1. RCCA E-NEWS

Vol. I Date- 06th April, 2012 Email: - samaranchi14@gmail.com

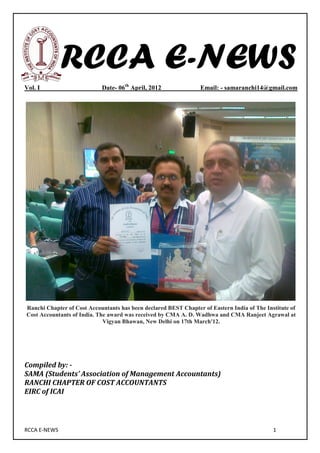

Ranchi Chapter of Cost Accountants has been declared BEST Chapter of Eastern India of The Institute of

Cost Accountants of India. The award was received by CMA A. D. Wadhwa and CMA Ranjeet Agrawal at

Vigyan Bhawan, New Delhi on 17th March'12.

Compiled by: -

SAMA (Students’ Association of Management Accountants)

RANCHI CHAPTER OF COST ACCOUNTANTS

EIRC of ICAI

RCCA E-NEWS 1

2. Patron’s Communique

Communique

Dear Students,

It is a matter of great pride for me that my students of Ranchi Chapter of ICAI (earlier ICWAI)

have not only formed SAMA (Students' Association of Management Accountants) but now

coming out with its official mouthpiece in the form of this e-newsletter. It shows the

management capacity of our students and hence, proves that we are really Management

Accountants.

Newsletter of any organization discusses the activities of the organization and provides a

platform to its members to discuss different professional issues for mutual benefits.

I am confident that this e-news letter will serve the above purpose.

I congratulate the students of Ranchi Chapter of ICAI for coming out with this newsletter and

pray for their success.

I am really proud of them.

Regards,

Ajay Deep Wadhwa, FCMA

wadhwa103@yahoo.co.in

RCCA E-NEWS 1

3. Chairman’s Communique

Dear All,

As you all know that reading is a very good habit and it always helps us to know about the new things and

let our self updated with the changes of world. As a professional we should keep our self updated with the

changes in corporate world which is changing and growing very rapidly. Presently, all the companies are

searching for Leaders & Managers who can do smart work and for this we have to keep grooming our

personalities, our writing skills, our talents etc. In Ranchi Chapter you mostly see that students are very active in

all the parts and their personality gets changed by the time passes. As I always think from my beginning of ICAI

(Earlier ICWAI, The Institute of Cost & Works Accountants of India) course that how the Personalities keep

themselves updated and know about so many things and not only they keep it with themselves but they tell

others so nicely that others also learn from it. With all these thinking I came to a point that it is all about reading

and writing regularly and then decision of publishing RCCA News (e-magazine)came to mind and then we all

discussed together with our Patron A. D. Wadhwa Sir and Faculty members of Ranchi Chapter and they

appreciated as they always use do with we students. We will publish articles and so many things by which we can

get to know about the changes and new things with every issue of this e-magazine and of course things related to

study also. In this magazine we will publish articles written by students, so you are having an opportunity to get

your articles published here, and in every issue we will select an article written by student to get published in

EIRC News which publishes in Eastern India of ICAI. I would like tell you a story happened with me once:

A well-known speaker started off his seminar by holding up a Rs. 500 note. In the room of 50 People, He asked,

"Who would like this Rs. 500 note?" Hands started going up. He said, "I am going to give this note to one of you

but first let me do this." He proceeded to crumple the note up. He then asked, "Who still wants it?" Still the hands

were up in the air. "Well," he replied, "What if I do this?" And he dropped it on the ground and started to grind it

into the floor with his shoe. He picked it up, now all crumpled and dirty. "Now who still wants it?" Still the hands

went into the air. "My friends, you have all learned a very valuable lesson. No matter what I did to the money. You

still wanted it because it did not decrease in value. It was still worth Rupee 500/-. Many times in our lives, we are

dropped, crumpled, and ground into the dirt by the decisions we make and the circumstances that come our way.

We feel as though we are worthless. But no matter what has happened or what will happen. Never lose your

value. You are special. Don't ever forget it! Never let yesterday's disappointments overshadow tomorrow's

dreams.

"VALUE HAS A VALUE ONLY IF ITS VALUE IS VALUED"

With moving, I would like to thank our guiders for their support, Manish, Neha, Shashi and Nikunj for compiling

this e-magazine under the planning of Pawan (Vice-chairman, SAMA) and also like to thank all the persons who

helped us directly or indirectly for publishing this e-magazine. We will keep our magazines improving time to time

by your suggestion so keep giving us your valuable comments on the magazine for improvement.

