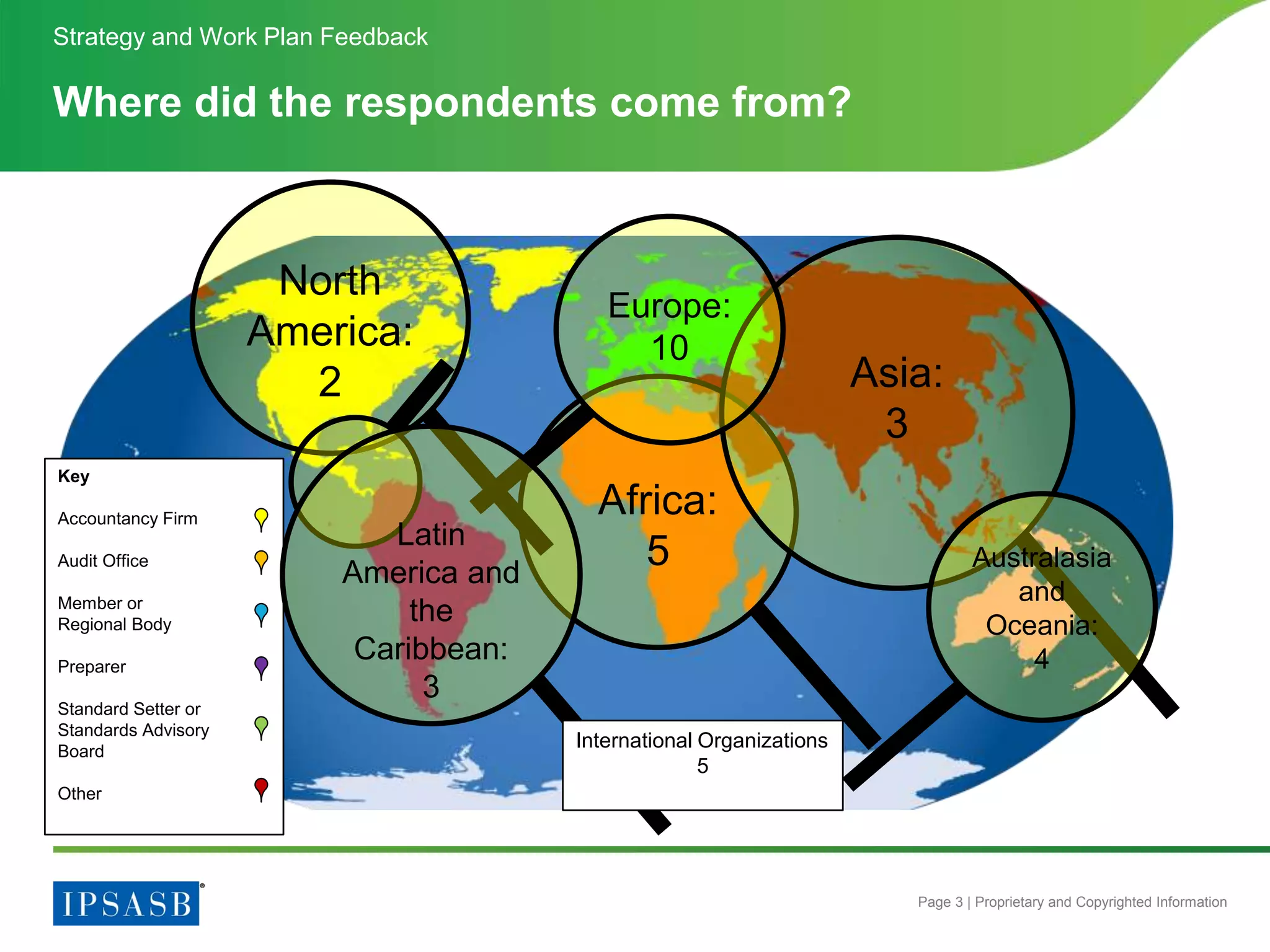

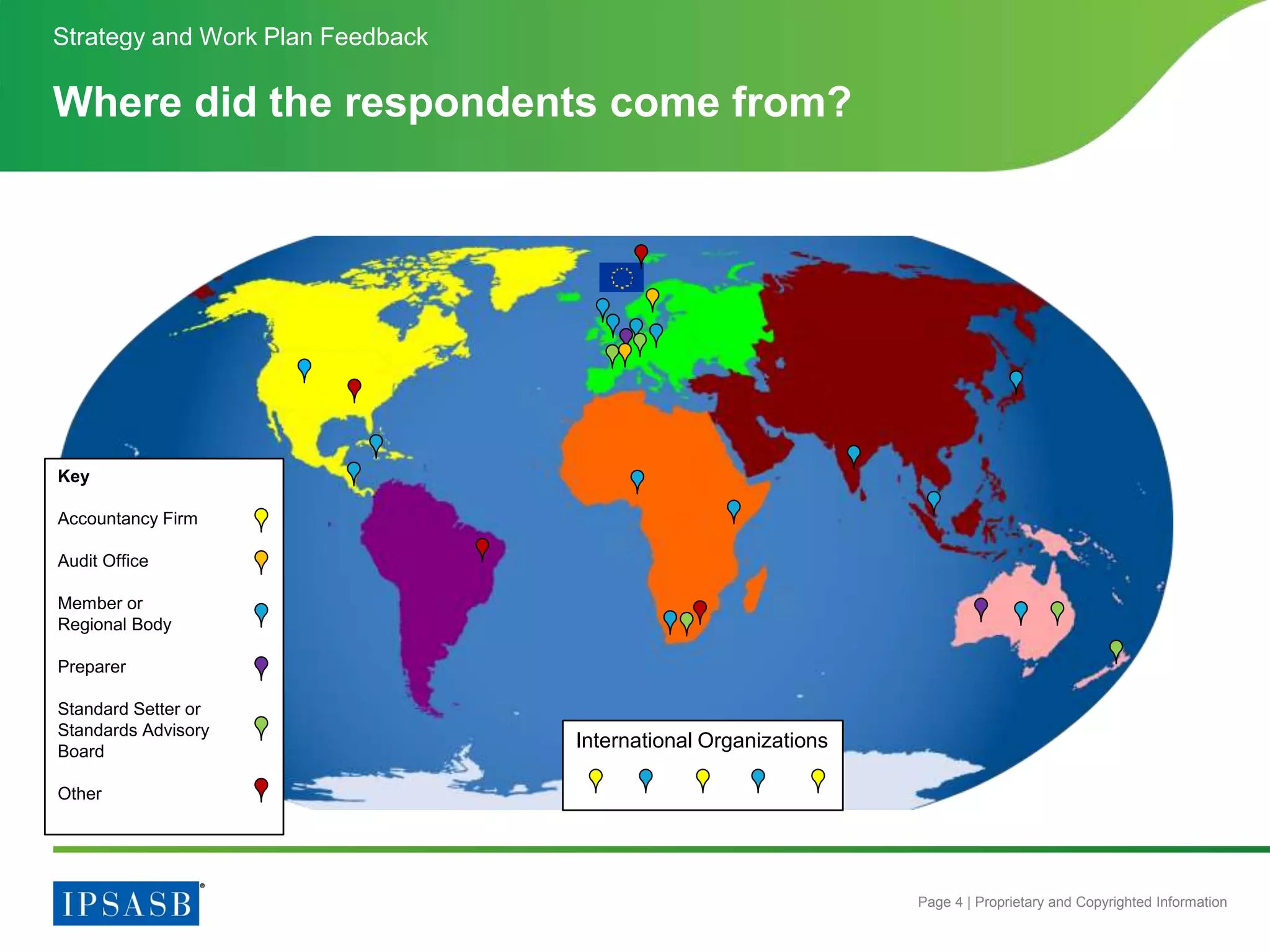

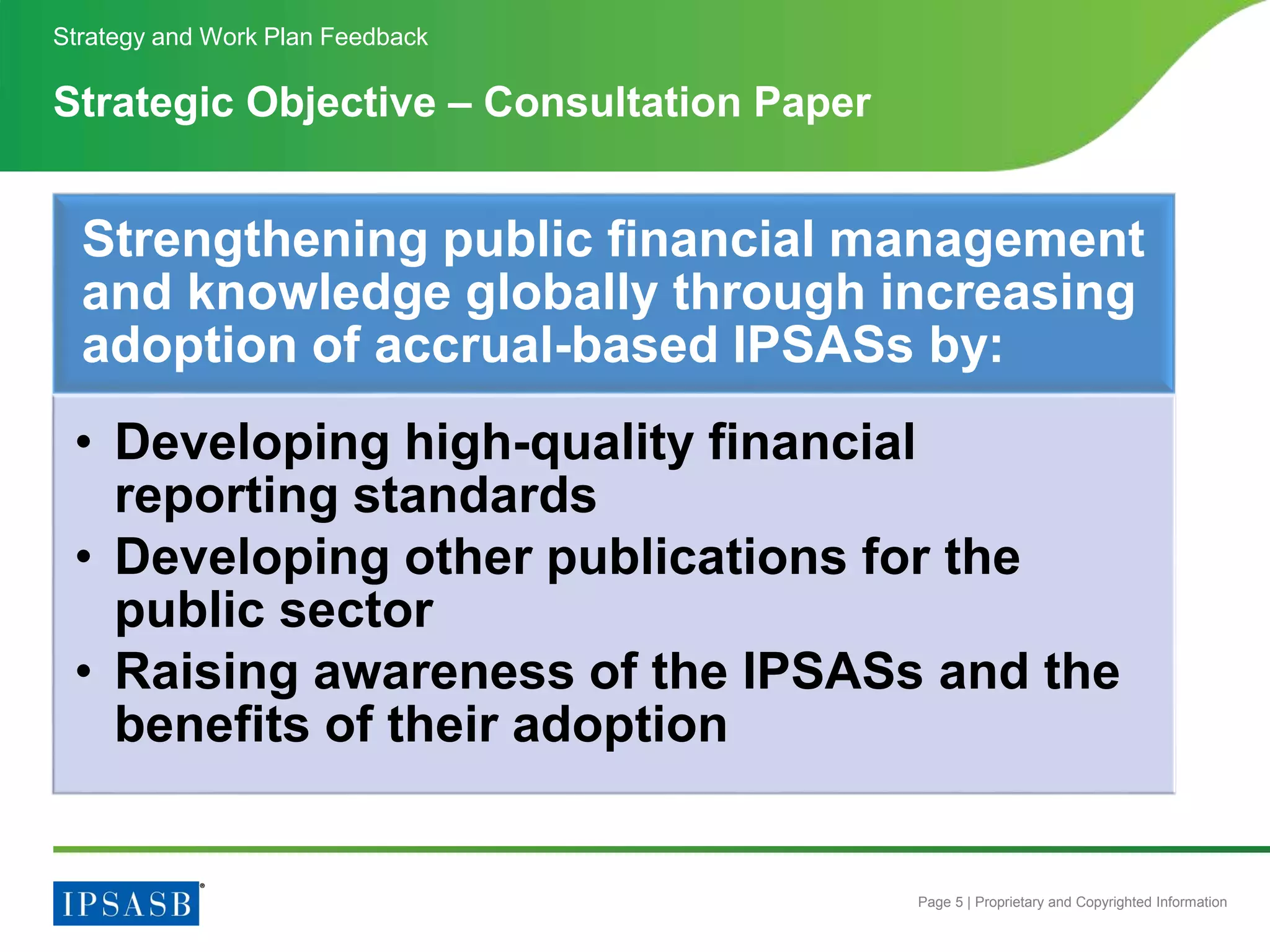

