Tricumen / Capital markets revenues and banks valuations 210714

•

0 likes•293 views

Capital markets revenues and banks’ valuations The variance of capital markets earnings is often said to (1) heighten the volatility of the share price and/or (2) depress the market valuation. For the banks included in this note, we find no evidence that the first assumption holds true … … but we do identify a strong correlation between the capital markets revenue dynamics and valuations: banks with (relatively) stable revenues are rewarded with higher valuations.

Recommended

Recommended

More Related Content

What's hot

What's hot (16)

Viewers also liked

Similar to Tricumen / Capital markets revenues and banks valuations 210714

Similar to Tricumen / Capital markets revenues and banks valuations 210714 (20)

More from Tricumen Ltd

More from Tricumen Ltd (20)

Recently uploaded

Recently uploaded (20)

Tricumen / Capital markets revenues and banks valuations 210714

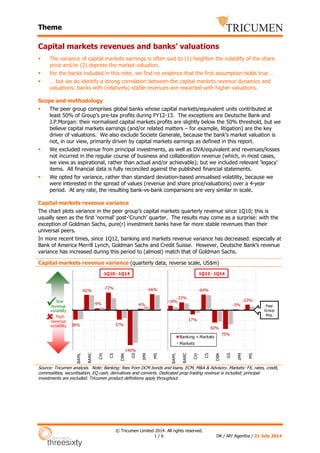

- 1. Theme © Tricumen Limited 2014. All rights reserved. 1 / 6 DK / AP/ Agentha / 21 July 2014 Capital markets revenues and banks’ valuations The variance of capital markets earnings is often said to (1) heighten the volatility of the share price and/or (2) depress the market valuation. For the banks included in this note, we find no evidence that the first assumption holds true … … but we do identify a strong correlation between the capital markets revenue dynamics and valuations: banks with (relatively) stable revenues are rewarded with higher valuations. Scope and methodology The peer group comprises global banks whose capital markets/equivalent units contributed at least 50% of Group’s pre-tax profits during FY12-13. The exceptions are Deutsche Bank and J.P.Morgan: their normalised capital markets profits are slightly below the 50% threshold, but we believe capital markets earnings (and/or related matters – for example, litigation) are the key driver of valuations. We also exclude Societe Generale, because the bank’s market valuation is not, in our view, primarily driven by capital markets earnings as defined in this report. We excluded revenue from principal investments, as well as DVA/equivalent and revenues/losses not incurred in the regular course of business and collaboration revenue (which, in most cases, we view as aspirational, rather than actual and/or achievable); but we included relevant ‘legacy’ items. All financial data is fully reconciled against the published financial statements. We opted for variance, rather than standard deviation-based annualised volatility, because we were interested in the spread of values (revenue and share price/valuations) over a 4-year period. At any rate, the resulting bank-vs-bank comparisons are very similar in scale. Capital markets revenue variance The chart plots variance in the peer group’s capital markets quarterly revenue since 1Q10; this is usually seen as the first ‘normal’ post-‘Crunch’ quarter. The results may come as a surprise: with the exception of Goldman Sachs, pure(r) investment banks have far more stable revenues than their universal peers. In more recent times, since 1Q12, banking and markets revenue variance has decreased: especially at Bank of America Merrill Lynch, Goldman Sachs and Credit Suisse. However, Deutsche Bank’s revenue variance has increased during this period to (almost) match that of Goldman Sachs. Capital markets revenue variance (quarterly data, reverse scale, US$m) Source: Tricumen analysis. Note: Banking: fees from DCM bonds and loans, ECM, M&A & Advisory. Markets: FX, rates, credit, commodities, securitisation, EQ cash, derivatives and converts. Dedicated prop trading revenue is included; principal investments are excluded. Tricumen product definitions apply throughout. 38% -62% -9% -72% 37% 140% -6% -66% BAML BARC Citi CS DBK GS JPM MS high revenue volatility low revenue volatility 1Q10 - 1Q14 -18% -33% 17% -64% 50% 75% -5% -23% BAML BARC Citi CS DBK GS JPM MS Banking + Markets Markets Peer Group Avg. 1Q12 - 1Q14

