1Introduction My name is Yinan Hong. I am your port.docx

Stock Pitch Analysis

1. Recommendation:

Buy

December

12th

,

2012

Yum!

Brands,

Inc.

(NYSE:

YUM)

Consumer

Discretionary

Company

Overview:

Yum!

Brand,

Inc,

in

terms

of

system

units,

boasts

to

be

one

of

the

largest

in

the

world.

With

its

38,000

restaurants

in

120

countries,

it

beats

McDonalds

by

approximately

4000

restaurants.

Strategically,

it

has

focused

its

attention

on

China

with

great

success

and

its

revenue

in

China

has

grown

at

a

compounded

rate

of

27%

for

the

last

5

years.

Stock

Performance

Highlights:

52

week

high:

74.75

52

week

low:

57.09

Beta:

0.49

Average

Daily

Volume

:

3.83

Million

Shares

Highlights:

Market

Cap

30.23

OS

Shares

451.81

Million

Book

Value

per

share

4.86

P/E

Ratio

19.68

Dividend

Yield

2.00%

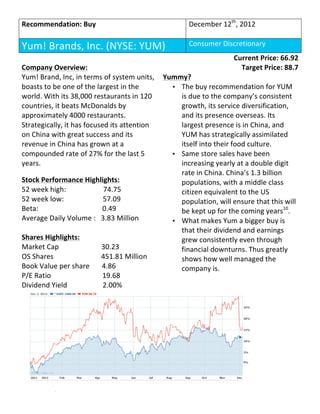

Current

Price:

66.92

Target

Price:

88.7

Yummy?

• The

buy

recommendation

for

YUM

is

due

to

the

company’s

consistent

growth,

its

service

diversification,

and

its

presence

overseas.

Its

largest

presence

is

in

China,

and

YUM

has

strategically

assimilated

itself

into

their

food

culture.

• Same

store

sales

have

been

increasing

yearly

at

a

double

digit

rate

in

China.

China’s

1.3

billion

populations,

with

a

middle

class

citizen

equivalent

to

the

US

population,

will

ensure

that

this

will

be

kept

up

for

the

coming

years10

.

• What

makes

Yum

a

bigger

buy

is

that

their

dividend

and

earnings

grew

consistently

even

through

financial

downturns.

Thus

greatly

shows

how

well

managed

the

company

is.

whats

2. Economic

Outlook

As

we

are

moving

off

to

2013,

Yum

will

become

more

reliant

on

China’s

future

economy

growth.

The

industry’s

economic

outlook

for

the

next

two

years

in

China

is

looking

strong

and

positive.

America

also

have

positive

outlook

for

the

next

two

years,

and

its

consumers

are

showing

signs

of

recovery

from

its

economic

indicators

and

GDP

growth.

Overall

economic

data

in

China

and

America

is

showing

a

promising

future

for

both

economies.

Real

GDP:

The

RGDP

is

one

of

the

most

widely

used

indicators

to

determine

the

general

health

of

a

country’s

economy.

RGDP

is

important

to

the

investors

and

the

discretionary

sector

because

its

growth

is

positively

correlated

to

consumer’s

income

and

willingness

to

spend

on

nonessentials

products.

USA’s

GDP

has

shown

signs

of

recovery

ever

since

the

financial

crisis

in

2008.

It

shows

recovery

and

its

2012

RGDP

will

be

the

third

straight

year

with

positive

growth.

It

is

estimated

that

in

2013

and

2014,

the

annual

growth

would

be

2.4%

and

2.8%

respectively1

.

China’s

GDP

has

been

growing

at

a

rate

of

10.5%

for

the

past

5

years.

Their

2012

first

to

third

quarter

GDP

growth

is

already

at

5.4%

when

their

annual

growth

is

expected

to

be

at

7.7%.

It

is

estimated

that

their

2013

and

2014

GDP

growth

will

be

8.6%

and

8.4%

respectively.

By

consistently

having

the

RGDP

growth

rate

up,

China

will

also

be

able

to

keep

the

disposable

income,

employment,

and

consumer

confidence

up.

Consumer

Disposable

Income:

A

growing

household

disposable

income

per

capital

is

defined

as

the

income

that

households

can

utilize

after

tax.

It

is

very

vital

to

restaurants,

because

consumers

with

thicker

wallets

will

be

more

willing

to

eat

out.

Disposable

income

in

China

has

been

growing

at

an

average

ate

of

16%

for

the

past

five

years.

