VVIP Pune Call Girls Katraj (7001035870) Pune Escorts Nearby with Complete Sa...

8 June Daily market report

1. Page 1 of 5

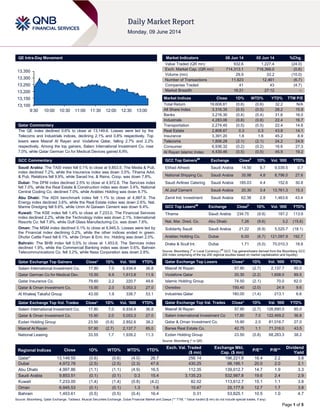

QE Intra-Day Movement

Qatar Commentary

The QE index declined 0.6% to close at 13,149.6. Losses were led by the

Telecoms and Industrials indices, declining 2.1% and 0.8% respectively. Top

losers were Masraf Al Rayan and Vodafone Qatar, falling 2.7% and 2.2%

respectively. Among the top gainers, Salam International Investment Co. rose

7.0%, while Qatar German Co for Medical Devices gained 6.9%.

GCC Commentary

Saudi Arabia: The TASI index fell 0.1% to close at 9,853.5. The Media & Pub.

index declined 7.2%, while the Insurance index was down 3.5%. Tihama Advt.

& Pub. Relations fell 9.9%, while Sanad Ins. & Reins. Coop. was down 7.8%.

Dubai: The DFM index declined 2.5% to close at 4,972.8. The Services index

fell 7.0%, while the Real Estate & Construction index was down 3.4%. National

Central Cooling Co. declined 7.0%, while Arabtec Holding was down 6.7%.

Abu Dhabi: The ADX benchmark index fell 1.1% to close at 4,997.9. The

Energy index declined 3.6%, while the Real Estate index was down 2.6%. Nat.

Marine Dredging fell 9.6%, while Umm Al Qaiwain Cement was down 9.4%.

Kuwait: The KSE index fell 1.4% to close at 7,233.0. The Financial Services

index declined 2.2%, while the Technology index was down 2.1%. International

Resorts Co. fell 7.8%, while Gulf Glass Manufacturing Co. was down 7.6%.

Oman: The MSM index declined 0.1% to close at 6,945.5. Losses were led by

the Financial index declining 0.2%, while the other indices ended in green.

Dhofar Cattle Feed fell 6.1%, while Oman & Emi. Inv. Holding was down 2.0%.

Bahrain: The BHB index fell 0.5% to close at 1,453.6. The Services index

declined 1.9%, while the Commercial Banking index was down 0.6%. Bahrain

Telecommunications Co. fell 3.2%, while Nass Corporation was down 2.8%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Salam International Investment Co. 17.80 7.0 6,934.4 36.8

Qatar German Co for Medical Dev. 15.50 6.9 1,613.8 11.9

Qatar Insurance Co. 79.60 2.2 220.7 49.6

Qatar & Oman Investment Co. 15.90 2.0 5,053.3 27.0

Al Khaleej Takaful Group 43.00 1.9 338.7 53.1

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Salam International Investment Co. 17.80 7.0 6,934.4 36.8

Qatar & Oman Investment Co. 15.90 2.0 5,053.3 27.0

Ezdan Holding Group 23.50 (0.8) 2,852.6 38.2

Masraf Al Rayan 57.90 (2.7) 2,137.7 85.0

National Leasing 33.55 1.7 1,939.2 11.3

Market Indicators 08 Jun 14 05 Jun 14 %Chg.

Value Traded (QR mn) 932.6 1,227.4 (24.0)

Exch. Market Cap. (QR mn) 714,313.1 718,366.0 (0.6)

Volume (mn) 29.9 33.2 (10.0)

Number of Transactions 11,623 12,461 (6.7)

Companies Traded 41 43 (4.7)

Market Breadth 16:21 27:12 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 19,608.81 (0.6) (0.6) 32.2 N/A

All Share Index 3,316.35 (0.5) (0.5) 28.2 15.9

Banks 3,216.30 (0.4) (0.4) 31.6 16.0

Industrials 4,283.06 (0.8) (0.8) 22.4 16.7

Transportation 2,274.45 (0.5) (0.5) 22.4 14.6

Real Estate 2,808.67 0.3 0.3 43.8 14.1

Insurance 3,391.20 1.6 1.6 45.2 8.9

Telecoms 1,806.28 (2.1) (2.1) 24.2 24.9

Consumer 6,936.32 (0.2) (0.2) 16.6 27.3

Al Rayan Islamic Index 4,430.46 (0.5) (0.5) 45.9 19.2

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Etihad Atheeb Saudi Arabia 14.50 9.7 9,039.5 0.7

