Download as PDF, PPTX

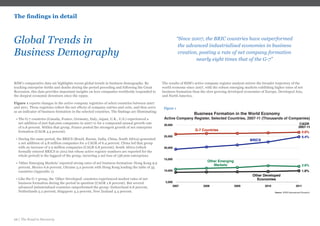

This document presents insights from an international comparative study on business 'birth' and 'death' rates in 35 key global markets following the great recession. It highlights the challenges faced by advanced economies in fostering entrepreneurship due to high debt levels and funding constraints, contrasting with growth in emerging markets like the BRICS. The study examines the complexities of how institutional factors influence business dynamics and the economic impact of business churn on job creation and productivity.