. Advanced Technology Co. rose 14.6%, while Senergy Holding Company was up 9.5%. Oman: The MSM 30 Index fell 0.2% to close at 4,033.8. Losses were led by the Services and Financial indices, falling 0.5% and 0.1%, respectively. Ahli Bank declined 4.3%, while Al Anwar Investment was down 3.8%. Bahrain: The BHB Index gained 0.5% to close at 1,560.9. The Commercial Banks index rose 0.8%, while the Insurance index gained 0.5%. Takaful International Company rose 9.5%, while Khaleeji Commercial Bank was up 1.5%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Qatar Cinema & Film Distribution 4.10 2.4 5.2 2.6 Industries Qatar 13.26 2.0 5,562.8 22.0 Mannai Corporation 3.68 1.6 290.1 22.6 Qatar International Islamic Bank 9.59 1.3 352.0 6.0 The Commercial Bank 5.37 1.1 1,642.1 22.1 QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Mazaya Qatar Real Estate Dev. 1.16 0.3 18,068.1 (8.4) Mesaieed Petrochemical Holding 1.91 0.2 12,543.4 (6.6) Salam International Inv. Ltd. 1.02 (0.5) 11,550.2 56.2 Qatar Aluminum Manufacturing Co 1.58 (0.1) 11,317.3 63.4 Baladna 1.59 (0.4) 9,581.0 (11.4) Market Indicators 14 Jun 21 13 Jun 21 %Chg. Value Traded (QR mn) 406.1 340.6 19.3 Exch. Market Cap. (QR mn) 629,983.5 626,186.6 0.6 Volume (mn) 134.7 140.1 (3.8) Number of Transactions 8,965 6,083 47.4 Companies Traded 47 47 0.0 Market Breadth 22:22 21:23 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 21,401.48 0.7 0.8 6.7 18.3 All Share Index 3,436.54 0.7 0.9 7.4 19.1 Banks 4,539.99 0.7 0.9 6.9 15.8 Industrials 3,609.50 1.1 1.7 16.5 27.7 Transportation 3,364.70 0.1 0.2 2.0 22.5 Real Estate 1,859.91 0.0 (0.0) (3.6) 17.6 Insurance 2,640.25 0.5 0.8 10.2 23.7 Telecoms 1,051.22 (0.2) (0.4) 4.0 27.9 Consumer 8,196.81 0.1 (0.1) 0.7 28.7 Al Rayan Islamic Index 4,610.95 0.4 0.4 8.0 19.8 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% HSBC Bank Oman Oman 0.11 3.8 20.0 19.8 Mabanee Co. Kuwait 0.75 3.4 2,028.0 21.0 Al Rajhi Bank Saudi Arabia 113.00 3.1 8,024.2 53.5 Industries Qatar Qatar 13.26 2.0 5,562.8 22.0 Bank Al-Jazira Saudi Arabia 18.92 1.9 9,952.2 38.5 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Ahli Bank Oman 0.11 (4.3) 17.2 (13.4) SABIC Agri-Nutrients Saudi Arabia 121.00 (3.4) 544.3 50.1 Jabal Omar Dev. Co. Saudi Arabia 34.35 (3.1) 2,232.3 18.0 National Industrialization Saudi Arabia 18.40 (2.4) 5,494.8 34.5 Sohar International Bank Oman 0.10 (2.0) 44.3 5.5 Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the S&P GCC Composite Large Mid Cap Index) QSE Top Losers Close* 1D% Vol. ‘000 YTD% INMA Holding 5.22 (1.5) 687.3 2.1 Qatari German Co for Med. Dev. 2.65 (1.2) 2,118.4 18.4 Dlala Brokerage & Inv. Holding Co 1.68 (1.1) 922.6 (6.4) Alijarah Holding 1.28 (0.9) 7,088.0 2.8 QLM Life & Medical Insurance Co 5.05 (0.9) 488.6 0.0 QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Industries Qatar 13.26 2.0 73,633.8 22.0 QNB Group 18.15 1.0 43,054.3 1.8 Mesaieed Petrochemical Holding 1.91 0.2 23,947.6 (6.6) Mazaya Qatar Real Estate Dev. 1.16 0.3 20,907.4 (8.4) Masraf Al Rayan 4.45 0.1 20,411.9 (1.8) Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 10,811.23 0.7 0.8 0.6 3.6 109.87 170,032.5 18.3 1.6 2.7 Dubai 2,868.02 0.9 0.9 2.5 15.1 85.00 106,882.0 21.8 1.0 2.8 Abu Dhabi 6,736.11 0.5 0.3 2.7 33.5 388.40 258,972.2 22.6 1.9 3.6 Saudi Arabia 10,913.56 0.1 1.1 3.4 25.6 4,057.47 2,599,383.6 35.8 2.4 1.8 Kuwait 6,360.95 0.5 0.9 2.4 14.7 244.86 120,318.8 40.5 1.6 2.0 Oman 4,033.78 (0.2) 0.1 4.7 10.2 9.18 18,094.6 14.2 0.8 3.9 Bahrain 1,560.87 0.5 1.0 2.2 4.8 2.04 23,908.0 26.8 1.0 2.1 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Market and Dubai Financial Market (** TTM; * Value traded ($ mn) do not include special trades, if any) 10,700 10,750 10,800 10,850 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 8 Qatar Market Commentary The QE Index rose 0.7% to close at 10,811.2. The Industrials and Banks & Financial Services indices led the gains. The index rose on the back of buying support from foreign shareholders despite selling pressure from Qatari, GCC and Arab shareholders. Qatar Cinema & Film Distribution and Industries Qatar were the top gainers, rising 2.4% and 2.0%, respectively. Among the top losers, INMA Holding fell 1.5%, while Qatari German Co. for Medical Devices was down 1.2%. Volume of shares traded on Monday fell by 3.8% to 134.7mn from 140.1mn on Sunday. Further, as compared to the 30-day moving average of 207.2mn, volume for the day was 35.0% lower. Mazaya Qatar Real Estate Dev. and Mesaieed Petrochemical Holding were the most active stocks, contributing 13.4% and 9.3% to the total volume, respectively. Source: Qatar Stock Exchange (*as a % of traded value) Ratings and Global Economic Data Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change The Commercial Bank Moody's Qatar BDR/BCA/ABCA/CR R/CRA A3/Prime-2/ba1/ ba1/A2-Prime-1/ A2(cr)/Prime-1(cr) A3/Prime-2/ba1/ ba1/A2-Prime-1/ A2(cr)/Prime-1(cr) – Stable – The Commercial Bank Fitch Qatar LT-IDR A A – Stable – Source: News reports, Bloomberg (* LT – Long Term, IDR – Issuer Default Rating, CRR – Counterparty Risk Ratings, BDR – Bank Deposit Ratings, CRA – Counterparty Risk Assessment, BCA – Baseline Credit Assessment, ABCA – Adjusted Baseline Credit Assessment) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 06/14 EU Eurostat Industrial Production SA MoM Apr 0.80% 0.40% 0.40% 06/14 EU Eurostat Industrial Production WDA