(Vedika) Low Rate Call Girls in Pune Call Now 8250077686 Pune Escorts 24x7

3 December Daily Market Report

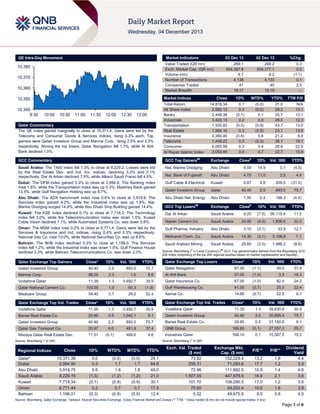

1. QE Intra-Day Movement

Market Indicators

10,380

10,370

10,360

02 Dec 13

%Chg.

269.1

554,367.8

9.1

4,138

41

18:17

268.2

554,177.1

9.2

4,133

40

15:19

0.3

0.0

(1.1)

0.1

2.5

–

Market Indices

10,350

10,340

9:30

03 Dec 13

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index gained marginally to close at 10,371.4. Gains were led by the

Telecoms and Consumer Goods & Services indices, rising 0.3% each. Top

gainers were Qatari Investors Group and Mannai Corp., rising 2.5% and 2.3%

respectively. Among the top losers, Qatar Navigation fell 1.1%, while Al Ahli

Bank declined 1.0%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

14,818.34

2,582.12

2,449.38

3,403.13

1,925.82

1,984.16

2,380.40

1,449.22

6,005.99

3,053.44

0.1

0.0

(0.1)

0.2

(0.5)

0.3

(0.6)

0.3

0.3

0.4

(0.0)

(0.0)

0.1

0.0

(0.9)

(0.5)

0.6

(0.3)

0.4

0.7

31.0

28.2

25.7

29.5

43.7

23.1

21.2

36.1

28.6

22.7

N/A

13.1

13.1

12.3

13.0

13.6

9.8

19.7

22.8

15.9

GCC Commentary

GCC Top Gainers##

Exchange

Close#

1D%

Vol. ‘000

Saudi Arabia: The TASI index fell 1.3% to close at 8,229.2. Losses were led

by the Real Estate Dev. and Ind. Inv. indices, declining 3.2% and 2.1%

respectively. Dar Al Arkan declined 7.5%, while Allianz Saudi Fransi fell 4.5%.

Nat. Marine Dredging

Abu Dhabi

9.55

14.9

0.1

(4.5)

Nat. Bank of Fujairah

Abu Dhabi

4.75

11.0

2.5

4.4

Dubai: The DFM index gained 0.3% to close at 2,994.9. The Banking index

rose 1.8%, while the Transportation index was up 0.3%. Mashreq Bank gained

13.5%, while Gulf Navigation Holding was up 8.7%.

Gulf Cable & Electrical

Kuwait

0.87

4.8

206.5

(31.0)

Qatari Investors Group

Qatar

40.40

2.5

893.0

75.7

Abu Dhabi: The ADX benchmark index rose 0.6% to close at 3,919.8. The

Services index gained 4.2%, while the Industrial index was up 1.8%. Nat.

Marine Dredging surged 14.9%, while Abu Dhabi Ship Building gained 14.4%.

Abu Dhabi Nat. Energy

Abu Dhabi

1.30

2.4

198.3

(4.4)

GCC Top Losers

Exchange

#

Kuwait: The KSE index declined 0.1% to close at 7,718.3. The Technology

index fell 3.0%, while the Telecommunication index was down 1.0%. Kuwait

Cable Vision declined 7.1%, while Automated Systems Co. was down 5.8%.

Dar Al Arkan

Saudi Arabia

9.20

(7.5)

56,115.4

11.5

Najran Cement Co.

Saudi Arabia

24.95

(4.0)

1,808.6

32.0

Oman: The MSM index rose 0.2% to close at 6,771.4. Gains were led by the

Services & Insurance and Ind. indices, rising 0.4% and 0.3% respectively.

National Gas Co. rose 10.0%, while National Securities Co. was up 8.6%.

Gulf Pharma. Industry

Abu Dhabi

3.10

(3.1)

33.9

12.7

Methanol Chem. Co.

Saudi Arabia

14.30

(3.1)

3,108.9

7.1

Saudi Arabian Mining

Saudi Arabia

29.60

(3.0)

1,488.2

(8.6)

Bahrain: The BHB index declined 0.3% to close at 1,198.0. The Services

index fell 1.2%, while the Industrial index was down 1.0%. Gulf Finance House

declined 3.3%, while Bahrain Telecommunications Co. was down 2.0%.

