Presentation Outlines

- Introductionon ISAs

- Objective of ISAs

- Scope of this ISAs

- Importance of ISAs

- Audit Regulatory Environment

- ISAs Related to Phase I, Client Acceptance

- ISAs Related to Phase II, Planning the audit

- ISAs Related to Phase III, Testing and Evidence

- ISAs Related to Phase IV, Evaluation and Reporting

05/10/2025

CompiIed by Abdirahman M.

3.

05/10/2025

Introduction of ISAs

International Standards on Auditing (ISAs) are

professional guidelines issued by the International

Auditing and Assurance Standards Board (IAASB).

They provide a framework for the conduct of high-

quality audits of financial statements, ensuring

consistency, transparency, and reliability across global

audit practices.

CompiIed by Abdirahman M.

4.

05/10/2025

Cont…

• ISAs outlinethe responsibilities of auditors and establish

requirements for key areas such as audit planning, risk

assessment, evidence gathering, and reporting.

• They are widely adopted by audit professionals around

the world and serve to enhance investor confidence by

promoting uniformity and credibility in the audit

process.

CompiIed by Abdirahman M.

5.

05/10/2025

Objective of ISA

Themain goal of ISAs is to enhance the quality and

reliability of audits, promote transparency, and

ensure that audits are conducted with

professionalism and due diligence across different

countries and industries.

CompiIed by Abdirahman M.

6.

05/10/2025

The other Objectivesof ISAs

- To enhance the degree of confidence of intended users in

the financial statements.

- To give expression of an opinion by the auditor s on

whether the financial statements are presented fairly.

- As the basis for the auditor’s opinion, ISAs require the

auditor to obtain reasonable assurance about whether the

financial statements as a whole are free from material

misstatement, whether due to fraud or error.

CompiIed by Abdirahman M.

7.

05/10/2025

Scope of thisISA

- This International Standard on Auditing (ISA) deals with

the independent auditor’s overall responsibilities when

conducting an audit of financial statements in accordance

with ISAs.

- Specifically, it sets out the overall objectives of the

independent auditor, and explains the nature and scope of

an audit designed to enable the independent auditor to

meet those objectives. CompiIed by Abdirahman M.

8.

05/10/2025

Importance of ISAs

Enhancing Audit Quality

Promoting Global Consistency

Comparability

Increasing Investor Confidence

Supporting Regulatory Oversight

Facilitating International Trade and Investment

Aiding Auditor Training and Development

Strengthening Public Interest Protection

CompiIed by Abdirahman M.

9.

05/10/2025

Regulatory Environment

IFAC InternationalFederation of Accountants

IFAC code of

ethics

IAASB International Auditing & Assurance

Standard Board.

International

Standards on

Auditing ( ISA,s)

International

Standards on

Quality Control

(ISQC)

CompiIed by Abdirahman M.

05/10/2025

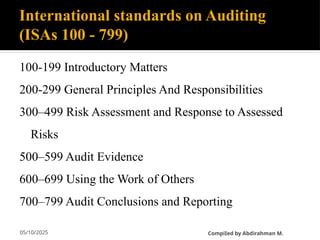

International standards onAuditing

(ISAs 100 - 799)

100-199 Introductory Matters

200-299 General Principles And Responsibilities

300–499 Risk Assessment and Response to Assessed

Risks

500–599 Audit Evidence

600–699 Using the Work of Others

700–799 Audit Conclusions and Reporting

CompiIed by Abdirahman M.

12.

05/10/2025

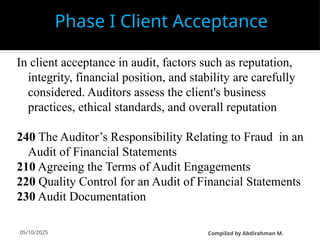

In client acceptancein audit, factors such as reputation,

integrity, financial position, and stability are carefully

considered. Auditors assess the client's business

practices, ethical standards, and overall reputation

240 The Auditor’s Responsibility Relating to Fraud in an

Audit of Financial Statements

210 Agreeing the Terms of Audit Engagements

220 Quality Control for an Audit of Financial Statements

230 Audit Documentation

Phase I Client Acceptance

CompiIed by Abdirahman M.

13.