YoY Apr 39.30% 37.40% 11.50% 06/14 Japan Ministry of Economy Trade and Industry Industrial Production MoM Apr F 2.90% – 2.50% 06/14 Japan Ministry of Economy Trade and Industry Industrial Production YoY Apr F 15.80% – 15.40% 06/14 India India Central Statistical Organisation CPI YoY May 6.30% 5.38% 4.29% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 34.18% 35.63% (5,908,560.3) Qatari Institutions 18.20% 33.85% (63,565,611.3) Qatari 52.38% 69.48% (69,474,171.6) GCC Individuals 0.47% 0.66% (808,911.4) GCC Institutions 3.49% 3.59% (398,412.9) GCC 3.95% 4.25% (1,207,324.3) Arab Individuals 11.98% 11.98% (1,468.7) Arab Institutions 0.00% 0.00% – Arab 11.98% 11.98% (1,468.7) Foreigners Individuals 4.50% 3.28% 4,940,215.6 Foreigners Institutions 27.19% 11.00% 65,742,749.0 Foreigners 31.69% 14.29% 70,682,964.6

- 3. Page 3 of 8 News Qatar Moody's affirms CBQK's ratings with a stable outlook, and places NBO's ratings on review for upgrade – Moody's Investors Service (Moody's) has today affirmed The Commercial Bank (CBQK)'s bank deposit ratings at A3/Prime-2 and maintained the stable outlook on the long-term ratings. At the same time the rating agency affirmed CBQK's ba1 Baseline Credit Assessment (BCA) and Adjusted BCA, its A2/Prime-1 Counterparty Risk Ratings (CRRs) and A2(cr)/Prime-1(cr) Counterparty Risk (CR) Assessment. Concurrently, the rating agency placed on review for upgrade National Bank of Oman SAOG (NBO)'s ba3 Adjusted BCA, Ba3 long-term deposit ratings, Ba3 senior unsecured ratings, Ba2 long-term local currency CRR and Ba2(cr) long-term CR Assessment. At the same time, the rating agency affirmed NBO's ba3 BCA, Ba2 long-term foreign currency CRR and all its short-term ratings and assessments at NP and NP(cr). Today's rating action follows CBQK's recent offer to the shareholders of NBO to acquire an additional 15.2% stake in NBO, which if successful would increase its shareholding in the bank to 50.1%. Following the potential increase in shareholding CBQK would consolidate NBO as a subsidiary. The offer period to the shareholders opened on 10 June 2021 and closes on 11 July 2021. (Moody’s, Bloomberg) Fitch Affirms CBQK; Places NBO on RWP on acquisition offer – Fitch Ratings has affirmed The Commercial Bank's (CBQK) Long-Term Issuer Default Rating (IDR) at 'A' with a Stable Outlook, and placed National Bank of Oman SOAG's (NBO) 'BB-' Long-Term IDR and '4' Support Rating (SR) on Rating Watch Positive (RWP). CBQK's and NBO's Viability Ratings (VR) are unaffected. A full list of rating actions is below. The rating action follows an offer by NBO's largest shareholder CBQK, on 3 June 2021, to acquire an additional 15.2% stake in NBO which, if successful, would increase its shareholding to 50.1%. The offer is expected to close on 11 July and is subject to CBQK obtaining necessary regulatory approvals in Oman and to a minimum acceptance level by NBO's shareholders. (Bloomberg) PSA: Qatar core inflation tops general CPI in May – Qatar's core inflation increased faster than the general consumer price index (CPI) inflation in May 2021 on both yearly and monthly basis, according to the official statistics. The CPI of May 2021 excluding “housing, water, electricity, gas and other fuels, surged 4.72% and 1.2% YoY and MoM, said the figures released by the Planning and Statistics Authority. Meanwhile, Qatar's cost of living, based on general CPI inflation, rose 2.47% YoY this May mainly on higher expenses towards transport, restaurants, communication and food. The country's CPI inflation was up 0.83% MoM in the review period, mainly owing to recreation, clothing and food sectors. The index of transport, which has a 14.59% weight, was seen shooting up 13.15% YoY, but declined 1.46% on monthly basis in May 2021. The sector has the direct linkage to the dismantling of the administered prices of petrol and diesel as part of the government measures to lower the subsidies. In May 2021, the price of super, premium gasoline and diesel witnessed 76.19%, 80% and 57.14% surge YoY respectively. However, on a monthly basis, the price of super was seen rising 2.78%; while that of premium and diesel declined 2.7% and 2.94% respectively. The index of restaurants and hotels, which has a 6.61% weight, soared 5.6% on a yearly basis but witnessed a 1.23% fall in May 2021. Communication, which carries a 5.23% weight, saw its group index unchanged on a monthly basis but saw a 4.3% jump YoY in the review period. Food and beverages, which has a weight of 13.45% in the CPI basket, witnessed 3.46% and 1.09% surge on yearly and monthly basis respectively in May 2021. Miscellaneous goods and services, with a 5.65% weight, saw its index jump 3.93% and 1.1% on yearly and monthly basis respectively in May 2021. Education, with a 5.78% weight, saw its index gain 3.72% YoY, but was down 0.06% MoM this May. In the case of furniture and household equipment, which has a 7.88% weight in the CPI basket, the index was up 3.27% and 0.09% respectively in May this year. The index of recreation and culture, with an 11.13% weight in the CPI basket, shot up 2.28% YoY despite a 10.97% surge MoM in May 2021. However, the index of housing, water, electricity and other fuels – with a weight of 21.17% in the CPI basket – saw 6.17% and 0.74% shrinkage on yearly and monthly basis respectively this May. The index of clothing and footwear, which has a 5.58% weight