Qatari Investors Group

Mannai Corp.

Close*

1D%

Vol. ‘000

YTD%

40.40

Qatar Exchange Top Gainers

2.5

893.0

75.7

88.00

2.3

1.5

8.6

1D% Vol. ‘000

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Close*

1D%

Vol. ‘000

YTD%

Qatar Navigation

87.00

(1.1)

49.0

37.9

Al Ahli Bank

57.00

(1.0)

3.5

16.3

Qatar Exchange Top Losers

Medicare Group

1.3

3,492.7

35.9

Qatar Insurance Co.

67.00

(1.0)

82.4

24.2

105.00

1.0

50.3

(1.9)

Gulf Warehousing Co.

41.00

(0.7)

25.5

22.4

54.40

Qatar National Cement Co.

0.7

29.2

52.4

Aamal Co.

14.85

(0.7)

22.5

9.1

Close*

1D%

Val. ‘000

YTD%

Vodafone Qatar

11.35

1.3

39,630.8

35.9

9.1

Qatari Investors Group

40.40

2.5

35,695.4

75.7

893.0

75.7

Barwa Real Estate Co.

29.95

0.5

31,150.8

9.1

0.0

491.9

37.4

QNB Group

169.80

(0.1)

27,057.3

29.7

(0.1)

488.6

4.6

Industries Qatar

168.10

0.1

15,587.5

19.2

Close*

1D%

Vol. ‘000

YTD%

Vodafone Qatar

11.35

1.3

3,492.7

35.9

Barwa Real Estate Co.

29.95

0.5

1,042.1

Qatari Investors Group

40.40

2.5

Qatar Gas Transport Co.

20.97

Mazaya Qatar Real Estate Dev.

11.51

Qatar Exchange Top Vol. Trades

Qatar Exchange Top Val. Trades

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Close

11.35

Vodafone Qatar

Regional Indices

##

YTD%

Close

1D%

WTD%

MTD%

YTD%

10,371.39

2,994.90

3,919.75

8,229.19

7,718.34

6,771.44

1,198.01

0.0

0.3

0.6

(1.3)

(0.1)

0.2

(0.3)

(0.0)

1.7

1.8

(1.2)

(0.9)

0.7

(0.9)

(0.0)

1.7

1.8

(1.2)

(0.9)

0.7

(0.9)

24.1

84.6

49.0

21.0

30.1

17.5

12.4

Exch. Val. Traded

($ mn)

73.92

255.31

72.98

1,507.05

101.70

75.50

0.32

Exchange Mkt.

Cap. ($ mn)

152,229.4

71,293.6

111,882.5

447,978.9

109,290.5

24,252.4

49,675.9

P/E**

P/B**

13.2

17.7

10.9

16.9

17.0

10.6

8.0

1.8

1.2

1.4

2.1

1.2

1.6

0.8

Dividend

Yield

4.4

3.0

4.6

3.6

3.6

3.8

4.0

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 6

2. Qatar Market Commentary

The QE index gained marginally to close at 10,371.4. The

Telecoms and Consumer Goods & Services indices led the

gains. The index rose on the back of buying support from Qatari

shareholders despite selling pressure from non-Qatari

shareholders.

Overall Activity

Buy %*

Sell %*

Net (QR)

Qatari

67.13%

66.56%

1,518,332.63

Non-Qatari

32.88%

33.43%

(1,518,332.63)

Source: Qatar Exchange (* as a % of traded value)

Qatari Investors Group and Mannai Corp. were the top gainers,

rising 2.5% and 2.3% respectively. Among the top losers, Qatar

Navigation fell 1.1%, while Al Ahli Bank declined 1.0%.

Volume of shares traded on Tuesday declined by 1.1% to 9.1mn

from 9.2mn on Monday. Further, as compared to the 30-day

moving average of 11.2mn, volume for the day was 18.8% lower.

Vodafone Qatar and Barwa Real Estate Co. were the most

active stocks, contributing 38.4% and 11.5% to the total volume

respectively.

