Call Girls Koregaon Park Call Me 7737669865 Budget Friendly No Advance Booking

QE Index Rises 1.0% as Telecoms, Transportation Gain

1. Page 1 of 5

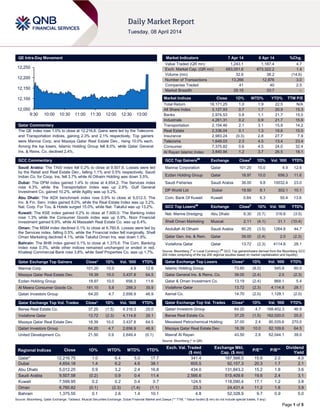

QE Intra-Day Movement

Qatar Commentary

The QE index rose 1.0% to close at 12,216.8. Gains were led by the Telecoms

and Transportation indices, gaining 2.3% and 2.1% respectively. Top gainers

were Mannai Corp. and Mazaya Qatar Real Estate Dev., rising 10.0% each.

Among the top losers, Islamic Holding Group fell 8.0%, while Qatar General

Ins. & Reins. Co. declined 2.4%.

GCC Commentary

Saudi Arabia: The TASI index fell 0.2% to close at 9,507.6. Losses were led

by the Retail and Real Estate Dev., falling 1.1% and 0.5% respectively. Saudi

Indian Co. for Coop. Ins. fell 3.7% while Al Othaim Holding was down 3.5%.

Dubai: The DFM index gained 1.4% to close at 4,654.2. The Services index

rose 4.3%, while the Transportation Index was up 2.9%. Gulf General

Investment Co. gained 10.2%, while Agility was up 5.2%.

Abu Dhabi: The ADX benchmark index rose 0.9% to close at 5,012.3. The

Inv. & Fin. Serv. index gained 8.0%, while the Real Estate Index was up 3.2%.

Nat. Corp. For Tou. & Hotels surged 15.0%, while Nat. Takaful was up 13.2%.

Kuwait: The KSE index gained 0.2% to close at 7,600.0. The Banking index

rose 1.3% while the Consumer Goods index was up 0.9%. Noor Financial

Investment gained 6.9%, while Al Massaleh Real Estate Co. was up 6.4%.

Oman: The MSM index declined 0.1% to close at 6,760.8. Losses were led by

the Services index, falling 0.5%, while the Financial index fell marginally. Shell

Oman Marketing declined 4.1%, while Takaful Oman Ins. was down 1.9%.

Bahrain: The BHB index gained 0.1% to close at 1,375.6. The Com. Banking

Index rose 0.3%, while other indices remained unchanged or ended in red.

Khaleeji Commercial Bank rose 3.8%, while Seef Properties Co. was up 1.7%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Mannai Corp. 101.20 10.0 4.9 12.6

Mazaya Qatar Real Estate Dev. 18.39 10.0 3,437.8 64.5

Ezdan Holding Group 18.97 10.0 656.3 11.6

Al Meera Consumer Goods Co. 181.10 5.8 288.3 35.9

Qatari Investors Group 64.20 4.7 2,656.9 46.9

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Barwa Real Estate Co. 37.25 (1.5) 4,316.3 25.0

Vodafone Qatar 13.72 (2.3) 4,114.8 28.1

Mazaya Qatar Real Estate Dev. 18.39 10.0 3,437.8 64.5

Qatari Investors Group 64.20 4.7 2,656.9 46.9

United Development Co. 21.50 0.9 2,649.4 (0.1)

Market Indicators 7 Apr 14 6 Apr 14 %Chg.

Value Traded (QR mn) 1,243.1 1,187.4 4.7

Exch. Market Cap. (QR mn) 683,051.6 673,322.2 1.4

Volume (mn) 32.6 38.2 (14.6)

Number of Transactions 13,266 12,876 3.0

Companies Traded 41 40 2.5

Market Breadth 25:15 33:7 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,171.25 1.0 1.9 22.5 N/A

All Share Index 3,127.93 0.7 1.7 20.9 15.3

Banks 2,974.53 0.8 1.1 21.7 15.0

Industrials 4,261.31 0.2 0.9 21.7 15.9

Transportation 2,154.46 2.1 3.1 15.9 14.2

Real Estate 2,336.04 0.1 1.3 19.6 15.0

Insurance 2,983.24 (0.3) 2.8 27.7 7.9

Telecoms 1,649.03 2.3 4.5 13.4 23.4

Consumer 7,375.82 0.6 4.5 24.0 32.4

Al Rayan Islamic Index 3,840.94 1.2 3.7 26.5 18.1

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Mannai Corporation Qatar 101.20 10.0 4.9 12.6