in the CPI basket, contracted 3.31% YoY despite 2.77% monthly increase in May 2021. The tobacco index, which has a 0.28% weight, was unchanged on yearly and monthly basis in the review period. (Gulf-Times.com) Qatar Chamber: Rise in trade shows Qatar’s economic recovery – Qatar’s economy has witnessed a remarkable recovery from the negative impacts of the COVID-19 pandemic, Qatar Chamber (QC) has said in its latest monthly report. According to QC’s monthly economic newsletter for May, Qatar’s economic status reached its pre-pandemic levels, where the private sector exports exceeded QR1.938bn. Qatar’s intervention to mitigate the effects of the pandemic on the economy through direct and indirect support led to a gradual recovery for the economy. Referring to Qatar’s foreign trade, the report said that Qatar saw a considerable growth of 61% to QR31bn in March 2021. The total exports of goods including exports of goods of domestic origin and re-exports amounted to around QR22.1bn in March, an increase of 7.3% compared to QR20.6bn in February. The imports of goods in March amounted to around QR8.9bn, an increase of 20.3% compared to QR7.4bn in February. Therefore, the country’s foreign merchandise trade balance, which represents the difference between total exports and imports showed a surplus of QR13.2bn. China was at the top of the countries of destination of Qatar’s foreign trade in March with about QR3.9bn, a share of 12.5% of the state’s total foreign trade. The volume of the private sector exports in March reached QR1.94bn, showing a MoM increase of 17.9% compared to QR1,644.5bn in February. On a YoY basis, it decreased by 0.3% compared to QR1,954bn in March 2020. “This increase demonstrated the ability of Qatar’s economy to overcome the repercussions of the COVID-19 pandemic and returning to pre- pandemic levels,” QC said. (Qatar Tribune) Qatari-Saudi Follow-up Committee holds its third meeting in Riyadh – The Qatari-Saudi Follow-up Committee held its third meeting at the Ministry of Foreign Affairs in Riyadh yesterday. The meeting was chaired on the Qatari side by HE the Special Envoy of the Minister of Foreign Affairs for Regional Affairs Ali bin Fahad Al-Hajri, and on the Saudi side by the Undersecretary of the Ministry of Foreign Affairs for Political and Economic Affairs Ambassador Eid Al-Thaqafi. The committee’s meetings come in implementation of the will of the two countries’ leaderships, and in accordance with what was included in Al-Ula Declaration, and to strengthen the bonds of the relationship between the two brotherly countries. (Gulf-Times.com)

- 4. Page 4 of 8 Qatar's F&B sector poised for strong recovery – Qatar’s retail and food and beverage (F&B) sectors are poised to have a strong recovery from the Covid-19 pandemic with the phased lifting of restrictions and allowing vaccinated nationals and residents from other GCC countries, according to Mall of Qatar General Manager Emile Sarkis. “There’s no doubt that it’s going to be very positive. I think Qatar would be the first country (in the region) to recover,” he told reporters on the sidelines of a recent event. The Ministry of Public Health (MoPH) had announced that “GCC citizens, their families and their household workers are allowed to enter the State of Qatar at any time, provided they follow the travel and return policy”. The MoPH added that “fully vaccinated GCC citizens who have received any of the Covid-19 vaccines recognized in Qatar with at least 14 days since the last dose and present an official vaccination card or certificate are exempted from quarantine". A detailed quarantine exemption criteria for individuals vaccinated against Covid-19 in GCC countries is posted on the ministry's website. (Gulf-Times.com) International NATO adopts tough line on China at Biden’s debut summit with alliance – NATO leaders warned on Monday that China presents “systemic challenges,” taking a forceful stance towards Beijing in a communique at Joe Biden’s first summit with an alliance that Donald Trump openly disparaged. The new US president has urged his fellow NATO leaders to stand up to China's authoritarianism and growing military might, a change of focus for an alliance created to defend Europe from the Soviet Union during the Cold War. The language in the summit's final communique, which will set the path for alliance policy, came a day after the Group of Seven (G7) rich nations issued a statement on human rights in China and Taiwan that Beijing said slandered its reputation. "China's stated ambitions and assertive behavior present systemic challenges to the rules-based international order and to areas relevant to alliance security," NATO leaders said in the communique. Biden also told European allies that the alliance's mutual defense pact was a "sacred obligation" for the US - a marked shift in tone from his predecessor, Trump, who had threatened to withdraw from the alliance and accused Europeans of contributing too little to their own defense. "I want all Europe to know that the US is there," said Biden. "NATO is critically important to us." Biden stopped at the NATO headquarters' memorial to the Sept. 11, 2001, attacks on the US by al Qaeda militants, when NATO triggered its Article 5 for the first and only time. Under the article, the alliance treats an attack on one member state as being an attack on all. Later at a news