05/10/2025

Cont…

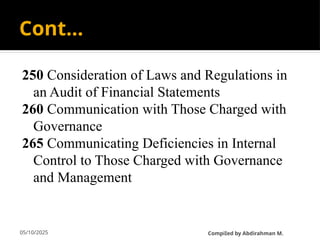

250 Consideration ofLaws and Regulations in

an Audit of Financial Statements

260 Communication with Those Charged with

Governance

265 Communicating Deficiencies in Internal

Control to Those Charged with Governance

and Management

CompiIed by Abdirahman M.

14.

05/10/2025

Cont…

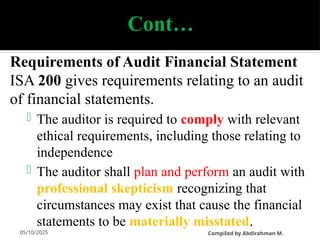

Requirements of AuditFinancial Statement

ISA 200 gives requirements relating to an audit

of financial statements.

The auditor is required to comply with relevant

ethical requirements, including those relating to

independence

The auditor shall plan and perform an audit with

professional skepticism recognizing that

circumstances may exist that cause the financial

statements to be materially misstated.

CompiIed by Abdirahman M.

15.

05/10/2025

Cont…

The auditorshall exercise professional

judgment in planning and performing an

audit of financial statements.

To obtain reasonable assurance, the auditor

must obtain sufficient appropriate audit

evidence to reduce audit risk to an

acceptably low level and thereby enable the

auditor to draw reasonable conclusions on

which to base the auditor’s opinion.

CompiIed by Abdirahman M.

16.

05/10/2025

Cont…

Key Definitions

Professionalskepticism—An attitude that includes a

questioning mind, being alert to conditions which

may indicate possible misstatement due to error or

fraud, and a critical assessment of evidence.

Material misstatement – A significant mistake in

financial information which would arise from errors

and fraud if it could influence the economic

decisions of users taken on the basis of the financial

statements.

CompiIed by Abdirahman M.

17.

05/10/2025

Cont…

Professional judgment—Theapplication of relevant

training, knowledge and experience, within the context

provided by auditing, accounting and ethical standards,

in making informed decisions about the courses of action

that are appropriate in the circumstances of the audit

engagement.

Sufficient appropriate audit evidence – Sufficiency is the

measure of the quantity (amount) of audit evidence.

Appropriateness is the measure of the quality of audit

evidence and its relevance to a particular assertion and

its reliability.

CompiIed by Abdirahman M.

18.

05/10/2025

Cont…

objectives of anaudit of financial statements

ISA 200 states the overall objectives of an audit of financial statements is

1. to obtain reasonable assurance about whether the financial

statements as a whole are free from material misstatement,

whether due to fraud or error, thereby enabling the auditor to

express an opinion towards financial statements

2. communicate as required by the ISAs, in accordance with the

auditor’s findings

Terms used 'give a true and fair view' or ‘present fairly, in all material

respects’ are equivalent terms.

CompiIed by Abdirahman M.

19.

05/10/2025

Phase II Planningthe audit

Planning the audit is a crucial phase in the audit

process where the auditor develops an overall

strategy and detailed approach to conduct the audit

efficiently and effectively.

Key Objectives:

• To understand the client's business and environment.

• To identify and assess risks of material

misstatement.

• To design audit procedures responsive to the

assessed risks.

CompiIed by Abdirahman M.

20.

05/10/2025

Cont…

300-499 Risk AssessmentAnd Response To

Assessed Risks

300 Planning an Audit of Financial Statements

315 Identifying and Assessing the Risks of Material

Misstatement through understanding the Entity and Its

Environment

320 Materiality in Planning and Performing an Audit

330 The Auditor’s Responses to Assessed Risks

402 Audit Considerations Relating to an Entity Using a

Service Organization

450 Evaluation of Misstatements Identified during the Audit

CompiIed by Abdirahman M.

21.

05/10/2025

Cont…

Content of auditstrategy:

Scope of engagement (e.g. input of other

auditors).

Reporting objectives of assignment (e.g.

reporting timetable).

Nature/timing/extent of resources.

Content of audit plan:

Risk assessment procedures.

Detailed planned audit procedures.

CompiIed by Abdirahman M.

22.

05/10/2025

Phase II Planningthe audit

ISA 315 Identifying and assessing the risk of material

misstatement

Required understanding of entity and environment:

Industry/regulatory factors affecting FS.