National Shipping Co. Saudi Arabia 35.98 4.8 8,796.0 27.6

Saudi Airlines Catering Saudi Arabia 185.03 4.4 152.6 30.8

Al Jouf Cement Saudi Arabia 20.30 3.4 13,761.3 15.3

Zamil Ind. Investment Saudi Arabia 62.38 2.8 1,463.6 43.4

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Tihama Saudi Arabia 234.75 (9.9) 187.2 113.9

Nat. Mar. Dred. Co. Abu Dhabi 7.26 (9.6) 3.2 (15.6)

Solidarity Saudi Saudi Arabia 21.22 (6.9) 5,525.7 (18.1)

Arabtec Holding Co. Dubai 6.00 (6.7) 121,097.9 192.7

Drake & Scull Int. Dubai 1.71 (5.0) 70,010.3 18.8

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Masraf Al Rayan 57.90 (2.7) 2,137.7 85.0

Vodafone Qatar 20.30 (2.2) 1,608.0 89.5

Islamic Holding Group 74.50 (2.1) 70.0 62.0

Ooredoo 150.40 (2.0) 24.9 9.6

Industries Qatar 180.00 (1.4) 213.1 6.6

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Masraf Al Rayan 57.90 (2.7) 126,890.5 85.0

Salam International Investment Co 17.80 7.0 122,469.2 36.8

Qatar & Oman Investment Co. 15.90 2.0 81,016.7 27.0

Barwa Real Estate Co. 42.75 1.1 71,316.0 43.5

Ezdan Holding Group 23.50 (0.8) 68,283.3 38.2

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 13,149.55 (0.6) (0.6) (4.0) 26.7 256.14 196,221.8 16.4 2.2 3.8

Dubai 4,972.78 (2.5) (2.5) (2.3) 47.6 430.25 98,186.1 20.0 2.0 2.1

Abu Dhabi 4,997.86 (1.1) (1.1) (4.9) 16.5 112.35 139,012.7 14.7 1.9 3.3

Saudi Arabia 9,853.51 (0.1) (0.1) 0.3 15.4 3,135.23 532,987.8 19.6 2.4 2.9

Kuwait 7,233.00 (1.4) (1.4) (0.8) (4.2) 82.02 113,612.7 15.1 1.1 3.8

Oman 6,945.53 (0.1) (0.1) 1.3 1.6 10.47 25,177.9 12.7 1.7 3.8

Bahrain 1,453.61 (0.5) (0.5) (0.4) 16.4 0.31 53,825.1 10.5 1.0 4.7

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

13,100

13,150

13,200

13,250

13,300

13,350

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 5

Qatar Market Commentary

The QE index declined 0.6% to close at 13,149.6. The Telecoms

and Industrials indices led the losses. The index fell on the back

of selling pressure from Qatari shareholders despite buying

support from non-Qatari shareholders.

Masraf Al Rayan and Vodafone Qatar were the top losers, falling

2.7% and 2.2% respectively. Among the top gainers, Salam

International Investment Co. rose 7.0%, while Qatar German Co.

for Medical Devices gained 6.9%.

Volume of shares traded on Sunday fell by 10.0% to 29.9mn

from 33.2mn on Thursday. However, as compared to the 30-day

moving average of 27.9mn, volume for the day was 7.1% higher.

Salam International Investment Co. and Qatar & Oman

Investment Co. were the most active stocks, contributing 23.2%

and 16.9% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

The Saudi

Investment Bank

(SAIB)

CI

Saudi

Arabia

FSR/LT FCR/ST FCR A-/A/A2 A-/A/A2 – Positive –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC

– Local Currency)

News

Qatar

Barwa Bank client base exceeds 14,000 in 2013 – According

to Barwa Bank’s Chairman Sheikh Mohamed bin Hamad bin

Jassim al-Thani, the bank’s client base exceeded 14,000 in

2013. He said that the banking group generated revenue

through more balanced streams and quality based earnings.