Waiting for your reply……………

Diptesh Nawal

Chairman, SAMA, Ranchi

dipnawal@yahoo.com

RCCA E-NEWS 1

4. COMMITTEE MEMBER OF RCCA

1. Mr. A. K. Sao, Chairman

2. Mr. Sanjay Kr. Singh, Vice-chairman

3. Mr. Ranjit Kr. Agarwal, Secretary

4. Mr. Vidyadhar Prasad, Treasurer

PATRONS of SAMA

1. Mr. A. D. Wadhwa

2. Mr. Ranjit Kr. Agarwal

EXECUTIVE MEMBERS OF SAMA, RANCHI

1. Diptesh Nawal, Chairman

2. Pawan Kumar, Vice Chairman

3. Rajeev Kumar Gupta, Secretary

4. Ekta Arya, Treasurer

COMMITTEE MEMBERS OF SAMA, RANCHI

1. Manish Kumar Tiwari

2. Manjeeta Rana

3. Nikunj Poddar

4. Neha Kumari

5. Gautam Kumar Pandey

COMPILERS OF E-MAGAZINE

Pawan Kumar Shashi Kr. Pandey Nikunj Poddar Neha Kumari

Vice Chairman Member Committee Member Committee Member

RCCA E-NEWS 1

5. ROLE OF FUTURE CMA’S IN CAPITAL MARKET

Swati Kumari

Student, RCCA of ICAI

Email: - swatiakki123@gmail.com

As the outset we should know about Capital Market. It is divided into two categories i.e., Money

Market & Share Market. The latter incorporates all types of shares, debentures & bonds etc. We

shall now focus on the mechanism of Share Market. Share can be defined as the smallest unit or

component of the capital market. Broadly shares can be classified into Equity Shares,

Preference Shares, Bonus Share and Sweat Equity Share.

Now to address the topic at hand, the precise role of future CMAs in the Capital Market.

No doubt we are basically familiar with the job profile of CMAs; I would like to make some

points at this stage. The most critical aspect of CMAs has to do with Investment. Regarding

Investors, It is classified in Individual, QIB (Qualified Institutional Buyers) & HNI (High Net-worth

Individual). Let’s precedes the matter by discussing the real problems faced by the new

investors. Prospective investors with large amount of funds at their disposal are generally seen

to be wary of investing their money, as many times happens to get nil returns etc. The root of

primary cause of their reluctance to shoulder the risk factor is the lack of sound financial

advisors or fund counselors to aid them to channelize their money. At this situation CMAs can

really come in handy, since they are well connected with the exact nature & behavior of the

roller coaster share market. They can show the way forward through lecture-cum-

demonstrations, presentations about the management etc. They can offer the range of services

including talking of future plans, vision & mission of the organization. Providing financial blue

print strategies & landing their financial hindsight.

Also it must be kept in mind that CMAs are the ones who maintain the primary valuation

of shares which are listed on the Share Market. As such they are expected to foresee the trends

& render accurate advice to potential investors. He / She also possess comparatively better &

relevant ideas and concepts about the capital structure of the particular company. Ratio

analysis yields the perfect knowledge about the gross profit, Net profit, capital assets & current

liabilities & many significant points too.

Apart from shares but not much a new investment funds been also accompanying in the

market. It’s very true, it is non-other than mutual funds. General public basically don’t have any

specific ideas regarding the investment made. How to enter & get into flow with the funds and

market up & downs. How to step (invest), when is the correct time, according to the flow of

markets which company would give better return and why to invest in Mutual Funds in spite of

investing or introducing directly to share in open market. Above questions are very genuine and

relevant in sight of investors to company as well. Because of numerous companies has captured

the Market and the customer different plans, strategies, schemes, refund & lots of formalities

RCCA E-NEWS 1

6. not only puzzle them but also misguided them too, Which lead them back with the fear of losing

their huge amount.

Lots of formalities, practices & procedures are required while doing investment or buying

& selling of any instruments of Capital Market. In earlier days all transactions were done

manually and took lots of time but today it’s not so. Every company is running with the waves of

modern and high technique. To cope-up with them each & every individual requires being as

observant as they are, which is quite impossible but here CMAs can favor the investor in dealing

in the Share Market by opening Demat A/c & accomplishing future formalities & hurdles. Earlier

it has been discussed that, cost accountant can act as an investment advisor. So, simultaneously

they can also solve the queries & grievances of public being as middleman between public or

investors and financial institutions like SEBI & RBI. Further the institutions strategies goes on

and finally taken into consideration. Not only this, a Cost Accountant can meet the public as a

share brokers. AS far as their sound knowledge is concern, they can perform the above said job

very well and efficiently. Through motivation they can repulse the General Public towards

investment.

At the end, I would like to conclude the topic by saying that CMAs should implement

ideas which are easy & convenient for the public to understand & instead of being wary they

feel it satisfactory & ease.

With Best Compliments from…………………

Manohar Lal Smriti

RANCHI

(An organisation to motivate and help students of ICAI)

Phone: - 0651-2560572

Country First……….

