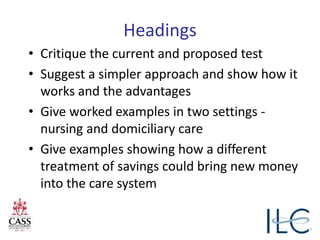

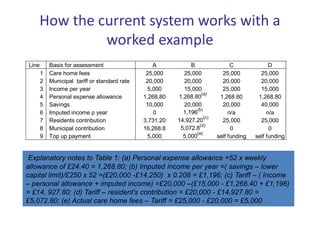

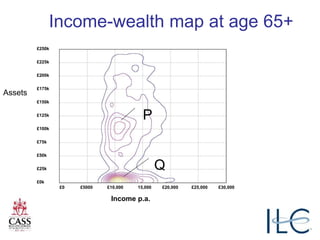

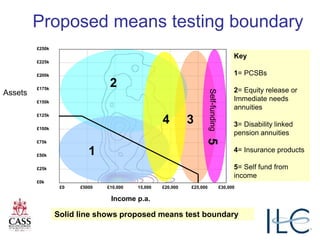

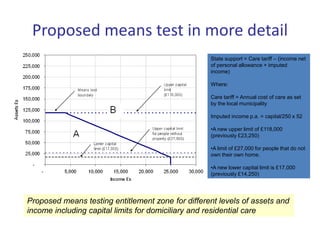

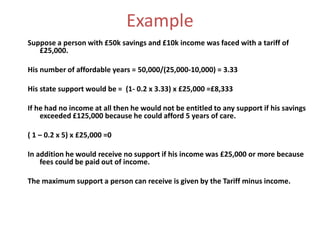

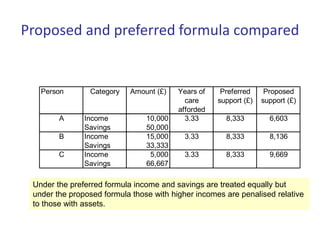

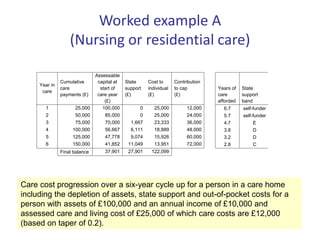

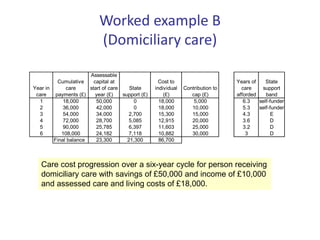

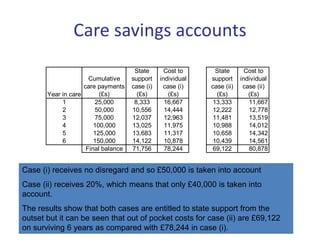

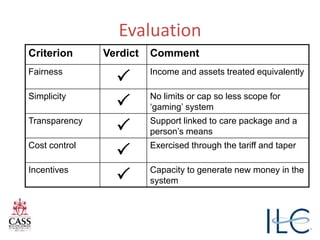

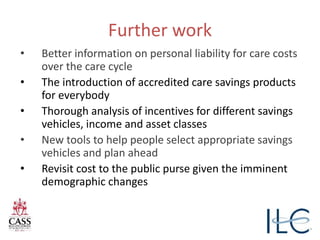

The document discusses the need for reform in the means-testing and funding of adult social care in England, highlighting the inadequacies and complexities of current systems. It proposes a simpler, fairer approach that treats income and savings equitably while aiming to attract new funding into the care system. Additionally, it critiques potential new means-testing boundaries and financial disincentives, ultimately suggesting mechanisms to reward savings for care.

![Ad presentation to lga summit 13th july[1]](https://cdn.slidesharecdn.com/ss_thumbnails/adpresentationtolgasummit13thjuly1-110720113424-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)