Ratings, Earnings and Global Economic Data

Ratings Updates

Company

Agency

Market

Doha Bank (DHBK)

Moody’s

Qatar

Doha Finance

Limited

Moody’s

Qatar

Type*

Old Rating

LT LC & FC deposit

rating/ ST LC & FC

deposit rating/ BFSR/

LT FC subordinated

debt rating/ LT FC

senior program rating/

LT FC subordinated

debt program rating

Backed FC senior

unsecured debt ratings/

Backed FC senior

unsecured debt

program ratings/

Backed FC senior

subordinated debt

program ratings

New Rating

Rating Change

Outlook

Outlook Change

A2/Prime1/D+/Baa2/(P)

A2/(P)Baa2

A2/Prime1/D+/Baa2/(P

)A2/(P)Baa2

–

Stable

–

A2/(P)A2/(P)Ba

a2

A2/(P)A2/(P)

Baa2

–

Stable

–

Source: News reports (* LT – Long Term, ST – Short Term, BFSR- Bank Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating)

Earnings Releases

Company

Market

International Petroleum

Investment Co. (IPIC)

Currency

Abu Dhabi

Revenue

(mn) 1H2013

% Change

YoY

Operating Profit

(mn) 1H2013

% Change

YoY

Net Profit (mn)

1H2013

% Change

YoY

95,700.0

-1.0%

–

–

3,200.0

6.7%

AED

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date

Market

Source

Indicator

Period

Actual

Consensus

Previous

12/03

US

Bloomberg

IBD/TIPP Economic Optimism

December

43.1

43.0

41.4

12/03

EU

Eurostat

PPI MoM

October

-0.50%

-0.20%

0.20%

12/03

EU

Eurostat

PPI YoY

October

-1.40%

-1.00%

-0.90%

12/03

UK

BRC

BRC Sales Like-For-Like YoY

November

0.60%

1.10%

0.80%

12/03

UK

Markit

PMI Construction

November

62.6

59.0

59.4

12/03

Italy

Italian Treasury

Budget Balance

November

-7.2B

–

-11.5B

12/03

China

China Fed. of Logistics

Non-manufacturing PMI

November

56.0

–

56.3

12/03

Japan

Bank of Japan

Monetary Base YoY

November

52.50%

–

45.80%

12/03

Japan

Bank of Japan

Monetary Base End of period

November

¥191.6T

–

¥189.8T

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QCB issues QR4bn T-bills – The Qatar Central Bank (QCB)

has issued three treasury bills worth QR4bn on December 3,

2013. Total bids stood at QR8.45bn for all three maturities. Yield

on 91-day T-bills declined to 1.20% from 1.28%, while yield for

182-day T-bills fell to 1.26% from 1.30% and for 273-day notes it

declined to 1.37% from 1.40%. (QCB)

Moody’s affirms DHBK’s currency deposit ratings at

A2/Prime-1 – Moody’s has affirmed Doha Bank’s (DHBK) global

foreign and local currency deposit ratings at “A2/Prime-1”.

Moody's has also affirmed DHBK’s standalone bank financial

strength rating (BFSR) at “D+”. The outlook on all these ratings

remains Stable. (Moody’s press release)

Page 2 of 6

3. Strong LNG sector, fiscal footing to boost Qatar economy

in 2014 – According to a report by the Standard Chartered Bank

(StanChart), Qatar’s 2014 economic outlook remains strong due

to factors like strengthening debt dynamics and successful

redirecting of LNG exports to Asian markets to offset market

conditions in North America and Europe. StanChart said while

the LNG-sector dynamics are likely to remain healthy and will

underpin the strong fiscal position, the country’s nonhydrocarbon economy will be the primary growth driver in 2014.

The report said the government’s commitments on infrastructure

for hosting the FIFA 2022 World Cup and its longer-term Vision

2030 objectives have resulted in a significant pick-up in

infrastructure investment in 2013 and expects to continue in

2014. Meanwhile, StanChart said inflation will be a key

challenge for Qatar next year, despite the overall rosy economic

outlook. The bank said that rents are likely to be a key inflation

driver and expects them to begin rising next year. (GulfTimes.com)

AREDC: Qatar office market to see rent drag in 2014 –

According to a report by the Al Asmakh Real Estate

Development Company (AREDC), Qatar’s office market is still in

its initial stages of growth, which may see a drag in rents in the

coming two to three quarters of 2014. The report said the

current supply of offices, especially in West Bay, C Ring Road,

and Barwa Commercial Avenue, may drag down rental rates

over the next two to three quarters. However, due to ongoing

changes in Doha city centre areas and existing business

dynamics owing to FIFA World Cup 2022, as well as lucrative

opportunities to new businesses within Qatar, the office market

will be positive in the long-term. (Gulf-Times.com)

