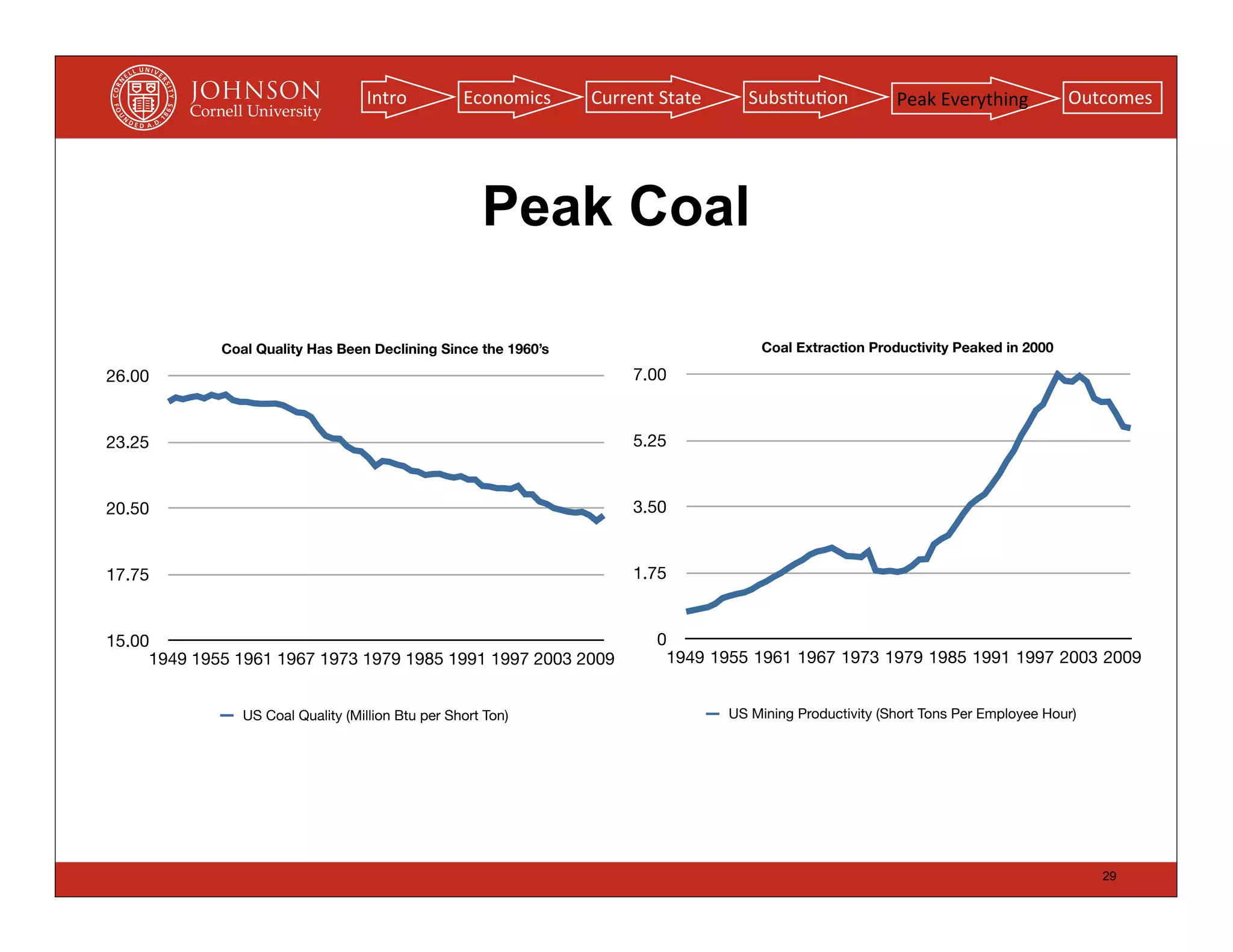

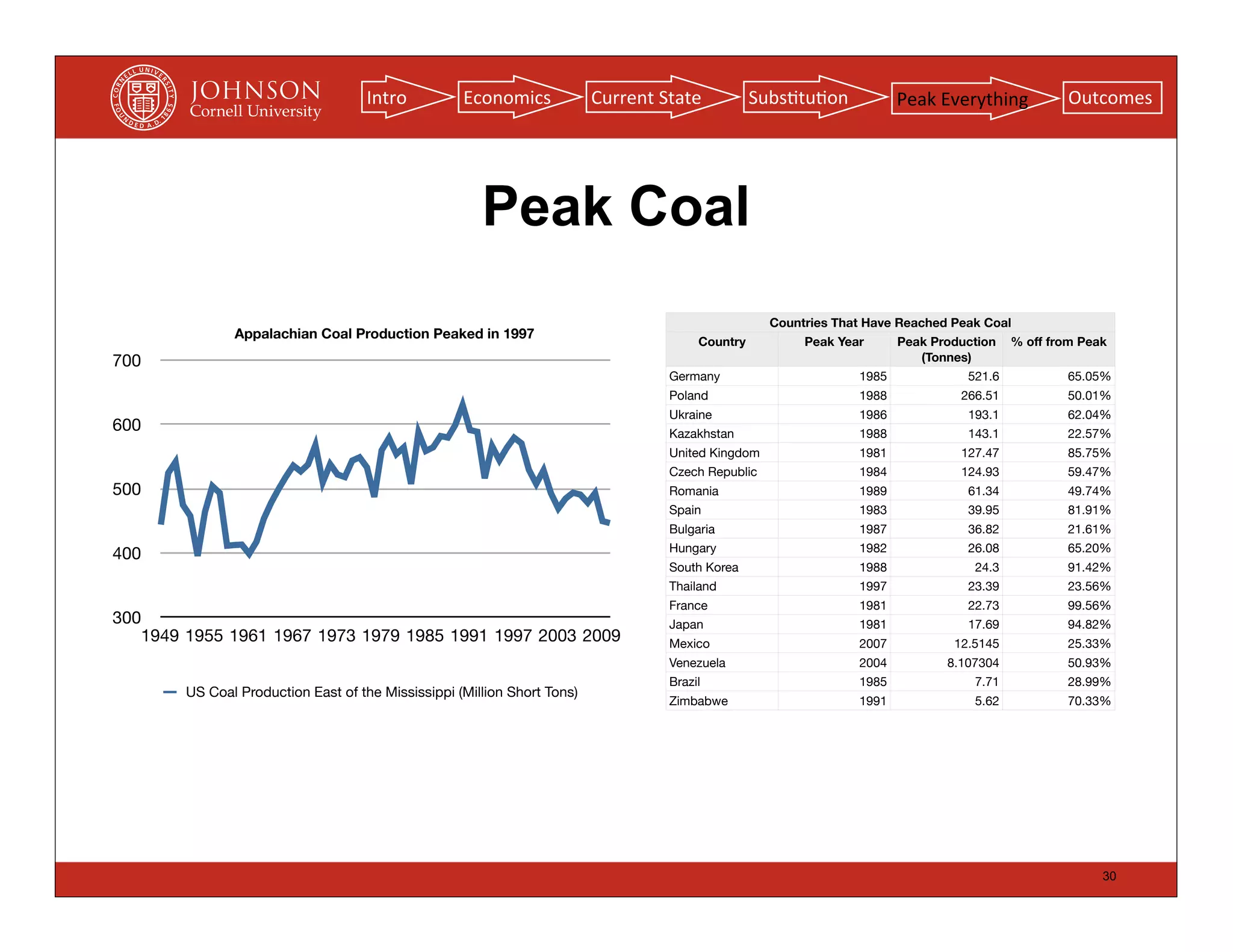

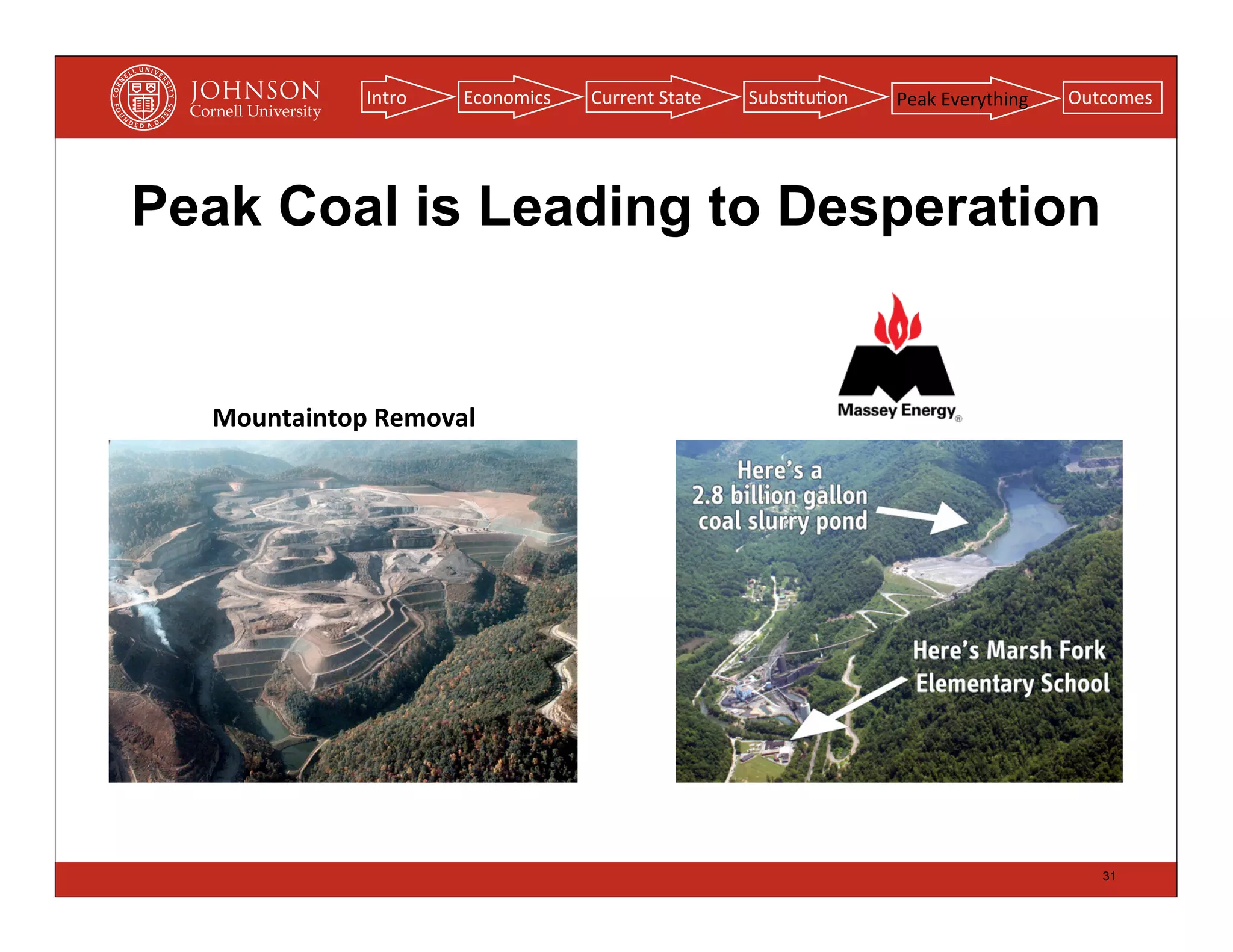

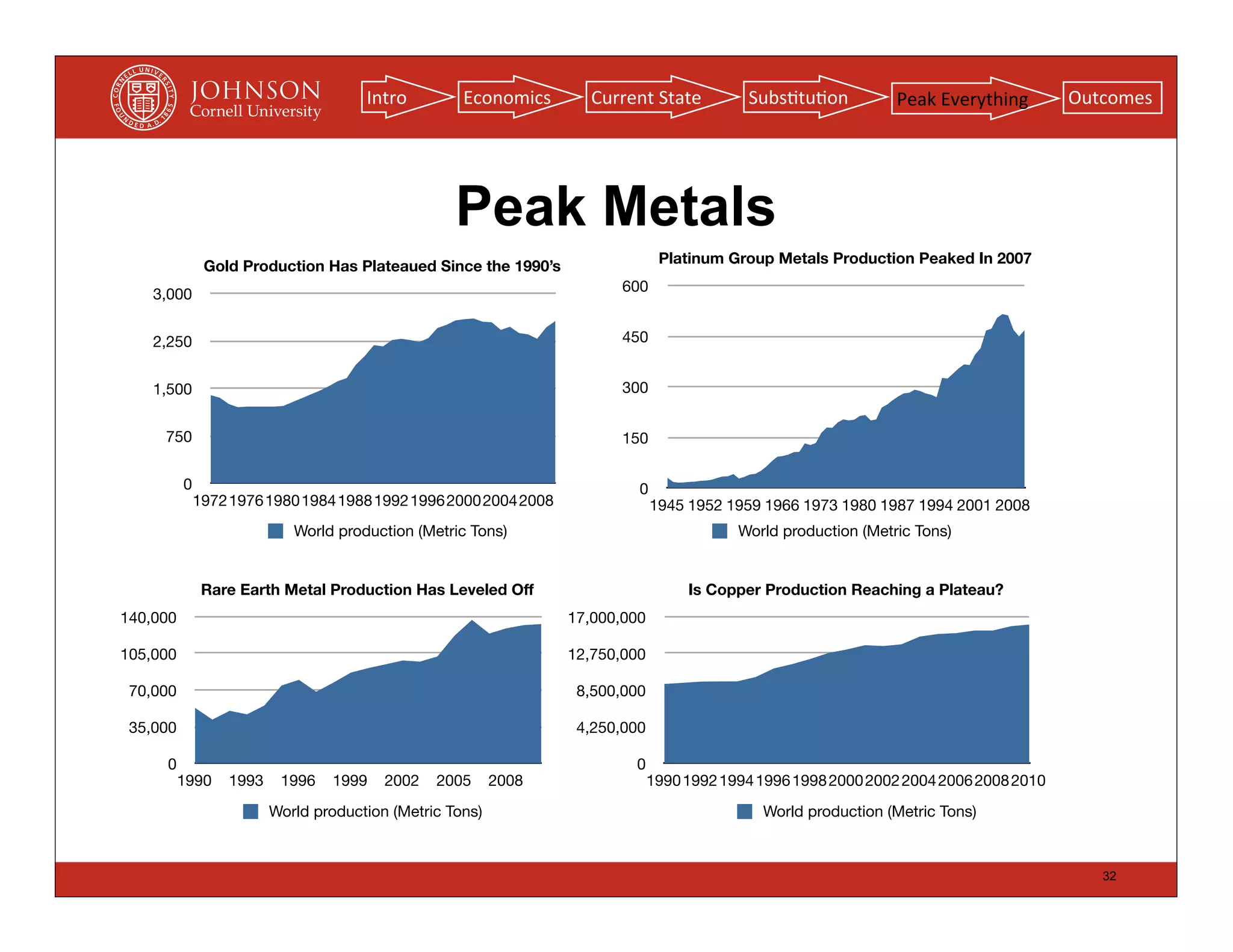

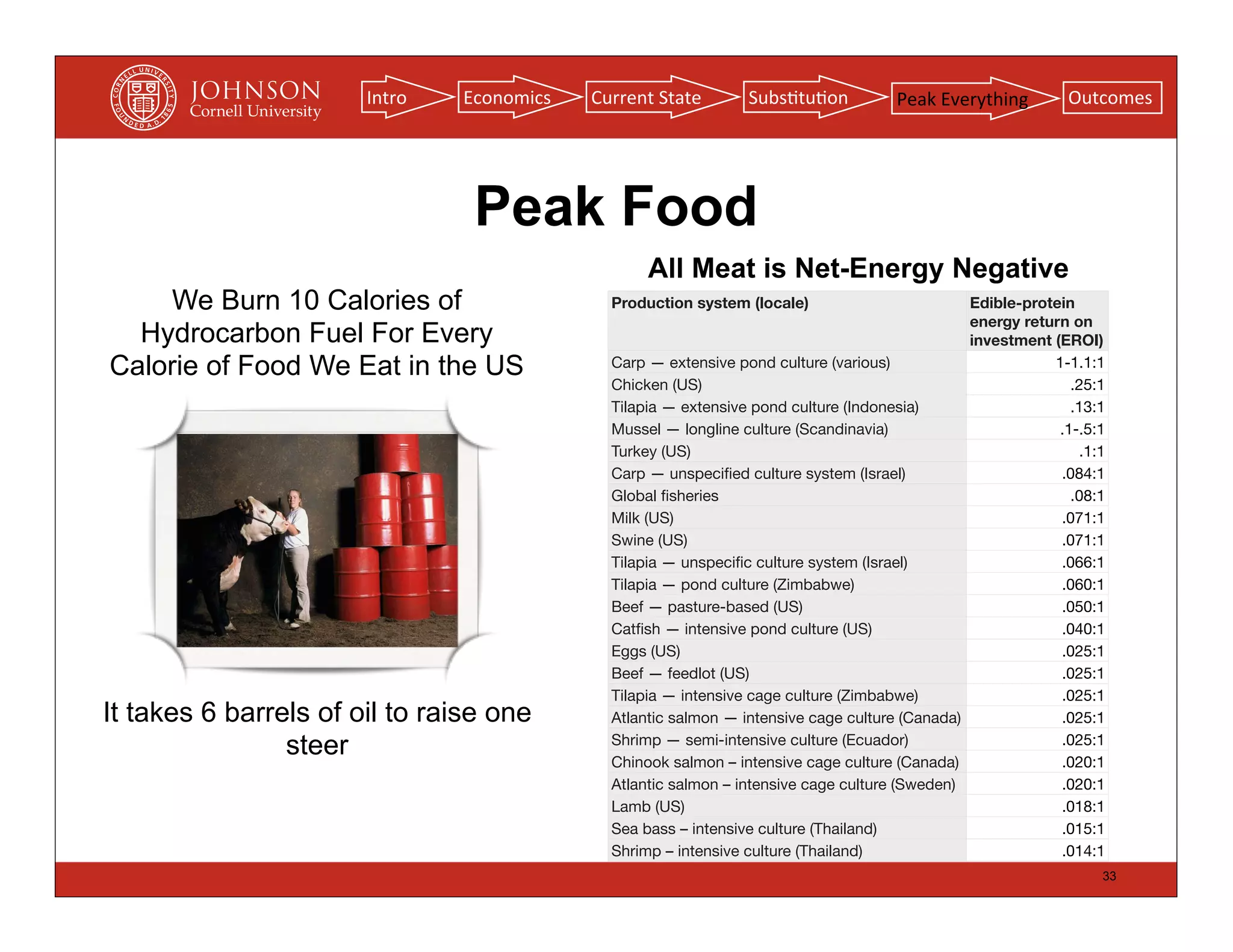

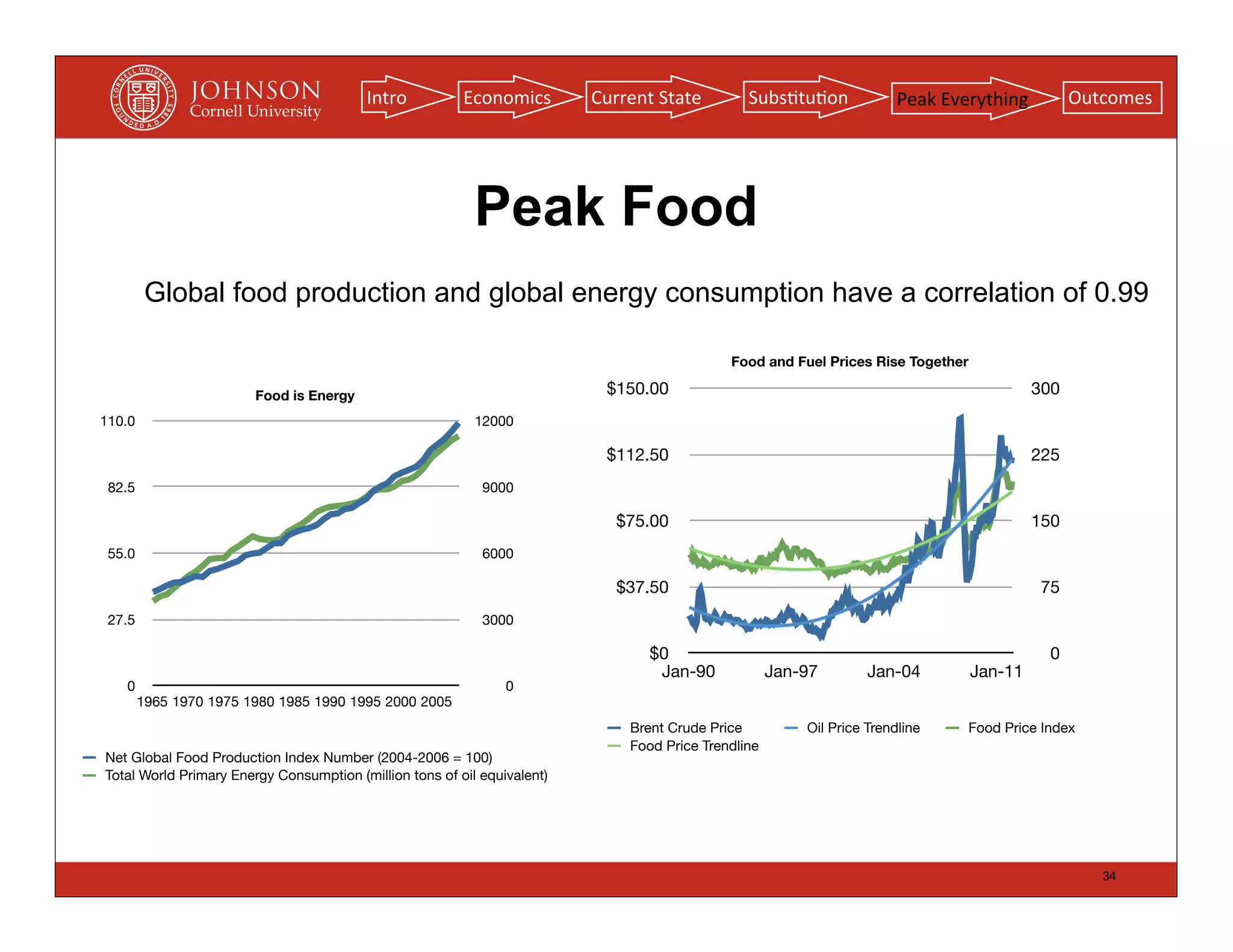

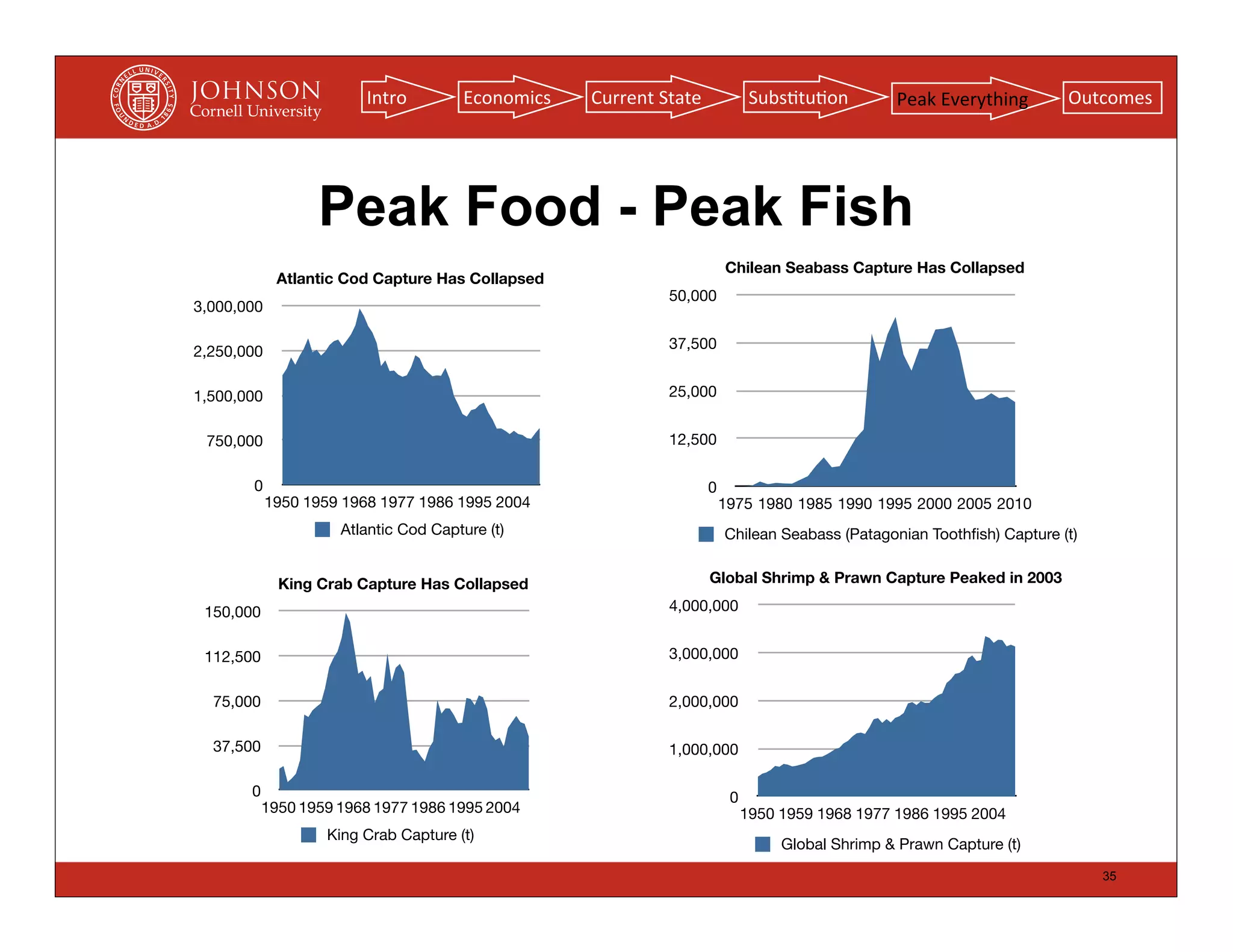

