Impact of COVID19 on Civil Construction in Brazil

•

0 likes•116 views

How the virus is affecting Industries and Retailers in Brazil

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Impact of COVID19 on Civil Construction in Brazil

Similar to Impact of COVID19 on Civil Construction in Brazil (20)

Recently uploaded

Recently uploaded (20)

Impact of COVID19 on Civil Construction in Brazil

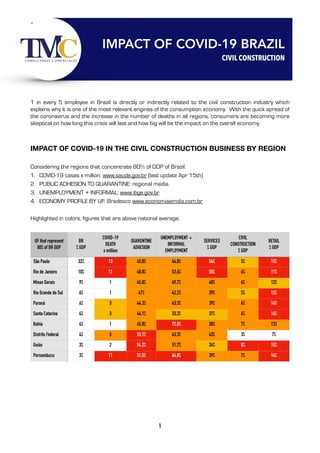

- 1. 1 in every 5 employee in Brazil is directly or indirectly related to the civil construction industry which explains why it is one of the most relevant engines of the consumption economy. With the quick spread of the coronavirus and the increase in the number of deaths in all regions, consumers are becoming more skeptical on how long this crisis will last and how big will be the impact on the overall economy. IMPACT OF COVID-19 IN THE CIVIL CONSTRUCTION BUSINESS BY REGION Considering the regions that concentrate 80% of GDP of Brazil: 1. COVID-19 cases x million: www.saude.gov.br (last update Apr 15th) 2. PUBLIC ADHESION TO QUARANTINE: regional media. 3. UNEMPLOYMENT + INFORMAL: www.ibge.gov.br 4. ECONOMY PROFILE BY UF: Bradesco www.economiaemdia.com.br Highlighted in colors, figures that are above national average. UF that represent 80% of BR GDP BR % GDP COVID-19 DEATH x million QUARENTINE ADHESION UNEMPLOYMENT + INFORMAL EMPLOYMENT SERVICES % GDP CIVIL CONSTRUCTION % GDP RETAIL % GDP São Paulo 32% 13 45,8% 44,8% 54% 5% 15% Rio de Janeiro 10% 11 48,8% 52,6% 50% 6% 11% Minas Gerais 9% 1 45,8% 49,7% 40% 6% 12% Rio Grande do Sul 6% 1 47% 42,2% 39% 5% 15% Paraná 6% 3 44,3% 43,3% 39% 6% 16% Santa Catarina 4% 3 44,1% 33,3% 37% 6% 16% Bahia 4% 1 45,8% 72,0% 38% 7% 13% Distrito Federal 4% 5 53,1% 43,3% 43% 3% 7% Goiás 3% 2 54,2% 51,7% 36% 8% 15% Pernambuco 3% 11 51,5% 64,8% 39% 7% 14% 1 IMPACT OF COVID-19 BRAZIL CIVIL CONSTRUCTION

- 2. ATTENTION SP and RJ: • Top region in volume of Civil Construction is facing the hardest situation with the pandemic. Due to quarantine, most services and retailers are closed, affecting the economic situation of all the population, but more severely, the low income families. At the same time, it is also affecting the public funds, by the reduction of collected taxes. • Governors of SP and RJ are in opposition to the President in regards to the Quarantine. They are open to the idea to strengthen restrictive measures for as long as required. • Half of the population in this region is already unemployed or working as independent professionals in service or retail segments with limited or no savings at all. This explains the level of low adherence to the quarantine, specially in low income areas (where level of infection is rising). • Exported products from Southeast region will suffer with global recession (i.e. Airplanes and commodities). It will also impact the amount of Public resources to fund big construction projects, as most of the budget will be redirected to Health and public programs to help those in most need. • If the Public Health system collapses, level of anxiety will increase among the general population who will delay any investment plan, such as purchasing new properties or enhancing existing spaces. Consumers will only solve home emergencies. Minas Gerais: • As one of the most relevant markets for the Civil Construction market, it should be kept under close follow up by the Commercial team, however the situation is not yet critical. • Primary Sector (Agriculture and Livestock) is the most relevant of the economy and should be less affected than Services and Retail. • However, top 5 Export Markets of Minas Gerais are China, USA, Holland, Japan and UK who might be affected by a global recession. • Governor is supporting the idea of avoiding extreme restrictive measures in areas where still there are no confirmed infection cases. He is positive to the idea of searching for alternatives to preserve the economy after virus. However he is facing strong opposition from municipalities and in the meantime most civil construction stores are either closed or working on limited hours. • As in the rest of the country, public resources are now redirected to support the fight against the virus. This is a politically correct measure. In this sense, it is expected that public construction projects will have to be delayed or totally cancelled. 2 REGIONAL ASSESSMENT