- 2. Theme © Tricumen Limited 2014. All rights reserved. 2 / 6 DK / AP / Agentha / 21 July 2014 Revenue variance vs share price performance … How correlated are capital markets revenues with share price performance? In two words – not much: investors reward individual banks’ revenue1 -generating ability. Below, we compare capital markets revenue variance (left hand scale – same data as in the left-hand chart on the first page) against the movement in banks’ period-end share prices for 1, 2, 3 and 4 years (right-hand scale) to the end of June-14. The data suggests that: There is no significant correlation between the two series of data. The share price of Goldman Sachs, the bank with the highest variance in capital markets revenue in this peer group, convincingly outperformed European banks with much more stable earnings. This may be a reflection of European banks’ political and/or regulatory environment as much as (or more than) their financial performance; but Goldman Sachs’ strong share price performance versus US peers also stands in contrast with its volatile revenue. Furthermore, there is no evidence that ‘pure’(r) the investment banks, Goldman Sachs and Morgan Stanley (though the later benefited from its newfound focus on equities and money management), underperformed the more diversified Bank of America Merrill Lynch or Citigroup. Interestingly, even the marketwide concerns about the outlook for FICC revenues over the last 12 months (red dots) did not unduly trouble Goldman Sachs’ share price: in fact, it did slightly better than Citigroup and J.P.Morgan, and was barely behind Bank of America Merrill Lynch. Capital markets revenue variance (LHS, quarterly data 1Q10-1Q14, reverse scale, US$) vs share price performance (RHS) Source: NASDAQ, FT.com, Tricumen revenue analysis. 1 We ran the same analysis against banks’ capital markets profits (instead of revenue), excluding collaboration profits. The result was not meaningfully different, despite significant variation between individual banks’ cost/income ratios. In our view, this shows that investors view revenue as the key driver of profits while cost management is, at best, a short-term play. This was the topic of our 27-Nov-13 note titled ‘Profit Drivers’. 38% -62% -9% -72% 37% 140% -6% -66% -120% -80% -40% 0% 40% 80% 120%-150% -100% -50% 0% 50% 100% 150% BAML BARC Citi CS DBK GS JPM MS Banking + Markets Revenue variance 1Q10-1Q14 Last 1Y Last 2Y Last 3Y Last 4Y Share price performance: period to end-2Q14 (local currency) low revenue volatility high revenue volatility share price increased share price declined

- 3. Theme © Tricumen Limited 2014. All rights reserved. 3 / 6 DK / AP / Agentha / 21 July 2014 … and share valuations Looking at the market valuation of the banks in this report, two related patterns are evident: Capital markets earnings do seem to carry a significant valuation discount. At end-June-14 and end-June-13 (red dots and orange boxes), the composite P/BV and P/E valuations of Goldman Sachs and J.P.Morgan2 were significantly below their three peers whose earnings are less dependent on a capital markets ‘story’ (Bank of America Merrill Lynch and Citigroup) and/or have made strategic changes to their group-wide franchises that investors approved of (Morgan Stanley). There is also a tangible link between revenue variance and market valuation. For example, Goldman Sachs’ composite P/BV and P/E valuation in two most recent periods was more than 50% below the peer group average (J.P.Morgan is penalised on P/E measure, but had the highest P/BV at end-June-14); while Barclays and Credit Suisse are among the most highly valued stocks overall, especially in more recent periods. Other banks generally fall between these three banks, but the pattern is evident. Also, while the book value calculation does not lend itself readily to adjustments, revenues could be refined – and that would further emphasise the link between revenue variance and valuations. We view P/BV as the more reliable measure of relative value, and have therefore weighted the composite valuation in favour of it. This resulted in a composite valuation that favours US banks: in recent years, investors priced the book value of US banks more highly that that of European banks’. European banks, however, achieved consistently higher P/E valuations. Finally, some might disagree with our favouring P/BV over P/E, and not without reason. The latter could be refined by, for example, weighting capital markets revenue versus the revenue of the Group; and/or the mix of capital market revenue to take account of the exposure to ‘slow’ area of business (for example, FICC). This would, in our view, further highlight the relationship between revenue dynamics and valuations. Capital markets revenue variance (LHS, quarterly data 1Q10-1Q14, reverse scale, US$) vs composite P/BV and P/E valuations (RHS, over/(under) peer group average) Source: NASDAQ, FT.com, Tricumen revenue, profit and book value analysis. Notes: (1) Our calculation of historical price/earnings (P/E) and price/book value (P/BV) ratios, is based on the Group published profit, book value and share count from the financial statements published prior to the valuation date shown. (2) P/E outliers falling outside the 3-standard deviation band for the peer group are excluded. 2 On P/BV measure alone, though, Goldman Sachs and J.P.Morgan were both comfortably ahead of their peers at end-June-14: J.P.Morgan 1.08x, Goldman Sachs 1.06x, Morgan Stanley 1.0x, Bank of America Merrill Lynch 0.75x, Citigroup 0.73x. 38% -62% -9% -72% 37% 140% -6% -66% -120% -80% -40% 0% 40% 80% 120%-150% -100% -50% 0% 50% 100% 150% BAML BARC Citi CS DBK GS JPM MS Banking + Markets Revenue variance 1Q10-1Q14 end-June-14 end-June-13 end-June-12 end-June-11 Composite P/BV and P/E valuations over/(under) peer group average at: low revenue volatility high revenue volatility valuation above peers' valuation below peers'