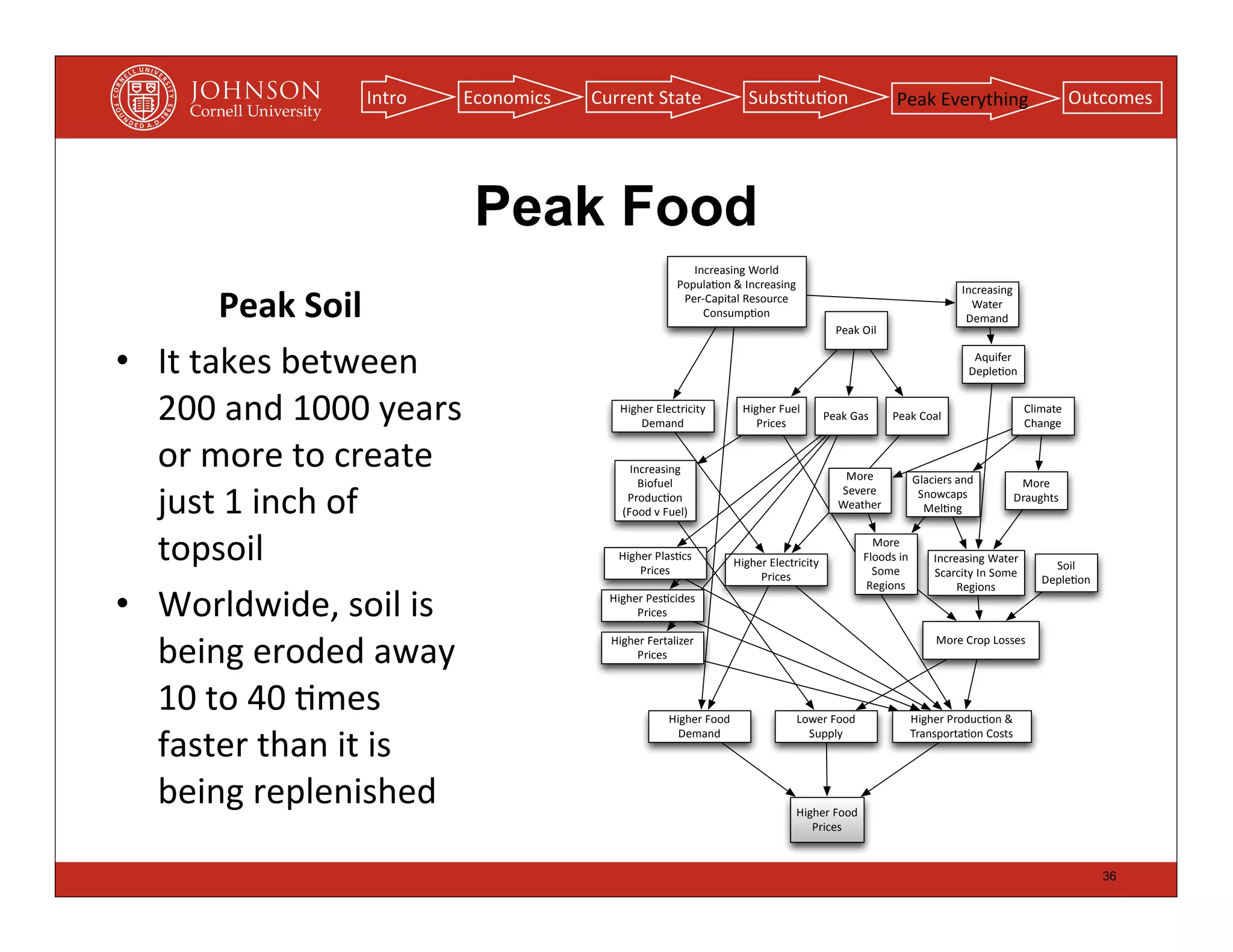

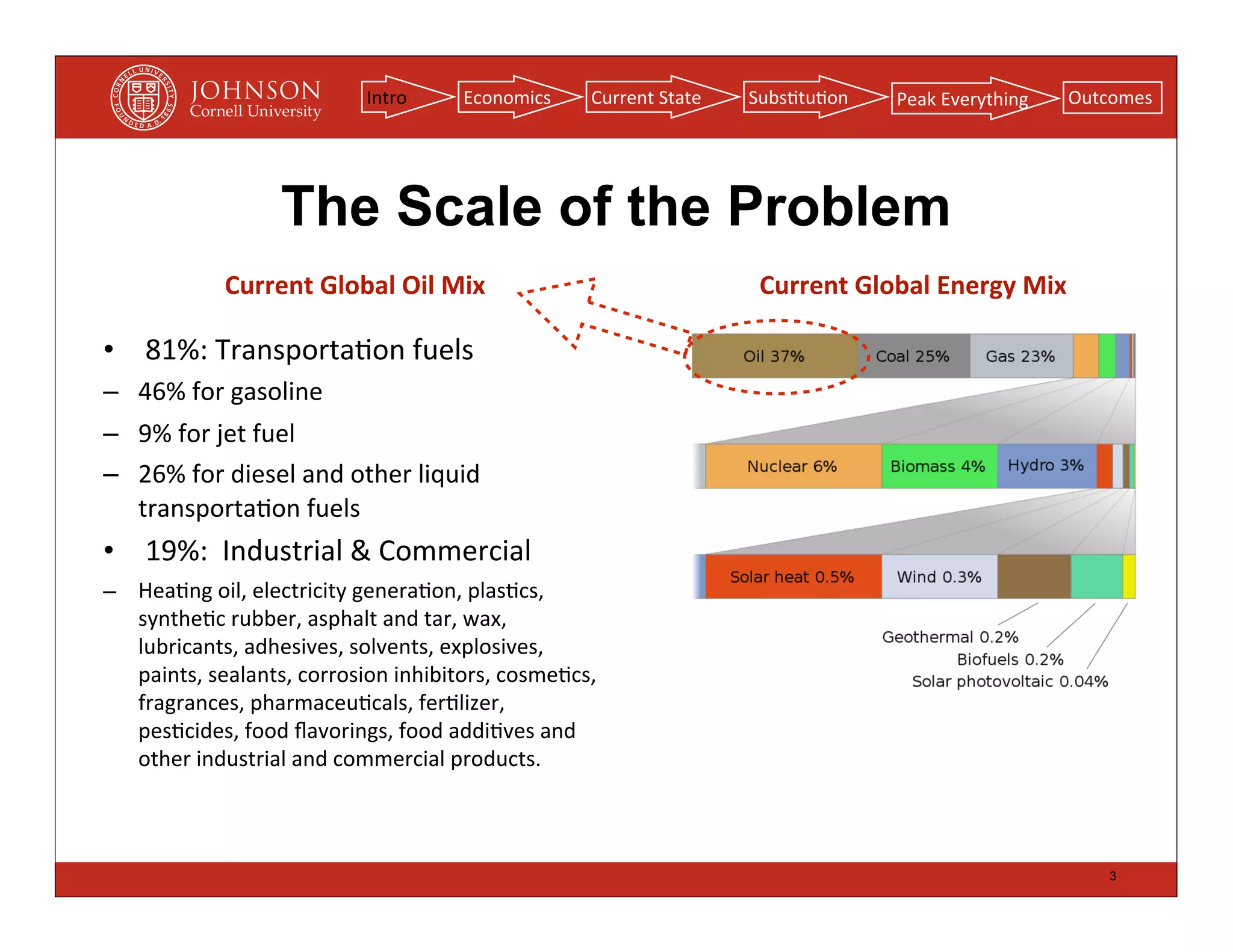

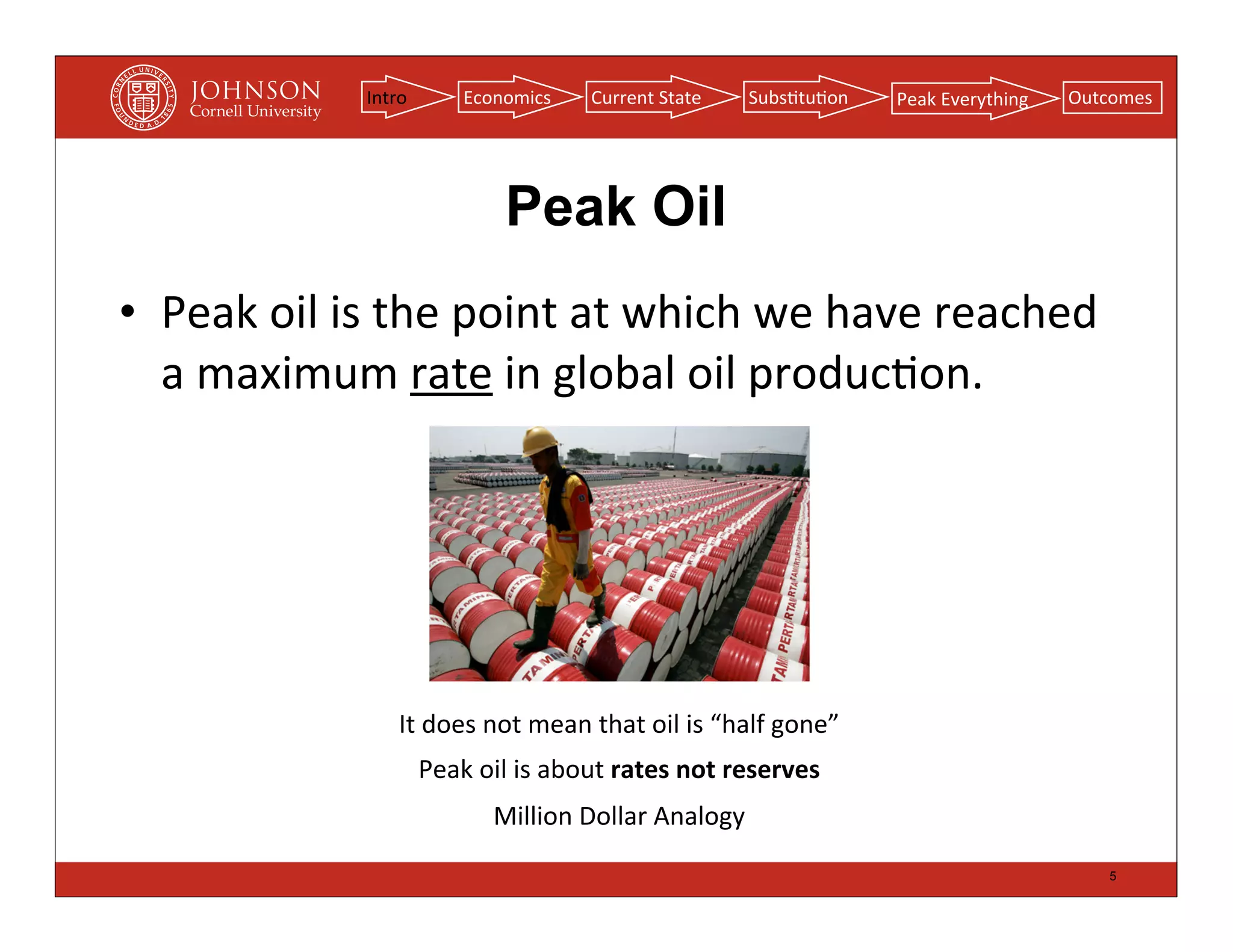

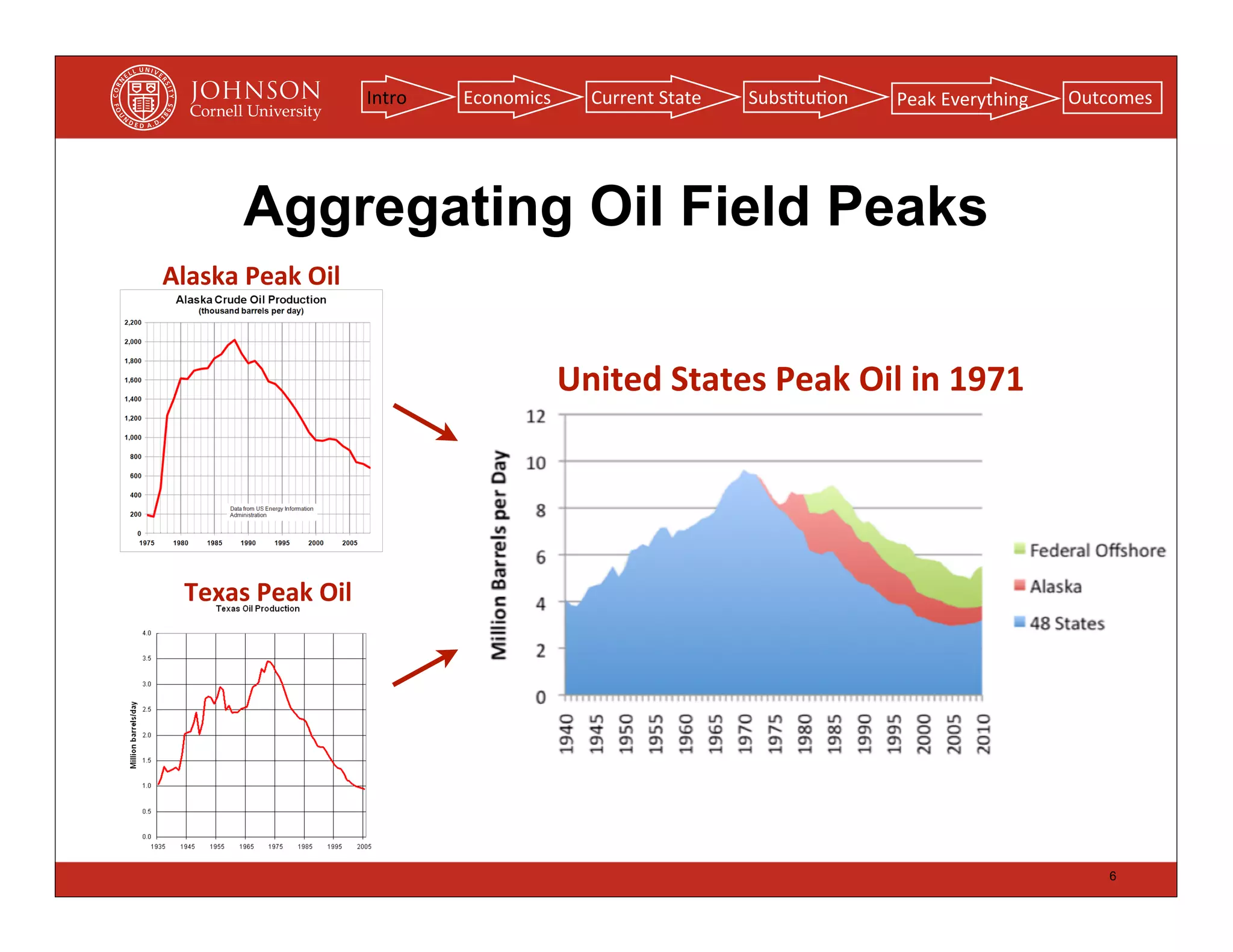

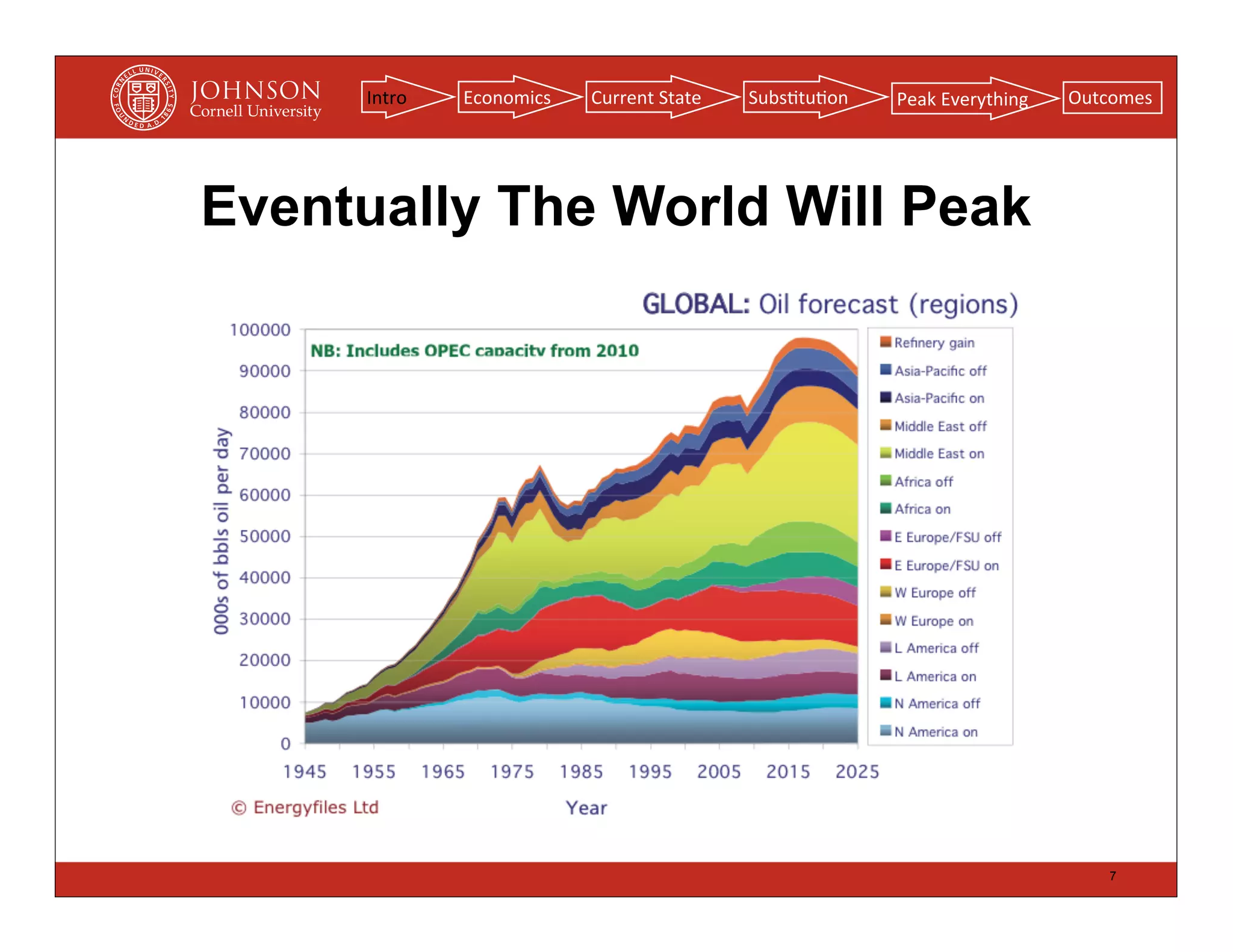

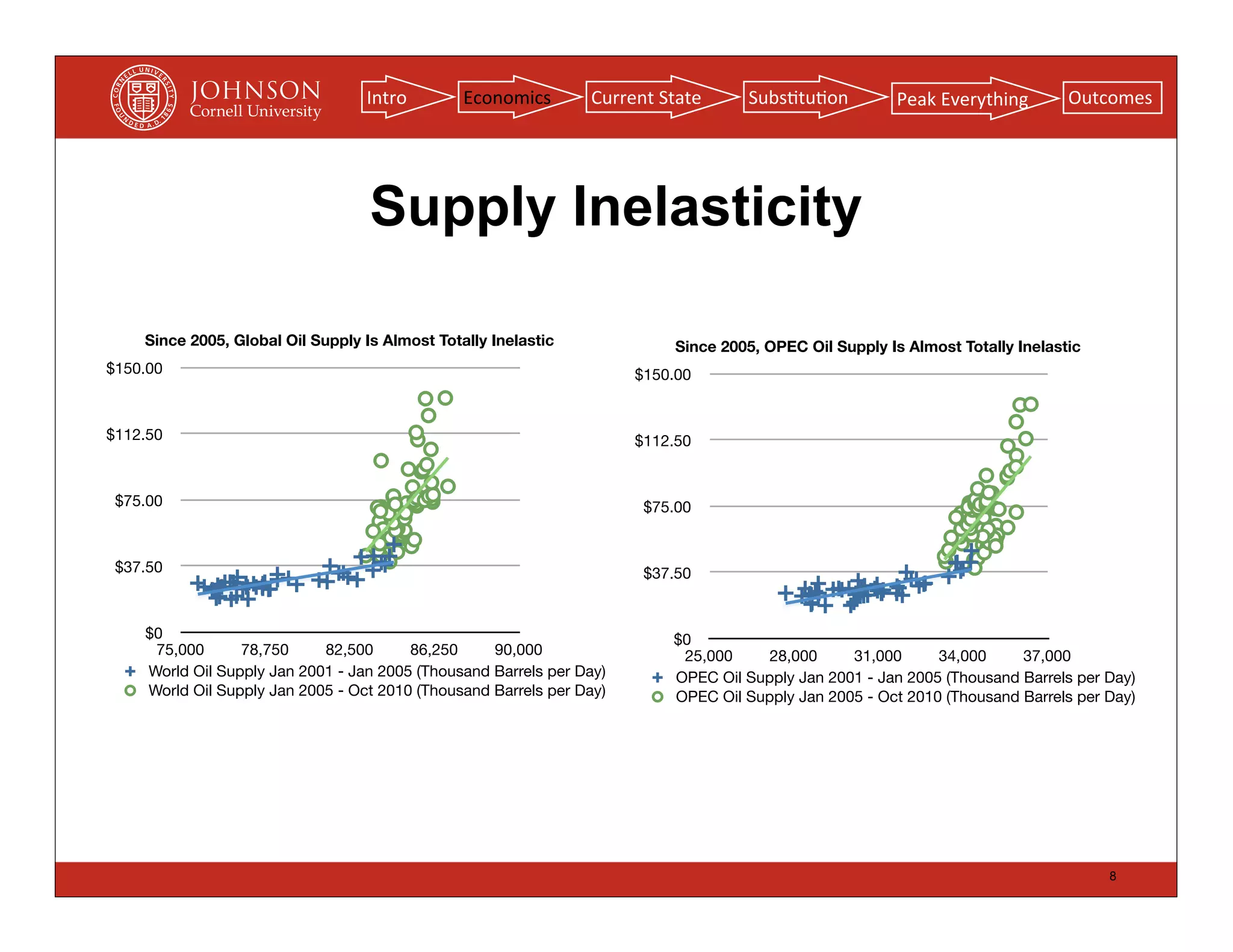

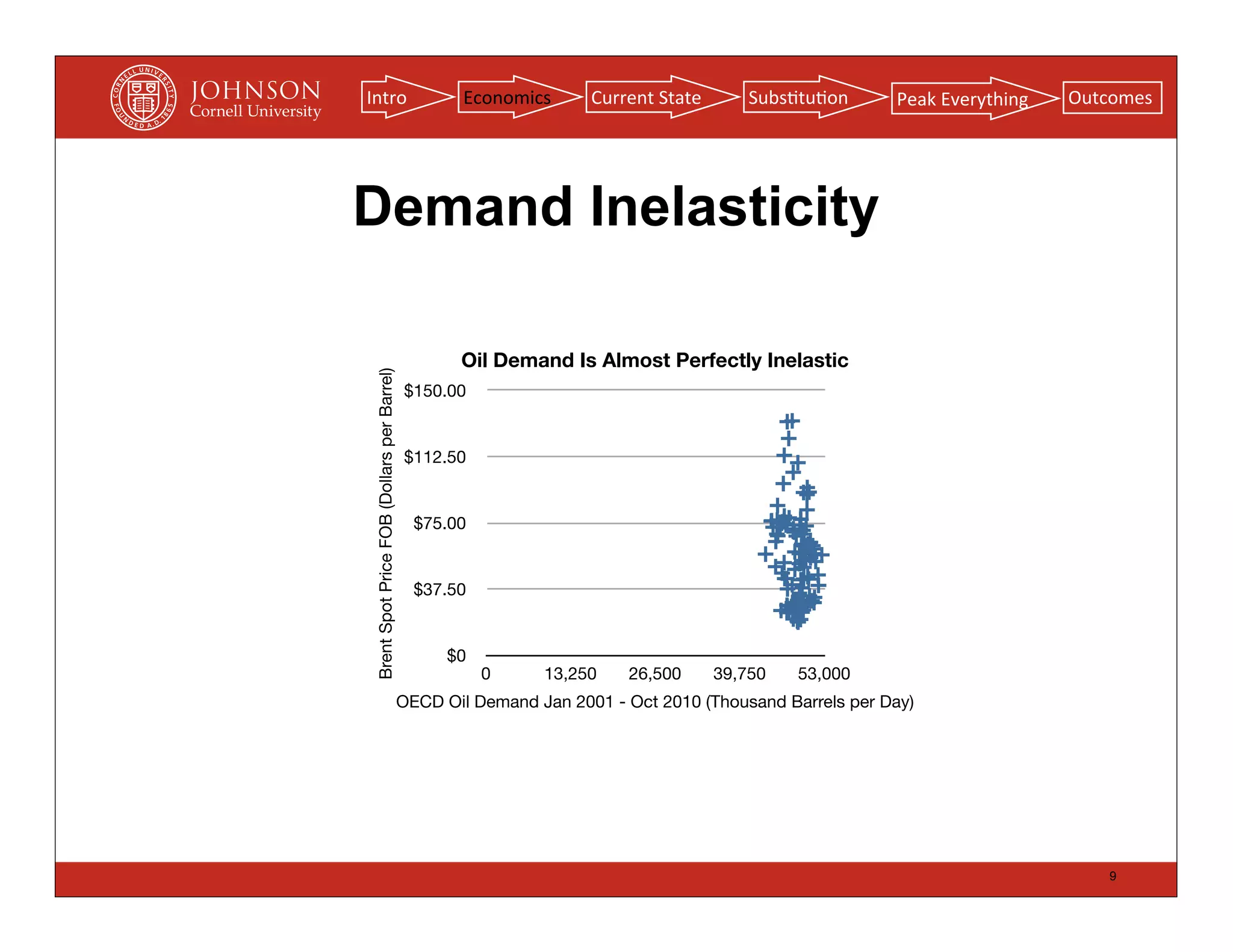