Property deals worth QR901.76mn during November 24-28 –

The Real Estate Registration Department at the Qatar’s Ministry

of Justice said real estate transactions worth QR901.76mn were

registered during November 24-28, 2013 in Qatar. Properties

that were traded include open plots of land, two-floor villas,

annexes, and residential buildings that are located in the

municipalities of Umm Salal, Al Khor, Doha, Al Rayyan, Al

Shamal, Al Daayen and Al Wakra. (Bloomberg)

Hill obtains QR30mn PM contract from RSG – US-based Hill

International has obtained a 30-month contract worth QR35mn

from Real Estate Services Group (RSG) to provide project

management services (PM) for the design & construction of two

mixed-use tower projects in the Lusail District of Doha. It will

provide PM services for a 35-story tower that includes a five-star

hotel, restaurants, villas and apartments, and another 27-story

tower that will feature offices, retail and other commercial uses.

The total construction cost of these two towers is expected to be

QR1bn. (Bloomberg)

Hamad airport commences operations – Hamad International

Airport (HIA) has commenced operations with Qatar Airways

receiving its first cargo shipment at the new airport on December

1. This new cargo terminal has the capacity to move 5,700

shipments simultaneously and can handle 1.4mn tons of cargo

per annum by 2015. This is an increase of 75% from the

capacity of current airport. (Bloomberg)

QA plans 4 weekly flights to Istanbul from May 2014 – Qatar

Airways (QA) is planning to operate four weekly passenger

flights to Istanbul’s Sabiha Gökçen Airport from May 2014. QA

currently operates 10 weekly flights to Istanbul’s Ataturk Airport

and four weekly flights to Ankara. So, this will be QA’s third

destination in Turkey. (Bloomberg)

International

Japan plans 18.6tn yen economic package to support

growth – According to sources, Japan is planning an 18.6tn yen

package to counter the impact of a sales-tax bump in April, as

Prime Minister Shinzo Abe tries to sustain a recovery in the

country’s economy. The steps will include 5.5tn yen in fiscal

spending and the government will use tax revenue to fund the

package, forgoing new bond sales. (Bloomberg)

Australia’s economy expands slower than forecast –

Australia’s economy expanded slower than economists forecast

last quarter after households boosted savings, suggesting the

central bank may need to do more to spur spending as a mining

investment boom wanes. Australian government data showed,

third-quarter GDP advanced 0.6% from the prior three months,

when it rose a revised 0.7% as compared to economists’

forecast for a 0.7% gain. Growth was 2.3% from a year earlier the third-straight quarter below 2.5% and less than economists’

estimates for a 2.6% expansion. (Bloomberg)

ECB to hold back, new projections key to next move – The

European Central Bank is likely to hold off any fresh policy

action tomorrow, but new forecasts will be in focus for signs of

prolonged price weakness that could lead it to act again next

year. After surprising the markets last month with a cut in rates

to a new record low, ECB President Mario Draghi said the

Eurozone may experience a prolonged period of low inflation

and that the ECB was ready to consider using all available

policy tools. He said this month’s ECB staff projections would

give a fuller picture of how long that prolonged period would last.

(Gulf-Times.com)

Russia slashes 2013 growth forecast again – Russia has

once again sharply lowered its growth forecast amid fresh

indications that the nation would remain one of the emerging

world’s worst performers for years to come. Russia’s Economy

Minister Alexei Ulyukayev said factors ranging from

disappointing investments levels to slowing consumer demand

and industrial production meant that Russia would achieve 1.4%

growth this year, instead of 1.8% forecasted just weeks ago.