Business income of the banking group was driven by the quality

of the financing portfolio, additionally enhanced by the

outstanding performance of the Treasury and Investment

Division. The bank reinforced its presence and services in the

retail sector through its unique structure and network of

branches in Doha. (Gulf-Times.com)

Ooredoo awarded Best Islamic Borrower – Ooredoo was

awarded "Best Islamic Borrower" at the annual EMEA Finance

Achievements Awards in London recently. Ooredoo won the

award for a variety of new activities undertaken in the Islamic

financing markets. It started with Ooredoo's first Commodity

Murabaha transaction in November 2012 and this was followed

by Ooredoo's inaugural $1.25bn sukuk in December 2013.

(Gulf-Times)

QA to launch non-stop flights to Zagreb – Qatar Airways

(QA) has announced to offer non-stop flights from Doha to

Zagreb three times weekly from October 1, 2014. The new route

will increase seats to 240 business class and 2,640 Economy

class seats per week, an increase of 72 and 384 seats

respectively. QA will continue to fly the A320 aircraft direct to

and from the Croatian capital. (Bloomberg)

Qatar reveals largest solar-power generating facility – Qatar

Solar Energy (QSE) has unveiled a first-of-its-kind solar panel

factory in the region with a capability to generate 300 megawatts

of energy a year. QSE also announced a three-phase plan to

eventually produce 2.5 gigawatts of solar energy annually.

(Bloomberg)

QInvest wins Qatar’s Best Investment Bank award –

Investment bank, QInvest has been awarded as the “Best

Investment Bank” in Qatar at the Euromoney Awards for

Excellence 2014. This marked the third year in a row that

QInvest received the award. (GulfBase.com)

International

Obama to issue order to ease student loan pressures – A

White House official said that US President Barack Obama will

issue an executive action on Monday aimed at making it easier

for young people to repay student loans. The president will sign

an order directing the Secretary of Education to ensure that

more students who borrowed federal direct loans be allowed to

cap their loan payments at 10% of their monthly incomes. The

official said the Federal law currently allows most students to do

this already. The president's order will extend this ability to

students who borrowed before October 2007 or those who have

not borrowed since October 2011. The administration says this

action will help up to 5mn more borrowers, although it will not be

available until December 2015. Faced with a Republican

majority in the House of Representatives that makes legislation

out of reach for most of his policy proposals, Obama has turned

to issuing executive orders to accomplish his agenda. (Reuters)

IMF admits underestimating the rally in UK economy – The

International Monetary Fund (IMF) Managing Director Christine

Lagarde stated that it underestimated the strength of the UK

economy when warning against the government’s austerity

program. Lagarde said the UK economic outlook was now more

sustainable as investment joins consumption as an engine. She

reiterated that the strength of the UK housing market remains a

threat, although its rise was multi-faceted rather than an outright

boom. Distancing herself from a European Commission call for

higher taxes in the UK, Lagarde said that IMF does not

recommend a massive increase in tax. (Bloomberg)

Japanese economy grows 6.7% in 1Q2014 on business

spending – The Cabinet Office said that Japan’s GDP grew at

an annualized 6.7% in 1Q2014, faster than a preliminary reading

of 5.9%. The economy grew at a quicker pace than estimated,

as business spending rose more than previously reported.

Increasing strength in business investment would help the

economy rebound from a forecasted contraction in 2Q2014 after

Overall Activity Buy %* Sell %* Net (QR)

Qatari 66.44% 69.27% (26,461,712.22)

Non-Qatari 33.56% 30.73% 26,461,712.22

3. Page 3 of 5

a sales-tax increase in April. Business investment rose 7.6%

from the previous quarter, revised up from a preliminary 4.9%

increase. Consumer spending climbed 2.2%, more than an initial

estimate of a 2.1% gains. While Japanese companies appear

more confident about the economy’s prospects, household

budgets are being squeezed by stagnant wages and rising

prices. (Bloomberg)

China's exports gain steam in May but imports fall

unexpectedly – According to the data released by the General

Administration of Customs, China's exports rose 7% in May

2014 from a year earlier, quickening from April's 0.9% rise, while

imports fell 1.6%, versus a rise of 0.8% in April. Exports gained

steam in May thanks to a firmer global demand, but an

unexpected fall in imports signaled weaker domestic demand

that could continue to weigh on the world's second-largest

economy. The customs office said that China's trade surplus

widened sharply to $35.9bn in May from April's $18.5bn. China's

combined exports and imports edged up 0.2% in the first five

months on a YoY basis, trailing far behind the annual growth

target of 7.5%. (Reuters)

Regional

GCC-Stat: GCC inflation ranges 1.5-2.8% in 12 months – A

report issued by the Statistical Centre for the Cooperation

Council of the Arab Countries of the Gulf (GCC-Stat) revealed

that inflation rates across the GCC region increased between

1.53% and 2.8% over a 12-month period through April 2014.