- 3. FOLLOW UP Northeast region • This is the region with the lowest GDP per capita and higher proportion of population with monthly income at risk because of the level of unemployment or informal employment. • Most civil construction stores are either closed or working on limited hours. • High level of business disruption is expected in Pernambuco, with already similar levels of death x million to RJ. • Because of the relevance of Tourism in Bahia, and the potential reduction in global prices of commodities, it is expected a difficult year for most of the population of the state. Even worse if level of infection continue to rise based on the low adhesion to the quarantine. • Further measures to restrict social contact might be defined by the Governments of these states in the following days, as their Health system has strong limitations to face this virus. Central West region: • In DF and Goiás, there is high level of adherence to the Quarantine. Most civil construction stores are either closed or working on limited hours. • Impact of Coronavirus in the economy of Brasilia is expected to be lower than other regions of Brazil, mainly due to the high proportion of public employees with granted income per month and penetration of internet. • Governor of Goiás is positive to the idea of strengthening quarantine terms to limit the expansion of the virus in the state. South Region: • Level of adherence to the quarantine in Santa Catarina is higher than the amount of unemployed or sub-employed people. Most civil construction stores are either closed or working on limited hours. • 75% of exports of Rio Grande do Sul are going to Asia, Europe and Middle East. Most of products are considered commodities and will suffer with decrease of the global demand. • It is probable that travel restrictions will still in place during Winter (July - Sep) affecting the population who depends of Tourism and Retail business. It is expected a reduction in the number of internal tourists this year. 3 REGIONAL ASSESSMENT

- 4. 4 KEY HIGHLIGHTS • Most consumers are postponing decision to purchase a new home or enhancing current spaces due to the uncertainty of what may happen in the future. • Despite Banks might reduce interest rates to motivate consumption in the mid term, high levels of unemployment will keep people away from long term commitments. CONSUMERS GOVERNMENT RETAILERS • The government is caught between the sword and the wall, trying to find a solution that is not limited to the selection between saving lives or the economy, but rather, trying to save the maximum number of lives without causing long-term damage to an economy that was starting to show signals of recovery in 2019. Politics can become a barrier for a quick recovery. • Most affected retailers are small and independent, attending low income Shoppers. Their main challenge is Cash Flow. Some families are having to use business cash to pay for food during quarantine. • High level of inventories at retail will become a barrier for a quick recovery of Industry volumes after the quarantine. • Chain stores and/or big independents are facing a sharp increase of online and/or phone purchases. Most of the large retailers already had online channels available, however they are not fully prepared to massively operate online. The dramatic flip in the operation, has created chaos and internal friction due to unclear or missing processes, systems, structure and people skills. COVID 19 has accelerated the need of a Digital Transformation of the store operation. • There is a huge internal pressure on their logistic operation to deliver on time in full simultaneous orders. Some stores used to deliver orders with their own vehicles, but now that the amount of online orders increased, it is necessary to implement a different operational model. • Due to limited cash flow, retailers will focus on maximize its GMROII, focusing on high rotation SKU’s • Big retailers are evaluating alternatives to increase the Back Margin of Online operation adjusting Trading Terms & Conditions to the online world. • Stock market will collapse, affecting Civil Construction Companies and Industries with open capital. • Big construction projects are expected to halt. Construction relies heavily on labourers who are not able to work from home. Consequently, any reduction in the labour supply due to quarantine requirements has the potential to delay projects. • Nonresidential construction activity is reliant on crude oil and other commodity prices, with the novel coronavirus posing a threat on global prices. • All players will start searching for cost reduction alternatives in short, mid and long term. • Short-Mid term efforts of Central or Regional governments to construct medical facilities would boost revenues for the Civil Construction industry. • All industries will fight for the same limited amount of cash flow of retailers INDUSTRY Complementing our previous report - General Impact of COVID 19

- 5. • Protect volume in SP and RJ, by strengthen relationship with strategic retailers whilst extending credit days to small stores until full recovery of pending payments. • Keep monitoring the evolution of the economy in MG, Central and South Regions. During the crisis, DF might gain tactical relevance due to the high proportion of public employees with granted income who could continue purchasing civil construction materials through online stores. • Key Accounts and Big Independent retailers with robust online platforms should become the critical partners to work with in search for alternatives to defend volume. • As the time invested on these clients will increase, Industries will adjust their Commercial Strategies to focus in a reduced amount of customers who concentrate 80% of volume. As a consequence, industries will have to review as well its Go to Market Model to expand the universe served through Distributors, in search for cost reduction alternatives. • To contribute with the Cash Flow of Key Strategic Retailers and Distributors, extend the credit days. At the same time, some industries are designing Shopper Marketing activities to be implemented by key retailers in order to motivate their shoppers to anticipate payment of products, even if the execution of projects is delayed until the end of the quarantine. • Industries are starting to review and adjust their Trading Terms and Conditions to be relevant to the new way of doing business through online retailers. Payments for Planograming, Space and In store locations in physical stores can be temporarily reduced or even stopped if quarantine last longer than 3 months. 5 BE PREPARED FOR A NEW NORMAL STRATEGY & TACTICS PEOPLE PROCESSES • Trade Marketing Representatives in charge on these strategic retailers will have to become truly business advisors during the crisis. Rather than only focusing on its exclusive category, they will have to be able to introduce and lead overall practical solutions to guide the store out of the crisis. • Most relevant skills to reinforce during the crisis: • Key Account Management • Crisis Management • Retail Management • Commercial Finance • Relationship Management Programs • Trading Terms and Conditions for online retail. • Persuasive Selling and Negotiation • Understanding Shopper Behavior online. • Effective Shopper Promotions online. • Speed up “Digital Transformation”: design, improve and formalize new operational processes, partners and skills for a fully only business. Guarantee a soft implementation during the crisis. • Adjust the process of Designing Promotions to reduce time to market. • Adjust Commercial, Logistic and Distribution processes to be aligned to the “New Normal” scenario.