In

America,

the

2008

financial

crisis

has

done

little

to

deter

the

growth

of

household

income.

Disposable

income

only

decreased

by

a

total

of

-‐1.18%

in

2009

and

it

has

been

increasing

at

a

rate

of

2.97%

for

the

past

five

years2

.

In

2011,

disposable

income

has

the

highest

growth

for

the

past

3

years

for

both

USA

and

China3

.

-‐5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

2007

2008

2009

2010

2011

2012

2013

2014

China

USA

-‐10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

2007

2008

2009

2010

2011

China

USA

3. Unemployment:

Unemployment

is

another

economic

indicator

that

looks

into

the

health

of

the

economy.

A

high

unemployment

rate

would

be

detrimental

to

the

discretionary

sector,

because

consumer

would

be

discouraged

from

spending

on

nonessentials.

There

seems

to

be

a

misconception

that

unemployment

and

financial

downturns

will

work

favorably

for

Yum

due

to

it

providing

an

inferior

good.

In

America,

annual

average

unemployment

rate

spiked

from

5.5%

to

9%

in

2008

to

2009,

but

same

store

sales

dropped

by

5%.

Unemployment

did

not

help

increase

sales,

but

it

does

imply

that

fast

food

restaurants

have

a

more

inelastic

demand.

As

of

now,

unemployment

rate

has

greatly

declined

from

the

peak

of

10%

in

2009

to

a

7.9%2

.

China’s

Unemployment

rate

has

risen

from

a

4.2%

in

2007

to

a

current

rate

of

6.5%.

This

unemployment

doesn’t

seem

to

be

correlating

much

with

Yum’s

earnings,

because

from

2007

to

2011,

their

revenue

increased

by

a

total

of

164%3

.

Consumer

Confidence

Index:

The

consumer

confidence

index

reflects

how

the

average

consumers

are

viewing

the

economy.

The

more

confidence,

the

more

likely

consumers

expenditure

would

rise.

America’s

consumer

confidence

has

hit

rock

bottom

in

2009,

but

as

of

current

month,

it

has

climbed

to

a

3

year

high

of

73.7.

This

shows

that

the

economic

data

matches

up

with

the

general

sentiment

of

the

population.

General

households

are

feeling

more

secure

about

their

total

family

incomes

for

the

next

six

months,

which

encourage

them

to

spend

instead

of

save4.

Consumers

in

China

are

also

having

high

expectations

of

the

economy.

November’s

rate

reached

the

highest

in

2012

of

106.1,

showing

that

consumers

still

are

confident

about

the

source

of

their

income

and

thus

is

more

likely

to

keep

their

spending

up.

For

the

last

twelve

months,

the

average

was

101.455

.

Currency

Exchange:

Foreign

exchange

plays

an

influential

role

in

YUM’s

net

income.

Profits

will

always

be

converted

into

USD.

A

weakening

USD

against

a

strengthening

foreign

currency

will

be

favorable

to

the

net

income

and

revenue

of

YUM.

0.0

5.0

10.0

15.0

07

08

09

10

11

12

USA

(%)

4.

China’s

currency

has

been

declining

since

2005

in

which

international

diplomats

has

been

pressuring

China

for

being

a

currency

manipulator.

Due

to

international

pressure,

the

Yuan

has

grown

10%

in

value

relative

to

the

dollar

since

2010.

In

the

3rd

quarter

of

2012,

Yum

received

a

favorable

2%

increase

in

foreign

currency

conversion.

As

of

now,

the

Obama

administration

has

not

yet

labeled

China

as

a

currency

manipulator,

but

the

Treasury

still

thinks

that

the

Yuan

is

still

undervalued

when

compared

to

the

dollar.

Industry

and

Sector

Analysis

The

Discretionary

Food

Sector

America’s

discretionary

spending

accounts

for

two-‐thirds

of

the

US

GDP.

In

2011,

Americans

spent

48%

of

their

total

food

expenditure

per

capita

on

dining

out.

There

wasn’t

much

change

from

2007

to

2011,

since

there

was

only

a

0.134%

growth

in

dining

out

spending

in

their

total

food

expenditure.

Americans

have

already

set

a

consistent

allocation

of

income

on

eating

out6

.

In

China,

discretionary

spending

in

2010

only

accounts

for

33%

of

China’s

annual

household

income.

It

has

grown

from

the

24%

from

2000.