conference, Biden, who will meet Russian President Vladimir Putin on Wednesday in Geneva, said China and Russia were trying to split the transatlantic alliance and that, while he was not seeking conflict with Russia, NATO would respond if Moscow "continued its harmful activities". He described Putin as tough and bright. "Russia and China are both seeking to drive a wedge in our transatlantic solidarity," Biden said. He also pledged to support Ukraine in its conflict with Moscow, although he was non- committal on whether Kyiv could one day join NATO. "We are going to put Ukraine in a position that they will be able to maintain their physical security," Biden said, without giving more details. US Senate Republicans to discuss details of new infrastructure plan – US Senate Republicans are due to hear details on Tuesday about a bipartisan proposal to revitalize America’s roads and bridges, which lawmakers believe could win support from the caucus as a part of President Joe Biden’s sweeping infrastructure plan. Members of a bipartisan Senate group will discuss the proposal with Republican senators at their weekly policy lunch, Republican lawmakers and aides said on Monday evening. “We’ll be discussing it,” Senator Bill Cassidy, a member of the group, told reporters. “It won’t be a formal sort of ‘OK - now we need your vote.’ It’ll be more kind of ‘OK - here’s more information for you.’” The bloc of Senate moderates, five Republicans and five Democrats, said last Thursday that it had reached an agreement after negotiations between Republican Senator Shelley Moore Capito and Biden broke down. It proposes to spend $974bn over five years, or $1.2tn over eight years, a source familiar with the package said. That is below Biden’s current $1.7tn proposal and it is unclear whether it can gather enough support to pass the 50-50 Senate. Senator John Thune, the chamber’s No. 2 Republican, told reporters that he expects Republican support for the proposal. “I don’t know how many Democrats they can get for something like what they’re talking about. But I think there would be substantial Republican support,” he said. “It’s good work.” Senator Dick Durbin, the chamber’s No. 2 Democrat, said he had urged senators to “get this moving.” He said any bipartisan deal, as well a separate measure Democrats are eyeing to try to pass their remaining infrastructure priorities without Republican support, would need to get in shape by the end of June because of a tight floor schedule. Biden has set his sights on infrastructure legislation that would both revamp the nation’s roads and bridges as well as boost spending on services including healthcare and childcare - although Republicans reject the idea that those latter priorities even qualify for the label “infrastructure.” The bipartisan plan unveiled last week sticks to spending on physical infrastructure like roads and bridges, members have said. House of Representatives Speaker Nancy Pelosi, a Democrat, expressed some skepticism about it on Sunday, saying it would be a hard sell to her party unless Democrats can be assured that there is “more to come.” UK shopper numbers dip 6.7% last week after strong previous week – Shopper numbers across Britain fell 6.7% in the week to June 12 compared with the previous week, which had been boosted by a school holiday and improved weather, researcher Springboard said on Monday. It said shopper numbers, or footfall, fell 9.0% on high streets week-on-week, by 7.5% in shopping centres and by 0.9% in retail parks. "UK retail destinations suffered post Bank Holiday blues last week, with footfall dropping back by around half of the uplift recorded in the week before, when the school half-term holiday coincided with the Spring bank holiday and amazing weather," said Diane Wehrle, Springboard's insights director. Overall UK footfall increased 11.6% in the week to June 5. Springboard said week to June 12 footfall was down 18.4% compared with the same week in 2019, before the pandemic started to disrupt traffic. Non-essential stores reopened in England and Wales on April 12 after more than three months of COVID-19 lockdowns. They reopened in Scotland on April 26 and Northern Ireland on April 30. Indoor hospitality was allowed from May 17. However, British Prime Minister Boris Johnson is expected to announce on Monday that the end of further restrictions will be delayed by several weeks following concerns about a rapid rise of Delta variant infections. read more Springboard said that with the removal of restrictions set to be delayed by as much as a month, footfall is not likely to strengthen significantly over the next four weeks. Lagarde: Eurozone economy on right path but too early to debate end of ECB help – The Eurozone economy is on the right path but the recovery must be firm and sustainable before the European Central Bank can debate clawing back emergency support, ECB President Christine Lagarde told Politico in an interview. “I am not suggesting that the pandemic emergency purchase program (PEPP) is going to stop on 31 March,” Lagarde was quoted on Monday as saying. “We have plenty of flexibility, but in terms of economic outlook we are heading in the right direction. “It is far too early to debate these issues,” she said about the 1.85tn euro PEPP that is scheduled to last at least until March 31 or until the crisis phase of the pandemic is over.