Ezdan Holding Group Qatar 18.97 10.0 656.3 11.6

Saudi Fisheries Saudi Arabia 38.00 9.8 10032.4 23.0

DP World Ltd Dubai 19.50 8.1 302.1 10.1

Com. Bank Of Kuwait Kuwait 0.84 6.3 50.4 13.6

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Nat. Marine Dredging Abu Dhabi 8.30 (5.7) 316.8 (3.5)

Shell Oman Marketing Muscat 2.11 (4.1) 31.1 (10.4)

Abdullah Al Othaim Saudi Arabia 90.25 (3.5) 1264.8 44.7

Qatar Gen. Ins. & Rein. Qatar 39.00 (2.4) 2.0 (2.3)

Vodafone Qatar Qatar 13.72 (2.3) 4114.8 28.1

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Islamic Holding Group 73.60 (8.0) 545.9 60.0

Qatar General Ins. & Reins. Co. 39.00 (2.4) 2.0 (2.3)

Qatar & Oman Investment Co. 13.19 (2.4) 868.1 5.4

Vodafone Qatar 13.72 (2.3) 4,114.8 28.1

Aamal Co. 14.70 (2.0) 1,129.1 (2.0)

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Qatari Investors Group 64.20 4.7 168,402.3 46.9

Barwa Real Estate Co. 37.25 (1.5) 162,020.0 25.0

Mesaieed Petrochemical Holding 37.00 2.4 90,535.6 270.0

Mazaya Qatar Real Estate Dev. 18.39 10.0 62,109.6 64.5

Masraf Al Rayan 43.50 2.6 62,044.1 39.0

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,216.75 1.0 6.4 5.0 17.7 341.4 187,566.0 15.6 2.0 4.0

Dubai 4,654.18 1.4 6.2 4.6 38.1 605.5 92,157.3 20.3 1.7 2.1

Abu Dhabi 5,012.25 0.9 3.2 2.4 16.8 434.0 131,843.2 15.2 1.8 3.6

Saudi Arabia 9,507.58 (0.2) 0.9 0.4 11.4 2,566.6 515,409.6 19.6 2.4 3.1

Kuwait 7,599.95 0.2 0.2 0.4 0.7 124.5 118,090.4 17.1 1.2 3.8

Oman 6,760.82 (0.1) (2.3) (1.4) (1.1) 23.3 24,431.4 11.2 1.6 3.9

Bahrain 1,375.55 0.1 2.6 1.4 10.1 4.8 52,328.9 9.7 0.9 5.0

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,050

12,100

12,150

12,200

12,250

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 5

Qatar Market Commentary

The QE index rose 1.0% to close at 12,216.8. The Telecoms and

Transportation indices led the gains. The index rose on the back

of buying support from non-Qatari shareholders despite selling

pressure from Qatari shareholders.

Mannai Corp. and Mazaya Qatar Real Estate Dev. were the top

gainers, rising 10.0% each. Among the top losers, Islamic

Holding Group fell 8.0%, while Qatar General Ins. & Reins. Co.

declined 2.4%.

Volume of shares traded on Monday fell by 14.6% to 32.6mn

from 38.2mn on Sunday. However, as compared to the 30-day

moving average of 17.1mn, volume for the day was 90.6%

higher. Barwa Real Estate Co. and Vodafone Qatar were the

most active stocks, contributing 13.2% and 12.6% to the total

volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings, Earnings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Qatar Islamic Bank CI Qatar

FSR/LT FCR/ ST

FCR/SR

A/A/A2/2 A/A/A2/2 – Stable

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC –

Local Currency)

Earnings Releases

Company Market Currency

Revenue

(mn)FY2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

United Electronics Co.