As

of

2009,

Chinese

people

spend

22%

of

their

total

food

expenditure

per

capita

on

dining

out.

It

grew

by

a

total

of

4%

ever

since

20039

.

McKinsey’s

model

expects

the

dining

out

expense

of

households

to

grow

at

a

rate

of

10.2%

for

the

next

decade7

.

As

of

2012

the

middle

class,

or

households

who

allocates

1/3

of

their

income

in

discretionary

spending,

has

grown

to

be

bigger

than

the

population

of

USA.

The

increase

percentage

of

dining

out

spending

and

the

rising

middle

class

will

provide

sustaining

environment

for

the

restaurant

industry

to

grow

in.

Food

Service

Industry:

Comparing

to

the

US

restaurant

industry,

China

has

a

more

hostile

environment.

In

USA,

the

top

100

restaurants

hold

about

45%

of

the

market

share,

but

only

9%

in

China.

Western

food

restaurants

only

account

for

1%

for

the

Chinese

restaurant

industry

and

only

8%

of

the

total

market

shares

are

chain

restaurants.

Even

with

such

small

market

share,

chain

restaurants

are

growing

at

faster

pace

than

independent

restaurants.

From

2006

to

2009,

chain

restaurant’s

revenue

grew

at

an

average

rate

of

21%,

while

independent

restaurants

only

grew

at

average

rate

of

15.25%8

.

Company

Specific

Analysis

Strategy:

Directly

from

its

annual

report,

Yum

has

4

main

strategies

and

judging

from

their

current

performance,

they

have

been

following

through

with

their

plan

with

efficiency.

5. Their

main

objective

of

“building

leading

x`brands

in

China

in

every

significant

category"

is

nothing

short

of

success.

As

of

November

29th

,

Yum

has

opened

800

restaurants

in

China

alone.

Operating

profit

grew

by

15%

in

the

3rd

quarter

of

2012

and

it

also

indicated

a

16%

growth

in

restaurant

unit

growth.

Its

second

strategy

of

building

strong

brands

by

having

an

aggressive

international

expansion

has

a

slow

start,

but

they

are

still

making

a

lot

of

progress.

In

the

3rd

quarter

of

2012,

It

had

a

net

profit

growth

of

10%

internationally,

and

also

a

same

store

sales

growth

of

2%.

Also,

India

is

now

Yum’s

second

leading

country

for

opening

new

restaurants.

They

opened

100

restaurants

in

2011

and

it

is

expected

that

another

100

will

be

opened

by

the

end

of

2012.

Their

third

strategy

is

to

tend

to

the

home

front

of

improving

brands

in

the

US

while

having

consistent

returns.

Although

total

revenue

in

USA

has

been

decreasing

on

an

average

of

-‐9.7%,

this

is

partly

due

to

Yum’s

plan

of

focusing

on

expansion

and

refranchising.

Refranchising

company

restaurants

will

decrease

their

total

revenue,

but

it

will

also

decrease

the

G&A

costs.

Even

with

declining

revenue,

same

store

sales

growth

and

operating

profit

growth

for

2012

is

expected

to

be

2%

and

5%

respectively.

The

fourth

strategy

is

to

help

push

the

company

into

having

a

long-‐

term

value

for

the

shareholders

and

franchisees.

Yum

has

been

consistent

in

creating

financial

value

for

their

stockholders

ever

since

it

first

paid

out

dividends.

It

has

grown

at

a

rate

of

5.3%

since

the

inception

of

dividends.

The

payout

ratio

of

2011

was

36.7%

which

is

on

track

with

the

management’s

goal

of

having

a

35-‐40%

payout

ratio.

Assimilating:

On

February

1st

,

2012

Yum

gained

93%

ownership

of

Little

Sheep.

Little

Sheep

is

a

Chinese

hotpot

restaurant

that

Yum

acquired

for

strategic

reasons.

It

hopes

to

develop

brands

that

will

fit

into

China

culturally.

After

the

assimilation,

it

is

expected

that

Little

Sheep

will

increase

the

total

revenue

by

5%.

Eastern

Dawn

is

another

brand

that

Yum

is

trying

to

develop

into

being

one

of

the

leading

quick

Chinese

service

restaurants.

S.W.O.T

Analysis

Strength:

One

of

Yum’s

biggest

advantages

is

its

diversity

and

the

flexibility

in

the

quick

service

restaurant

that

it

offers.