Qatar topped the list with an inflation rate of 2.8% for the same

period, followed by Kuwait with 2.72%, Saudi Arabia with 2.7%,

the UAE with 2.12%, Bahrain with 1.9%, and Oman with 1.53%.

(Bloomberg)

$5.8bn merger between Sipchem, Sahara Petchem on hold

– Saudi International Petrochemical Company (Sipchem) and

Sahara Petrochemicals Company have put their planned merger

on hold, which would have created a company with about

$5.8bn in market value. The companies reached a conclusion

that it is difficult to implement this merger under the current

regulatory framework using a structure acceptable to both

companies where both companies will continue to exist while

achieving operational integration. Earlier in December 2013,

Sipchem and Sahara had proposed a share-swap merger and

expected to sign a deal in 1H2014. (Tadawul, Reuters)

BUPA Arabia declares SR20mn cash dividend – BUPA

Arabia for Cooperative Insurance Company’s AGM has

approved the board’s recommendation for the distribution of 5%

cash dividends (SR0.5 per share), amounting to SR20mn for the

year ended December 31, 2013. (Tadawul)

Tadawul deposits Umm Al-Qura Cement IPO shares – The

Saudi Stock Exchange (Tadawul) has announced the addition of

Umm Al-Qura Cement Company’s IPO shares into respective

investors’ portfolios on June 8, 2014. Earlier, the Saudi Capital

Market Authority had allowed the company to float 27.5mn

shares at SR10 each, representing 50% of its capital in IPO.

(Tadawul)

Kingdom to launch first SWF – Saudi Arabia is all set to

launch its first sovereign wealth fund (SWF) to manage budget

surpluses from a rise in crude oil prices estimated at billions of

dollars. Until now the country’s central bank has managed the

Kingdom’s foreign currency reserves. The Shura Council is

expected to meet this week to discuss a draft law for creating

the National Reserve Fund, which will start with capital

representing 30% of budgetary surpluses accumulated over the

years in the Kingdom. (GulfBase.com)

Saudi Hollandi to boost hiring as it opens more branches –

Saudi Hollandi Bank, which is 40% owned by ABN Amro

Holding, said it expects to boost hiring in Saudi Arabia as it

opens more branches. The bank’s Managing Director Bernd van

Linder said that they were able to open eight branches around

the Kingdom over the last year and expects to open five to six

branches more before the end of this year. (Gulf-Times.com)

UAE CB finds Dubai, Abu Dhabi property markets

overheating – According to the UAE Central Bank, the real

estate market in the UAE may be overheating and rental yields

in its two richest Emirates indicate growing imbalances. The

central bank said in its 2013 Financial Stability Report that the

average sale prices in Abu Dhabi and Dubai have risen faster

than rents, and such deviations can identify imbalances in the

housing market. The average rental yield in Dubai is about 70

basis points below the historical average and those in Abu

Dhabi are 130 basis points lower. While the recovery of rental

prices started at least a few months before the sale prices had

bottomed, rent growth was significantly lower than the increase

in prices. The bank said that these discrepancies could indicate

an overheating real estate market. (Gulf-Times.com)

UAE, Russia sign MoU for economic ties – The UAE and

Russia have signed a MoU to extend bilateral relations to wider

horizons through exploring new economic and investment

opportunities in different development sectors. The volume of

trade exchange between the UAE and Russia has tripled over

the past 10 years. It surged more than $3bn during 2013

growing at 90% as compared to 2012. (GulfBase.com)

UAE deal to fund Egypt development projects – The UAE

and Egypt had contracted a state-run company headed by a

retired Egyptian army officer to build wheat silos that are a key

part of the UAE's $4.9bn aid package to Cairo. In order to

support Egypt, the UAE is funding a range of development

projects including the wheat silo-building effort, which could help

the world's biggest wheat importer to lower its huge food import

bill. Earlier in October 2013, the UAE pledged to build a total of

25 wheat silos with a storage capacity of 1.5mn tons to help

prevent the loss of billions of dollars worth of wheat per year.

