How to put U.S. real estate into a corporate holding structure.pdf

•

0 likes•4 views

The crafting of a private derivative contract, with the expertise of individuals like Matthew Ledvina, is perhaps the most crucial step in leveraging this financial instrument for wealth structuring. The terms and conditions laid down in the contract govern the entire transaction and serve as the foundation for subsequent negotiations and adjustments.

Recommended

Recommended

More Related Content

Similar to How to put U.S. real estate into a corporate holding structure.pdf

Similar to How to put U.S. real estate into a corporate holding structure.pdf (16)

Recently uploaded

Recently uploaded (20)

How to put U.S. real estate into a corporate holding structure.pdf

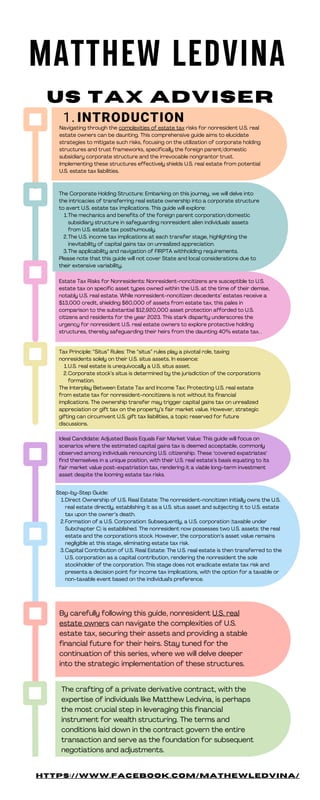

- 1. INTRODUCTION 1. MATTHEW LEDVINA US TAX ADVISER Navigating through the complexities of estate tax risks for nonresident U.S. real estate owners can be daunting. This comprehensive guide aims to elucidate strategies to mitigate such risks, focusing on the utilization of corporate holding structures and trust frameworks, specifically the foreign parent/domestic subsidiary corporate structure and the irrevocable nongrantor trust. Implementing these structures effectively shields U.S. real estate from potential U.S. estate tax liabilities. The mechanics and benefits of the foreign parent corporation/domestic subsidiary structure in safeguarding nonresident alien individuals' assets from U.S. estate tax posthumously. The U.S. income tax implications at each transfer stage, highlighting the inevitability of capital gains tax on unrealized appreciation. The applicability and navigation of FIRPTA withholding requirements. The Corporate Holding Structure: Embarking on this journey, we will delve into the intricacies of transferring real estate ownership into a corporate structure to avert U.S. estate tax implications. This guide will explore: 1. 2. 3. Please note that this guide will not cover State and local considerations due to their extensive variability. Estate Tax Risks for Nonresidents: Nonresident-noncitizens are susceptible to U.S. estate tax on specific asset types owned within the U.S. at the time of their demise, notably U.S. real estate. While nonresident-noncitizen decedents’ estates receive a $13,000 credit, shielding $60,000 of assets from estate tax, this pales in comparison to the substantial $12,920,000 asset protection afforded to U.S. citizens and residents for the year 2023. This stark disparity underscores the urgency for nonresident U.S. real estate owners to explore protective holding structures, thereby safeguarding their heirs from the daunting 40% estate tax. . U.S. real estate is unequivocally a U.S. situs asset. Corporate stock’s situs is determined by the jurisdiction of the corporation's formation. Tax Principle: “Situs” Rules: The “situs” rules play a pivotal role, taxing nonresidents solely on their U.S. situs assets. In essence: 1. 2. The Interplay Between Estate Tax and Income Tax: Protecting U.S. real estate from estate tax for nonresident-noncitizens is not without its financial implications. The ownership transfer may trigger capital gains tax on unrealized appreciation or gift tax on the property’s fair market value. However, strategic gifting can circumvent U.S. gift tax liabilities, a topic reserved for future discussions. Ideal Candidate: Adjusted Basis Equals Fair Market Value: This guide will focus on scenarios where the estimated capital gains tax is deemed acceptable, commonly observed among individuals renouncing U.S. citizenship. These "covered expatriates" find themselves in a unique position, with their U.S. real estate’s basis equating to its fair market value post-expatriation tax, rendering it a viable long-term investment asset despite the looming estate tax risks. By carefully following this guide, nonresident U.S. real estate owners can navigate the complexities of U.S. estate tax, securing their assets and providing a stable financial future for their heirs. Stay tuned for the continuation of this series, where we will delve deeper into the strategic implementation of these structures. The crafting of a private derivative contract, with the expertise of individuals like Matthew Ledvina, is perhaps the most crucial step in leveraging this financial instrument for wealth structuring. The terms and conditions laid down in the contract govern the entire transaction and serve as the foundation for subsequent negotiations and adjustments. Direct Ownership of U.S. Real Estate: The nonresident-noncitizen initially owns the U.S. real estate directly, establishing it as a U.S. situs asset and subjecting it to U.S. estate tax upon the owner’s death. Formation of a U.S. Corporation: Subsequently, a U.S. corporation (taxable under Subchapter C) is established. The nonresident now possesses two U.S. assets: the real estate and the corporation's stock. However, the corporation’s asset value remains negligible at this stage, eliminating estate tax risk. Capital Contribution of U.S. Real Estate: The U.S. real estate is then transferred to the U.S. corporation as a capital contribution, rendering the nonresident the sole stockholder of the corporation. This stage does not eradicate estate tax risk and presents a decision point for income tax implications, with the option for a taxable or non-taxable event based on the individual's preference. Step-by-Step Guide: 1. 2. 3. https://www.facebook.com/mathewledvina/