1. Price and Cost Analysis

Compared

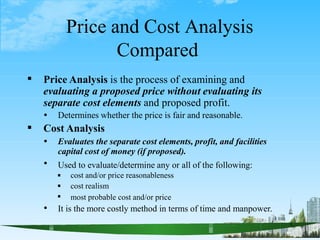

1

Price Analysis is the process of examining and

evaluating a proposed price without evaluating its

separate cost elements and proposed profit.

Determines whether the price is fair and reasonable.

Cost Analysis

Evaluates the separate cost elements, profit, and facilities

capital cost of money (if proposed).

Used to evaluate/determine any or all of the following:

cost and/or price reasonableness

cost realism

most probable cost and/or price

It is the more costly method in terms of time and manpower.

2. 5

Definition of Cost Analysis

The review and evaluation of the separate

cost elements and profit in an offeror’s or

contractor’s proposal (including cost or

pricing data or information other than cost

or pricing data), and the application of

judgement to determine how well the

proposed costs represent what the cost of

the contract should be, assuming

reasonable economy and efficiency (FAR

15.404(c)(1)).

3. Cost Analysis: When to apply it.

3

It is performed if certified cost or pricing data are required.

It may be used to evaluate information other than cost or

pricing data, e.g., non-certified cost data.

Normally, it is not needed if adequate price competition

exists. In this case, it still may be used if the price is

determined to be unreasonable or you are considering a cost

realism evaluation [see FAR 15.305(a)(1)].

Cost analysis is one of the approaches that should be used

when a cost realism evaluation is required.

When you perform a cost analysis, you should also include a

price analysis to verify price reasonableness.

4. engineering

m

anufacturing

field service

ILS

direct labor

travel

vendor

tooling

odc

raw material

purchased parts

standard commercial

items

subcontracts

direct material

direct cost

engineering

m

anufacturing

field service

ILS

m

aterial

handling

burden (O/H)

engineering

m

anufacturing

field service

ILS

m

aterial

handling

G&A

G&A FCCM (COM)

indirect cost

cost profit

Contract Price

Contract Price = Cost + Profit

4

5. Direct Costs (FAR 31.202)

5

Definition: Direct costs are identifiable to a final

cost objective (a particular contract).

Examples: direct material and direct labor.

All costs identified specifically with a contract

are direct costs for that contract and shall not be

charged to another contract directly, or indirectly.

No cost shall be charged to a contract as a direct

cost, if other costs incurred for the same purpose

in like circumstances have been charged as an

indirect cost.

6. Indirect Costs (FAR 31.203)

6

Definition: Indirect costs are not directly

identifiable with a final cost objective (e.g. a

particular contract), but identified with two or

more final cost objectives.

The distribution of indirect costs to various

contracts should roughly be based on the benefits

received on each contract.

No cost shall be charged to a contract as an

indirect cost if other costs incurred for the same

purpose in like circumstances have been charged

as a direct cost to that contract or any other

contract.

7. Alternative Direct Cost

Treatment (FAR 31.202)

7

For practicality, any direct cost of minor

dollar amount may be treated as an indirect

cost if this treatment:

Is consistently applied across all contracts,

and

Produces substantially the same results as

treating the cost as a direct cost

8. 14

Proposal Major Cost Elements

Direct Labor Cost

Labor Categories

Labor Rates

Labor Hours

Direct Material Cost

The Actual Materials

Raw material

Purchased parts and/or

assemblies

Subcontracts

Miscellaneous material

Discounts, Scrap,

Inventory Shrinkage, &

Freight-in

Indirect Costs

Material Handling

Fringe Benefits

Overhead (or burden)

G&A Expenses

Other Direct Costs

Nonrecurring costs

Subcontracts

Travel

Profit or Fee

Cost of Money

Escalation

9. 15

Cost Analysis: First Step

Pre-solicitation involvement by the price/cost analyst

(FSO) and engineer (ESO) is recommended

Price/cost input

Section B set-up, Price/Cost Evaluation Template, Section L

price/cost data requirements, and Section M price/cost evaluation

factors

Engineering and price/cost input

SOW/PWS

Read the solicitation, section B, and SOW/PWS

What is being purchased?