RCCA E-NEWS 1

7. Audit Material

Shashi Kr. Pandey & Nikunj Poddar

ICAI (INTER)

1. Management Audit

1. Management Audit is an Independent Appraisal Activity.

2. Purpose: To find Out efficiency of Internal Control System.

3. Scope: Very wide than any other Audit.

4. Periodicity: Once in 2-3 Years.

5. Management Auditor has to report to Top Management.

6. Report Submitted to M.D/Executive Director.

7. Management Audit covers that all activities for which Top Management is Responsible.

Who will Conduct Management Audit?

1. Company Talent – include

- Administrative Staff

- Audit Committee

2. Outside Management Consultant

- CA

- CWA

- MANAGEMENT CONSULTANT

2. CARO-2003

1. CARO is A Modified version of MAOCARO.

2. CARO=Companies Auditor’s Report Order, 2003

3. CARO, 2003 is issued by Central Government.

4. Required to follow each and every Company but Exemption is there.

5. Following Indian Company are Exempted from the Provision Of CARO:

- Banking Company

- Insurance Company

- Private Ltd Company which are Exempted

Less Then Whose

50 Lakh Paid Up Capital + Reserves

500 Lakh Annual Turnover

- Company licensed to operate as per the provisions of Sec.25 of Companies Act.

6. As per CARO,2003 Auditor has to give Expert Opinion On Following issues on Auditors’ Report:

- Fixed Assets

- Inventory

- Loans

- Public Deposits

- Sickness

- Fraud

- Maintenance Of Cost Records

- Internal Audit System

- Financial Management etc.

7. To give Expert Comment is mandatory for the Auditor

RCCA E-NEWS 1

8. 3. Branch Audit

1. Normally Company Auditor shall be appointed as a Branch Auditor.

2. Normally: Branch Auditor=Branch Auditor

3. Duty:

- To Prepare Branch Audit Report

- Forward Report to Company Auditor

- If Company Auditor = Branch Auditor, No Need to prepare Branch Auditor.

4. Right:

- Right to access Books, Accounts, Vouchers.

- Right to Obtain Information and Expenses.

- Right to Visit Branch.

5. Do not have a Right:

- To receive Notice of General Meeting.

- To Attend and participate such General Meeting.

6. Remuneration:

- Remuneration received from General Meeting/BOD (as decided in General Meeting).

4. Audit Committee

1. Sec.292 (A) Company Act.1956 Apply.

2. Mandatory for:

- Public Company

- Having Paid Up Capital

3. Minimum:

- Out Of Members minimum 3 must be Director.

- Out of Directors minimum 2/3 must be M.D/W.T.D

4. Duty:

- Interact with Auditors about

A. Internal Control

B. Financial Statement

5. Act as Suggested by B.O.D

6. Scope And Function Of Audit Committee

1. Review of Financial Statement before submission to Board of Directors

2. Selection of Statutory Auditors to be recommended for Appointment

3. To act as Liaison between Statutory Auditor and Board Of Directors

4. Administrative Control of internal control function.

5. To select and Establish Accounting Policies.

6. Review financial Statements and seek clarification from the statutory Auditors.

7. Maintain Internal Audit Operation.

8. Review Expense Accounts of Senior Officers.

7. Benefits Of Audit Committee

1. Ensures reliability and credibility of the functionality of the Management.

2. Helps Board of Directors in discharging their functions properly.

3. Act as a communication link between Internal Auditor, Statutory Auditor & Board of Directors.

4. Act as Evidence in litigation cases in which Board of Directors and other officials of the

organization might be involved.

5. Presentation and Publication of statements relating to Financial Position and Business

Operation.

To be continued with next issue........

RCCA E-NEWS 1

9. CONVERGENCE WITH IFRS

Pawan Kumar

M.Com, ICAI (INTER)

Ranchi Chapter of Cost Accountant

Email- pawaniinrg@gmail.com

India has been seeing a lot of changes in the legal and regulatory environment in the recent time

including New Direct Tax Code, Companies Bill, 2009, Goods & Service Tax (GST) and Adoption of

IFRS, even though all these proposed changes are presently in draft form. Keeping in view the fact that

International Financial Reporting Standards (IFRS) are fast becoming the global accounting and

financial reporting language, Indian accounting practices are set to converge with IFRS from 01.04.2011

in a phased manner as announced by Ministry of Corporate Affairs and The Institute of Chartered

Accountants of India (ICAI). More than 100 countries all over the world have already adopted IFRS and

many more including India, Korea, Brazil and Canada have committed to make the transition by 2011.

How IFRS Can Be Adopted?

IASB recognizes two ways of adopting IFRS by the member countries. These ways are:

1. Adopting IFRS in verbatim

2. Convergence with IFRS

While the former refers to replacing the national Accounting Standards with International Financial

Reporting Standards, the latter incorporates the IFRS provisions in the national Accounting Standards to

make those IFRS compliant.

