Finance: A Week In Review

•

0 likes•62 views

- Major stock market indexes rose between 2.75-3.93% over the past week, but remain down between 5-16% over the past year. Commodity prices like oil and gold also declined since last year. - Economic data released in the coming week will provide insights into consumer confidence, durable goods orders, GDP growth, and consumer sentiment. - The Conference Board's leading economic index declined for the second straight month but does not signal a significant recession risk in early 2016, while industrial production rose more than expected in January.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (13)

Similar to Finance: A Week In Review

Similar to Finance: A Week In Review (20)

Recently uploaded

Recently uploaded (20)

Finance: A Week In Review

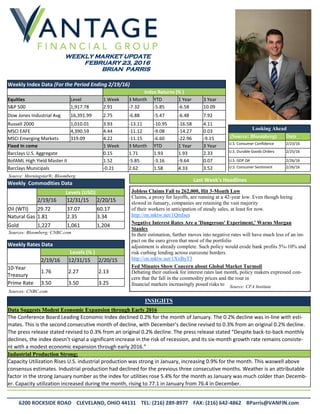

- 1. Weekly Index Data (For the Period Ending 2/19/16) Index Returns (% ) Equities Level 1 Week 3 Month YTD 1 Year 3 Year S&P 500 1,917.78 2.91 -7.32 -5.85 -6.58 10.09 Dow Jones Industrial Avg 16,391.99 2.75 -6.88 -5.47 -6.48 7.92 Russell 2000 1,010.01 3.93 -13.11 -10.95 -16.58 4.11 MSCI EAFE 4,390.59 4.44 -11.12 -9.08 -14.27 0.03 MSCI Emerging Markets 319.09 4.22 -11.15 -6.60 -22.96 -9.15 Fixed In come 1 Week 3 Month YTD 1 Year 3 Year Barclays U.S. Aggregate 0.15 1.71 1.93 1.93 2.33 BofAML High Yield Master II 1.52 -5.85 -3.16 -9.64 0.07 Barclays Municipals -0.21 2.62 1.58 4.33 3.52 WEEKLY MARKET UPDATE FEBRUARY 23, 2016 BRIAN PARRIS Looking Ahead (Source: Bloomberg) Date U.S. Consumer Confidence 2/23/16 U.S. Durable Goods Orders 2/25/16 U.S. GDP Q4 2/26/16 U.S. Consumer Sentiment 2/26/16 Weekly Commodities Data Levels (USD) 2/19/16 12/31/15 2/20/15 Oil (WTI) 29.72 37.07 60.17 Natural Gas 1.81 2.35 3.34 Gold 1,227 1,061 1,204 Weekly Rates Data Levels (% ) 2/19/16 12/31/15 2/20/15 10-Year Treasury 1.76 2.27 2.13 Prime Rate 3.50 3.50 3.25 Last Week's Headlines Jobless Claims Fall to 262,000, Hit 3-Month Low Claims, a proxy for layoffs, are running at a 42-year low. Even though hiring slowed in January, companies are retaining the vast majority of their workers in anticipation of steady sales, at least for now. http://on.mktw.net/1QmIses Negative Interest Rates Are a 'Dangerous' Experiment,' Warns Morgan Stanley In their estimation, further moves into negative rates will have much less of an im- pact on the euro given that most of the portfolio adjustment is already complete. Such policy would erode bank profits 5%-10% and risk curbing lending across eurozone borders. http://on.mktw.net/1XxByT3 Fed Minutes Show Concern about Global Market Turmoil Debating their outlook for interest rates last month, policy makers expressed con- cern that the fall in the commodity prices and the rout in financial markets increasingly posed risks to Source: Morningstar®; Bloomberg Sources: Bloomberg; CNBC.com Sources: CNBC.com Source: CFA Institute INSIGHTS Data Suggests Modest Economic Expansion through Early 2016 The Conference Board Leading Economic Index declined 0.2% for the month of January. The 0.2% decline was in-line with esti- mates. This is the second consecutive month of decline, with December’s decline revised to 0.3% from an original 0.2% decline. The press release stated revised to 0.3% from an original 0.2% decline. The press release stated “Despite back-to-back monthly declines, the index doesn’t signal a significant increase in the risk of recession, and its six-month growth rate remains consiste- nt with a modest economic expansion through early 2016.” Industrial Production Strong; Capacity Utilization Rises U.S. industrial production was strong in January, increasing 0.9% for the month. This waswell above consensus estimates. Industrial production had declined for the previous three consecutive months. Weather is an attributable factor in the strong January number as the index for utilities rose 5.4% for the month as January was much colder than Decemb- er. Capacity utilization increased during the month, rising to 77.1 in January from 76.4 in December. 6200 ROCKSIDE ROAD CLEVELAND, OHIO 44131 TEL: (216) 289-8977 FAX: (216) 642-4862 BParris@VANFIN.com

- 2. Weekly Market Update Disclosures Past performance is not indicative of future results. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information presented here to be reliable, but do not warrant its accuracy or com- pleteness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. The material has been prepared for informational purposes only, and is not intended to provide, nor should it be relied upon for, accounting, legal, or tax advice. References to future returns are not promises or estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or inter- preted as a recommendation. The price of equity securities may rise or fall because of changes in the broad market or changes in a company's financial condition, sometimes rapidly or unpredictably. International investing involves a greater degree of risk and increased volatility. There is no guarantee that companies that can issue dividends will declare, continue to pay, or increase dividends. Investments in commodities may have greater volatility than invest- ments in traditional securities, particularly if the instruments involve leverage. All returns represent total returns for the stated period. The Standard & Poor’s 500 Index is a market capitalization free-float adjusted index of the prices of 500 large capitalization common stocks traded in the United States. The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq. The Russell 2000 Index is a market capitalization free-float adjusted index that is considered to be representative of the small cap segment of the U.S. equity universe. The MSCI EAFE Index is a market capitalization weighted index and is designed to measure the equity market performance of developed markets (Europe, Australasia, and Far East) excluding the U.S. and Canada. The MSCI Emerging Markets Index is a free-float adjusted market capitalization index that is designed to measure the equity market performance in the global emerging markets. The Barclays Aggregate Bond Index is a market-capitalization weighted index that is considered to be representative of U.S. traded investment grade bonds. The Barclays Municipal Bond Index is a market- capitalization weighted index that is considered to be representative of U.S. traded investment grade municipal bonds. The Bank of America Merrill Lynch High Yield Master Index is a market-capitalization weighted index that tracks the performance of below investment grade U.S. dollar-denominated corporate bonds publicly issued in the U.S. domestic market. You cannot invest directly in an index. Registered Representative offering securities and advisory services through Cetera Advisor Networks LLC, member FINRA/SIPC. Cetera is under separate ownership from any other named entity. All e-mail sent to or from this address will be received or otherwise recorded by Vantage Financial Group, Inc. corporate e-mail system and is subject to archival, monitoring and/or review by and/or disclosure to, someone other than the recipient. Vantage Financial Group, Inc. has taken precautions to screen this message for viruses, but we cannot guarantee that it is virus free nor are we responsible for any damage that may be caused by this message. This email transmission and its attachments, if any, are confidential and intended only for the use of particular persons and entities. They may also be work product and/or protected by the attorney-client privilege or other privileges. Delivery to someone other than the intended recipient(s) shall not be deemed to waive any privilege. Review, distribution, storage, transmittal or other use of the email and any attachment by an unintended recipient is expressly prohibited. If you are not the name addressee (or its agent) or this email has been addressed to you in error, please immediately notify the sender by reply email and permanently delete the email and its attachments.