Not as easy as looking at the Section B CLINs and/or SLINs

What are the solicitation requirements for the contractor and the

government?

10. 16

Cost Analysis: Second Step

Read the contractor’s proposal price/cost

narrative

It will discuss the contractor’s proposal structure,

assumptions, rationale, etc.

The length and quality will vary

An important source of proposal information

Study/know the proposal set-up

Check the math:

Is the arithmetic correct? The Section B unit prices multiplied by

the quantities result in the total amounts?

Do the amounts “foot”? Do they add-up and/or calculate

correctly?

Do the numbers “track”? Can the figures be traced among the

support schedules?

11. Cost Analysis: Third Step

11

What is the basis of the proposed cost?

How did you come up with this number?

What is your rationale?

What are your assumptions?

What are the calculations you used?

The contractor’s responses provide the

answer to the question:

Why is this price and/or cost reasonable?

12. Cost Estimating Methods Used

by the Contractor

12

Common methods:

Round Table: Experts get together and make

judgments on projected costs

Comparison: Adjustments are made to a past or

current item to derive the cost

Parametric: Projections are based on formulas, or cost

estimating relationships

Detailed: A thorough review is made, with detailed

information comprising the estimate

An offeror may use any generally accepted estimating

methods that are equitable and consistently applied in

similar situations.

13. FAR 15.404-4(c) Contracting

Officer Responsibilities: Profit

13

Contracting officer responsibilities.

(1) When the price negotiation is not

based on cost analysis, contracting

officers are not required to analyze profit.

(2) When the price negotiation is based on

cost analysis, contracting officers in

agencies that have a structured approach

shall use it to analyze profit.

14. DFARS 215.404-4(b)(1) Profit

14

Departments and agencies must use a

structured approach for developing a pre-

negotiation profit or fee objective on any

negotiated contract action when cost or

pricing data is obtained, except for cost-plus-

award-fee contracts or contracts with

Federally Funded Research and

Development Centers.

DFARS 215.404-70 DD FORM 1547

DFARS 215.404-71 Weighted Guidelines Method

15. FAR 15.404-4(c)(4):

Fee - Statutory Limitations

15

For R&D work performed under a CPFF contract, the fee

shall not exceed 15% of the contract’s estimated cost,

excluding fee.

For architect-engineer services for public works or

utilities, the contract price or the estimated cost and fee

for production and delivery of designs, plans, drawings,

and specifications shall not exceed 6% of the estimated

cost of construction of the public work or utility,

excluding fees.

For other CPFF contracts, the fee shall not exceed 10% of

the contract’s estimated cost, excluding fee.

16. Source Selection Sect M:

Cost/Price Evaluation Criteria

16

Price Reasonableness: No FAR definition – see next slide

Cost Realism: Measure of the appropriateness of a cost to its

corresponding work element. The Government will determine if the

proposed costs/price(s) are realistic for the work to be performed,

reflect a clear understanding of the solicitation’s requirements, and

are consistent with the various elements of the Offeror’s technical

proposal (FAR 15.404-1(d)).

Completeness (non-FAR definition): An accurate reflection, within

the cost/price proposal, of all aspects of the technical proposal;

compliance with the cost/price preparation instructions in the RFP

Section L – Instructions, Conditions, and Notices to Offerors; and

compliance with any other applicable directions.

17. 36

Cost Realism Analysis FAR 15.404-1(d)(2)

(Cost Reimbursement Contracts)

The following apply to both competitive and sole source

environments:

Government shall perform cost realism analyses for cost-

reimbursement contracts.

Individually determine the probable cost of performance of each

offeror.

Probable Cost is the government’s best estimate of the cost of any

contract that is likely to result from the offeror’s proposal.

Probable cost determined by adjusting each offeror’s

costs, and fee when appropriate, to reflect any

understatements or overstatements based on the results

of the cost realism analysis.