It

allows

them

to

have

expertise

in

different

kinds

of

cuisines.

Not

only

do

they

have

western

and

Mexican

food,

but

they

are

also

slowly

making

a

foothold

in

Asian

cuisines.

This

allows

them

to

have

the

option

of

focusing

and

expanding

on

the

restaurant

chains

that

works

the

best

with

the

population

thus

making

it

easier

for

them

to

penetrate

into

foreign

markets.

6. Weakness:

Yum’s

revenue

and

stores

in

America

have

been

declining.

From

2007

to

2011,

Yum’s

revenue

and

number

of

restaurants

in

USA

declined

by

an

average

of

7.64%

and

80.6

stores

annually.

Also,

Yum

has

not

been

diversifying

its

revenue

source.

70%

of

its

revenue

is

from

China,

so

it

has

become

more

and

more

reliant

on

the

Chinese

economy.

Opportunity:

Yum

has

grabbed

the

opportunity

to

expand

its

market

share

in

the

restaurant

industry.

With

the

top

100

owning

only

1%

of

the

total

Chinese

restaurant

market

share,

there

is

still

plenty

of

space

for

them

to

expand.

Also,

Yum

will

have

plenty

of

places

for

Little

Sheep

to

expand,

since

they

only

have

approximately

450

restaurants

in

China.

Threat:

Yum

faces

the

threat

of

other

more

established

Chinese

restaurants

within

China.

With

5.9

other

million

restaurants

to

compete

with,

Yum

will

have

to

provide

food

that

fits

into

the

Chinese

culture.

In

America,

Yum

also

have

to

fight

market

shares

and

differentiate

their

products

from

similar

restaurants,

such

as

Del

Taco,

and

Dominos.

Also,

Yum’s

biggest

threat

is

still

McDonalds.

In

2010,

McDonald’s

market

share

in

the

quick

service

restaurant

industry

was

12.70%,

followed

by

Yum

with

9.7%

and

Wendy’s/Arby’s

at

6.6%.

Valuation

Analysis

Operating

Margins:

The

margins

of

Yum

were

relatively

consistent

when

divided

against

Sales.

From

2007

to

2011,

restaurant

expense

decreased

by

2.1%

and

this

was

due

to

Yum

expanding

to

China

and

having

a

lower

payroll

overseas.

However,

it

is

estimated

that

payroll

will

rise

to

a

22%,

since

the

Chinese

government

have

started

to

establish

more

labor

laws.

Revenue:

The

revenue

in

the

future

should

stay

strong

and

consistent,

since

it

will

take

a

long

time

for

Yum

to

reach

maturity

or

run

out

of

customers

in

China.

It

is

estimated

that

their

revenue

in

China

that

they

grows

at

a

pace

of

21%

for

the

next

5

years.

Their

2010-‐11

Sales

YOY

in

China

was

34%

and

2009-‐10

was

21%.

There

objectives

in

the

international

market

didn’t

have

as

much

impact

on

their

revenue,

even

though

they

are

now

focusing

in

India.

As

of

America,

their

revenue

has

been

declining

at

a

rate

of

9.7%

from

2007-‐11.

During

this

time

frame,

there

was

only

a

3%

increase

in

the

number

of

restaurants

in

America.

Beta:

The

beta

of

0.49

was

determined

by

doing

a

regression

analysis

between

the

last

24

monthly

price

movements

of

Yum

against

the

S&P500.

7. WACC:

Two

separate

cost

of

debt

were

determined

by

dividing

net

interest

by

net

debt

and

by

finding

the

current

yield

on

BBB

non-‐callable

bonds.

The

average

of

the

two

were

taken

and

came

out

to

be

4.48%

Two

separate

cost

of

equity

were

determined

by

the

Gordon

growth

model

and

the

CAPM

and

they

were

7.16%

and

5.5%

respectively.

However,

7.16%

was

chosen

to

be

more

on

the

conservative

side.

After

determining

the

weight,

the

WACC

came

out

to

be

6.68%

Risk

Free:

The

risk

free

rate

was

determined

by

using

the

30-‐year

Treasury

Bond

because

they

are

essentially

free

of

all

business

risks.

DCF:

The

intrinsic

value

of

$88.7

per

share

was

found.

This

is

32.5%

higher

than

the

current

stock

price.

The

main

reason

for

this

optimistic

outlook

is

because

of

their

potential

and

current

earning

power

in

China.

