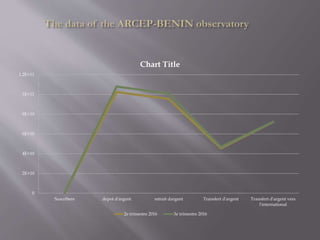

The document discusses the development of mobile money services in Benin. It notes that mobile money significantly increases financial inclusion in Benin as mobile phone penetration is around 87% compared to only 10% of the population having access to banks. Mobile money facilitates around 8 billion CFA francs in deposits and 7 billion CFA francs in withdrawals daily. The goal is to increase use of digital financial services like mobile money to 12% of Benin's adult population by 2019.

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)