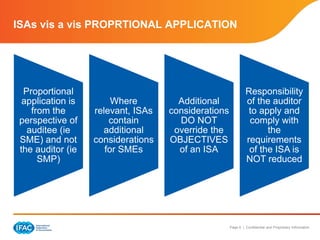

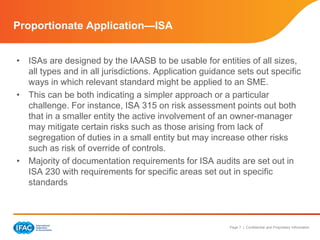

The document outlines the application of International Standards on Auditing (ISAs) and their proportional application in audits for small and medium enterprises (SMEs). It emphasizes the importance of tailoring audit strategies to the size and complexity of the entity while ensuring compliance with standard requirements. Specific audit procedures, documentation expectations, and considerations related to internal controls and related party transactions are also discussed in the context of SMEs.