Convergence with IFRS

Convergence with IFRS refers to achieving harmony of national accounting practices with IFRS. It may

be important to note that as per Statement of Best Practices: Working Relationship between the IASB and other

Accounting Standard-Setters issued by The International Accounting Standards Board (IASB),

convergence with IFRS does not mean adoption of IFRS in to, but adoption of IFRS provisions. Hence,

when the Indian standards will be converged to IFRS, the compliance with Indian Accounting

Standards would automatically ensure compliance with IFRS. The Accounting Standards Board is

however free to eliminate any optional treatments provided in IFRS or provide for any additional

disclosure requirements in the road to convergence.

Benefits of Convergence with IFRS

1) Improved Access to International Capital Markets – Comparable financial reporting across firms

from different countries facilitates access to international capital markets.

2) Access to Low-cost Foreign Funds – Accounting and reporting on common accounting principles

provide access to foreign funds through higher acceptability of the global accounting language, thereby

leading to higher FII inflow and lower cost of capital.

3) Easier Comparability with Global Peers – Global reporting language in the form of IFRS is bound to

facilitate the comparability of an enterprise with not only its national competitors but global peers as

well.

4) Elimination of Multiple Reporting Costs – Multinationals having global operations in IFRS driven

countries will find cost savings by having all their business units/investments on a common accounting

platform. Further, the IFRS-compliant financial statements will eliminate multiple reporting in different

accounting standards in different countries.

5) Opportunities for Professionals – Being a comparatively new subject, professionals with sound

theoretical and practical knowledge of IFRS are certain to have more opportunities in the times to come.

RCCA E-NEWS 1

10. IFRS & IAS – Are These Terms Synonymous?

IFRS stands for International Financial Reporting Standards and includes Standards & Interpretations

adopted by International Accounting Standards Board (IASB) including International Accounting

Standards (IAS) and Interpretations developed by International Financial Reporting Interpretation

Committee (IFRIC). Hence, IFRS is a wider term and includes previously issued IAS as well. IASB

started issuing the standards using the term International Financial Reporting Standards (IFRS) to

emphasize upon its commitment towards better financial reporting after some Accounting Scandals

such as Enron came into picture. So, it should be made clear that 29 IAS and 8 IFRS issued by IASB

stand at par in terms of financial accounting & reporting and when one talks of an entity being IFRS

compliant, it covers the compliance of an entity with IAS as well.

Roadmap to Convergence with IFRS

Ministry of Corporate Affairs has constituted a Core Group for convergence of Indian Accounting

Standards with International Financial Reporting Standards (IFRS). The group has a consensus on the

fact that the convergence with IFRS is to be done in a phased manner based upon the public

accountability of the company. Acknowledging the fact that there would be two categories of companies

at any given point of time till the convergence process gets completed, the Core Group has agreed that

there will be two separate sets of Accounting Standards u/s Section 211(3C) of Companies Act, 1956.

1. First set would comprise of the Indian Accounting Standards which have been converged with IFRSs

which shall be applicable to the specified class of companies.

2. The second set would comprise of the existing Accounting Standards which would be applicable to

the rest of the companies to which First Set of converged Accounting Standards is not applicable

including Small & Medium Companies (SMCs).

Phased Applicability of Converged Accounting Standards

Types of Companies Date of Applicability & Specified Class of Companies

Companies other than 01.04.2011

Companies which are part of NSE – Nifty 50

Banking Companies, NBFCs

Companies which are part of BSE – Sensex 30

and Insurance Companies Companies whose shares or other securities are listed

On stock exchanges outside India

Companies, whether listed or not, which have a net

Worth in Excess of Rs. 1000 crores.

01.04.2013

Companies, whether listed or not, which have a net worth

exceeding Rs. 500 crores but not exceeding Rs. 1000 crores

01.04.2014

Listed Companies which have a net worth of Rs. 500 crores or Less

Companies which do not fall into the above categories i.e.

RCCA E-NEWS 1

11. Non - listed companies with net worth of Rs. 500 crores or less and

whose shares or other securities are not listed on stock exchanges

outside India, and

Small & Medium Companies (SMCs) will not be required to follow

the converged Accounting Standards, though they can voluntarily

opt to do so.

Banking Companies 01.04.2013

All scheduled commercial banks

All Urban Co-operative Banks (UCBs) with net worth exceeding

Rs. 300 crores

01.04.2014

Urban Co-operative Banks which have a net worth Exceeding Rs.

200 crores but not exceeding Rs. 300 crores Banks which do not

fall into the above categories i.e.

Urban Co-operative Banks with net worth of Rs. 200 crores or less,

and

Regional Rural Bank (RRBs) will not be required to follow the

converged Accounting Standards, though they can voluntarily opt

to do so.

Insurance Companies 01.04.2012 for all the insurance companies

NBFCs 01.04.2013

Companies which are part of NSE – Nifty 50

Companies which are part of BSE – Sensex 30

Companies, whether listed or not, which have a net worth in excess

of Rs. 1000 crores.