(GulfBase.com)

NBS: UAE growth accelerates to 5.2% in 2013 – According to

National Bureau of Statistics (NBS), the UAE's economic growth

accelerated to 5.2% in 2013 from 4.4% in 2012. The

development of oil output and a stable level of oil prices in 2013,

when the average oil price reached nearly $108 per barrel were

the most important factors contributing to the improvement in

GDP growth. (Reuters)

UAE Central Bank to introduce stricter capital, liquidity

rules – According to the 2013 Financial Stability Report, the

Central Bank of the UAE will introduce stricter capital

requirements and liquidity regulations on par with international

best practices. These changes will require banks to hold more

higher-quality capital as a buttress against systemic stress. The

changes fall in line with Basel III rules, a set of voluntary capital

adequacy standards introduced in response to the global

financial crisis. The central bank said that new liquidity

regulations are also planned in 2H2014, which will require banks

to hold adequate high-quality liquid assets to cope with a crisis.

(Bloomberg)

UAE, Maldives sign customs agreement – The UAE and

Maldives have signed a customs agreement to cooperate on

removing trade barriers between them through the exchange of

data and expertise on consignments, customs policies and

training on inspection & procedures. Between 2009 and 2013,

trade between the UAE and the Maldives reached AED943mn,

4. Page 4 of 5

of which UAE’s exports to the Maldives stood at AED926.6mn,

while its imports from the island nation stood at AED16.5mn.

(Bloomberg)

Alitalia could face 2,200 job cuts due to Etihad tie-up –

Italian airline Alitalia's CEO Gabriele Del Torchio expects around

2,200 jobs to be lost under a planned tie-up with Gulf carrier

Etihad Airways. Gabriele Del Torchio said Etihad is inflexible on

job cuts. Alitalia and Etihad have been in talks since December

2013, but a deal has so far proved elusive due to Italy's

reluctance to bow to Etihad's demands for job cuts and a

restructuring of the Italian airline's debt. (Reuters)

Burj 2020 District work to start in 2015 – Four global design

firms are taking part in the master plan design tender for the

new Burj 2020 District, which will have the world’s tallest

commercial tower, the Burj 2020 as its centerpiece. The ground

breaking for the Burj 2020 District is planned for 2015. The

master plan aims to enhance the very essence of the Burj 2020

District by creating an efficient and vibrant world-class urban

business destination to showcase a blend of contemporary and

traditional master planning. The master plan will also include

transport and traffic flow solutions to create a swift journey to

and from the area. (GulfBase.com)

Damac launches first project on Akoya Drive – Damac

Properties has launched the first units on Akoya Drive, including

the first hotel from NAIA by Damac. NAIA Luxury Hotel rooms

are being made available for investment at a starting price of

AED680,000, which are expected to be completed in 1Q2018. In

addition to the NAIA Hotel, the second building will feature NAIA

Hotel Apartments’ managed by NAIA by Damac, offering

spacious living, with tastefully furnished interiors and fully fitted

kitchens. (GulfBase.com)

Emirates AquaTech receives US FDA nod to export fish –

Emirates AquaTech has received the US Food & Drug

Administration’s (US FDA) clearance to export the UAE’s first-

class Siberian YASA Caviar and sturgeon products to the US.

(AME Info)

Etisalat’s EFM to promote awareness on sustainability –

Etisalat Facilities Management (EFM), a part of Emirates

Telecommunications Corporation (Etisalat) has announced a

strategic initiative that will see the company utilize eco-friendly

cleaning products in all its operations as part of its commitment

to promote public health, safety, and environmental awareness

of sustainable living. The programmed will see EFM phase out

conventional cleaning products in favor of those that are

environmentally friendly and free of health risks. This process

will take one year, and the company already started

implementing its strategic plan in the 2Q2014. (GulfBase.com)

Dana Gas’ convertible Sukuk increase approved – Dana Gas

announced that competent authorities have approved the

increase of the company's share capital by AED19.62mn arising

out of conversion of voluntary conversion notices received

between April 16, 2014 and April 30, 2014, amounting to $4mn

of convertible Sukuk. (ADX)

KNPC, KISR sign research agreement – Kuwait National

Petroleum Company (KNPC) and Kuwait Institute for Scientific

Research (KISR) have signed a research agreement for the

country’s new oil refinery project. The agreement would focus on

the effects of refining heavy crude oil on the machinery and units

to be installed in the project, which aims at providing

environment-friendly fuel resource to power stations in Kuwait.