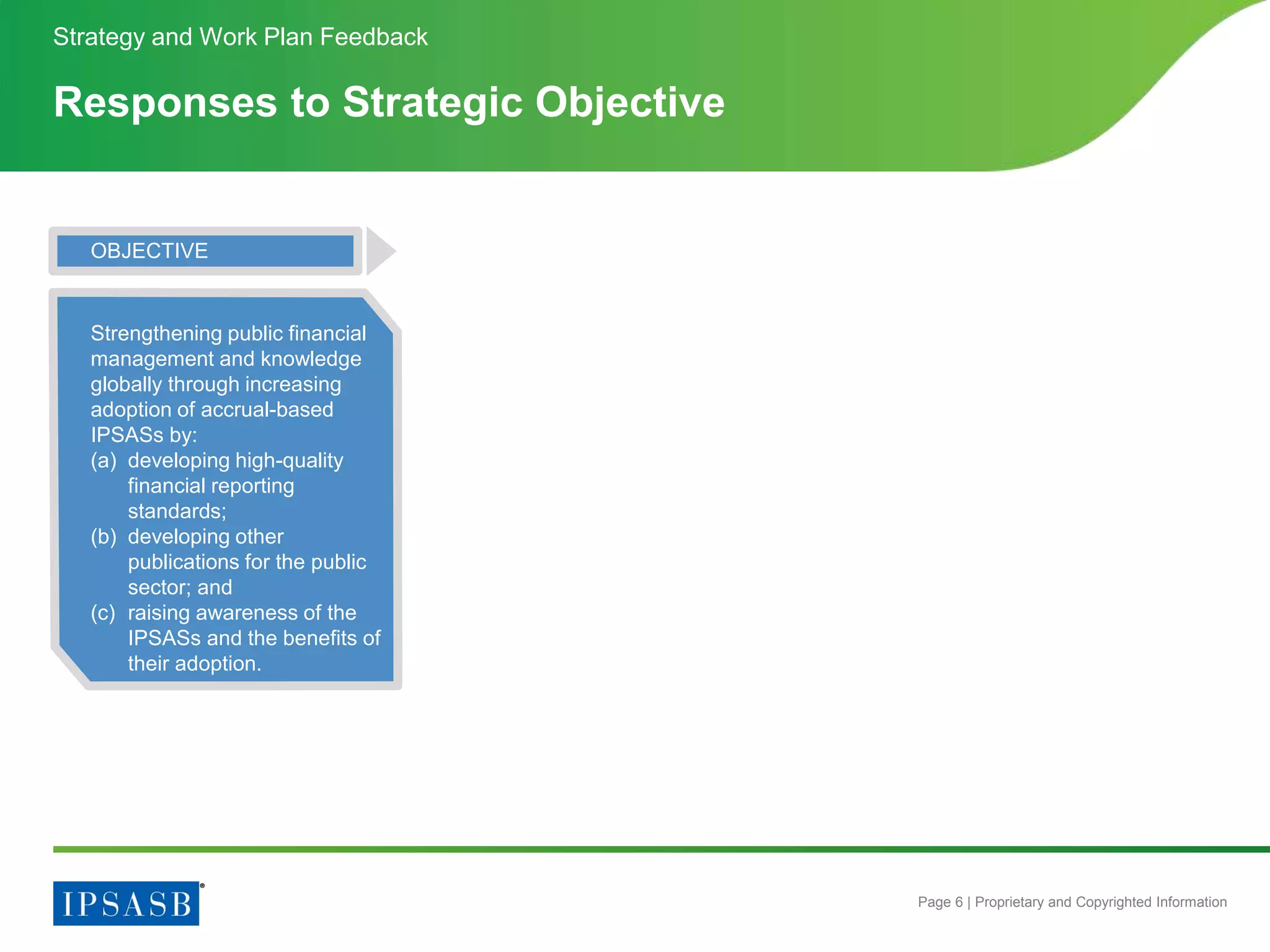

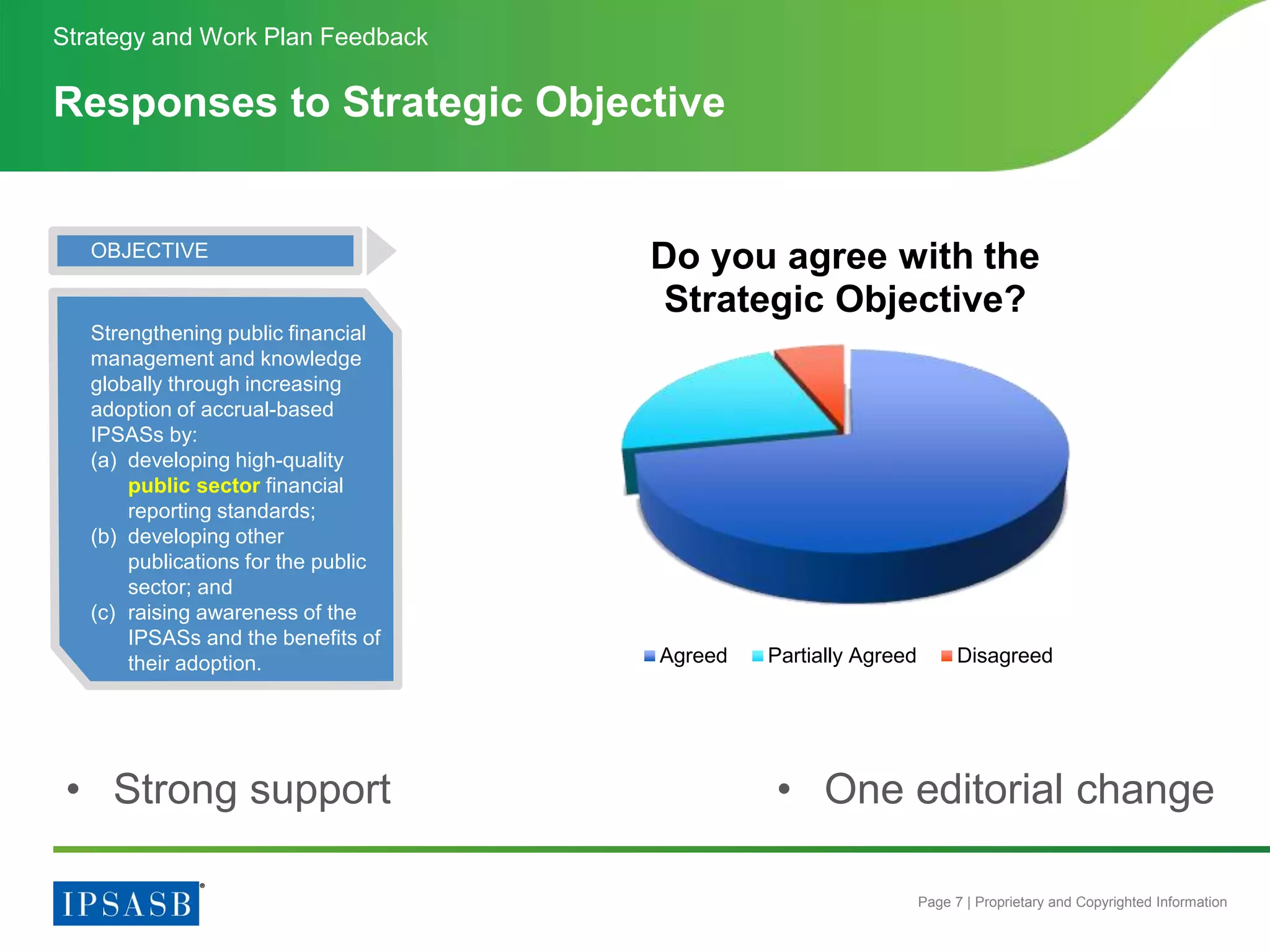

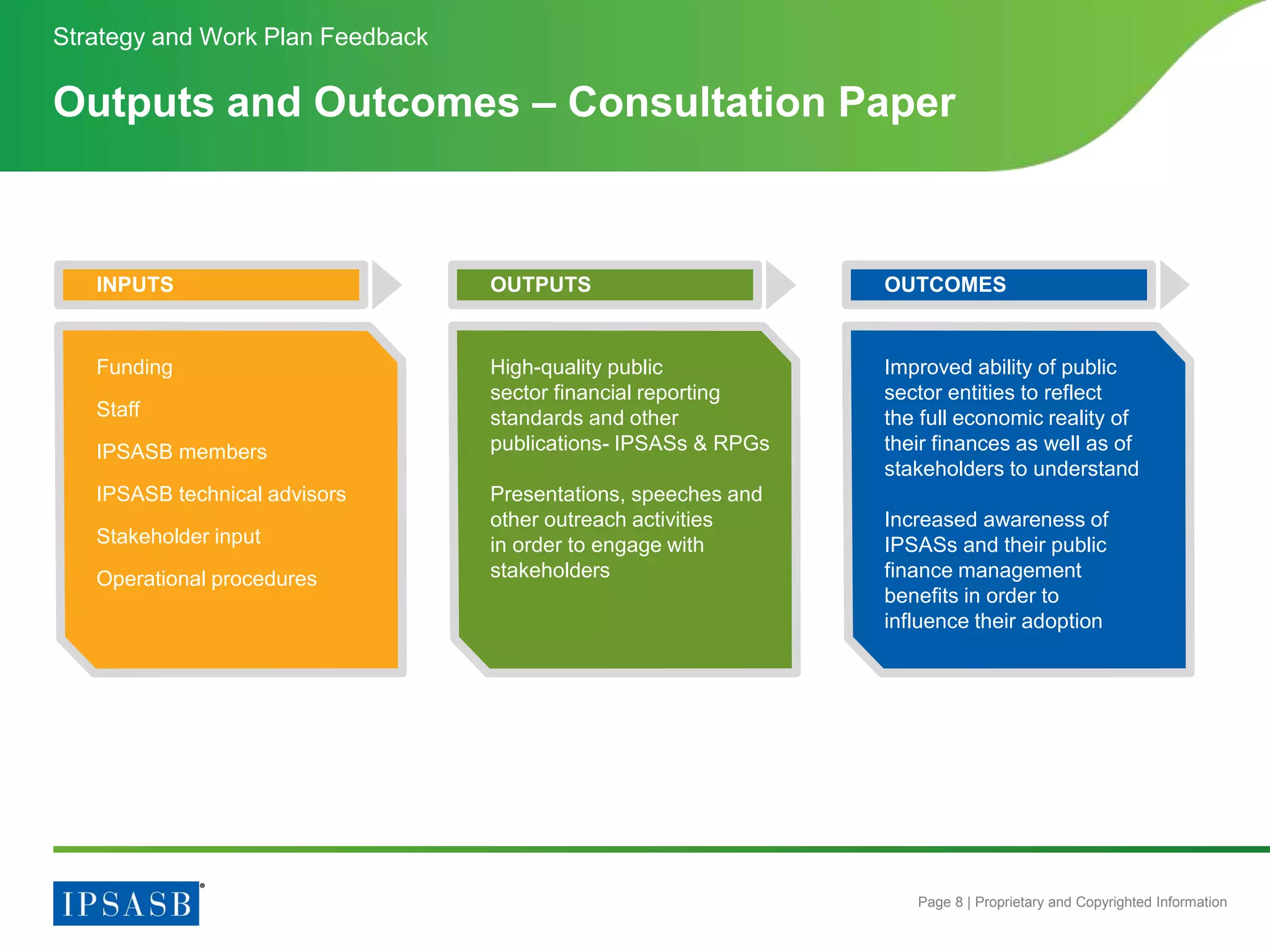