(Extra)

Saudi Arabia SR – – 30.6 13.9% 29.3 11.6%

Banque Saudi Fransi (BSF) Saudi Arabia SR – – 1,401.0 16.3% 856.0 25.1%

National Industries Group

Holding (NIG) *

Dubai Kuwait 109.6 3.0% – – 10.2 -21.6%

Financial Services Company

(FSC)

Oman OMR 0.3 25.1% – – 0.2 -12.8%

Source: Company data, DFM, ADX, MSM (* FY2013 results)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

04/07 EU Sentix Behavioral Indi. Sentix Investor Confidence April 14.1 13.9 13.9

04/07 Germany Deutsche Bundesbank Industrial Production SA MoM February 0.40% 0.30% 0.70%

04/07 Germany Bundesministerium Industrial Production WDA YoY February 4.80% 4.70% 4.90%

04/07 UK Lloyds Bank Lloyds Employment Confidence March -2.0 – -2.0

04/07 Spain INE Industrial Output NSA YoY February 3.10% – -0.10%

04/07 Spain INE Industrial Output SA YoY February 2.80% 1.70% 1.10%

04/07 Italy ISTAT Deficit to GDP YTD 4Q2013 2.80% – 3.40%

04/07 Japan Ministry of Finance Official Reserve Assets March $1279.3B – $1288.2B

04/07 Japan ESRI Leading Index CI February 108.5 108.8 113.1

04/07 Japan ESRI Coincident Index February 113.4 113.4 115.2

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 71.50% 77.82% (78,651,607.04)

Non-Qatari 28.50% 22.18% 78,651,607.04

3. Page 3 of 5

News

Qatar

Fitch: Qatar’s non-oil growth to pick up in 2014 – According

to Fitch Ratings, Qatar‟s non-oil economic growth is forecast to

pick up in 2014. The rating agency added that Qatar‟s high

government capital spending and population growth should

sustain double-digit non-hydrocarbon growth. The country‟s

planned huge project spending brings management challenges

and overcapacity risks. However, benign external environment is

keeping its inflation under control despite rising rents. Fitch said

the average sovereign ratings of energy exporters and importers

in the Middle East & North Africa region (MENA) have further

diverged in 2014. Credit fundamentals across all energy

exporters are expected to remain strong, driven by triple digit oil

prices. Fitch forecasts that Brent crude will average $105 per

barrel in 2014 and $100 per barrel in 2015. As a result, all

energy exporters are expected to record external surpluses and

all (except Bahrain – „BBB‟) are forecast to post fiscal surpluses

in 2014 and 2015. Fitch assumes that economic performance

would improve in most energy importers as well in 2014 due to

greater external financial support, a recovery in the Eurozone

and improved political stability in some cases. We note QNB

Group expects Qatar‟s real GDP to grow by 6.8% in 2014.

(Peninsula Qatar)

DHBK to inject $25mn to expand in India – Doha Bank

(DHBK) will initially invest $25mn into its India operations and is

set to invest heavily into trade finance, corporate banking and

treasury services. DHBK‟s CEO R Seetharaman said the lender

would initially operate as a branch for which it got a license.

After opening its first branch in Mumbai, the bank will further

expand into South India, probably in the state of Kerala to start

with, where most of the expatriates from the Gulf are stationed.

In addition, the lender would like to be present in cities with

trade links with GCC countries such as the states of Tamil Nadu,

Gujarat and others. DHBK has an exposure of around $1bn in

India and expects to take it to around $5bn over the next two to

three years. (Bloomberg)

QCFS to disclose 1Q2014 results on April 20 – Qatar Cinema

& Film Distribution Company (QCFS) has announced its intent

to disclose 1Q2014 financial results on April 20, 2014. (QE)

AHCS’ AGM approves agenda, to disclose 1Q2014 results

on April 29 – Aamal Company‟s (AHCS) AGM has approved

the recommendations from the board of directors regarding

profit and balance sheet. Meanwhile, AHCS announced that it

will disclose its 1Q2014 financial results on April 29, 2014. (QE)

KCBK to disclose 1Q2014 financials on April 22 – Al Khalij

Commercial Bank (KCBK) will disclose its 1Q2014 financial

results on April 22, 2014. (QE)

QISI to disclose 1Q2014 results on April 21 – Qatar Islamic

Insurance Company (QISI) has announced its intent to disclose

1Q2014 financial results on April 21, 2014. (QE)

QE suspends trading in BRES’ shares on April 8 – The Qatar

Exchange (QE) has announced a trading suspension of Barwa

Real Estate Company‟s (BRES) shares on April 8, 2014 due to

the company‟s AGM being held on that day. (QE)

International

Fed: US consumer credit rises boosted by student loans –

Consumer credit in the US rose more than expected in February

2014, likely reflecting a surge in demand for student and

automobile loans. The Federal Reserve said that the total

consumer credit increased by $16.49bn to $3.13tn. January's

consumer credit figure was revised to show a $13.80bn rise

instead of $13.70bn gain. Economists polled by Reuters had

expected consumer credit to rise by $14.09bn in February.