Nature of entity:

Operations;

Ownership and governance; and

Financing.

CompiIed by Abdirahman M.

05/10/2025

Cont…

ISA 320 Materiality

Materiality: Misstatements, including omissions, are considered to be

material if they, individually or in the aggregate, could reasonably be

expected to influence the economic decisions of users taken on the

basis of the financial statements

Performance materiality: Performance materiality is set at a level

below overall materiality to reduce the probability that the aggregate of

uncorrected and undetected misstatements exceeds overall materiality..

CompiIed by Abdirahman M.

25.

05/10/2025

Cont…

Tolerable error:A monetary amount set by

the auditor in respect of which the auditor

seeks to obtain an appropriate level of

assurance that the monetary amount set by the

auditor is not exceeded by the actual

misstatement in the population.

CompiIed by Abdirahman M.

26.

05/10/2025

Phase III Testingand Evidence

500-599 Audit Evidence

500 Audit Evidence

501 Audit Evidence – Specific Considerations for Selected

Items

505 External Confirmations

510 Initial Audit Engagements—Opening Balances

520 Analytical Procedures

CompiIed by Abdirahman M.

27.

05/10/2025

Cont…

530 Audit Sampling

540Auditing Accounting Estimates and Related Disclosures

Including Fair Value Accounting Estimates, and Related

Disclosures

550 Related Parties

560 Subsequent Events

570 Going Concern

580 Written Representations

CompiIed by Abdirahman M.

28.

05/10/2025

Cont…

600-699 Using WorkOf Others

600 Special Considerations - Audits of Group

Financial Statements (including the work of a

competent auditor)

610 Using the Work of Internal Auditors

620 Using the Work of an Auditor’s Expert

CompiIed by Abdirahman M.

29.

05/10/2025

Cont…

ISA 500 AuditEvidence

Characteristics Audit Evidence :

Appropriateness: quality linked to relevance and reliability.

Sufficiency: quantity linked to quality and to risk of material

misstatement.

Relevance: linked to assertions.

Reliability:

Independent better than internal.

Auditor generated better than indirectly obtained.

Documentary better than oral.

Originals better than photocopies.

CompiIed by Abdirahman M.

30.

05/10/2025

Cont…

ISA 510 InitialAudit Engagement, Opening

balance

Objective: To obtain sufficient appropriate

evidence whether

Opening balances are misstated

Consistency accounting policies with current year

CompiIed by Abdirahman M.

31.

05/10/2025

Cont…

ISA 540 AuditingAccounting Estimates

Accounting estimates are approximations of

amounts in the financial statements that cannot be

precisely measured. These could include:

• Bad debt provisions/expenses

• Inventory obsolescence/wear out

• Fair value of financial instruments

• Depreciation and amortization

• Asset impairments (asset which has a current market value

that is less than the value listed on the balance sheet)

CompiIed by Abdirahman M.

32.

05/10/2025

Cont…

Why Estimates Matter

Estimates involve management judgment

and assumptions, which makes them

inherently risky and vulnerable to bias,

error, or even fraud. As a result, they are a

significant focus during an audit.

CompiIed by Abdirahman M.

33.

05/10/2025

Phase IV, Evaluationand Reporting

700-799 Audit Conclusions And Reporting

700 Forming an Opinion and Reporting on Financial Statements

705 Modifications to the Opinion in the Independent Auditor’s

Report

706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in

the Independent Auditor's Report

710 Comparative Information-Corresponding Figures and

Comparative Financial Statements

720 The Auditor’s Responsibilities Relating to Other Information in

Documents Containing Audited Financial Statements

CompiIed by Abdirahman M.

34.

05/10/2025

Cont…

ISA 700– Forming an Opinion and Reporting

on Financial Statements

ISA 700 provides guidance to auditors on how to

form an opinion on the financial statements and

how to communicate that opinion through the

auditor’s report.

CompiIed by Abdirahman M.

35.

05/10/2025

Cont…

The auditor must:

Form an opinion on whether the

financial statements:

1.Are prepared in accordance with the

applicable financial reporting framework

2.Give a true and fair view or are presented

fairly, in all material respects

Issue a written audit report that

clearly expresses that opinion.

CompiIed by Abdirahman M.

36.