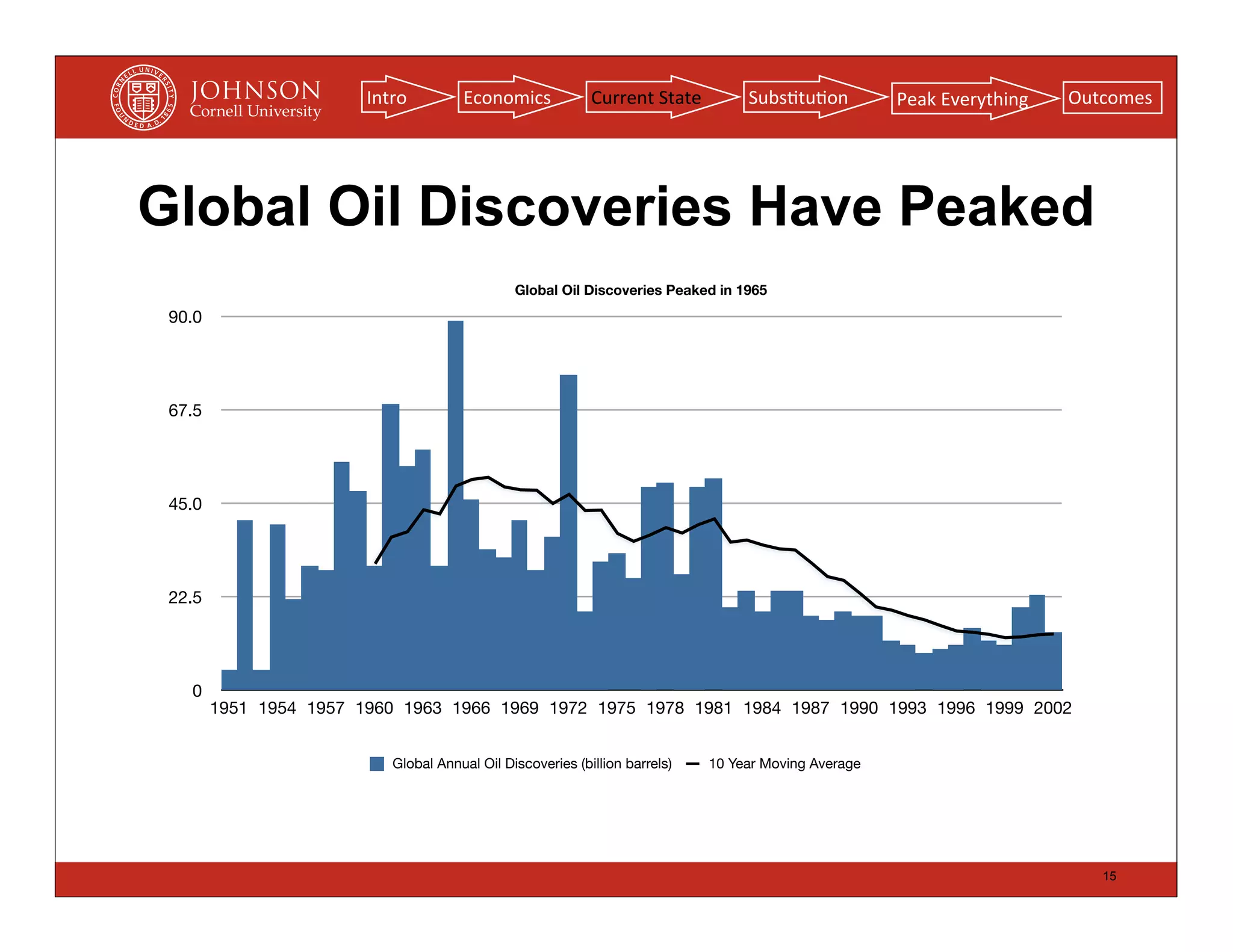

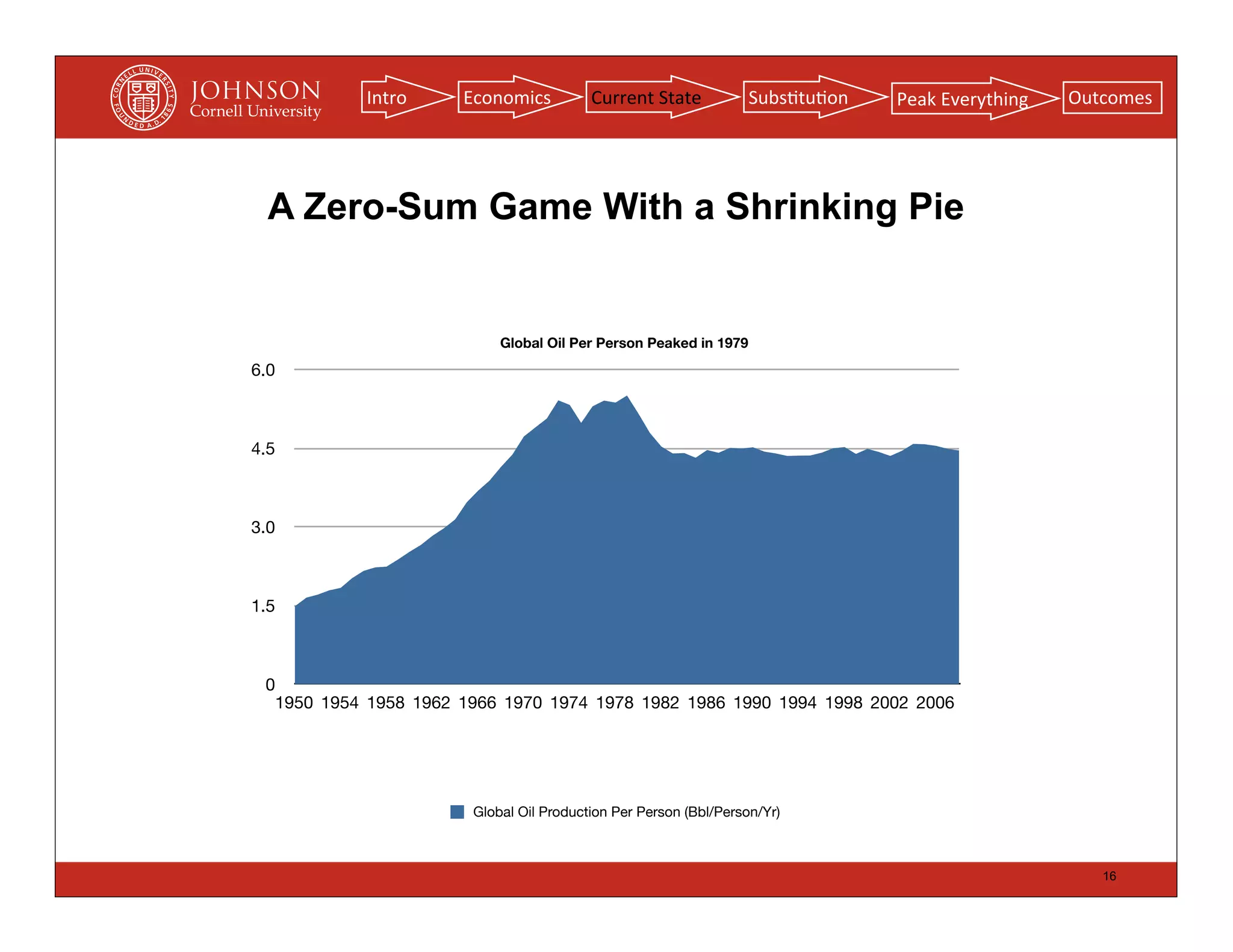

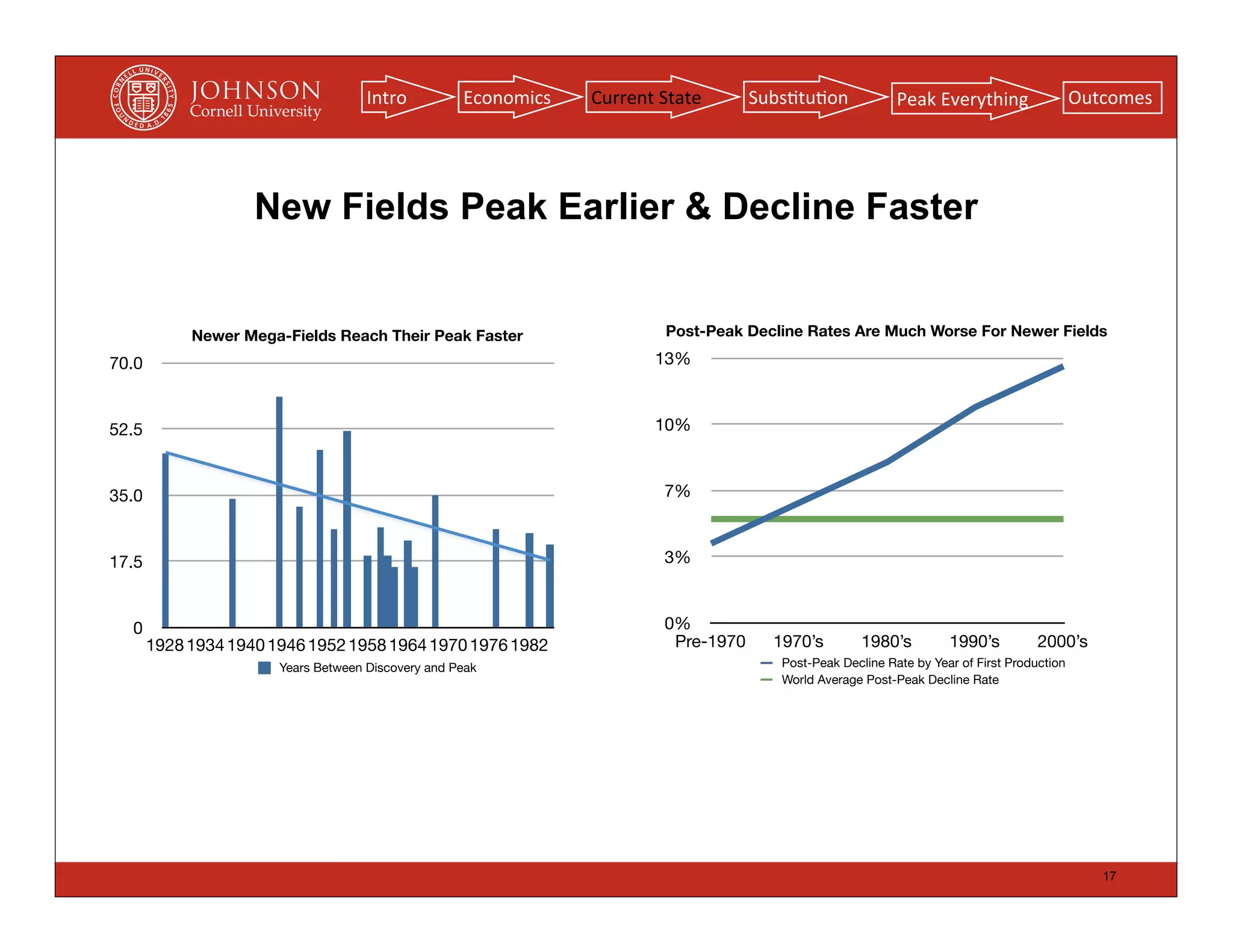

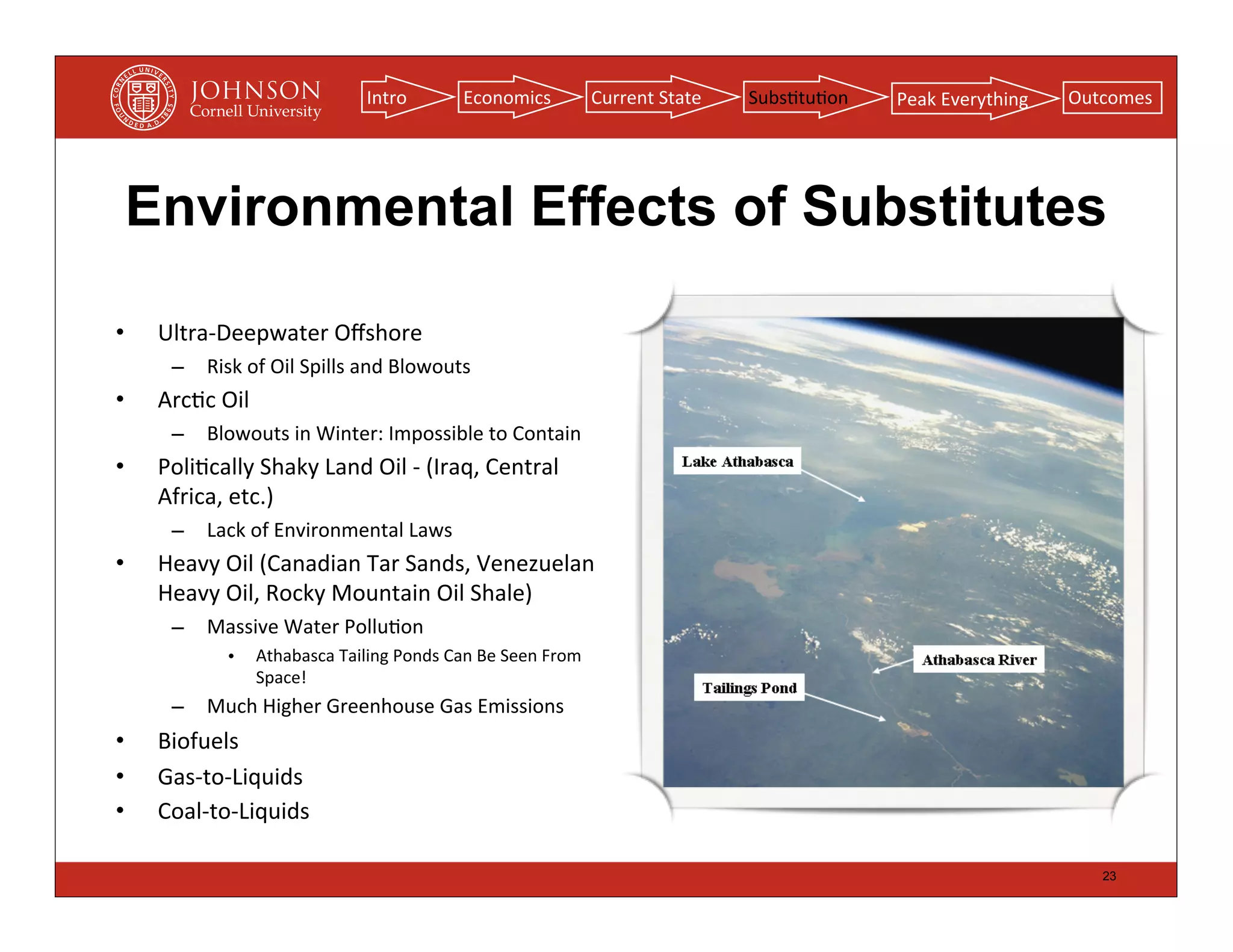

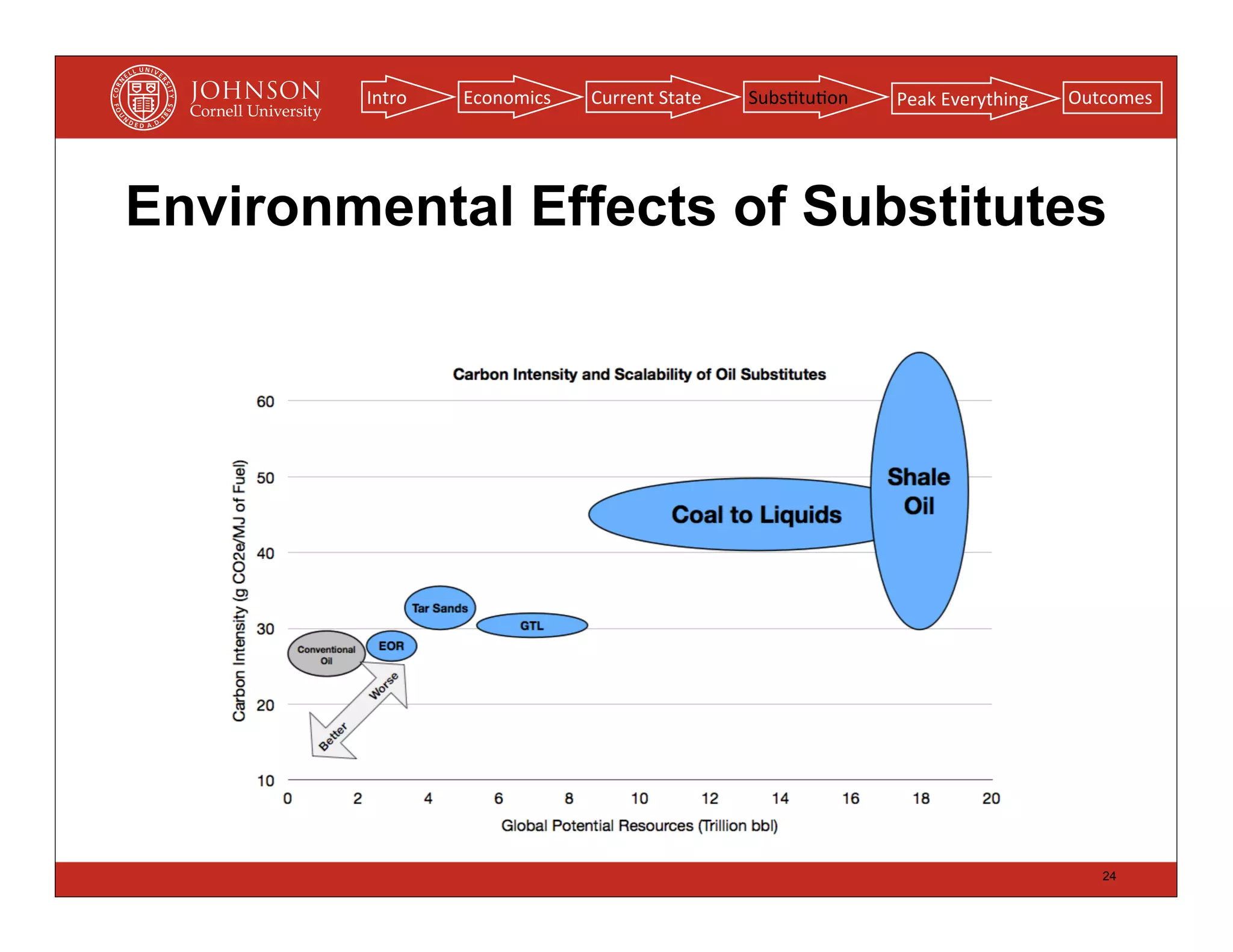

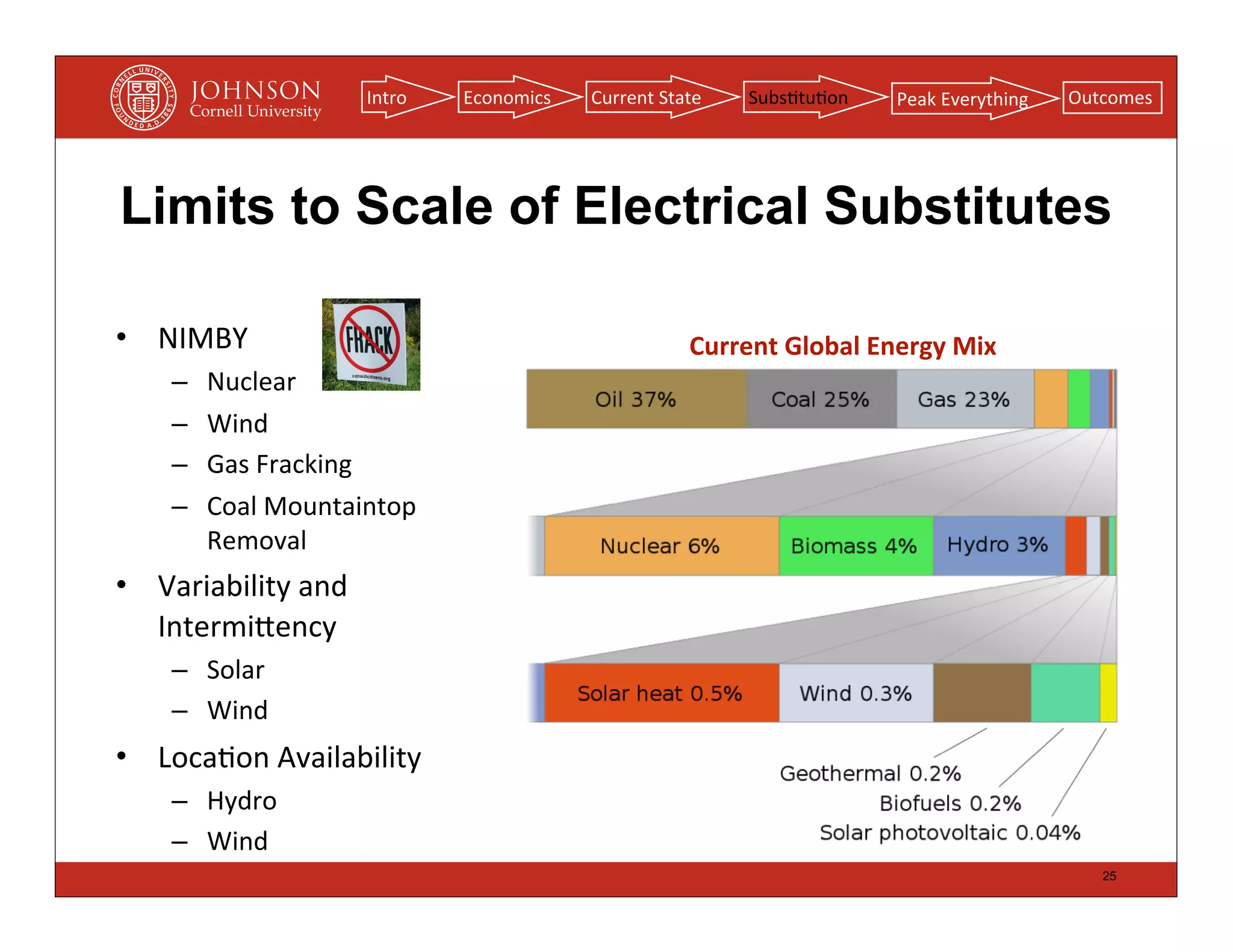

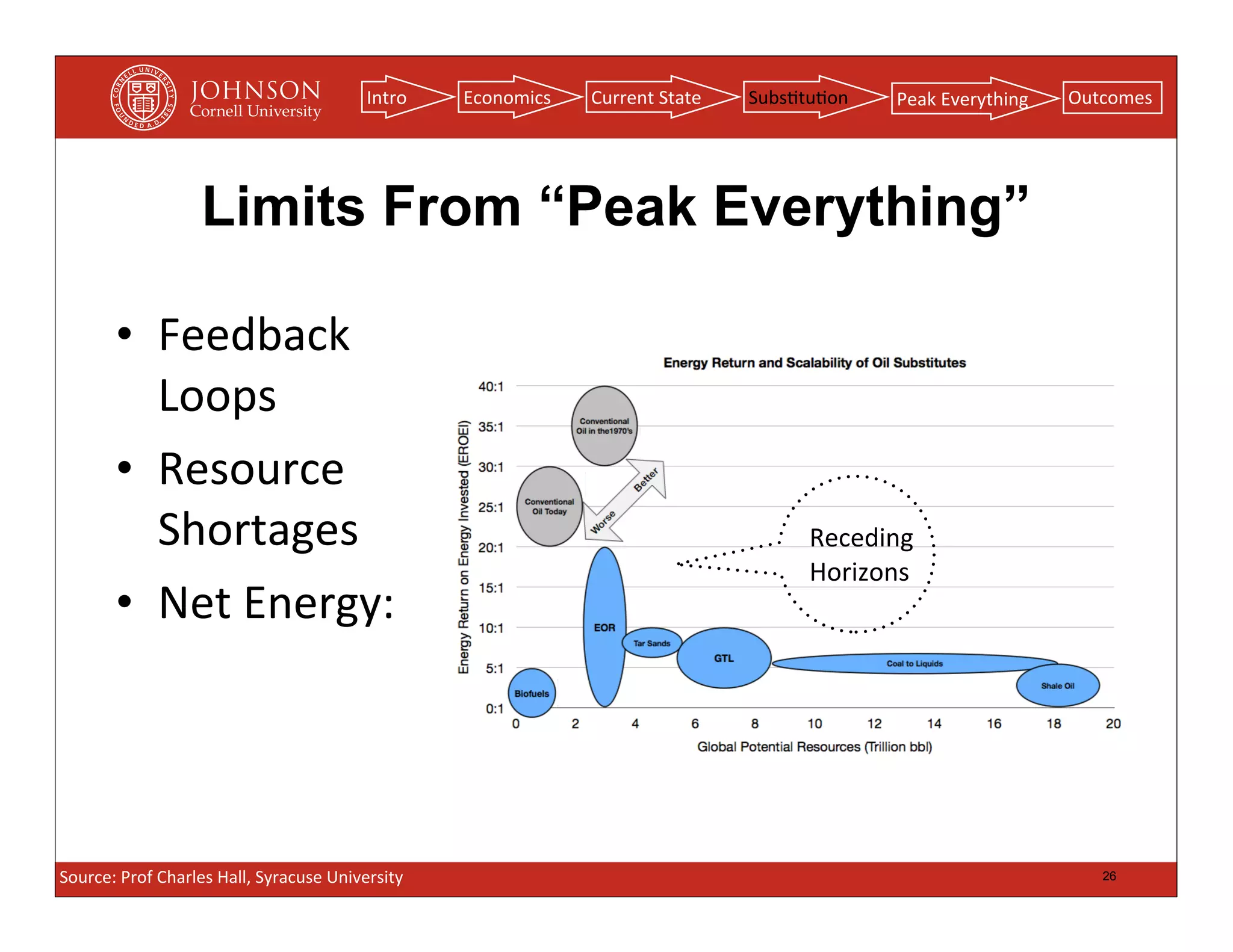

