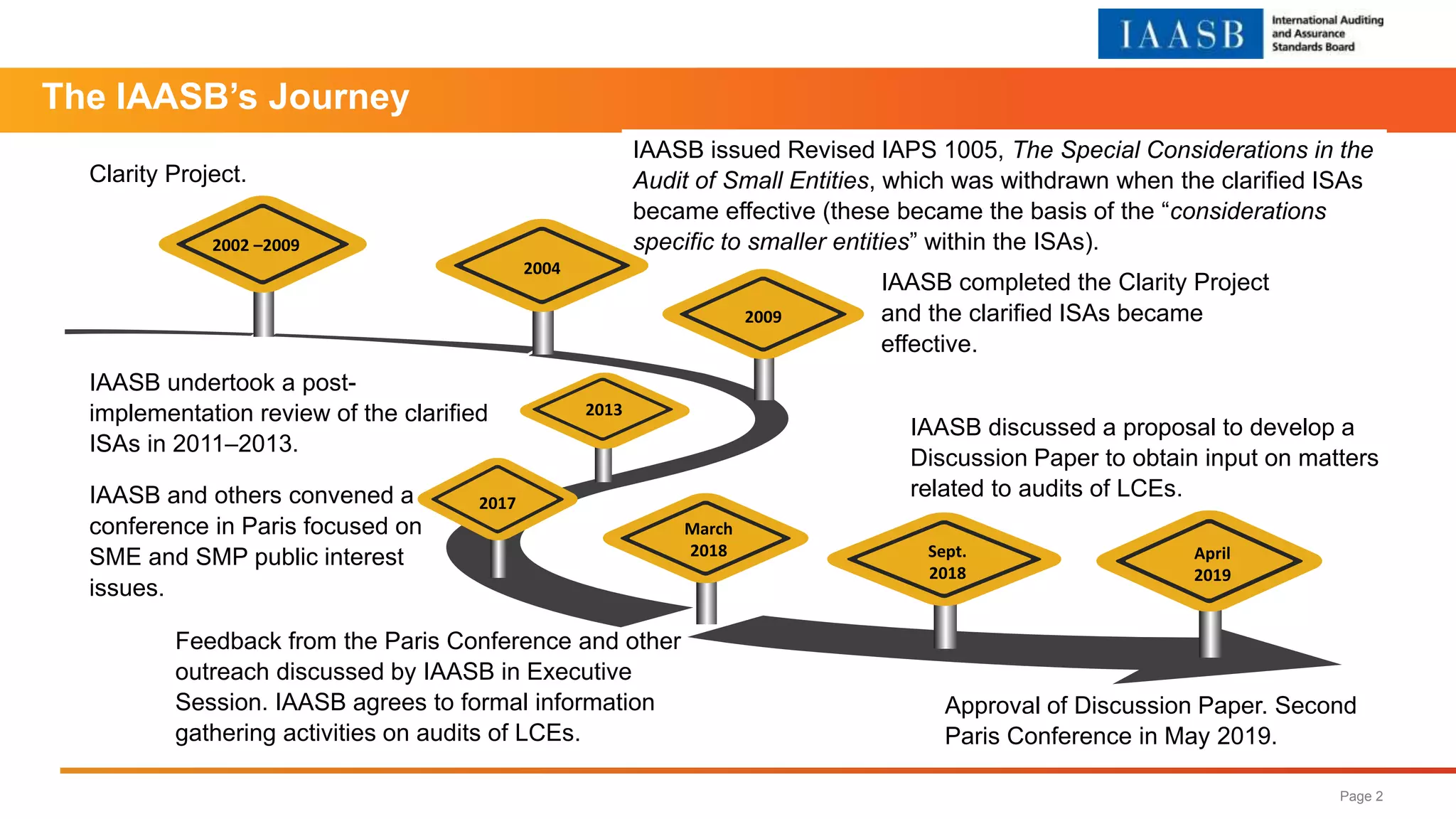

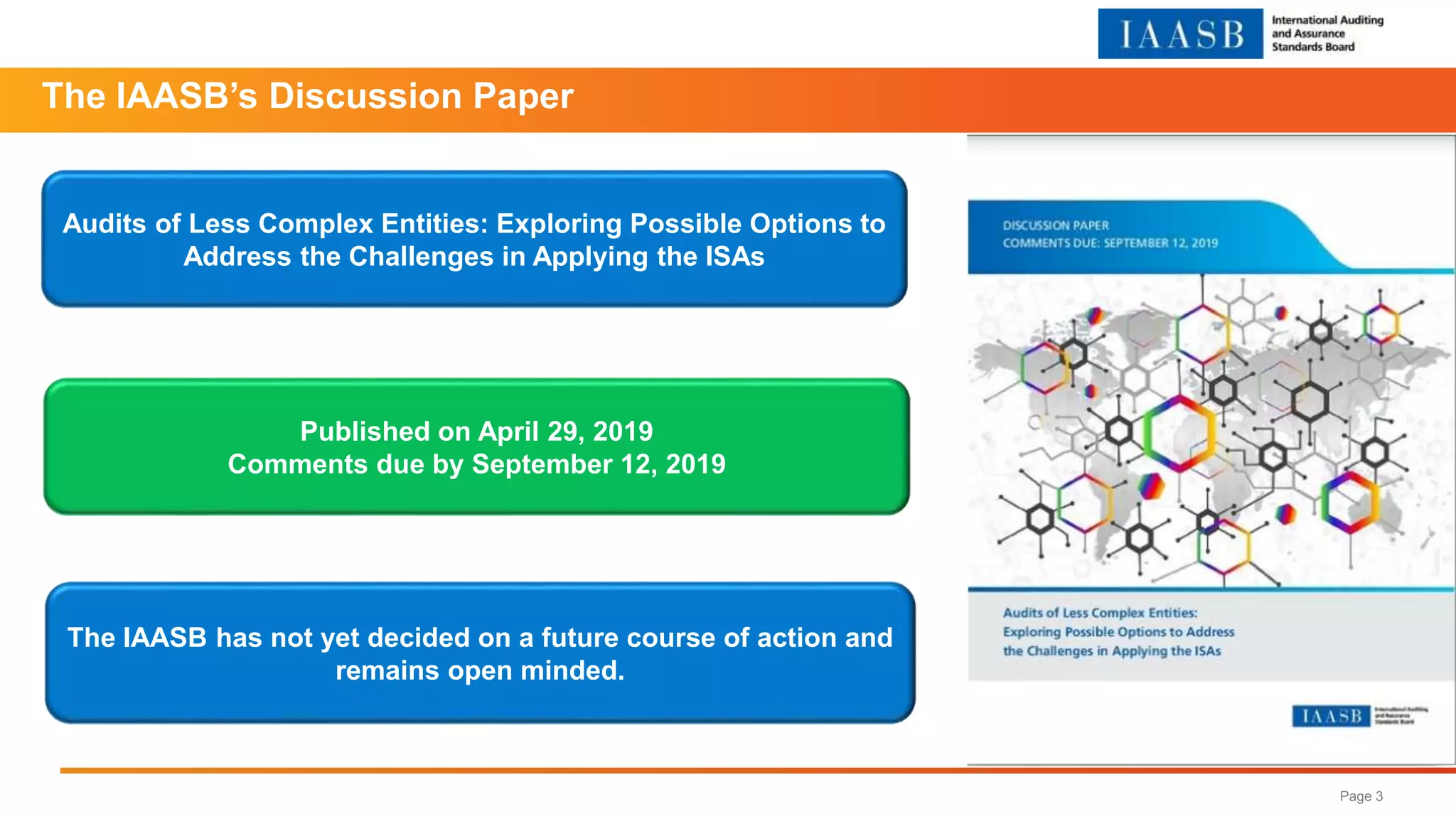

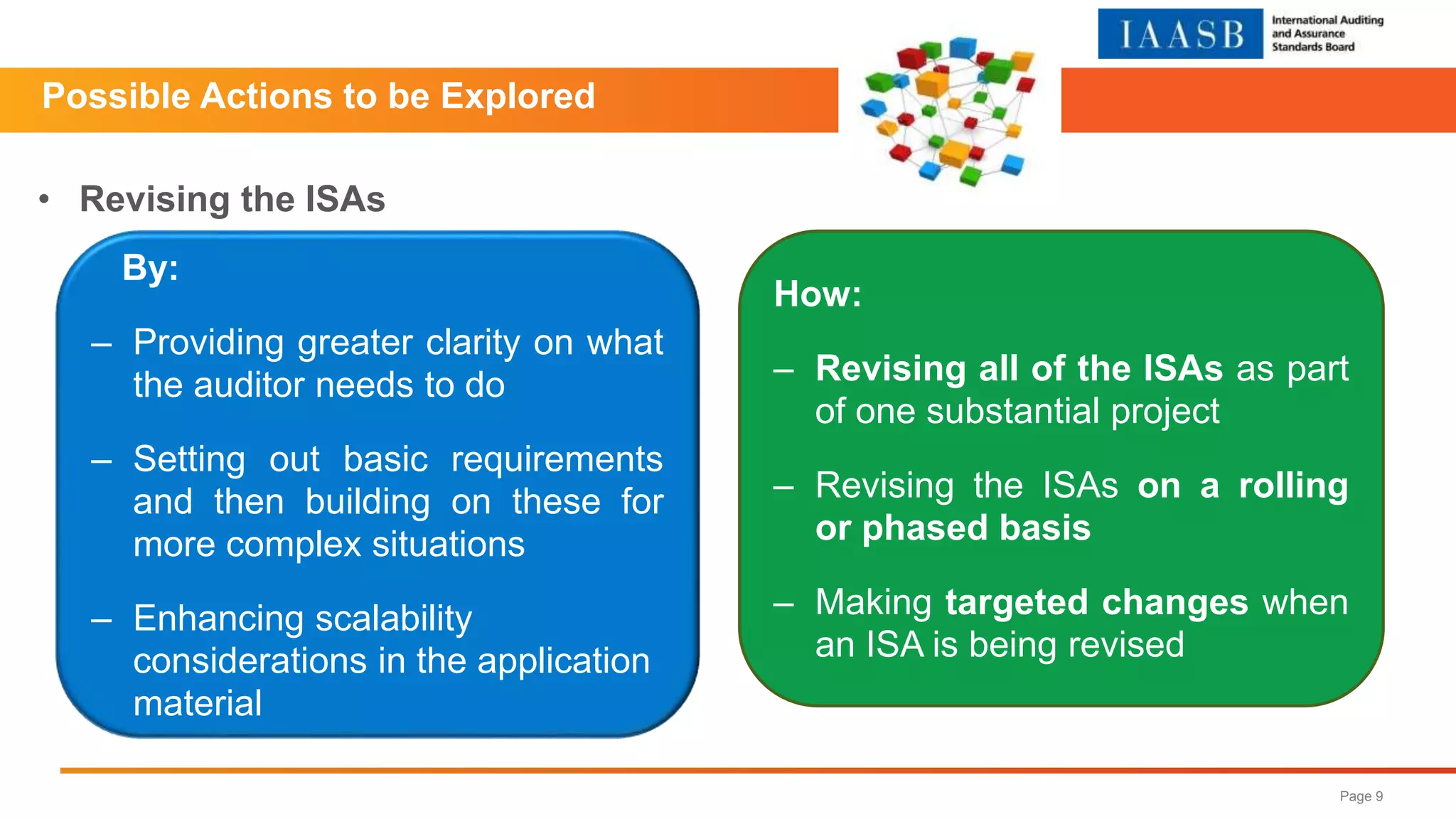