For a CPFF contract, the fee would not be adjusted.

Probable cost is used in deciding best value.

(Competitive environment only).

18. 37

Cost Realism Analysis FAR 15.404-1(d)(3)

(Competitive Fixed Price Contracts)

May be performed on Fixed Price Incentive contracts.

Situations where cost realism analysis may be done on

competitive fixed price contracts:

When new requirements may not be fully understood by

competing offerors, or

There are quality concerns, or

Past experience indicates that contractors’ proposed costs have

resulted in quality or service shortfalls

You cannot adjust offered prices as a result of the cost

realism analysis.

Results of the analysis may be used in performance risk

assessments and responsib ility determ inations.

19. 38

Cost Realism Analysis

and Cost Analysis

There is a difference between the two, but

Confusion between the terms

Often used interchangeably

Cost Realism Analysis applies to source

selections

Used to verify that the contractor’s technical approach

has been priced in the proposal

Used mainly on cost reimbursement type contracts

Used to determine the Probable Cost of Performance

(Most Probable Cost)

Cost Analysis methods/procedures are used to

determine Cost Realism.

20. Technical Analysis

[FAR 15.404-1(e)]

20

Evaluation performed by personnel having specialized

knowledge, skills, experience, or capability in

engineering, science, or management on proposed

material types and quantities, labor, processes, special

tooling, facilities, reasonableness of scrap and spoilage,

and other factors in the proposal in order to determine the

need for and reasonableness of the proposed resources.

At a minimum:

examine the types and quantities of material (“kinds and

quantities” evaluation)

and the need for the types and quantities of labor hours and the

labor mix (skill and category)

21. Field Pricing Support & the

Cost or Pricing Data Threshold

21

DFARS 215.404-2(a):

PCO should consider field pricing support for

Fixed price proposals exceeding $650K

Cost type proposals exceeding $650K from offerors with

significant estimating system deficiencies

Cost type proposals exceeding $10 million from offerors

without significant estimating system deficiencies

PCO should not request field pricing support for

proposals less than $650K; exceptions:

lack of knowledge of particular contractor

sensitive conditions/problem areas

22. Points to Consider When

Requesting Field Pricing Support

Per FAR 15.404-2(a)(1):

The contracting officer should request field pricing assistance

when the information available at the buying activity is

inadequate to determine a fair and reasonable price; tailor

requests to reflect the minimum essential supplementary

information needed to conduct a technical or cost or pricing

analysis.

Consider cost risk!

Contract type: there is more risk on a FFP than CPFF or CPAF

contracts.

Proposal total dollar value

The DCAA PLA or FA can help determine the type of65

field pricing support/audit services needed.

23. FSO is the POC for DCAA

23

Request DCAA audits through the FSO

Submit audit request to DCAA

Receive/file DCAA audit reports

Tracking/report status of DCAA audits

AFARS 5142.1-90-2

Contract Audit Follow Up (CAFU) Program

DoDD 7640.2

AFARS 5142.1-90-2

SOP Number 25

24. Contract Audit Follow Up

(CAFU) Program (1 of 2)

24

Track/provide status of “reportable audits”

Reportable Audits

Estimating/accounting system and internal control

reviews

Incurred costs including final indirect cost rates

Claims

Defective pricing reviews

Termination settlements

CAS issues/cost impact statement reviews

25. Contract Audit Follow Up

(CAFU) Program (2 of 2)

25

Recent revision: DCMA database now used

Rules/procedures?

Reviewed/updated:

March 31st

September 30th

Overage Audit Review Board

Discuss unresolved DCAA audits over 6 months old

with the Commander

Bottom Line: reportable audits must be resolved

in a timely manner

28. Reasonableness - (FAR 31.201-3)

28

Definition: A cost is reasonable if, in its

nature and amount, it does not exceed what

a prudent person would pay in the conduct

of competitive business.

Considerations

Is the cost necessary?

Is the cost consistent with sound business

practice and law?