Revolving credit, which mostly measures credit-card use,

tumbled by $2.42bn after January's $241mn drop. It was the

second straight month of declines. Non-revolving credit, which

includes automotive loans as well as student loans made by the

government, surged $18.91bn in February. That was the biggest

gain in a year and followed a $14.04bn increase in January.

(Reuters)

UK pay growth accelerates to fastest in seven years – Pay

growth in the UK accelerated at the fastest pace in almost seven

years by the end of the first quarter as companies reported

stronger overseas demand. KPMG and the Recruitment &

Employment Confederation said an index of wage growth for

full-time employees rose to 62.2 in March 2014, the highest

since July 2007, from 61.7 in February. Separately, the British

Chambers of Commerce said measures of export sales and

employment intentions by manufacturers and services

companies increased in the first quarter. The strengthening of

pay growth coupled with cooling inflation may support consumer

spending, the main driver of the economy in 2013. Both the UK

government and the Bank of England are counting on a pickup

in exports and investment to keep up the recovery momentum.

(Bloomberg)

Bundesbank: France's budget policies 'test case' for

Eurozone fiscal rules – The President of the German central

bank warned that the credibility of the Eurozone's budgetary

rules was at stake and that France's suggestion that the bloc's

budget deficit targets be weakened are a "test case" for the

rules. Bundesbank‟s President Jens Weidmann, who is also a

member of the European Central Bank's board, stated that it is

vital to stick to fiscal rules, since the credibility of these rules is

at stake. A currency union needs its members to aim for

stability. Part of that is having an orderly budget and part of that

is sticking to agreements, added Weidmann. Earlier, France's

new Finance Minister Michel Sapin had said the country would

seek a review of its deadline for meeting the European Union's

budget deficit ceiling of 3%. (Reuters)

Japan’s current account rebounds to first surplus in 5

months – Japan‟s current account rebounded into surplus in

February from a record deficit the previous month as income

from overseas investments outweighed deficits in trade and

services. The Ministry of Finance reported that the 613bn yen

($5.9bn) surplus was the first in five months. The median

forecast in a Bloomberg News survey was for an excess of

618.1bn Yen. Japanese officials are assessing the strength of

the economy after a sales-tax increase on April 1 that is

projected to trigger a contraction this quarter. The Bank of Japan

is forecast to refrain from adding to its unprecedented monetary

easing at its upcoming meeting, waiting to see the extent of the

tax rise‟s blow to consumption. (Bloomberg)

Regional

CDS: Saudi construction trade to grow 35% – The Saudi

construction market is set to grow at a rate of 35% over the next

three years. The total value of projects planned is estimated at

$732bn. Construction projects worth a total of $42bn were

awarded in 2013 in the Kingdom as compared to $17bn in 2012.

According to the Central Department of Statistics (CDS), Saudi‟s

GDP grew 3.19% in 3Q2013 at current prices as compared to a

2.7% rise during 2Q2013. The country‟s GDP value rose to

SR696.7bn in 3Q2013 from SR675.19bn in 3Q2012. In the

public sector, the GDP fell by 18.52% to SR102.6bn in current

prices as compared to the same period in 2012. The private

4. Page 4 of 5

sector achieved a growth of 6.53% in current prices in 3Q2013

to reach SR244.08bn as compared to SR229.13 billion in

3Q2012. The construction & building sector and downstream

industries showed high growth of 9.76% and 7.87% respectively.

(GulfBase.com)

Tadawul deposits ASLAK’s bonus shares – The Saudi Stock

Exchange (Tadawul) announced the addition of the United Wire

Factories Company‟s (ASLAK) bonus shares into its investors‟

portfolios. Earlier, ASLAK‟s EGM had approved an increase in

the company‟s capital via bonus shares. The fluctuation limits for

the company‟s shares on April 7, 2014 will be based on a stock

price of SR37.3. (Tadawul)

Othaim’s EGM approves 30% dividend distribution, bonus

shares deposited by Tadawul – Abdullah Al-Othaim Markets

Company‟s (Othaim) EGM has approved the board‟s

recommendation for the distribution of 30% cash dividend (SR3

per share) amounting to SR67.5mn for 2013. Further, the EGM

approved an increase in the company‟s capital from SR225mn

to SR450mn by issuing one bonus share for every share owned.