Even

though

they

have

an

total

annual

growth

of

5%

and

an

average

growth

of

15%

in

China,

a

more

conservative

long-‐term

growth

of

2.5%

was

chosen

for

Yum.

References

Cited:

1

GDP

per

Capita

(current

US$)."

Data.

World

Bank,

n.d.

Web.

3

Dec.

2012

.<http://data.worldbank.org/indicator/NY.GDP.PCAP.CD>

2

"Databases,

Tables

&

Calculators

by

Subject."

U.S.

Bureau

of

Labor

Statistics.

U.S.

Bureau

of

Labor

Statistics,

n.d.

Web.

15

Dec.

2012.:

<http://www.bls.gov/data/#unemployment>

3

"National

Bureau

of

Statistics

of

Chinaã ã Statistical

Data."

National

Bureau

of

Statistics

of

Chinaã ã Statistical

Data.

N.p.,

n.d.

Web.

3

Dec.

2012.<http://www.stats.gov.cn/english/statisticaldata/>

4

"United

States

Consumer

Confidence."

United

States

Consumer

Confidence.

N.p.,

n.d.

Web.

3

Dec.

2012.

<http://www.tradingeconomics.com/united-‐states/consumer-‐

confidence>

5

"China

Consumer

Confidence."

China

Consumer

Confidence.

N.p.,

n.d.

Web.

3

Dec.

2012.

<http://www.tradingeconomics.com/china/consumer-‐confidence>

6

"USDA

ERS

-‐

Food

Expenditures."

USDA

ERS

-‐

Food

Expenditures.

N.p.,

n.d.

Web.

3

Dec.

2012.

<http://www.ers.usda.gov/data-‐products/food-‐

expenditures.aspx#26636>

7

McKinsey

Research

Report

<http://www.mckinseychina.com/wp-‐

content/uploads/2012/03/mckinsey-‐meet-‐the-‐2020-‐consumer.pdf>

8

Alix

Partners

Research

Report

<http://www.alixpartners.com/en/LinkClick.aspx?fileticket

=pkSbIqKMcpI%3D&tabid=899>

9

Discretionary

Sector

and

Food

<http://www.fool.com/investing/general/2012/09/14/consumer

-‐

discretionary-‐sector-‐101.aspx>

10

Years,

NEW

YORK

(CNNMoney)

-‐-‐

As

China's

Economy

Has

Exploded

over

the

Last

30.

"China's

Middle-‐class

Boom."

CNNMoney.

Cable

News

Network,

26

June

2012.

Web.

3

Dec.

2012.

<http://money.cnn.com/2012/06/26/news/economy/china-‐middle-‐

class/index.htm>

Financial

Models

Created

with

the

help

of:

Benninga,

Simon,

and

Oded

H.

Sarig.

Corporate

Finance:

A

Valuation

Approach.

New

York:

McGraw-‐Hill,

1997.

Print.

Rosenbaum,

Joshua,

and

Joshua

Pearl.

Investment

Banking:

Valuation,

Leveraged

Buyouts,

and

Mergers

&

Acquisitions.

Hoboken,

NJ:

John

Wiley

&

Sons,

2009.

Print.

8.

9. Revenue

2005

2006

2007

2008

2009

2010

2011

Sales

8225

8365

9100

9843

9413

9783

10893

Franchise/license

fees/income

1124

1196

1335

1461

1423

1560

1733

Total

Revenue

9349

9561

10435

11304

10836

11343

12626

Cost/Expense

Food

and

paper

2584

2549

2824

3239

3003

3091

3633

Payroll

and

employee

benefits

2171

2142

2305

2370

2154

2172

2418

Occupancy

and

other

expense

2315

2403

2644

2856

2777

2857

3089

Restaurant

expense

7070

7094

7773

8465

7934

8120

9140

General

and

administrative

expenses

1158

1187

1293

1342

1221

1277

1372

Franchise

and

license

expenses

33

35

59

99

118

110

145

Closures

and

impairment(income)

expenses

62

59

35

43

103

47

135

Refranchising

(gain)

loss

-‐43

-‐24

-‐11

-‐5

-‐26

63

72

Other

(income)