- 5. Page 5 of 8 Eurozone production stronger than expected in April – Eurozone industrial production was stronger than expected in April, driven by a more than doubling of durable consumer goods output from a year earlier as economies steadily reopened after COVID-19 pandemic lockdowns, data showed on Monday. The European Union’s statistics office Eurostat said industrial output in the 19 countries sharing the euro rose 0.8% month-on-month for a 39.3% YoY surge. Economists polled by Reuters had expected a 0.4% monthly and a 37.4% annual jump. The biggest production gain in April against March was in durable consumer goods, where output rose 3.4% after 1.2% monthly declines in both February and March. In YoY terms, the gain in durable consumer goods output was a spectacular 117.3% after a 34.5% annual rise in March, with capital goods also surging 65.4% year- on-year and intermediate goods up 38.7%. French central bank sees stronger-than-expected rebound – France’s economy is set to grow faster than expected as a rebound gains momentum from the second half of the year, the French central bank forecast on Monday. The economy was poised to grow 5.8% this year, well above the euro’s zone average of 4.6%, the Bank of France said, revising its forecast up by 0.4 percentage points from its last estimate in March. The euro zone’s second-biggest economy was then on course to grow 4.1% in 2022 and 2.1% in 2023, up by 0.3 and 0.4 percentage points respectively from March, the central bank said in its quarterly economic outlook. It said its monthly business surveys showed activity picking up already in the three months to the end of June, with quarterly growth expected at 0.5% from the previous quarter. As coronavirus restrictions are gradually lifted and a vaccination campaign gains further momentum, activity was seen accelerating even more in the second half of the year. The economy would get back to pre-crisis levels of activity from the start of next year - earlier than previously expected - as a burst of consumer spending and business investment fueled the recovery. The central bank said households would start tapping into the extra savings built up under coronavirus restrictions that forced many retail outlets to close for months and which were expected to peak at 7% of gross domestic product by year-end. Business investment was already seen topping out at record levels this year, as firms profit margins improved while companies benefited from new tax breaks under the government’s 100bn euro recovery plan. Bank of Spain sees 2.2% second-quarter growth, ups longer- term outlook – Spain’s economy is likely to grow 2.2% in the second quarter from the January-March period, when it shrank 0.5%, thanks to rising internal demand unleashed by looser COVID-19 restrictions and rising vaccination rates, the central bank said on Monday. After a record 10.8% slump last year, the central bank expects gross domestic product to expand between 4.6% and 6.8% this year, with its central scenario pointing to 6.2% growth, up from 6% in its previous outlook released in March. It also raised its forecasts to 5.8% for next year, from 5.3% previously, and to 1.8% for 2023, from 1.7%. In the second quarter, its quarter-on-quarter growth forecast ranges from 1.4% to 2.7%. “This upturn in activity has intensified markedly in the course of the second quarter of the year, in line with the more favorable evolution of the pandemic,” the Bank of Spain said in its report, though it added that uncertainty was still high. It also predicted a services and consumption-driven recovery, thanks in part to savings accumulated by Spanish households, to be buoyed by a gradual recovery of the labor market and the implementation of EU-funded business projects. Still, with international travel likely to remain subdued amid concerns over more contagious COVID-19 variants, the bank does not expect Spain’s tourism-dependent economy to reach pre-pandemic levels until the end of 2022. Chief Economist Oscar Arce warned this summer would be far from normal in terms of tourist numbers and expenditure, and pushed back a forecast for international arrivals to recover pre-pandemic levels to 2023 from 2022. Central bank: Dutch economy to rebound faster from COVID slump than expected – Economic growth in the Netherlands will rebound faster from the coronavirus slump than previously expected, as consumers start spending pent up savings and international trade continues to recover, the Dutch central bank (DNB) said on Monday. The euro zone’s fifth largest economy is set to grow 3% this year and 3.7% in 2022, the DNB said, following a contraction of 3.7% last year due to the pandemic. Growth is expected to slow to 1.9% in 2023. The central bank, which late last year predicted growth of 2.9% for both 2021 and 2022, said the economy would be back to its pre-coronavirus level at the end of this year. “The recession is less severe than expected”, DNB director Olaf Sleijpen told reporters. “Consumers and companies have adapted pretty well to the pandemic, and international trade remained much stronger than expected.” Growth has resumed in the second quarter, the bank said, following a short recession caused by the coronavirus lockdown due to which bars, restaurants and many stores were closed from October. The lockdown has been gradually eased in recent weeks, as the roll out of vaccinations significantly lowered the infection rate. Bars and restaurants have reopened and restrictions for non-essential stores have been lifted. The central bank said the government had successfully helped companies survive the health crisis with lavish support schemes, but should try to phase out support in the coming quarter. “It’s now time to deal with structural problems, such as the energy transition, the housing market and labour market reforms”, Sleijpen