Consequently, company‟s outstanding shares will increase from

22.5mn to 45mn. The bonus shares‟ eligibility is limited to those

shareholders who are registered at the close of trading on the

day of the EGM. Meanwhile, the Saudi Stock Exchange

announced the addition of Abdullah Al-Othaim Markets

Company‟s (Othaim) bonus shares into its investors‟ portfolios.

The fluctuation limits for the company‟s shares on April 7, 2014

will be based on a stock price of SR93.5. (Tadawul)

Jarir Marketing declares 58% dividend – Jarir Marketing

Company‟s AGM has approved the distribution of 58% total

cash dividend (SR5.8 per share) for 2013. (Tadawul)

Marka to launch IPO in Dubai market – Marka, a retail and

food company in the UAE, will launch its IPO on Dubai's main

stock market. The 12-day offer of 275mn shares is priced at

AED1 each, representing 55% of the company's capital. The

company has received final regulatory approval and will start

listing on the Dubai Financial Market on April 13. The rest of its

capital was subscribed last month by 151 founders including

wealthy UAE businessmen. (Reuters)

Dubai reaches in-principle deal on bourse merger with Abu

Dhabi – A top Dubai economic policymaker said that an

agreement has been reached in principle to merge the two main

stock markets in the UAE – the Dubai Financial Market and the

Abu Dhabi Securities Exchange. Sheikh Ahmed bin Saeed al-

Maktoum, head of Dubai‟s Supreme Fiscal Council said the

agreement has been reached between the two Emirates, but it is

not yet finalized. (Gulf-Times.com)

DGCX to launch agricultural contracts in 1Q2015 – The

Dubai Gold & Commodities Exchange (DGCX) is planning to

launch contracts in agricultural commodities in 1Q2015.

(Reuters)

Etisalat declares dividends for 2H2013 – Emirates

Telecommunications Corporation‟s (Etisalat) AGM has approved

the board of directors‟ recommendation for the distribution of

dividends for 2H2013 at the rate of 35 fils per share. This brings

the total dividend distributed for 2013 to 70 fils per share. (ADX)

Aldar plans to float IPO for property unit – Abu Dhabi-based

Aldar Properties is planning to float its property management

unit Khidmah through an IPO of shares in coming years. Aldar is

the majority shareholder in Khidmah holding a 60% stake.

(GulfBase.com)

RAKBANK seeks to double foreign ownership limit to 40% –

Shareholders of National Bank of Ras al-Khaimah (RAKBANK)

will meet on May 1 to decide whether to allow foreigners to hold

up to 40% of its shares. The bank, which is listed in Abu Dhabi,

currently has a 20% cap on foreign ownership. According to

Thomson Reuters data, Foreigners currently own 19.3% of the

bank's shares. (Reuters)

Kuwait to invite bids for new refinery; oil capacity rises to

3.3mn bpd – Kuwait Petroleum Corporation‟s (KPC) CEO Nizar

Al-Adsani said Kuwait will invite bids for a new multi-billion dollar

oil refinery next month as part of its drive to modernize the oil

sector. Al-Adsani said another project costing $1bn for the

development of heavy oil from northern oilfields will be awarded

later in April 2014. The cost of the new 615,000 barrels per day

Al Zour refinery is estimated to be around $15bn. Contracts for

another $12bn project to upgrade existing refineries will be

signed next week with three consortia led by British, US and

Japanese companies. Meanwhile, Al-Adsani said Kuwait has

increased its oil production capacity to 3.3mn barrels per day

(bpd) and is hoping to reach 3.5mn bpd by 2015. Kuwaiti

officials had previously said that the country‟s capacity was

around 3.1-3.2mn bpd. Al-Adsani said Kuwait still hopes to

reach a capacity of 4 million bpd in 2020, despite slow progress

in developing new projects. (Bloomberg)

Americana’s chairman says unaware of potential stake sale

– Kuwait Food Company‟s (Americana) chairman said,

Americana is not aware of any potential stake sale by its

majority shareholder. According to sources, Kuwait's billionaire

al-Kharafi family was looking to sell Americana and had hired

bankers to explore a deal. Americana Chairman Marzouk al-

Kharafi stated that they don't know anything about this subject.