01.04.2014

All listed NBFCs

Unlisted NBFCs which have a net worth exceeding Rs. 500 crores

but not exceeding Rs. 1000 crores NBFCs which do not fall into the

above categories i.e. non – listed NBFCs having a net worth of Rs.

500 crores or less will not be required to follow the converged

Accounting Standards, though they can voluntarily opt to do so.

The specified class of companies would be required to convert their opening balance sheets as on the

specified dates according to the first set of Accounting Standards. The converged Accounting Standards

would be applicable to specified class of companies in a staggered form as per the following schedule:

Further, it has been made clear by the Core Group that once an entity starts following

Converged Accounting Standards, it cannot switch back to the existing Accounting Standards in any

case, even if it stops fulfilling any of the conditions for applicability of converged Accounting Standards.

Basic Differences between Existing Standards and IFRS

While there are many differences between the existing set of Accounting Standards and IFRS, few of the

basic differences are being listed below,

RCCA E-NEWS 1

12. S. No. Indian GAAP Indian GAAP

1 Financial Statements are presented upon Financial Statements are prepared on

standalone basis, unless required by any other Consolidated basis.

law/regulations.

2 Depreciation on Fixed Assets is charged on asset as Depreciation on Fixed Assets is charged on

a whole. components of Fixed Assets.

3 Proposed Dividend is required to be shown as Dividend is to be recorded and shown in the

Current Liability in the financial statements of the financial statements in the financial year in

financial year to which it relates as per which it is declared

requirements of Schedule VI of the Companies Act.

4 Prior Period items are shown as a separate item in Adjustments for the prior period items are

Income Statement in the year it is detected. made retrospectively.

5 In case of conflict between law and AS, former In case of conflict between law and IFRS,

prevails latter prevails.

These are just a few of the differences between Indian GAAP (Generally Accepted Accounting

Principles) and IFRS. It can be noticed that there are several legal and regulatory issues before complete

convergence with IFRS can be achieved. However, steps have already been initiated in this direction by

the concerned agencies:

1) The Institute of Chartered Accountants of India– ICAI has already issued Exposure Drafts for AS 17

Operating Segments (Corresponding to IFRS 8), AS 15 Employee Benefits (Corresponding to IAS 19), AS 9

Revenue (Corresponding to IAS 18), AS 39 Insurance Contracts (Corresponding to

IFRS 4), AS 38 Agriculture (Corresponding to IAS 41), AS 26 Intangible Assets (Corresponding to IAS 38),

AS 33 Share Based Payments (Corresponding to IFRS 2), AS 36 Accounting and Reporting by Retirement

Benefit Plans (Corresponding to IAS 26), AS 22 Income Taxes (Corresponding to IAS

12), AS 28 Impairment of Assets (Corresponding to IAS 36), AS 27 Interest in Joint Ventures (Corresponding

to IAS 31) and AS 24 Non-current Assets Held for Sale and Discontinued Operation

(Corresponding to IFRS 5) for comments from interested groups and general public at large.

2) Securities Exchange Board of India – SEBI has already amended listing agreement allowing for

voluntary adoption of IFRS by the listed companies having subsidiaries vide circular dated

April 5, 2010. This is positive step towards encouraging voluntary adoption of IFRS.

3) Ministry of Corporate Affairs – Schedule VI of Companies Act, 1956 and suitable amendments in the

Companies Act, 1956 are proposed to be introduced in a time bound manner.

Unanswered Issues, while the Ministry of Corporate Affairs remains committed towards initiation of

convergence of IFRS in India by 2011, there are several issues which remain unanswered at this point of

time and suitable clarifications are awaited from the concerned regulatory authorities. Few of these

issues are:

1) Deferred Tax Assets/Liabilities arising out of retrospective application of IFRS in Transition Year as

per AS-22 Taxes on Income

2) Applicability of Minimum Alternative Tax (MAT) in transition year and the availability of MAT

Credit thereon as the impact of transition from present Accounting Standards to the converged

Accounting Standards on the financial statements and book profits especially is estimated to be huge.

3) Unrealized losses and gains on derivatives are required to be marked-to-market under IFRS.

Taxation issues arising out of these notional gains & losses are still awaited to be clarified. Convergence

with IFRS is hence a lengthy & tedious process and it is hoped that India makes a smooth transition

towards adoption and compliance of IFRS, though the same is likely to affect India Inc. in the early years

of adoption.