said. Despite heavy spending on coronavirus support, Dutch government finances leave room for investments, DNB said. Government debt is expected to peak around 60% of gross domestic product (GDP) next year, while the government’s deficit is set to shrink significantly as the economy recovers. Ex-c.banker Sakurai: BOJ likely to extend pandemic-aid scheme this week – The Bank of Japan is likely to extend a September deadline for its pandemic-relief program at this week's policy meeting, former BOJ board member Makoto Sakurai said. In an interview with Reuters conducted on Monday, Sakurai also said it was "too early" to take further steps to revitalize the Japanese government bond (JGB) market made dormant by the central bank's huge presence. In a policy review in March, the BOJ clarified that it would allow 10-year JGB yields to move 50 basis points around its 0% target in the hope of boosting market trading. But trading volume in the JGB market dwindled to a near- two-decade low in May, prompting some calls for the BOJ to take more steps to revitalize the market such as trimming its bond purchases. The BOJ meets for a two-day rate review ending on Friday. Survey: Brazil 2021 inflation, GDP and interest rate forecasts surge to new highs – Forecasts for Brazilian growth, inflation and interest rates in 2021 hit new highs, a survey of economists showed on Monday, with the central bank now seen tightening policy much faster as inflation sails above the upper limit of its target range. The median forecast for 2021 inflation from more than 100 economists in the central bank’s weekly FOCUS survey jumped to 5.8% from 5.4%, more than two percentage points above the bank’s year-end goal of 3.75% and well above the 5.25% upper limit of its wider range. Following the release of stronger-than-expected first quarter gross domestic product growth figures earlier this month, the median 2021 growth forecast jumped to a new high of 4.9% from 4.4%, the survey showed. Just over a month ago that stood at 3.2%. These findings marked the 10th consecutive rise in the inflation outlook, and the eighth rise in growth forecasts. The central bank is widely

- 6. Page 6 of 8 expected to raise its benchmark Selic rate by 75 basis points on Wednesday for a third time, to 4.25%, and perhaps drop its commitment to only a “partial” normalization of policy. The FOCUS survey on Monday showed that economists’ year-end Selic median forecast jumped to 6.25% from 5.75% a week ago. Four weeks ago it stood at 5.50%. This shows economists now believe the central bank will raise the Selic towards the so-called ‘neutral’ rate, widely considered to be around 6.00%-6.50%, much earlier than previously thought. Next year’s median forecast held steady at 6.50%. Central bank chief Roberto Campos Neto said recently that the bank is “100% committed” to meeting its inflation goals. India’s May retail inflation picks up to 6.30% y/y, highest in six months – India’s retail inflation accelerated in May, at its fastest pace in six months as fuel and food prices rose at a higher pace, putting pressure on the central bank to tame prices amid a faltering economic recovery. The Reserve Bank of India earlier this month warned that high energy prices could stoke inflation while cutting the growth forecast to 9.5% from 10.5% for the current fiscal year beginning April. Annual retail inflation (INCPIY=ECI) rose 6.30% year-on-year, up from 4.29% in April. Analysts had forecast retail inflation at 5.30%, according to a Reuters poll. Economists fear a rise in prices after the second wave of coronavirus hit the economy while killing tens of thousands of people since April. "We expect the CPI (consumer price inflation) prints to remain above 5% until September driving the annual average CPI to 5.2% for current fiscal year," said Garima Kapoor, economist institutional securities, Elara Capital, Mumbai. She said the central bank could tolerate high inflation close to the upper end of its 2-6% target band as the recovery from the second wave was likely to be more gradual and subdued than the first wave. Food prices, which account for nearly half of the Ministry of Statistics' inflation basket, rose 5.01% YoY from 3.15% in the previous month. A global recovery has led to a rally in commodity prices including crude prices. Brent crude futures have risen to over $72 a barrel from a low closing price of $19.33 in March 2020. In India fuel prices have risen by over 30% from May of last year. High energy and commodity prices are also raising input costs for companies in India pushing wholesale price inflation to at least a 15 year high of 12.94% year-on-year in May, according to Refinitiv data. May core inflation, excluding food and fuel costs, was estimated in the range of 6.54% to 6.56% by three economists, after the data release. India does not release core inflation numbers. Regional Saudi first quarter GDP shrinks 3%, hit by oil sector decline – Saudi Arabia’s GDP fell 3% in the first quarter, slightly less than official estimates and compared with a 1% contraction last year, as a sharp fall in the oil sector pulled back the economy, data showed. The Kingdom’s economy has been hit hard by the twin shock of last year’s historic oil price crash and the COVID-19 pandemic. The non-oil sector grew 2.9%, from 1.6% growth a year earlier, while the oil sector declined by 11.7% which was a much sharper fall than the 4.6% contraction a year earlier, the General Authority for Statistics said in a statement on Monday. In flash estimates in May the authority said the economy shrank 3.3% in the first quarter and the non-oil sector grew for the first since the first quarter of 2020. The non-oil and private sectors are at the center of Vision 2030, de facto ruler Crown Prince, Mohammed bin Salman’s transformation plan to wean the Saudi economy