The document outlines the concept of peak oil, which denotes the maximum rate of global oil production, and discusses the inelasticity of both supply and demand in the oil market since 2005. It details the current state of global oil and energy consumption, highlights various countries that have experienced peak oil, and addresses the environmental and engineering challenges of alternative energy sources. Additionally, it touches on the broader implications of 'peak everything,' including other natural resources such as coal, gas, and metals.

![Intro Economics Current

State Subs(tu(on Peak

Everything Outcomes

Peak Gas

Countries That Have Reached Peak Gas

US Gas Peaked in 1974 but Decline Has Been Halted by Fracking

Country Peak Peak % off from

23 Year Production Peak

(Bcf/D)

United Kingdom 2000 10.45684986 47.15%

17 Ukraine 1985 3.75452235 52.19%

Romania 1982 3.57715492 70.43%

Germany 1979 1.96117317 47.57%

12 Italy 1994 1.77870648 58.60%

Denmark 2005 1.0107839 21.77%

Poland 1978 0.64114656 38.04%

6

The

Fracking

Treadmill

0

1930 1939 1948 1957 1966 1975 1984 1993 2002 “regardless

of

their

produc(vity,

[shale

gas

wells]

exhibit

an

early

peak

US Natural Gas Production (Tcf) Fracking

of

produc(on

and

then

a

rapid

decline”

-‐Interna(onal

Energy

Agency

28](https://image.slidesharecdn.com/willmartin-peakoillecture-120424110922-phpapp02/75/Peak-Oil-Peak-Everything-Lecture-at-Cornell-28-2048.jpg)