GAAP and Accounting Policies

1) The document discusses the key aspects of Accounting Standard 1 (AS-1) regarding disclosure of accounting policies, including the meaning of accounting policies, disclosure requirements of fundamental accounting assumptions, factors to consider when selecting accounting policies, and disclosing changes in accounting policies. 2) Fundamental accounting assumptions include going concern, consistency, and accrual. Significant accounting policies adopted must be disclosed as part of the financial statements in a single place. 3) Key considerations for selecting accounting policies are providing a true and fair view, prudence, substance over form, and materiality. Any changes in accounting policies that materially affect the financial statements must be disclosed along with the financial impact.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to GAAP and Accounting Policies

Similar to GAAP and Accounting Policies (20)

Recently uploaded

Recently uploaded (20)

GAAP and Accounting Policies

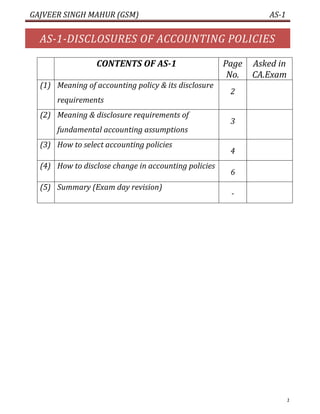

- 1. GAJVEER SINGH MAHUR (GSM) AS-1 1 AS-1-DISCLOSURES OF ACCOUNTING POLICIES CONTENTS OF AS-1 Page No. Asked in CA.Exam (1) Meaning of accounting policy & its disclosure requirements 2 (2) Meaning & disclosure requirements of fundamental accounting assumptions 3 (3) How to select accounting policies 4 (4) How to disclose change in accounting policies 6 (5) Summary (Exam day revision) -

- 2. GAJVEER SINGH MAHUR (GSM) AS-1 2 1. Meaning of Accounting policy & How to disclose Accounting policies Accounting policy 1) All significant accounting policies adopted in the preparation and presentation of financial statements should be disclosed. 2) The disclosure of the significant accounting policies as such should form part of the financial statements. 3) The significant accounting policies should normally be disclosed in one place. Note: It is not appropriate to scatter the disclosures of accounting policies over the financial statement. For example, it is not correct to disclose depreciation policy as part of schedule of fixed assets and inventory policy as part of schedule of inventory. Note: Being a part of the financial statement, the opinion of auditors shall cover the disclosures of accounting policies. How to disclose Accounting policy Page no 8

- 3. GAJVEER SINGH MAHUR (GSM) AS-1 3 Explanation of meaning of Accounting policy Accounting policies Specific Accounting principles Methods of applying those accounting principles in preparation & presentation of Financial Statement Eg. Stock should be valued at COST or NRV , whichever is less and Eg, cost of stock may be calculated by using FIFO or Weight average method 2. Meaning & disclosure requirements of Fundamental Accounting Assumptions Meaning of fundamental Accounting Assumptions (FAA) 1) It is generally assumed that financial statements are prepared on the basis of fundamental accounting assumption. 2) Fundamental accounting assumptions are: i) Going concern ii) Consistency iii) Accrual Going concern The financial statements are normally prepared on the assumption that an enterprise will continue its operations in the foreseeable future and neither

- 4. GAJVEER SINGH MAHUR (GSM) AS-1 4 there is intention, nor there is need to materially curtail the scale of operations. Note: foreseeable future means coming one or two years. Consistency The principle of consistency refers to the practice of using same accounting policies for similar transactions in all accounting periods. Accrual Under this basis of accounting, transactions are recognised as soon as they occur, whether or not cash or cash equivalent is actually received or paid. Note: Section 209(3)(b) of the Companies Act makes it mandatory for companies to maintain accounts on accrual basis only. How to disclose FAA 1) If fundamental accounting assumptions has been followed, then no need to disclose in financial statement. 2) If fundamental accounting assumptions has not been followed, then this fact must be disclosed in financial statement. 3. How to select accounting policies Primary factor Selected accounting policies should present true & fair view of state of affairs of B/S & P/L A/c. Secondary factor Following factors should be considered for selecting accounting policies: i) Prudence

- 5. GAJVEER SINGH MAHUR (GSM) AS-1 5 ii) Substance over form iii) Materiality Prudence 1) Selected accounting policies should consider prudence concept. 2) As per prudence concept, recognise all future losses but don’t recognise future income. 3) The most common example of exercise of prudence in selection of accounting policy is the policy of valuing inventory at lower of cost and net realisable value. Eg. Provision for warranty. Substance over form(law) 1) Selected accounting policies should record transactions on the basis of substance of transaction not only on the basis of legal form. 2) Transactions and other events should be accounted for and presented in accordance with their substance and financial reality and not merely with their legal form. 3) The most common example of exercise of substance over form in selection of accounting policy is the policy of recording assets in the books of hire purchaser though he is not the legal owner of the assets Materiality 1) Selected accounting policies should disclose all material items. Note: Material items-those items, the knowledge of which might influence the decisions of the user of the financial statement. Note: examples of materiality as per (REVISED SCH-VI)