off oil. Real GDP, an inflation-adjusted measure, shrank 4.1% last year. The International Monetary Fund expects the Saudi economy to grow 2.1% this year. Saudi Arabia’s private sector expanded by 4.4% in the first quarter and the government sector declined slightly, by 0.4%, the official data showed. On a quarterly basis, real GDP declined by 0.5%, mainly due to an 8.7% drop in the oil sector, while the non-oil sector expanded by 4.9% compared to the fourth quarter, driven by a 6.3% private sector expansion as well as 1.7% growth in the government sector. (Reuters) ACWA Power raises SR2.8bn via Sukuk issuance – ACWA Power raises SR2.8bn via Sukuk issuance. The funds raised through a senior, unsecured floating Sukuk rate issuance with a 7-year tenor. The price guidance 100 basis points p/yr SAIBOR. Issuance marks company’s entry into Saudi debt capital markets. Fund managers, government funds and insurance cos accounted for approximately 30% of issuance. Over-subscription was 1.8 times issue size. HSBC Saudi Arabia and Samba Capital acted as joint lead managers and book-runners. (Bloomberg) Dubai plane leasing firm DAE adds more banks to bond deal – Dubai Aerospace Enterprise (DAE), one of the world's biggest aircraft leasing companies, has added more banks to its planned sale of US dollar-denominated bonds that would be its second this year, an investor presentation seen by Reuters showed. DAE, owned by the Dubai government's main investment arm the Investment Corporation of Dubai, will issue bonds in tranches of three- and/or seven years to exercise a call option on bonds due next year and 2024, the presentation showed on Monday. It will also use the proceeds from the new bonds for general corporate purposes. The bonds will be of benchmark size, which generally means at least $500mn. A document from one of the banks on the deal seen by Reuters on Friday did not specify a tenor and said DAE hired BNP Paribas, Credit Agricole, Emirates NBD Capital, JPMorgan and Trust Securities to organize fixed income investor calls on Monday. (Reuters) Dubai Islamic Bank hires banks for five-year dollar Sukuk – Dubai Islamic Bank (DIB) has hired banks to arrange an offering of US dollar-denominated five-year sukuk, or Islamic bonds, a document showed on Monday. Bank ABC, Dubai Islamic Bank, Emirates NBD Capital, First Abu Dhabi Bank, HSBC, KFH Capital, Standard Chartered and the Islamic Corporation for the Development of the Private Sector will arrange fixed income investor calls starting on Monday, the document from one of the banks showed. (Zawya) Nakheel sells business that supplies chilled air – Dubai state developer Nakheel sold its business that supplies chilled air to such local landmarks as artificial palm-shaped islands, according to sources. Emirates Central Cooling Systems Corp, a joint venture between a unit of Dubai Holding and a state-owned utility, has acquired Nakheel’s cooling operations, the sources said. The assets are worth around AED1bn, sources added. Coming off years of declines in property prices, some developers in the UAE have looked to offload their cooling operations, especially after the coronavirus pandemic further upended the local economy. (Bloomberg) Malabar Investments joins Nasdaq Dubai private market – Malabar Investments’ shares have been registered with Nasdaq Dubai’s Central Securities Depository and will be traded through Emirates NBD Securities. Trading will take place off-exchange as the company remains privately held. Malabar Investments is the international investment arm of Malabar Gold & Diamonds. (Bloomberg) ADIA reviews real estate strategy as pandemic bites – The Abu Dhabi Investment Authority (ADIA), one of the world’s largest property investors, is considering changes to its real estate strategy during the coronavirus pandemic after some of its key holdings, sources said. Sovereign Wealth Fund is reviewing the asset performance of its assets following weakness in several shopping malls and office buildings in its portfolio, according to people who asked anonymity as the information is private. ADIA may consider reducing its exposure to some troubled

- 7. Page 7 of 8 investments, the people said. ADIA has moved in recent years to make more direct asset investments and rely less on outside managers. According to estimates from data provider Global SWF, the state-owned investor has amassed less than $700bn in assets, and the ADIA states that real estate traditionally accounts for about 5% to 10% of that overall portfolio. While ADIA will continue to be a major player in property, it may shift its focus to future deals and increase exposure in areas such as warehouses, life science properties, technology hubs and affordable housing, sources said. (Bloomberg) Abu Dhabi fund bets on airplane leasing amid downturn – An Abu Dhabi fund is backing a startup aircraft leasing company run by former Ryanair Chief Financial Officer, Howard Millar to build a fleet of 100 jets over the next three years. Abu Dhabi Catalyst Partners, part-owned by Abu Dhabi sovereign wealth fund Mubadala, is an anchor investor in Sirius Aviation, which is headquartered in the Emirate. Millar, who left Ryanair in 2014 after 23 years, told Reuters Abu Dhabi Catalyst Partners invested $100mn in Sirius, which has joint ventures with US investment firms Corrum Capital and HPS Investment Partners. Sirius, established in March 2020, on Monday announced it had acquired its first 10 jets. (Reuters) Abu Dhabi exchange lists Etisalat's dual-tranche euro bonds – The Abu Dhabi Securities Exchange (ADX) said Monday it has listed the EUR1bn in dual-tranche bonds issued by UAE telecoms operator Etisalat. The issuance, which was more than six times oversubscribed, has been listed in two equal tranches maturing in 2028 and 2033, ADX said in a statement. The first EUR500mn in