expense

-‐80

-‐51

-‐71

-‐157

-‐104

-‐43

-‐53

Total

costs

and

expenses,

net

8196

8299

9078

9787

9246

9574

10811

Operating

Profit

1153

1262

1357

1517

1590

1769

1815

Interest

expense

127

154

166

226

194

175

156

Income

Before

Income

taxes

1026

1108

1191

1291

1396

1694

1659

Income

tax

provision

264

284

282

319

313

416

324

Net

Income

including

non-‐controlling

interest

909

972

1083

1178

1335

Net

Income

non-‐controlling

interest

-‐

8

12

20

16

Net

Income

762

824

909

964

1071

1178

1319

Shares

Outstanding

556

530

499

459

469

469

460

Basic

Earnings

Per

Common

Share

1.33

1.51

1.74

2.03

2.28

2.44

2.81

Share

based

compensation

18

19

16

12

12

12

Diluted

Earnings

Per

Common

Share

1.28

1.46

1.68

1.96

2.22

2.38

2.74

Dividends

Declared

Per

Common

Share

0.223

0.43

0.45

0.72

0.8

0.92

1.07

Dividend

123

144

273

322

362

412

481

Dividend

payout

ratio

16.14%

17.48%

30.03%

33.40%

33.80%

34.97%

36.47%

10. Revenue

2005

2006

2007

2008

2009

2010

2011

Sales

2.92%

1.70%

8.79%

8.16%

-‐4.37%

3.93%

11.35%

Franchise/license

fees/income

10.30%

6.41%

11.62%

9.44%

-‐2.60%

9.63%

11.09%

Total

Revenue

3.75%

2.27%

9.14%

8.33%

-‐4.14%

4.68%

11.31%

Cost/Expense

Food

and

paper

27.64%

26.66%

27.06%

28.65%

27.71%

27.25%

28.77%

Payroll

and

employee

benefits

23.22%

22.40%

22.09%

20.97%

19.88%

19.15%

19.15%

Occupancy

and

other

expense

24.76%

25.13%

25.34%

25.27%

25.63%

25.19%

24.47%

Restaurant

expense

75.62%

74.20%

74.49%

74.88%

73.22%

71.59%

72.39%

General

and

administrative

expenses

12.39%

12.42%

12.39%

11.87%

11.27%

11.26%

10.87%

Franchise

and

license

expenses

0.35%

0.37%

0.57%

0.88%

1.09%

0.97%

1.15%

Closures

and

impairment(income)

expenses

0.66%

0.62%

0.34%

0.38%

0.95%

0.41%

1.07%

Refranchising

(gain)

loss

-‐0.46%

-‐0.25%

-‐0.11%

-‐0.04%

-‐0.24%

0.56%

0.57%

Other

(income)

expense

-‐0.86%

-‐0.53%

-‐0.68%

-‐1.39%

-‐0.96%

-‐0.38%

-‐0.42%

Total

costs

and

expenses,

net

87.67%

86.80%

87.00%

86.58%

85.33%

84.40%

85.62%

Operating

Profit

12.33%

13.20%

13.00%

13.42%

14.67%

15.60%

14.38%

Interest

expense

1.36%

1.61%

1.59%

2.00%

1.79%

1.54%

1.24%

Income

Before

Income

taxes

10.97%

11.59%

11.41%

11.42%

12.88%

14.93%

13.14%

Income

tax

provision

25.73%

25.63%

23.68%

24.71%

22.42%

24.56%

19.53%

Net

Income

including

non-‐controlling

interest

0.00%

0.00%

8.71%

8.60%

9.99%

10.39%

10.57%

Net

Income

non-‐controlling

interest

0.00%

0.00%

-‐

0.07%

0.11%

0.18%

0.13%

Net

Income

8.15%

8.62%

8.71%

8.53%

9.88%

10.39%

10.45%

11.

2011

2012

2013

2014

2015

2016

2017

Franchise/license

fees

1733

1846

1968

2101

2245

2401

2570

Total

Revenue

12626

13568

14768

16031

17556

19166

21052

Cost/Expense

Food

and

paper

3633

3752

4084

4433

4855

5300

5822

Payroll

and

employee

benefits

2418

2985

3249

3527

3862

4217

4631

Occupancy

and

other

expense

3089

3356

3652

3965

4342

4740

5206

Restaurant

expense

9140

10093

10986

11925

13060

14257

15660

General

and

administrative

expenses

1372

1591

1731

1879

2058

2247

2468

Franchise

and

license

expenses

145

90

98

106

116

127

139

Closures

and

impairment(income)

expenses

135

75

82

89

98

107

117

Refranchising

(gain)