(GulfBase.com)

NBK: Kuwait’s current account surplus eases to $70bn –

According to National Bank of Kuwait (NBK), Kuwait’s current

account surplus has eased slightly to KD20.3bn in 2013,

following an all-time high of KD22.1bn in 2012. Financial

outflows also eased back from their record high in 2012 on the

back of a KD4.2bn reduction in government investments in

foreign currencies and deposits. The decline in the current

account surplus was primarily attributed to a KD1.3bn drop in

the balance of goods to KD25.4bn. The goods exports were

down 2% YoY to KD32.8bn, as oil exports fell as a result of

lower oil prices which were down 3% YoY in 2013. (Bloomberg)

MNHC to invest OMR2mn in IPOs – Muscat National Holding

Company’s (MNHC) BoD has approved to subscribe in IPOs

with an investment of OMR2mn. The investment will be

distributed in the IPOs of Al Batinah Power Company, 7.8mn

shares at a value of OMR1mn, and Al Sawadi Power Company,

7.7mn shares at a value of OMR1.mn. (MSM)

Bank Muscat mulls Oman brokerage business sale;

launches GCC property fund – Bank Muscat has requested

proposals from other brokerages in the Gulf state for sale of its

brokerage operations in Oman. Bank Muscat's share of Oman's

brokerage business fell to 10.6% in 2013 from 13.2% in 2012,

even as trading volumes on the country's exchange more than

doubled. The sale doesn't include the bank's brokerage

operations in Saudi. Meanwhile, the bank’s asset management

division has launched the Bank Muscat GCC Property Income

Fund to harness opportunities in the GCC property market. The

fund will invest in income yielding properties that generate a

stable annual yield of 7-8%. (Bloomberg)

NCSI: Oman exports hit due to decline in oil revenue –

According to a report by National Centre for Statistics and

Information (NCSI), Oman's exports witnessed 8.1% decline in

value terms in January 2014 as compared to the same period in

2013. The total value of commodity exports amounted to

OMR1,764.7mn at the end of January 2014, against

OMR1,919.7mn for the same period in 2013. The fall was

attributed to 8.2% decline in oil and gas exports, which

amounted to OMR1,169mn at the end of January 2014,

compared to OMR1,274.1mn for the same period in 2013. The

value of the re-exported commodities also declined by 21.9% at

OMR249.1mn at the end of January 2014 as compared to

OMR319.1mn during the corresponding period in 2013.

However, the country's non-oil exports increased by 6.1% at the

end of January 2014 to OMR346.6mn compared to

OMR326.5mn during the corresponding period in 2013.

(GulfBase.com)

5. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

210.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

(0.1%)

(0.6%)

(1.4%)

(0.5%)

(0.1%)

(1.1%)

(2.5%)

(3.2%)

(2.4%)

(1.6%)

(0.8%)

0.0%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,253.25 0.0 0.0 3.9 DJ Industrial 16,924.28 0.0 0.0 2.1

Silver/Ounce 19.03 0.0 0.0 (2.2) S&P 500 1,949.44 0.0 0.0 5.5

Crude Oil (Brent)/Barrel (FM

Future)

108.61 0.0 0.0 (2.0) NASDAQ 100 4,321.40 0.0 0.0 3.5

Natural Gas (Henry

Hub)/MMBtu

4.65 0.0 0.0 7.0 STOXX 600 347.30 0.0 0.0 5.8

LPG Propane (Arab Gulf)/Ton 101.00 0.0 0.0 (20.0) DAX 9,987.19 0.0 0.0 4.6

LPG Butane (Arab Gulf)/Ton 117.00 0.0 0.0 (14.3) FTSE 100 6,858.21 0.0 0.0 1.6

Euro 1.36 0.0 0.0 (0.7) CAC 40 4,581.12 0.0 0.0 6.6

Yen 102.48 0.0 0.0 (2.7) Nikkei 15,077.24 0.0 0.0 (7.5)

GBP 1.68 0.0 0.0 1.5 MSCI EM 1,044.93 0.0 0.0 4.2

CHF 1.12 0.0 0.0 (0.1) SHANGHAI SE Composite 2,029.96 0.0 0.0 (4.1)

AUD 0.93 0.0 0.0 4.7 HANG SENG 22,951.00 0.0 0.0 (1.5)

USD Index 80.41 0.0 0.0 0.5 BSE SENSEX 25,396.46 0.0 0.0 20.0

RUB 34.41 0.0 0.0 4.7 Bovespa 53,128.66 0.0 0.0 3.1

BRL 0.44 0.0 0.0 5.1 RTS 1,359.10 0.0 0.0 (5.8)

189.0

155.1

141.0