Are the contractor’s purchases done on an

“arm’s-length basis”?

29. Allocability - (FAR 31.201-4)

29

Definition: A cost is allocable to one or more

cost objectives (e.g., contracts) if it is charged

based on the relative benefits received or some

other equitable relationship.

A cost is Allocable to a Government contract if:

It is incurred specifically for the contract, or

It benefits the contract and other work (e.g. it’s

an overhead cost), and can be fairly distributed

based on benefits received, or

It is necessary to overall operation of the

business (e.g. certain G&A expenses).

30. 73

The Most Common Ways Costs are

Incurred

Expend Cash - Actual outlay of dollars (by cash,

check, etc.) in exchange for goods or services.

(e.g. Pay a vendor for raw materials)

Accrue Expense - For accounting purposes,

because a future obligation is being incurred or

an asset is being used. (e.g. Incurring an

obligation to current workers, for their future

pensions)

Use Inventory - For example, contractor buys

inventory in advance and charges it to contracts

as inventory is used.

31. Sources of Accounting

Principles & Standards

31

Generally Accepted Accounting

Principles (GAAP)

Cost Accounting Standards (CAS)

FAR Part 31 Contract Cost Principles

and Procedures

32. Accounting: Financial & Cost

32

In semi-plain English:

Accounting is the process of identification, measurement,

and communication of financial information about

economic entities to interested parties. Two types:

Financial accounting focuses on measuring the results of an

organization’s operations for a period of time, reflected in the

financial statements.

Cost (or management) accounting focuses on cost allocation to

a product, service, or contract; management uses the information

to plan, evaluate, and control within its organization and to assure

appropriate use of, and accountability for, its resources.

33. Generally Accepted Accounting

Principles (GAAP)

33

Generally Accepted Accounting Principles or GAAP

refers to the common set of accounting concepts,

standards, and procedures which represent a general

guide.

GAAP principles are those that have substantial

authoritative support or are based on accounting practices

accepted over time by prevalent use.

Financial Accounting Standards Board (FASB), American

Institute of CPAs (AICPA), Accounting Principles Board (APB),

etc.

The end products of the accounting cycle, the financial

statements (balance sheet, income statement, etc.) are

prepared in accordance with GAAP.

34. Cost Accounting Standards (CAS)

(1 of 2)

34

Purpose of CAS:

Promulgate standards to achieve uniformity

and consistency in cost accounting practices

to be followed by contractors and

subcontractors for defense contracts. It is an

attempt to provide common ground between

the contractors and the federal government on

cost accounting issues during proposal

preparation, negotiations, etc.

35. Cost Accounting Standards (CAS)

(2 of 2)

35

Currently, there are 19 standards.

Cost Accounting Standards Board (CASB) administers

CAS: five members, includes representatives from

government, industry, and academia.

CAS/CASB was originally established in August 1970

under the legislative branch.

Ceased operations September 30, 1980 due to lack of

funds.

Re-established in November 1988 under the executive

branch within Office of Federal Procurement Policy

(OFPP) which is under Office of Management and

Budget (OMB).

36. Exemptions From CAS (1 of 2)

36

Eleven exemptions, with the most common (7)

below:

Sealed bid contracts.

Negotiated contracts/subcontracts less than $650,000.

Contracts & subcontracts with small businesses.

FFP & FFP with EPA contracts/subcontracts for the

acquisition of commercial items.

FFP contracts & subcontracts awarded on the basis of

adequate price competition without the submission of

cost/price data.

37. Exemptions From CAS (2 of 2)

37

Contracts/subcontracts in which the price is set

by law or regulation.

Contract/subcontract executed and

performed outside the U.S., its territories, and

its possessions.

38. CAS Coverage

38

Two types of CAS can be applicable, depending on the

dollar value of previous awards and current acquisitions.

Full coverage: comply with all CAS in effect on the contract

award date and with any new standards.

Modified coverage: requires contractor to comply with four

standards

CAS 401, Consistency in estimating, accumulating, & reporting

costs.