(Gulf-Times.com)

OECD countries’ inflation cools in October – The

Organization for Economic Cooperation & Development (OECD)

said inflation among advanced countries slowed marginally to

1.3% in October from 1.5% in September. OECD said CPI has

dropped from a yearly peak of 2% in July as energy prices fell

and the increase in food prices slowed in October. Concerns

about a possible destructive deflationary spiral have pushed the

European Central Bank into cutting its main interest rate by a

quarter of a percentage point to a record low of 0.25%. The

Eurozone’s inflation fell to 0.7% in October, below the 1.1%

registered by Japan. (Gulf-Times.com)

Regional

IMF: Riyadh must boost private sector to meet surge in

jobseekers – The International Monetary Fund’s Deputy

Managing Director Min Zhu said Saudi Arabia needs to

strengthen its private sector to satisfy demand for jobs by its

young population and reduce its dependence on oil exports. The

Kingdom has realized that high unemployment among young

people is its biggest challenge in coming decades, but it has

struggled to turn private-sector growth into jobs for Saudis. Min

Zhu said the Saudis also face a challenge in reducing

dependence on their main energy markets such as China. He

said the global credit expansionary cycle is ending, which

means the Middle East needs to seek more growth drivers from

Page 3 of 6

4. inside the economy rather than from external demand. (Qatar

Tribune)

Global crude market well balanced – The Saudi Arabian Oil

Minister Ali al-Naimi said the global crude oil market is in

equilibrium and inventories are in a good position. Al-Naimi said

he is satisfied with the current crude prices as well as supply

and demand levels. Meanwhile, demand for OPEC’s crude is

expected to remain near the current levels in 2014. So in their

December 4 meeting in Vienna, OPEC ministers are expected to

stick to their output ceiling of 30mn barrels per day. (Bloomberg)

Saudi Aramco raises crude price premiums for Asia – The

Saudi Arabian Oil Company (Saudi Aramco) has raised its

premiums used to set official selling prices for light crudes to

Asian customers for January and increased differentials on all

grades for US buyers. Saudi Aramco said it raised the monthly

formula differential for Arab Light for Asia to a two-year high,

boosting the premium by 30 cents a barrel, to $3.75 more than

the average of Oman and Dubai grades, the Gulf benchmarks.

Saudi Aramco trimmed differentials for Arab Medium and Arab

Heavy crude to Asia, the only cuts it announced for January.

(Gulf-Times.com)

Alstom SA, BEMCO to establish Alstom Arabia Power

Factory Ltd – Alstom Saudi Arabia Transport & Power Ltd

(Alstom SA) has entered into a JV agreement with Arabian

Bemco Contracting Company (BEMCO) to establish “Alstom

Arabia Power Factory Ltd”. Alstom and BEMCO will hold 50%

stakes in the new company. In the phase one, a world class

manufacturing facility will be established in Saudi Arabia for

power generation components with an initial investment of

SR240mn. In the second phase, Alstom SA and BEMCO will

expand the scope of this facility to other power generation

equipment as well. Located in King Abdullah Economic City, the

new factory will train and employ hundreds of Saudi nationals.

(Bloomberg)

Al-Khodari Sons renews credit facilities with NCB – Abdullah

A. M. Al-Khodari Sons Company has renewed its existing

Islamic credit agreement worth SR443.96mn with the National

Commercial Bank (NCB). These credit facilities comprise 39%

Murabaha financing, 61% multi-bonds and documentary credit.

The facilities are secured by promissory notes and contract

proceeds from the financed projects. The agreement will expire

on September 30, 2014; however, the credit limits will mature

over the life of the prospective financed projects, ranging from 1

to 2 years. (Tadawul)

SABIC opens technical center in Shanghai – Saudi Basic

Industries Corporation’s (SABIC) Chairman Prince Saud Bin

Abdullah Bin Thunayan has inaugurated the SABIC Technical

Center (STC) in Shanghai. The new center worth $100mn will

serve as the Greater China Head Office for all Shanghai-based

employees that include R&D and supporting functions.

(Gulfbase.com)

Saudi CMA approves Maceen Capital’s capital increase

request – The Saudi Capital Market Authority Board (Saudi

CMA) has approved Maceen Capital’s request for increasing its

capital from SR50mn to SR100mn. (Tadawul)

UAE MoF signs deal with Netherlands to protect

investments – The UAE’s Ministry of Finance (MoF) has signed

an agreement with the Netherlands for protecting and

encouraging investments in the Netherlands. This agreement

aims to create a suitable investment environment for both

countries and protect them from any non-commercial and

political risks. (Bloomberg)

Cluttons: HNWIs eye Dubai as real estate recovery drives

inward investment – According to a report by Cluttons, Dubai

is poised to enjoy heightened investor interest as its real estate

recovery drives further inward investment, particularly from the

GCC region and the Middle East. High net worth individuals

(HNWIs) from Manama and Muscat favor Dubai over London as

their primary global real estate investment destination. Cluttons

said the property market is unlikely to overheat since average

residential values remain well below the market peak despite

recent gains. The report argued that the recent steps taken by

the UAE Central Bank such as federal mortgage caps and the

Dubai Land Department doubling the property registration fees

from 2% to 4% are expected to dampen any speculation.