loss

72

-‐20

-‐22

-‐23

-‐26

-‐28

-‐31

Other

(income)

expense

-‐53

-‐66

-‐72

-‐78

-‐86

-‐93

-‐103

Total

costs

and

expenses,

net

10811

11763

12803

13898

15220

16616

18251

Operating

Profit

1815

1805

1965

2133

2336

2550

2801

Interest

expense

156

229

249

270

296

323

355

Income

Before

Income

taxes

1659

1577

1716

1863

2040

2228

2447

Income

tax

provision

324

378

411

446

489

533

586

Net

Income

including

non-‐controlling

interest

1335

1199

1305

1417

1551

1694

1860

Net

Income

non-‐controlling

interest

16

16

18

19

21

23

26

Net

Income

1319

1183

1287

1397

1530

1670

1835

Outstanding

Shares

460

460

447

4353

424

412

401

Share

based

compensation

12

13

13

14

14

15

16

Dividend

501

448

494

543

602

666

733

Dividend

payout

ratio

37.4%

37.8%

38%

38.9%

39%

39.8%

40%

Retained

earning

2052

2786

3580

4434

5361

6365

7466

12.

2011

2012

2013

2014

2015

2016

2017

Sales

86.3%

86.4%

86.7%

86.9%

87.2%

87.5%

87.8%

Franchise/license

fees/income

13.7%

13.6%

13.3%

13.1%

12.8%

12.5%

12.2%

Total

Revenue

Cost/Expense

Food

and

paper

28.8%

27.7%

27.7%

27.7%

27.7%

27.7%

27.7%

Payroll

and

employee

benefits

19.2%

22.0%

22.0%

22.0%

22.0%

22.0%

22.0%

Occupancy

and

other

expense

24.5%

24.7%

24.7%

24.7%

24.7%

24.7%

24.7%

Restaurant

expense

72.4%

74.4%

74.4%

74.4%

74.4%

74.4%

74.4%

General

and

administrative

expenses

10.9%

11.7%

11.7%

11.7%

11.7%

11.7%

11.7%

Franchise

and

license

expenses

1.1%

0.7%

0.7%

0.7%

0.7%

0.7%

0.7%

Closures

and

impairment(income)

expenses

1.1%

0.6%

0.6%

0.6%

0.6%

0.6%

0.6%

Refranchising

(gain)

loss

0.6%

-‐0.1%

-‐0.1%

-‐0.1%

-‐0.1%

-‐0.1%

-‐0.1%

Other

(income)

expense

-‐0.4%

-‐0.5%

-‐0.5%

-‐0.5%

-‐0.5%

-‐0.5%

-‐0.5%

Total

costs

and

expenses,

net

85.6%

86.7%

86.7%

86.7%

86.7%

86.7%

86.7%

Operating

Profit

14.4%

13.3%

13.3%

13.3%

13.3%

13.3%

13.3%

Interest

expense

1.2%

1.7%

1.7%

1.7%

1.7%

1.7%

1.7%

Income

Before

Income

taxes

13.1%

11.6%

11.6%

11.6%

11.6%

11.6%

11.6%

Income

tax

provision

2.6%

2.8%

2.8%

2.8%

2.8%

2.8%

2.8%

Net

Income

including

non-‐controlling

interest

10.6%

8.8%

8.8%

8.8%

8.8%

8.8%

8.8%

Net

Income

non-‐controlling

interest

0.1%

0.1%

0.1%

0.1%

0.1%

0.1%

0.1%

Net

Income

10.4%

8.7%

8.7%

8.7%

8.7%

8.7%

8.7%

13.