RCCA E-NEWS 1

13. LIST OF FORM FOR RETURN FILLING & SERVICE TAX

Diptesh Nawal

Ranchi Chapter of Cost Accountants

Email: - dipnawal@gmail.com

Service Tax Forms

FORM NO SUBJECT

FORM ST- 1 Application form for Registration

FORM ST- 2 Performa of Registration Certificate

FORM ST- 3 New Form for Return of Service Tax

FORM ST-3A Memorandum of Provisional Deposit

FORM ST- 4 Form of Appeal to Commissioner (Appeals)

FORM ST- 5 Form of Appeal to Tribunal

FORM ST- 6 Form of Memo of cross objection to Tribunal

FORM ST- 7 Form of Application to Tribunal by Department

ST GAR7 Challan Service Tax GAR7 Challan

FORM TR- 6 Challan Form for deposit of service tax

FORM AAR (ST) Application for Advance Ruling

FORM ASTR -1 Application for filing a claim of rebate of service tax and cess paid on

taxable services exported

FORM ASTR -2 Application for filing a claim of rebate of duty paid on inputs, service

tax and cess paid on input services

Vakalatnama For appointing a lawyer for hearing in court

Income Tax Forms

Form No.

Particulars

ITR-1 SAHAJ Indian Individual Income tax Return English Form

ITR – V Acknowledgment

ITR-2 For Individuals and HUFs not having Income from Business English Form

or Profession ITR – V Acknowledgment

ITR-3 For Individuals/HUFs being partners in firms and not English Form

carrying out business or profession under any proprietorship ITR – V Acknowledgment

SUGAM (ITR- Sugam - Presumptive Business Income tax Return English Form

4S) ITR – V Acknowledgment

ITR-4 For individuals and HUFs having income from a proprietary English Form

business or profession ITR – V Acknowledgment

ITR-5 For firms, AOPs and BOIs English Form

ITR – V Acknowledgment

ITR-6 For Companies other than companies claiming exemption English Form

under section 11 ITR – V Acknowledgment

ITR-7 For persons including companies required to furnish return English Form

under section 139(4A) or section 139(4B) or section 139(4C)

or section 139(4D)

Acknowledgment ITR – V Acknowledgment

RCCA E-NEWS 1

14. Accounting Dictionary

Neha Kumari

ICAI (INTER)

AAA is American Accounting Association, Association of Accounting Administrators, or see

ACCUMULATED ADJUSTMENT ACCOUNT.

AAA-CPA is American Association of Attorney-Certified Public Accountants.

AACSB is American Assembly of Collegiate Schools of Business.

AAFI is Associated Accounting Firms International.

AAHCPA is American Association of Hispanic CPAs.

A&E can mean either Appropriation & Expense or Analysis & Evaluation.

A&G is Administrative & General.

A&M is Additions and Maintenance.

A&P is an acronym for Administrative and Personnel.

AAT, in Great Britain, is Association of Accounting Technicians.

ABA is the American Bar Association. See below also.

ABA (Accredited Business Accountant or Accredited Business Advisor), in the US, is a national

credential conferred by Accreditation Council for Accountancy and Taxation to professionals who

specialize in supporting the financial needs of individuals and small to medium sized businesses.

ABA is the only nationally recognized alternative to the CPA. Most accredited individuals do not

perform audits. Generally, they are small business owners themselves. In addition to general

accounting work, CPAs are also heavily schooled in performing audits; however, only a small

fraction of America's businesses require an audit. In general, a CPA has majored in accounting,

passed the CPA examination and is licensed to perform audits. An ABA has majored in accounting,

passed the ABA comprehensive examination and in most states is not licensed to perform audits.

ABATEMENT, in general, is the reduction or lessening. In law, it is the termination or suspension of

a lawsuit. For example, an abatement of taxes is a tax decrease or rebate.

ABNORMAL RETURNS is the difference between the actual return and that is expected to result

from market movements (normal return).

ABNORMAL SPOILAGE is spoilage that is not part of everyday operations. It occurs for reasons

such as the following: out-of-control manufacturing processes, unusual machine breakdowns, and

unexpected electrical outages that result in a number of spoiled units. Some abnormal spoilage is

considered avoidable; that is, if managers monitor processes and maintain machinery appropriately,

little spoilage will occur. To highlight these types of problems so that they can be monitored,

abnormal spoilage is recorded in a Loss from Abnormal Spoilage Account in the general ledger and

is not included in the job costing inventory accounts (work in process, finished goods, and cost of

goods sold).

ABOVE THE LINE, in accounting, denotes revenue and expense items that enter fully and directly

into the calculation of periodic net income, in contrast to below the line items that affect capital

accounts directly and net income only indirectly.

ABOVE THE LINE, for the individual, is a term derived from a solid bold line on Form 1040 and

1040A above the line for adjusted gross income. Items above the line prior to coming to adjusted

gross income, for example, can include: IRA contributions, half of the self-employment tax, self-

RCCA E-NEWS 1

15. employed health insurance deduction, Keogh retirement plan and self-employed SEP deduction,

penalty on early withdrawal of savings, and alimony paid. A taxpayer can take deductions above the

line and still claim the standard deduction.

ABSOLUTE CHANGE is a numerical change in an empirical value, e.g. cost of goods was reduced

by $9.00.