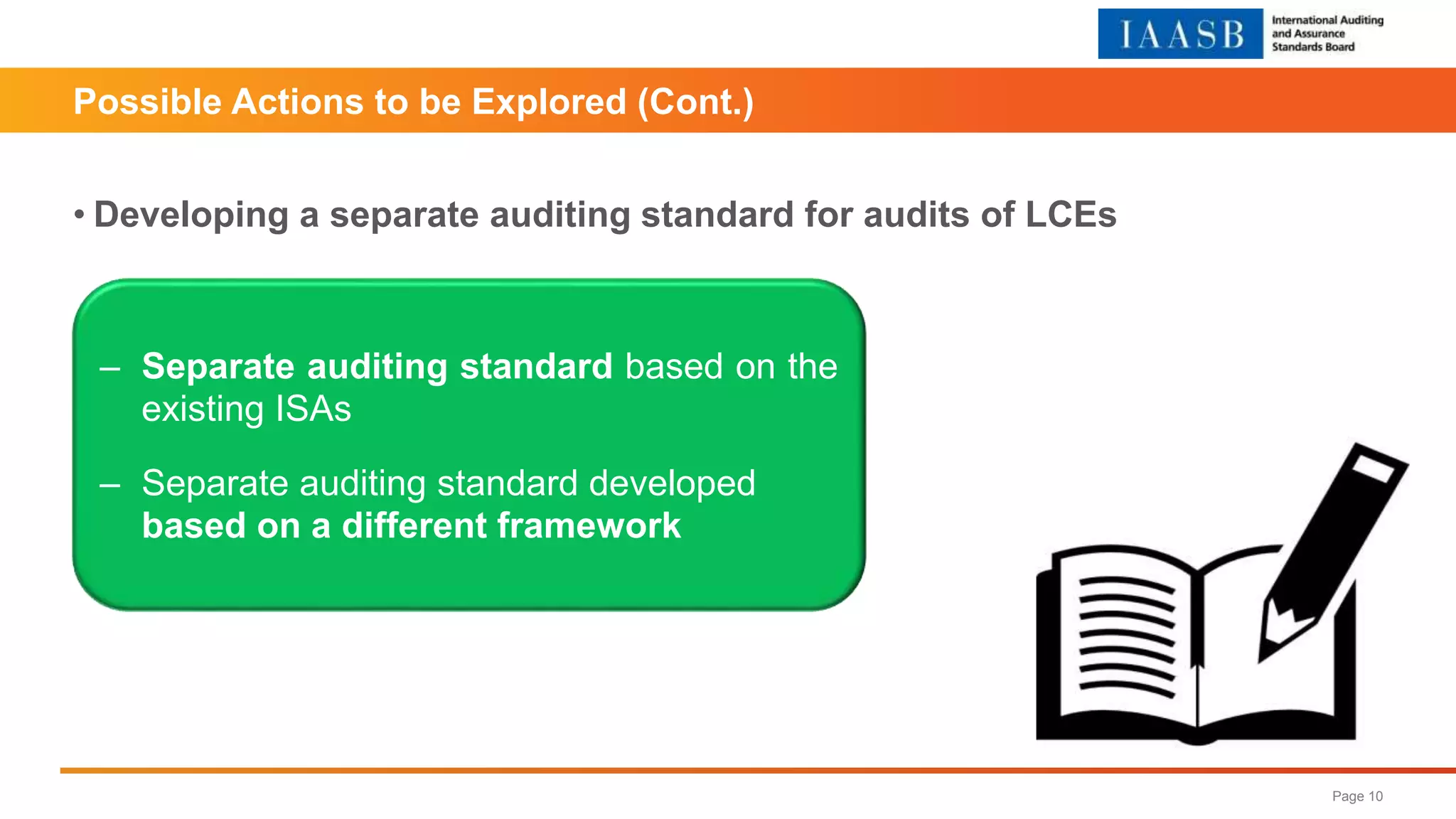

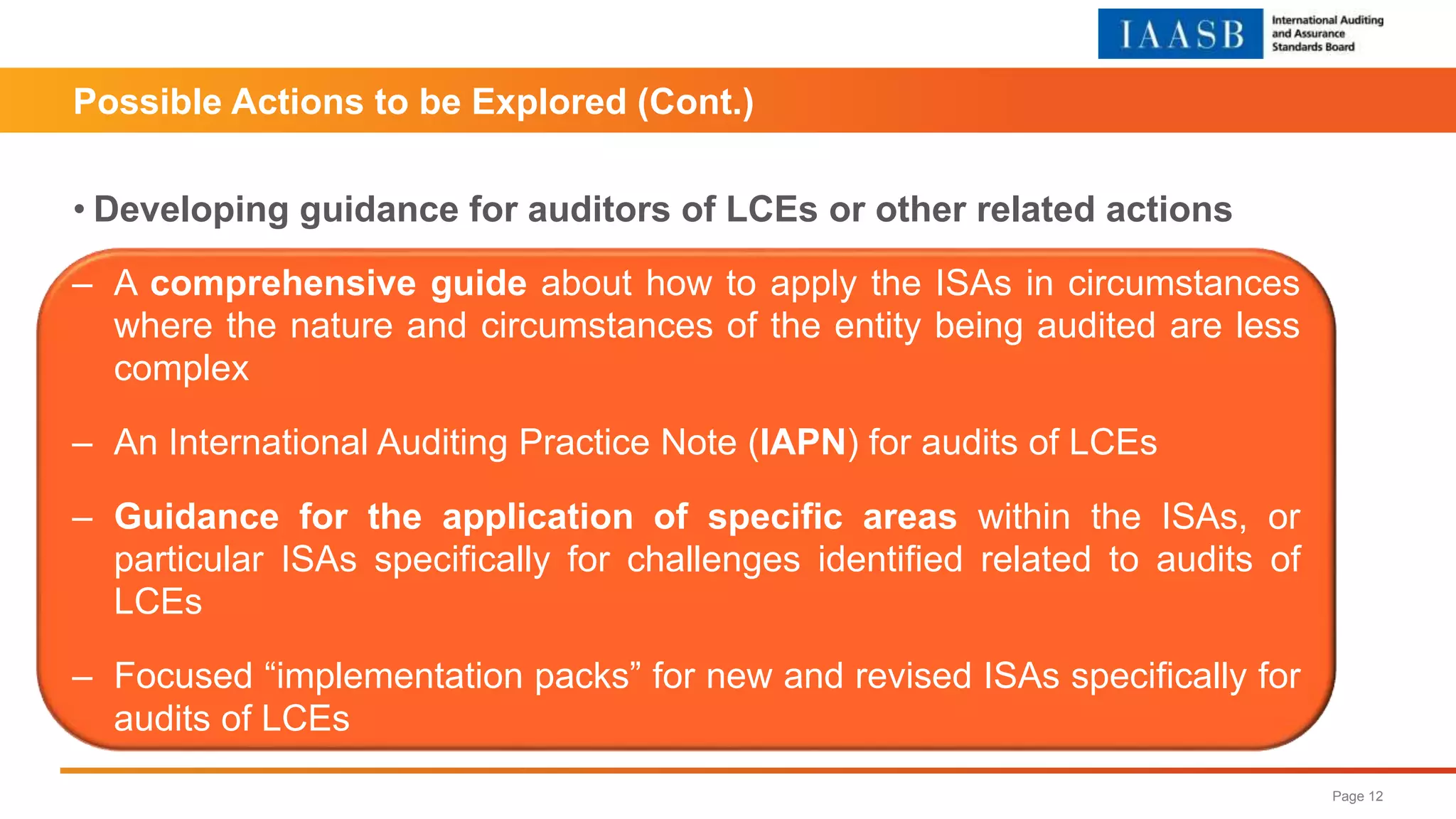

The IAASB is reviewing audits of less complex entities (LCEs) to address challenges related to the application of International Standards on Auditing (ISAs). A discussion paper was published in April 2019 to gather feedback, with a deadline for comments set for September 12, 2019, and several potential actions for revising the ISAs included. The IAASB plans to analyze feedback and make recommendations for future direction in early 2020.