![The ISAs and micro-entity audits

You only need to comply with:

A) Relevant ISAs [200.18]

B) Relevant Requirements [200.22]

But you do need to comply with all of these in every audit

Page 4 | Confidential and Proprietary Information](https://image.slidesharecdn.com/session2-pc-120322142016-phpapp01/85/Phil-Cowperthwaite-The-ISAs-and-Micro-Entity-Audits-4-320.jpg)

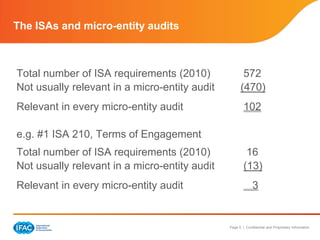

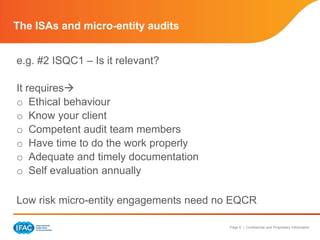

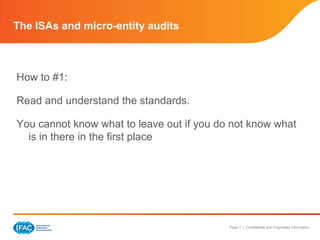

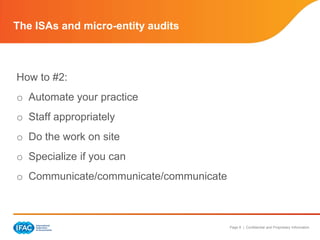

The document discusses proportionately applying International Standards on Auditing (ISAs) to micro-entity audits. It notes that while an audit is an audit, a proportionate approach is possible. Only relevant ISA requirements and relevant ISQC1 requirements must be complied with. For example, in a typical micro-entity audit there are only 102 relevant ISA requirements out of 572 total. It provides examples of how ISA 210 and ISQC1 can be applied proportionately. The document advises auditors to read the standards fully to understand what can be left out and offers tips like automating practices and specializing to efficiently conduct micro-entity audits.

![4_smartid_poster_FINAL_4.21.08[1]](https://cdn.slidesharecdn.com/ss_thumbnails/dd7a276b-d531-4059-9d62-a68bc1a2f630-150818212216-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)