ABSORB is to assimilate, transfer or incorporate amounts in an account or a group of accounts in a

manner in which the first entity loses its identity and is "absorbed" within the second entity. For

example, see ABSORPTION COSTING.

ABSORBED COSTS incorporates both variable and fixed costs.

ABSORPTION see ABSORB.

ABSORPTION COSTING is the method under which all manufacturing costs, both variable and

fixed, are treated as product costs with non-manufacturing costs, e.g. selling and administrative

expenses, being treated as period costs.

ABSORPTION PRICING is where all costs, both fixed and variable; plus a percentage mark-up for

profit; are recovered in the price.

ABSORPTION VARIANCE is the variance from budgeted absorption costing of manufactured

product. See also ABSORPTION COSTING.

ACA is Accreditation Council for Accountancy.

ACAT (Accreditation Council for Accountancy and Taxation) is a national organization established in

1973 as a non-profit independent testing, accrediting and monitoring organization. The Council

seeks to identify professionals in independent practice who specialize in providing financial,

accounting and taxation services to individuals and small to mid-size businesses. Professionals

receive accreditation through examination and/or coursework and maintain accreditation through

commitment to a significant program of continuing professional education and adherence to the

Council's Code of Ethics and Rules of Professional Conduct.

ACB normally refers to 'adjusted cost base.'

ACCELERATED DEPRECIATION is a method of calculating depreciation with larger amounts in the

first year(s).

ACCEPTANCE is a drawee's promise to pay either a TIME DRAFT or SIGHT DRAFT. Normally, the

acceptor signs his/her name after writing "accepted" (or some other words indicating acceptance)

on the bill along with the date. That "acceptance" effectively makes the bill a promissory note, i.e.

the acceptor is the maker and the drawer is the endorser.

ACCOMODATION ENDORSEMENT is a) the guarantee given by one legal entity to induce a lender

to grant a loan to another legal entity. b) a banking practice where one bank endorses the

acceptances of another bank, for a fee, qualifying them for purchase in the acceptance market.

ACCOUNT is the detailed record of a particular asset, liability, owners' equity, revenue or expense.

ACCOUNT AGING usually refers to the methods of tracking past due accounts in accounts

receivable based on the dates the charges were incurred. Account aging can also be used in

accounts payable, to a lesser degree, to monitor payment history to suppliers. See also AGING OF

ACCOUNTS.

ACCOUNT ANALYSIS is a way to measure cost behavior. It selects a volume-related cost driver and classifies

each account from the accounting records as a fixed or variable cost. The cost accountant then looks at each

RCCA E-NEWS 1

16. cost account balance and estimates either the variable cost per unit of cost driver activity or the periodic fixed

cost.

ACCOUNTANT'S OPINION is a signed statement regarding the financial status of an entity from an

independent public accountant after examination of that entities records and accounts.

ACCOUNT-CLASSIFICATION METHOD, also called account analysis, is a cost estimation method that

requires a study of an account in the general ledger. The experienced analysts use the account information as

well as their own judgment to determine how costs will behave in the future.

ACCOUNT CURRENT is a running or continued account between two or more parties, or a statement of the

particulars of such an account.

ACCOUNT DISTRIBUTION is the process by which debits and credits are identified to the correct accounts.

ACCOUNT GROUP, in accounting, is a designation of a group of accounts of like type (for example: accounts

receivable and fixed assets).

ACCOUNTING is primarily a system of measurement and reporting of economic events based upon the

accounting equation for the purpose of decision making. Generally, when someone says "accounting" they are

referring to the department, activity or individuals involved in the application of the accounting equation.

ACCOUNTING CONCEPTS are the assumptions underlying the preparation of financial statements, i.e., the

basic assumptions of going concern, accruals, consistency and prudence.

ACCOUNTING CONVENTION see CONVENTION.

ACCOUNTING CYCLE is the sequence of steps in preparing the financial statements for a given period. It refers to

the fact that because financial reports are given each period (usually a year) there are a set of steps (cycle) taken

each period that result in the reports and preparation for the next period or cycle. The term cycle is used because

every period there is a start and an end. The cycle usually starts with the budget, goes through the journal

entries, adjusting entries, posting to the accounts, financial reports, and closings.

ACCOUNTING DATA is all the information and data contained in journals, ledgers and other records that

support financial statements, e.g. spreadsheets. It may be in computer readable form or on paper.

ACCOUNTING DIVERSITY is the recognition that many diverse national and international accounting

standards exist in the world.

ACCOUNTING ENTITY ASSUMPTION states that a business is a separate legal entity from the owner. In the

accounts the business’ monetary transactions are recorded only.

ACCOUNTING ENTITY is an organization, institution or being that has its own existence for legal or tax purposes.

An accounting entity is often an organization with an existence separate from its individual members--for

example, a corporation, partnership, trust, etc. See also ACCOUNTING ENTITY ASSUMPTION.

To be continued with next issue........