05/10/2025

Cont…

ISA 705 Modificationof Audit Opinion

Sometimes, the auditor can't give a clean

(unmodified) opinion. ISA 705 guides auditors

on when and how to modify their opinion in

such cases.

CompiIed by Abdirahman M.

37.

05/10/2025

Cont…

When is aModified Opinion Required?

A modification is needed if:

There is a material issue but not pervasive

There is a material and pervasive misstatement in

the financial statements, or

The auditor is unable to obtain sufficient

appropriate audit evidence

CompiIed by Abdirahman M.

38.

05/10/2025

Cont…

Types of ModifiedOpinions

A. Qualified Opinion

🔹 Used when the issue is material but not pervasive

B. Adverse Opinion

🔹 When the misstatement is both material and pervasive

C. Disclaimer of Opinion

🔹 When the auditor cannot obtain sufficient evidence

and the effects could be material and pervasive

CompiIed by Abdirahman M.

#11 Class Question: What is the process of auditing? Illustration 1.1 List of 2004 International Standards on Auditing pages 8-9;

Updated International Federation of Accountants. 2010. Handbook Of International Quality Control, Auditing, Review, Other Assurance, And Related Services Pronouncements 2010 Edition Part I

#12 Class Question: What is risk? Illustration 1.1 List of 2004 International Standards on Auditing pages 8-9

320 (Revised and Redrafted), Materiality in Planning and Performing an Audit

#14 ISA 200 sets out several requirements relating to an audit of financial statements. The auditor is required to comply with relevant ethical requirements, including those pertaining to independence, relating to financial statement audit engagements The auditor shall plan and perform an audit with professional skepticism recognizing that circumstances may exist that cause the financial statements to be materially misstated. The auditor shall exercise professional judgment in planning and performing an audit of financial statements. To obtain reasonable assurance, the auditor must obtain sufficient appropriate audit evidence to reduce audit risk to an acceptably low level and thereby enable the auditor to draw reasonable conclusions on which to base the auditor’s opinion.

Ibid. ISA 200. Paragraphs 14–17.

Professional skepticism—An attitude that includes a questioning mind, being alert to conditions which may indicate possible misstatement due to error or fraud, and a critical assessment of evidence. Discussed in more detail in Chapter 4.

Material misstatement – A significant mistake in financial information which would arise from errors and fraud if it could influence the economic decisions of users taken on the basis of the financial statements.

Professional judgment—The application of relevant training, knowledge and experience, within the context provided by auditing, accounting and ethical standards, in making informed decisions about the courses of action that are appropriate in the circumstances of the audit engagement. Discussed in more detail in Chapter 4.

Sufficient appropriate audit evidence – Sufficiency is the measure of the quantity (amount) of audit evidence. Appropriateness is the measure of the quality of audit evidence and its relevance to a particular assertion and its reliability. We will discuss evidence at some length in Chapters 9 and 10.

#16 Professional skepticism—An attitude that includes a questioning mind, being alert to conditions which may indicate possible misstatement due to error or fraud, and a critical assessment of evidence. Discussed in more detail in Chapter 4.

Material misstatement – A significant mistake in financial information which would arise from errors and fraud if it could influence the economic decisions of users taken on the basis of the financial statements.

Professional judgment—The application of relevant training, knowledge and experience, within the context provided by auditing, accounting and ethical standards, in making informed decisions about the courses of action that are appropriate in the circumstances of the audit engagement. Discussed in more detail in Chapter 4.

Sufficient appropriate audit evidence – Sufficiency is the measure of the quantity (amount) of audit evidence. Appropriateness is the measure of the quality of audit evidence and its relevance to a particular assertion and its reliability. We will discuss evidence at some length in Chapters 9 and 10.

#20 Class Question: What is audit evidence? Illustration 1.1 List of 2004 International Standards on Auditing pages 8-9

#26 Class Question: Why would an auditor need to use the assistance of someone else? Illustration 1.1 List of 2004 International Standards on Auditing pages 8-9

Class Question: What is an audit opinion?

#27 Class Question: Why would an auditor need to use the assistance of someone else? Illustration 1.1 List of 2004 International Standards on Auditing pages 8-9

Class Question: What is an audit opinion?

#33 Class Question: What kinds of audit opinions are there? Illustration 1.1 List of 2004 International Standards on Auditing pages 8-9