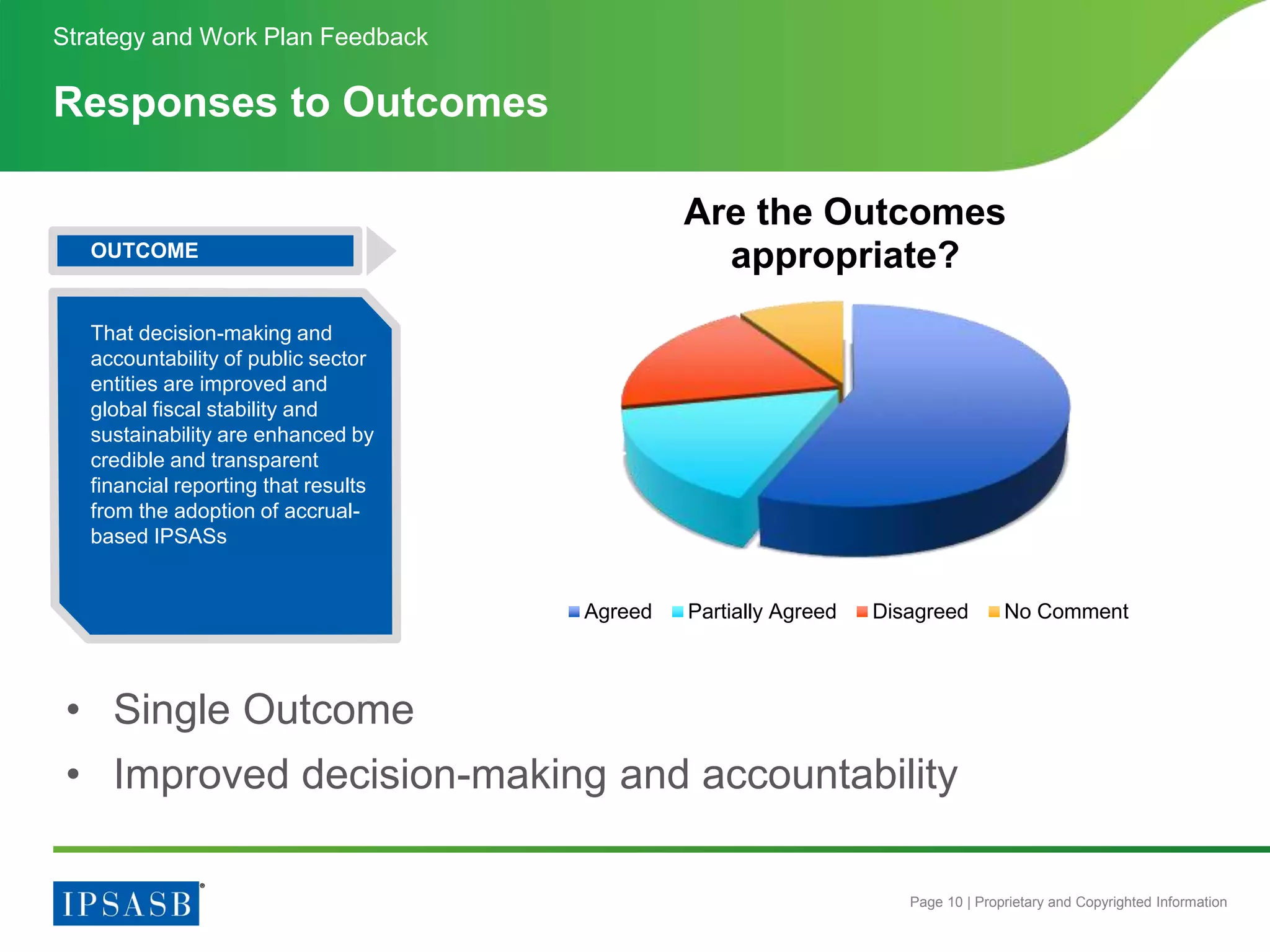

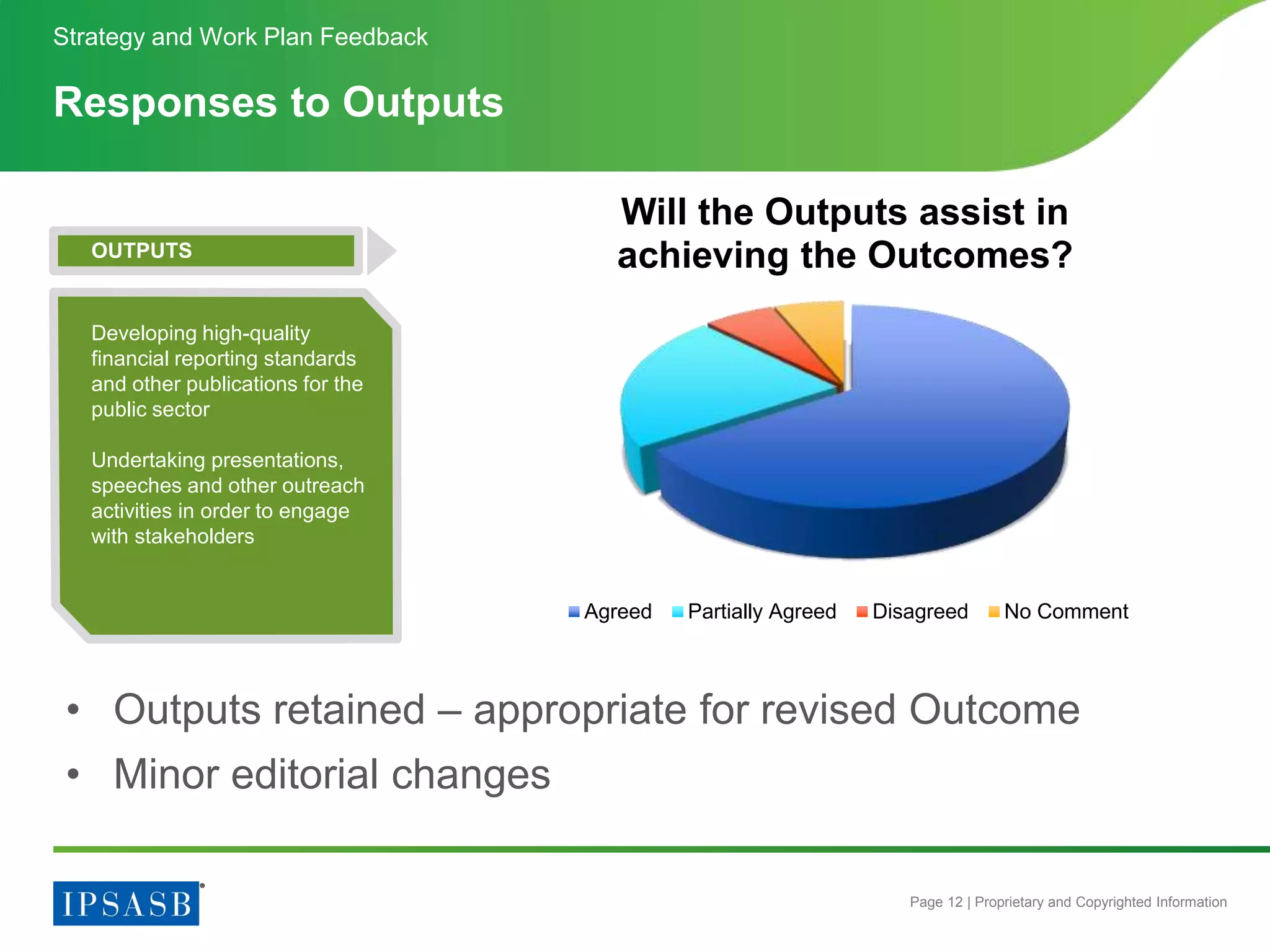

The document summarizes feedback received on the IPSASB's strategy and work plan. It includes: - Responses came from various regions, with most from Europe. - Stakeholders strongly supported the strategic objective of strengthening public financial management globally. - Feedback supported modifying the single outcome to focus on improved decision-making and accountability. - The outputs of developing standards and publications and stakeholder engagement were deemed appropriate.

![01_INTRODUCTION_TO_PUBLIC_SECTOR_REPORTING-1[1].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/01introductiontopublicsectorreporting-11-250711045942-40314283-thumbnail.jpg?width=640&height=640&fit=bounds)