RCCA E-NEWS 1

17. STUDENTS’ASSOCIATIONOF MANAGEMENTACCOUNTANTS (SAMA)

of Ranchi Chapter of Cost Accountant of EIRC of ICAI

303, Gridhar Plaza, Near Gaushala, Harmu Road, Ranchi

E-mail:-samaranchi14@gmail.com

REGISTRATION FORM S. No. ………….

Fill in Block Letters. Leave one box blank between words. * mark fields are necessary to be filled.

*Full Name:

*Address :

*Date of Birth *Male Female

*Phone No. *E-mail Id:

*Foundation Group: - I II III IV [Tick the correct box (es)]

*Inst. Registration No. Year

Academic Qualification……………………………………………………

Pursuing any other Course (s) / Qualification: Yes No (If Yes, write the details in the space provided.)

Qualification University/Institution Remarks

Association Registration No.(To be S R / 0 0 0 filled by the officials)

Declaration

I declare that to the best of my knowledge and belief the information given above is correct and complete in all

respects, in the event of being found otherwise I shall abide by the decision of the Association to summarily

reject my application. I also undertake to abide by the regulations framed by the Association.

Date:

Enclosure: ..……………………………………….

1. One Passport Size Photo. Signature of Applicant

2. Xerox of Inst. Identity Card.

Students’ Association of Management Accountants (SAMA)

For Office Use Only Sl. No.: ……………

Name (Mr. / Ms.): ………………………………………………………...……………………………………………...........

Association Registration No. S R / 0 0 0

Amount Towards: Registration Fees/Membership Fees

In words: ` One Hundred only ` 100.00

Date: ............................................................

Recipient’s Signature

RCCA E-NEWS 1

18. SAMA’s By-laws

Objective: - SAMA, an association created by the students of ICAI (Earlier ICWAI) for the

development of its members by organizing events, classes, interviews, workshops

and other problems regarding their study & chapter etc.

Membership: -

Students of Ranchi Chapter of ICAI only can become the member of SAMA

Membership Fees: -

For membership of the Association Students have to pay Rs. 100/- and an Annual

Subscription of Rs. 50/- only.

Terms, Rules & Regulations:-

1. Office of the SAMA will be at the concerned chapter of the ICAI

2. Every member should have to attend the meeting of the association on 4th Sunday of

each month at the pre-decided place (scheduled timings may change if committee

think so.

3. Association should consists of two categories,

a. Managing Committee- Managing Committee will be decided by the existing

chairman under the guidance of Patrons and should consist of

i. Chairman

ii. Vice- Chairman

iii. Secretary

iv. Treasurer

b. Patrons- Cost Accountants having the membership of the Institute, can only

become the Patron of the Association by paying Rs. 500.

4. In the following cases membership of the members will be terminated:

a. If they found guilty of practicing unwanted means within the Association.

b. If they complete their study in the Institute or become the member of the

Institute, i.e. ICAI.

c. If they crosses the age of 29 years.

5. Association will have to maintain its accounts and get it audited every year by a Cost

Accountant.

6. It should call its AGM on 4th Sunday of May every year and present the audited

account in front of members.

7. Members should have a valid mail id for effective communication.

RCCA E-NEWS 1

19. Desk of Compilers

Dear Readers,

Since its inception from 14.11.2010, SAMA is trying to magnify the quality inherent in the students in the areas of

cost accountancy. To achieve the goal, Students’ Association of Management Accountants (SAMA) of Ranchi

Chapter is organizing many events for development and updation of the knowledge of its members and of the

chapter’s students.

Recently, SAMA has organized Business Quiz in Ranchi Chapter of Cost Accountant, venue was in Capitol Hill,

Ranchi on 13.11.2011 and in this Quiz many student had participated. The quiz master was Mr. A. D. Wadhwa

along with Score calculator Mr. Pawan Kumar & Mr. Krishna Kr. Sharma.

Besides this SAMA is also organizing many workshops time to time on different topics like dress code, personality

development and some extra classes are being taken by senior student for juniors in different subjects which will

help them in their examination.

In future too, we look forward to carry the same for promotion and development of our members.

Note: - You can also get you articles published in E-magazine, for that sends your article in our mail id, i.e.

samaranchi14@gmail.com

MEMORIES FROM REGIONAL COST CONFERENCE 2011

RCCA E-NEWS 1

20. Delegates inaugurating the Phone Directory of RCCA. Group photo of Students of RCCA with Mr. A. D

Wadhwa.

Contestants of Bussiness Quiz, organised by SAMA Manjeeta Rana receiving the award “Best student

on the day of Annual Seminar of Ranchi Chapter. of the year 2011”.

.

Volunteers of annual seminar 2011. Volunteers & Students with Mr. A. D. Wadhwa Past

Chairman, EIRC, Mr. Sanjay Kr. Singh Vice-chairman,

RCCA & Mr. Ranjit Agarwal, Secretary RCCA in

annual seminar 2011.

RCCA E-NEWS 1