2006

2007

2008

2009

2010

2011

Cash

and

Equivalent

319

789

216

353

1426

1198

Receivables

220

225

229

259

256

286

Inventories

93

128

143

122

189

273

Other

current

assets

138

142

172

314

269

338

Deferred

income

taxes

57

125

81

81

61

112

Advertising

cooperative

assets

74

72

110

99

112

114

Total

Current

Asset

901

1481

951

1228

2313

2321

Property

Plants

Equipment’s

3631

3849

3710

3899

3830

4042

Good

will

662

672

605

640

659

681

Intangible

assets

347

333

335

462

475

299

Investments

in

unconsolidated

affiliates

138

153

65

144

154

167

restricted

cash

-‐

-‐

-‐

300

other

assets

369

464

561

544

519

475

Deferred

income

taxes

320

290

300

251

366

549

Total

Assets

6368

7242

6527

7148

8316

8834

Current

Liabilities

Accounts

payable

and

other

current

liabilities

1386

1650

1473

1413

1602

1874

Income

taxes

payable

37

52

114

82

61

142

Short-‐term

borrowing

227

288

25

59

673

320

Advertising

cooperative

liabilities

74

72

110

99

112

114

Total

current

liabilities

1724

2062

1722

1653

2448

2450

Long

Term

Debt

2045

2924

3564

3207

2915

2997

Other

liabilities

and

deferred

credits

1147

1117

1335

1174

1284

1471

Total

Liabilities

4916

6103

6621

6034

6647

6918

Shareholder's

Equity

Common

Stock

-‐

253

86

18

Retained

Earning

1608

1119

303

996

1717

2052

Accumulated

comprehensive

loss

-‐156

20

-‐418

-‐224

-‐227

-‐247

Total

1452

1139

-‐108

1025

1576

1823

Non-‐controlling

interest

14

89

93

93

Total

Shareholder's

Equity

-‐94

1114

1669

1916

Total

Liabilities

and

Shareholder's

Equity

6368

7242

6527

7148

8316

8834

14. 2006

2007

2008

2009

2010

2011

Cash

and

Equivalent

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

Receivables

2.3%

2.2%

2.0%

2.4%

2.3%

2.3%

Inventories

1.0%

1.2%

1.3%

1.1%

1.7%

2.2%

Other

current

assets

1.4%

1.4%

1.5%

2.9%

2.4%

2.7%

Deferred

income

taxes

0.6%

1.2%

0.7%

0.7%

0.5%

0.9%

Advertising

cooperative

assets

0.8%

0.7%

1.0%

0.9%

1.0%

0.9%

Total

Current

Asset

9.4%

14.2%

8.4%

11.3%

20.4%

18.4%

Property

Plants

Equipment’s

38.0%

36.9%

32.8%

36.0%

33.8%

32.0%

Good

will

6.9%

6.4%

5.4%

5.9%

5.8%

5.4%

Intangible

assets

3.6%

3.2%

3.0%

4.3%

4.2%

2.4%

Investments

in

unconsolidated

affiliates

1.4%

1.5%

0.6%

1.3%

1.4%

1.3%

restricted

cash

0.0%

0.0%

0.0%

0.0%

0.0%

2.4%

other

assets

3.9%

4.4%

5.0%

5.0%

4.6%

3.8%

Deferred

income

taxes

3.3%

2.8%

2.7%

2.3%

3.2%

4.3%

Total

Assets

66.6%

69.4%

57.7%

66.0%

73.3%

70.0%

Current

Liabilities

Accounts

payable

and

other

current

liabilities

14.5%

15.8%

13.0%

13.0%

14.1%

14.8%

Income

taxes

payable

0.4%

0.5%

1.0%

0.8%

0.5%

1.1%

Short-‐term

borrowing

2.4%

2.8%

0.2%

0.5%

5.9%

2.5%

Advertising

cooperative

liabilities

0.8%

0.7%

1.0%

0.9%

1.0%

0.9%

Total

current

liabilities

18.0%

19.8%

15.2%

15.3%

21.6%

19.4%

Long

Term

Debt

21.4%

28.0%

31.5%

29.6%

25.7%

23.7%

Other

liabilities

and

deferred

credits

12.0%

10.7%

11.8%

10.8%

11.3%

11.7%

Total

Liabilities

51.4%

58.5%

58.6%

55.7%

58.6%

54.8%

Shareholder's

Equity

Common

Stock

0.0%

0.0%

0.0%

2.3%

0.8%

0.1%

Retained

Earning

16.8%

10.7%

2.7%

9.2%

15.1%

16.3%

Accumulated

other

comprehensive

loss

-‐1.6%

0.2%

-‐3.7%

-‐2.1%

-‐2.0%

-‐2.0%

Total

15.2%

10.9%

-‐1.0%

9.5%

13.9%

14.4%

Non-‐controlling

interest

0.0%

0.0%

0.1%

0.8%

0.8%

0.7%

Total

Shareholder's

Equity

0.0%

0.0%

-‐0.8%

10.3%

14.7%

15.2%

Total

Liabilities

and

Shareholder's

Equity

66.6%

69.4%

57.7%

66.0%

73.3%

70.0%