CAS 402, Consistency in allocating costs incurred for the same

purpose.

CAS 405, Accounting for unallowable costs.

CAS 406, Cost accounting period.

39. 82

CAS - Disclosure Statement

Firms that have contracts/subcontracts subject to

full CAS coverage should have submitted a

CASB Disclosure Statement, providing

information on how they charge specific types of

costs.

Contractor discloses/documents company accounting

practices to the government.

The ACO and cognizant DCAA auditor are

responsible for reviewing the contractor’s

Disclosure Statement for adequacy, and for

compliance with FAR Part 31 and CAS.

40. GAAP vs. CAS

40

GAAP and CAS are not the same.

GAAP generally refers to financial, not cost,

accounting guidance.

CAS is an attempt to extend GAAP-like guidance

to government cost accounting.

CAS Objectives:

Common cost treatment, same terminology, and the

avoidance of cost manipulation (gaming).

Facilitate proposal preparation and negotiations.

41. CAS: FAR References

41

FAR Part 30

CAS Administration

Policies and Procedures for applying

CAS to negotiated contracts &

subcontracts

FAR Appendix B

Contains the actual CAS

42. FAR 31.2 Cost Principles for

Commercial Organizations

42

Applies to all contractors.

Defines direct and indirect costs.

Addresses specific kinds of costs as to

whether allowable, unallowable, or

allowable with restrictions.

Examples of unallowable costs: interest

expense, bad debts, entertainment costs,

donations, attorney fees for claims.

43. FAR Part 31: Examples of

Unallowable Costs

43

31.205-3 -- Bad Debts

31.205-8 -- Contributions or Donations

31.205-14 -- Entertainment Costs

31.205-20 -- Interest and Other

Financial Costs

31.205-51 -- Costs of Alcoholic

Beverages

44. FAR Part 31 Cost Principles for

“Other” Organizations

44

Refer to FAR 31 for separate, unique

coverage of the cost principles for

contracts with:

Educational institutions (FAR 31.3)

State & local governments, &

federally recognized Indian tribal

governments (FAR 31.6)

Nonprofit organizations (FAR 31.7)

45. Contract Terms & Cost Principles

45

Specific costs may be addressed in RFP or

contract. (e.g. Although transportation

costs are generally allowable, the contract

may restrict them to a certain mode.)

On cost allowability, contract terms can

only be more restrictive than other factors.

(e.g. Contract terms cannot make interest

expense allowable on the contract.)

47. Management/Cost Accounting

System

47

Contractors’ have to manage their organizations,

products/services, and contracts

There needs to be a system in place to determine

whether the service, product, or contract

Is on schedule for completion

Is at its budgeted cost

And if not

Why not?

What is being done to correct the situation?

All major companies have such a system!

48. Adequate Estimating System

48

ACO estimating system approval means that the system

has the controls to consistently produce adequate and

reliable estimates.

established policies, procedures, and practices to persons

responsible for preparing and supporting estimates

A disapproved system is a red flag indicating that the

firm's estimating system does not consistently provide

adequate proposals.

Normally, proposals from a firm with a disapproved system

should be subjected to closer scrutiny, particularly closer scrutiny

by audit professionals.

49. Adequate Accounting System

49

Primary goal of an acceptable accounting system:

Ensure that costs are appropriately, equitably, and consistently allocated

to all final cost objectives (i.e., individual contracts, jobs, or products).

Pre-award accounting system survey performed by DCAA.

System should answer affirmative to specific questions:

IAW GAAP? (IAW CAS?)

Identify & segregate direct from indirect costs, allocating these costs

equitably to specific contracts on a consistent basis?

Timekeeping & labor distribution systems appropriately identify direct

and indirect labor charges to intermediate & final cost objectives?

Accumulates costs integrated with, and reconcilable to, the general

ledger?

Determine cost of work performed at interim points (at least monthly)

because of routine posting to books of account?

If required by the contract, identify costs by CLIN/SLIN or by unit?

Specifically: Are there accounting “controls” in place?