Download to read offline

![Questions? Comments? Dianne Chipps Bailey Robinson, Bradshaw & Hinson, P.A. 101 N. Tryon Street, Suite 1900 Charlotte, North Carolina 28246 704-377-8323 (Phone) 704-373-3923 (Fax) [email_address]](https://image.slidesharecdn.com/rbhcharlotte1110309v1baileynonprofitnewform990powerpoint-12856197854696-phpapp01/85/IRS-Form-990-Oresentation-28-320.jpg)

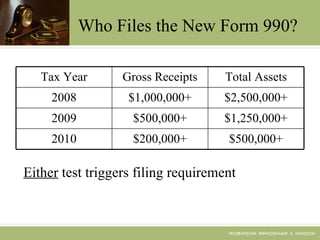

This document summarizes the key changes and requirements of the updated IRS Form 990. It outlines who must file the form based on gross receipts and total assets. It describes the increased scrutiny of insiders like directors, officers, and key employees. It also summarizes new governance standards regarding board independence, related party transactions, management companies, document retention policies, and disclosure of governing documents and compensation practices.