- 4. Theme © Tricumen Limited 2014. All rights reserved. 4 / 6 DK / AP / Agentha / 21 July 2014 Appendix 1 – Share price and P/BV Bank of America Merrill Lynch Barclays Citigroup Credit Suisse Deutsche Bank Goldman Sachs J.P.Morgan Morgan Stanley Source: NASDAQ, FT.com, Tricumen book value analysis. 0.2x 0.3x 0.4x 0.5x 0.6x 0.7x 0.8x 0.9x $0 $5 $10 $15 $20 $25 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 BAC (daily close) P/BV 0.3x 0.4x 0.4x 0.5x 0.5x 0.6x 0.6x 0.7x 0.7x 0.8x 0.8x 100p 150p 200p 250p 300p 350p 400p Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 BARC (daily close) P/BV 0.3x 0.4x 0.5x 0.6x 0.7x 0.8x 0.9x $15 $20 $25 $30 $35 $40 $45 $50 $55 $60 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Citi (dailyclose) P/BV Note: Adjusted for 10-1 split in May-11 0.3x 0.5x 0.7x 0.9x 1.1x 1.3x 1.5x CHF10 CHF15 CHF20 CHF25 CHF30 CHF35 CHF40 CHF45 CHF50 CHF55 CHF60 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 CS (daily close) P/BV 0.2x 0.3x 0.4x 0.5x 0.6x 0.7x 0.8x EUR10 EUR20 EUR30 EUR40 EUR50 EUR60 EUR70 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 DBK (daily close) P/BV 0.3x 0.4x 0.5x 0.6x 0.7x 0.8x 0.9x 1.0x 1.1x 1.2x $80 $100 $120 $140 $160 $180 $200 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 GS (daily close) P/BV 0.3x 0.4x 0.5x 0.6x 0.7x 0.8x 0.9x 1.0x 1.1x 1.2x $20 $25 $30 $35 $40 $45 $50 $55 $60 $65 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 JPM (daily close) P/BV 0.2x 0.3x 0.4x 0.5x 0.6x 0.7x 0.8x $10 $15 $20 $25 $30 $35 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 MS (daily close) P/BV

- 5. Theme © Tricumen Limited 2014. All rights reserved. 5 / 6 DK / AP / Agentha / 21 July 2014 Appendix 2 – P/BV dynamics P/BV dynamics (1-Jan-10 – end-June-14) Source: NASDAQ, FT.com, Tricumen book value analysis. 20 40 60 80 100 120 140 160 180 31-Dec-09 31-Mar-10 30-Jun-10 30-Sep-10 31-Dec-10 31-Mar-11 30-Jun-11 30-Sep-11 31-Dec-11 31-Mar-12 30-Jun-12 30-Sep-12 31-Dec-12 31-Mar-13 30-Jun-13 30-Sep-13 31-Dec-13 31-Mar-14 BAC BARC Citi CS DBK GS JPM MS

- 6. Theme © Tricumen Limited 2014. All rights reserved. 6 / 6 DK / AP / Agentha / 21 July 2014 About Tricumen Tricumen was founded in 2008. It quickly became a strong provider of diversified market intelligence across the capital markets and has since expanded into transaction and corporate banking coverage. Tricumen’s data has been used by many of the world’s leading investment banks as well as strategy consulting firms, investment managers and ‘blue chip’ corporations. Situated near Cambridge in the UK, Tricumen is almost exclusively staffed with senior individuals with an extensive track record of either working for or analysing banks; and boasts what we believe is the largest capital markets-focused research network of its peer group. Caveats No part of this document may be reproduced or transmitted in any form by any means without written permission of Tricumen Limited. Such consent is often given, provided that the information released is sourced to Tricumen and that it does not prejudice Tricumen Limited’s business or compromise the company’s ability to analyse the financial markets. Full acknowledgement of Tricumen Limited must be given. Tricumen Limited has used all reasonable care in writing, editing and presenting the information found in this report. All reasonable effort has been made to ensure the information supplied is accurate and not misleading. For the purposes of cross- market comparison, all numerical data is normalised in accordance to Tricumen Limited’s proprietary product classification. Fully-researched dataset may contain margin of error of 10%; for modelled datasets, this margin may be wider. The information and commentary provided in this report has been compiled for informational purposes only. We recommend that independent advice and enquiries should be sought before acting upon it. Readers should not rely on this information for legal, accounting, investment, or similar purposes. No part of this report constitutes investment advice, any form of recommendation, or a solicitation to buy or sell any instrument or to engage in any trading or investment activity or strategy. Tricumen Limited does not provide investment advice or personal recommendation nor will it be deemed to have done so. Tricumen Limited makes no representation, guarantee or warranty as to the suitability, accuracy or completeness of the report or the information therein. Tricumen Limited assumes no responsibility for information contained in this report and disclaims all liability arising from negligence or otherwise in respect of such information. Tricumen Limited is not liable for any damages arising in contract, tort or otherwise from the use of or inability to use this report or any material contained in it, or from any action or decision taken as a result of using the report. © Tricumen Limited 2014. All rights reserved.