He further added that this subject is for the shareholders. The

sources further added that there was no formal process

underway, but the family was working with investment bank

Rothschild to approach potential buyers including private equity

groups and sovereign wealth funds in the region to explore their

interest in the $3.6bn group. (Reuters)

Moody's places GIC ratings on review for upgrade –

Moody's Investors Service has placed the (P) Baa2 rating on the

senior unsecured MTN program of the Gulf Investment

Corporation (GIC) on review for upgrade. In a related action, the

ratings associated with GIC Funding Ltd - a fully-owned special

purpose vehicle of GIC - were also placed on review for

upgrade. (Moody's)

OGC signs MoU for setting up LPG plant in Salalah – The

Oman Gas Company (OGC) has signed a MoU for setting up a

world class Liquefied Petroleum Gas (LPG) processing plant at

Salalah Free Zone (SFZ) and for establishing related storage

and export facilities at the Port of Salalah. The state-of-the-art

plant will allow for high recovery of propane, butane and

condensates from natural gas flowing through OGC‟s southern

gas grid. Around 1,000 people will be engaged in the

construction of the complex, which will provide employment to

around 170 highly skilled technical staff. While the free zone will

house the LPG extraction plant, the storage facilities, as well as

an export jetty, are proposed to be constructed at the adjoining

port. (GulfBase.com)

Bahrain’s 4Q GDP growth slows to 5.4% – According to the

data from official statistics, growth in Bahrain's inflation-adjusted

GDP has slowed to 5.4% YoY in 4Q2013 from a revised 5.7% in

3Q2013. However, GDP rose 0.7% from the previous quarter.

The mining sector led the growth in 4Q2013, expanding 14.6%

from a year earlier. Most other major sectors grew much more

slowly, with construction and financial services growing at 1.5%

each. (GulfBase.com)

5. Contacts

Saugata Sarkar Keith Whitney Sahbi Kasraoui

Head of Research Head of Sales Manager - HNWI

Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg (* Market closed on April 7, 2014) Source: Bloomberg (* Market closed on April 7, 2014)

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

(0.2%)

1.0%

0.2%

0.1%

(0.1%)

0.9%

1.4%

(0.5%)

0.0%

0.5%

1.0%

1.5%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,297.35 (0.5) (0.5) 7.6 DJ Industrial 16,245.87 (1.0) (1.0) (2.0)

Silver/Ounce 19.88 (0.4) (0.4) 2.1 S&P 500 1,845.04 (1.1) (1.1) (0.2)

Crude Oil (Brent)/Barrel (FM

Future)

105.82 (0.8) (0.8) (4.5) NASDAQ 100 4,079.75 (1.2) (1.2) (2.3)

Natural Gas (Henry

Hub)/MMBtu

4.55 1.7 1.7 4.8 STOXX 600 334.96 (1.2) (1.2) 2.0

LPG Propane (Arab Gulf)/Ton* 108.00 0.0 0.0 (14.6) DAX 9,510.85 (1.9) (1.9) (0.4)

LPG Butane (Arab Gulf)/Ton 121.00 (0.6) (0.6) (10.9) FTSE 100 6,622.84 (1.1) (1.1) (1.9)

Euro 1.37 0.3 0.3 (0.0) CAC 40 4,436.08 (1.1) (1.1) 3.3

Yen 103.10 (0.2) (0.2) (2.1) Nikkei 14,808.85 (1.7) (1.7) (9.1)

GBP 1.66 0.2 0.2 0.3 MSCI EM 1,004.15 0.2 0.2 0.1

CHF 1.13 0.5 0.5 0.6 SHANGHAI SE Composite* 2,058.83 0.0 0.0 (2.7)

AUD 0.93 (0.2) (0.2) 4.0 HANG SENG 22,377.15 (0.6) (0.6) (4.0)

USD Index 80.23 (0.2) (0.2) 0.2 BSE SENSEX 22,343.45 (0.1) (0.1) 5.5

RUB 35.64 1.0 1.0 8.4 Bovespa 52,155.28 2.1 2.1 1.3

BRL 0.45 1.1 1.1 6.6 RTS 1,193.78 (3.3) (3.3) (17.3)

175.5

151.4

137.3