seven-year notes are set to mature on May 17, 2028 and carry a 0.375% coupon. The second tranche of EUR500mn will mature on May 17, 2033 and carry a 0.875% coupon. (Zawya) National Bank of Oman’s outlook revised to Stable by Moody's – National Bank of Oman's outlook has been revised to Stable from Negative by Moody's. (Bloomberg) Oman sells OMR218.4mn 28-day bills at yield of 0.637% – Oman sold OMR218.4mn of 28-day bills due on July 14. The bills were sold at a price of 99.951, have a yield of 0.637% and will settle on June 16. (Bloomberg) Bank ABC, FAB arrange $250mn Syndicated loan for Bank Dhofar – Bank ABC and First Abu Dhabi Bank (FAB) acted as joint coordinators, underwriters, initial mandated lead arrangers and bookrunners on the two-year syndicated term loan facility. The syndication was launched in May and was over 2x oversubscribed. Total of 9 banks (excluding the joint coordinators) from the GCC, Europe and Asia participated in the facility. Abu Dhabi Commercial Bank, Al Ahli Bank of Kuwait, Bank of Baroda, Doha Bank, State Bank of India joined as mandated lead arrangers. Commercial Bank of Dubai joined as lead arranger. Banque Du Caire, HSBC Bank Middle East and Mashreqbank joined as arranger. The facility will be utilized to refinance its $250mn facility dated June 13, 2018. (Bloomberg) Fitch affirms GFH at 'B'; with a Stable outlook – Fitch Ratings has affirmed GFH Financial Group (GFH) Long- and Short-Term Issuer Default Ratings (IDR) at 'B'. The Outlook on the Long-Term IDR is Stable. Fitch has also affirmed the 'B'/'RR4' senior unsecured long-term rating of the $500mn 2025 certificates issued through GFH Sukuk Company Limited (GFH SCL). GFH SCL is a special-purpose vehicle, incorporated in the Cayman Islands as a trust for charitable purposes, with its share capital held by Walkers Fiduciary Limited. GFH SCL was established solely to issue certificates (Sukuk). GFH is a Bahrain-domiciled Shari’ah-compliant financial institution focusing on investment banking, real-estate and infrastructure investments, asset management, treasury activities and, via its majority-owned subsidiary Khaleeji Commercial Bank (KHCB), commercial and retail banking in Bahrain. The IDRs of GFH primarily reflect real- estate concentrations in its investment portfolio, its dependence on transactional gains for a significant share of its profitability and its fast-growing treasury activities. The ratings also consider GFH's resilient performance since the onset of the pandemic, improved funding access (as evident in its Sukuk issuance in early 2020) and management's strategic objective of reshaping the company's business model towards more stable and recurring revenue sources, such as fee generation and lower-risk, lower- return investments. GFH's primary operating region is Bahrain (B+/Stable), where the company is incorporated and operates under an Islamic wholesale investment-banking license issued by the Central Bank of Bahrain (CBB). It is listed on the Bahrain, Kuwait and Dubai Financial Market Stock Exchanges. GFH's key business activities are commercial banking via the Shari’ah- compliant banking subsidiary KHCB, real-estate investments, investment- banking and treasury activities. Bahrain's sovereign rating does not cap GFH's Long-Term IDR at its current level. However, the operating environment still exerts an influence on GFH's prospects, both in relation to the company's own domestic investments and via the domestic-banking activities of KHCB. KHCB is a significant contributor to GFH's revenue (around 20% in 2020) and net profit, mainly through the provision of Islamic- financing products, and provides a source of more stable deposit funding to the group. Following a balance sheet clean-up exercise in recent years KHCB's asset quality has been improving but is still weak and lags higher-rated peers.' (Bloomberg) Bahrain sells BHD43mn 91-day Islamic Sukuk; bid-cover at 5.13x – Bahrain sold BHD43mn of 91-day Islamic Sukuk due on September 15. Investors offered to buy 5.13 times the amount of securities sold. The Sukuk will settle on June 16. (Bloomberg)

- 8. Contacts QNB Financial Services Co. W.L.L. Contact Center: (+974) 4476 6666 info@qnbfs.com.qa Doha, Qatar Saugata Sarkar, CFA, CAIA Shahan Keushgerian Mehmet Aksoy, PhD Head of Research Senior Research Analyst Senior Research Analyst saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa mehmet.aksoy@qnbfs.com.qa Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 8 of 8 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns, # Market was closed on June 14, 2021) 60.0 80.0 100.0 120.0 140.0 160.0 May-17 May-18 May-19 May-20 May-21 QSE Index S&PPan Arab S&PGCC 0.1% 0.7% 0.5% 0.5% (0.2%) 0.5% 0.9% (0.5%) 0.0% 0.5% 1.0% Saudi Arabia Qatar Kuwait Bahrain Oman Abu Dhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,866.18 (0.6) (0.6) (1.7) MSCI World Index 3,019.88 0.2 0.2 12.3 Silver/Ounce 27.86 (0.2) (0.2) 5.5 DJ Industrial 34,393.75 (0.2) (0.2) 12.4 Crude Oil (Brent)/Barrel (FM Future) 72.86 0.2 0.2 40.7 S&P 500 4,255.15 0.2 0.2 13.3 Crude Oil (WTI)/Barrel (FM Future) 70.88 (0.0) (0.0) 46.1 NASDAQ 100 14,174.14 0.7 0.7 10.0 Natural Gas (Henry Hub)/MMBtu 3.24 0.0 0.0 36.1 STOXX 600 458.32 0.4 0.4 13.9 LPG Propane (Arab Gulf)/Ton 94.50 (0.5) (0.5) 25.6 DAX 15,673.64 0.1 0.1 12.7 LPG Butane (Arab Gulf)/Ton 99.88 (0.6) (0.6) 43.7 FTSE 100 7,146.68 0.2 0.2 14.4 Euro 1.21 0.1 0.1 (0.8) CAC 40 6,616.35 0.4 0.4 18.2 Yen 110.07 0.4 0.4 6.6 Nikkei 29,161.80 0.4 0.4 (0.3) GBP 1.41 0.0 0.0 3.2 MSCI EM 1,383.19 0.1 0.1 7.1 CHF 1.11 (0.2) (0.2) (1.6) SHANGHAI SE Composite# 3,589.75 - - 5.4 AUD 0.77 0.1 0.1 0.2 HANG SENG# 28,842.13 - - 5.8 USD Index 90.52 (0.0) (0.0) 0.7 BSE SENSEX 52,551.53 0.3 0.3 9.9 RUB 72.10 0.0 0.0 (3.1) Bovespa 130,208.00 1.8 1.8 11.8 BRL 0.20 1.1 1.1 2.6 RTS 1,687.37 0.5 0.5 21.6 143.7 138.1 106.9