- 6. GAJVEER SINGH MAHUR (GSM) AS-1 6 i) A company shall disclose by way of notes additional information regarding any item of income or expenditure which exceeds 1% of the revenue from operations or ₹1,00,000 whichever is higher ii) A company shall disclose in Notes to Accounts, shares in the company held by each shareholder holding more than 5 per cent shares specifying the number of shares held. 4. How to disclose change in accounting policies (AS Text) Reason of change in accounting policies A change in an accounting policy should be made only if the adoption of a different accounting policy is: 1) Required by statute or 2) For compliance with an accounting standard or 3) If it is considered that the change would result in a more appropriate presentation of the financial statements of the enterprise. How to disclose 1) Any change in the accounting policies which has a material effect in the current period or which is reasonably expected to have a material effect in a later period should be disclosed. 2) In the case of a change in accounting policies,

- 7. GAJVEER SINGH MAHUR (GSM) AS-1 7 which has a material effect in the current period, the amount by which any item in the financial statements is affected by such change should also be disclosed to the extent ascertainable. 3) Where such amount is not ascertainable, wholly or in part, the fact should be indicated. Example of disclosure of change in accounting policy 1) A simple disclosure that an accounting policy has been changed is not of much use for a reader of a financial statement. 2) The effect of change should therefore be disclosed wherever ascertainable. 3) Suppose a company has switched over to weighted average formula for ascertaining cost of inventory, from the earlier practice of using FIFO. If the closing inventory by FIFO is ₹ 2 lakh and that by weighted average formula is ₹1.8 lakh, the change in accounting policy pulls down profit and value of inventory by ₹ 20,000. The company may disclose the change in accounting policy in the following manner: ‘The company values its inventory at lower of cost and net realisable value. Since net realisable value of all items of inventory in the current year was greater than respective costs, the company valued its inventory at cost. In the present year the company has changed to weighted average formula, which better reflects the consumption pattern of inventory, for ascertaining inventory costs from the earlier practice of using FIFO for the purpose.

- 8. GAJVEER SINGH MAHUR (GSM) AS-1 8 The change in policy has reduced profit and value of inventory by ₹ 20,000’. Explanation of disclosure of Accounting policies AS-1 Disclosure of Accounting policies Disclosure of fundamental Accounting Assumptions Selection of Accounting policy Disclosure of change in Accounting policy Disclose all significant accounting policies at one place & should form part of Financial Statement 1) FAA are: i) Going concern ii) Consistency iii) Accrual 2) Disclose FAA if not followed 1) Primary factor: --- True & fair view of B/S & P/L A/c 2) secondary factor: i) prudence ii) substance over form iii) Materiality 1) old policy 2) New policy 3) reason of change 4) financial impact of such change

- 9. GAJVEER SINGH MAHUR (GSM) AS-1 9 QUESTION 1 Indicate any three areas in respect for which different accounting policies may be adopted by different enterprises. or Enumerate various areas in which different polices could be adopted. or Mention any six areas in which different accounting policies may be adopted by different enterprises. Solution: Major Areas in which different accounting policies may be adopted by different enterprises includes: (1) Method of depreciation, depletion and amortisation, e.g., WDV method, SLM method. (2) Treatment of expenditure during construction, e.g., capitalization, written off, deferment (3) Conversion or translation of foreign currency items, e.g. average rate, TT buying rate. (4) Valuation of inventories, e.g., FIFO, weighted average method. (5) Treatment of goodwill, e.g., capitalization method, super profit method (6) Valuation of investment, e.g., lower of cost and fair value (7) Treatment of retirement benefits, e.g., Pay as you go QUESTION 2 Write a short note on fundamental accounting assumptions. QUESTION 3 What are the major considerations, which govern the selection and application of accounting policies? OR What are the major considerations governing the Accounting Policies? QUESTION 4 Write a short note on discloser of accounting policy. OR Indicate the requirements with regard to discloser of accounting policies. OR

- 10. GAJVEER SINGH MAHUR (GSM) AS-1 10 ‘Discloser of significant accounting policy adopted in the preparation and presentation of the financial statements enhance the intangibility of financial statements.’ Discuss. OR Briefly describe the requirements of Accounting Standard-1 in regard to discloser of significant accounting policies. OR Indicate the requirements with regard to discloser of accounting policies. Can discloser of accounting policies or of changes therein remedy a wrong or inappropriate treatment of the item in the accounts?