(GulfBase.com)

Damac successfully raises $348mn through GDRs – Damac

Real Estate Development Ltd has successfully raised $348mn

through an issue of Global Depositary Receipts (GDR) on the

London Stock Exchange. These GDRs were priced at $12.25

each. Damac sold 28.39mn shares, which value the company at

$2.65bn. (Reuters)

Al Mazaya to expand investments in Dubai – Al Mazaya

Holding’s acting CEO Ibrahim Al Saqabi said the company’s

strategic plan over the next five years includes expanding

investments in the Dubai market. Al Saqabi said that the World

Expo 2020 is expected to significantly increase foreign capital

inflows, and provide 300,000 jobs over the next six or seven

years. (Peninsula Qatar)

Emirates begin A380-800 on Dubai-Los Angeles route –

Emirates Airline has increased the seat capacity on its Dubai

Los Angeles route by replacing Boeing 777-200LR with an

Airbus A380-800. This service will increase the airline’s capacity

to 489 seats as compared to up to 266 onboard the Boeing 777.

With this, Emirates now flies the longest A380 route in

operation. (Bloomberg)

Taqa’s Moroccan unit to issue IPO next week – Moroccan

power company Jorf Lasfar Energy Company (JLEC), which is

owned by Abu Dhabi National Energy Company (Taqa), has

received the go-ahead from the Moroccan market regulator for a

share sale next week to raise 1.5bn Moroccan dirhams. JLEC

will sell 2.25mn new shares in the offering at 447 Moroccan

dirhams each, raising around 1bn Moroccan dirhams. (GulfTimes.com)

IMF: Strong buffers and oil prices strengthen Kuwait’s GDP

growth – The International Monetary Fund’s (IMF) Executive

Board has concluded the Article IV consultation with Kuwait,

which showed that high oil prices and increased production have

enabled the government to continue to post high fiscal and

external surpluses and build strong buffers. Kuwait’s overall real

non-oil GDP growth is projected to gain modestly to 3% in 2013,

driven by the rising domestic consumption and a pick-up in

public investment. However, a slight reduction in oil production

will bring down total real GDP growth below 1%. Meanwhile,

IMF has forecasted the overall average consumer price inflation

(CPI) at 3% in 2013, and fiscal and external surpluses as a

percentage of GDP to be at 27% and 39% respectively. Further,

IMF said Kuwait’s monetary policy has remained

accommodative and its bank credit growth has picked up. Gross

non-performing loans have declined to 4.6% in June 2013 from

5.2% at the end of 2012. Further, IMF expects the economic

outlook to improve further in 2014, where non-oil growth is

expected to increase to 4.4% supported by public capital

spending, in turn pushing the average inflation to 3.5%. (IMF

press release)

Page 4 of 6

5. Kuwait Airways may issue bonds or sukuk – Kuwait Airways’

adviser Amani Bourseli said the airline may issue bonds or

sukuk to finance a deal with Airbus for buying 25 new aircraft

and lease 12 other new planes. The adviser added that part of

this will be from the company’s capital and the rest will be

financed through loans. Bonds or sukuk will be issued

depending on the decision taken by the board of directors. (GulfTimes.com)

Zain not in talks to buy Canar from Etisalat – Kuwaiti

telecoms company Zain said it would not enter any negotiations

to buy Sudanese telecom operator, Canar. Earlier, a source had

said that the UAE’s Etisalat could resurrect talks to sell its

Sudanese subsidiary to Zain. (Gulf-Times.com)

Oman Air signs repair deal with Bombardier Aerospace –

Oman Air has signed an eight-year repair agreement with

Bombardier Aerospace to perform all maintenance work on

Rolls Royce Trent 700 inlet cowls for its Airbus A330 aircraft

fleet. The airline currently operates seven A330s along with

another three A330s to be delivered in 2014. (GulfBase.com)

SBJ appoints Atkins to supervise infrastructure works –

The Saraya Bandar Jissah (SBJ) has appointed UK-based

Atkins to supervise the infrastructure works for the $600mn

project in Oman. Atkins Oman will manage the progress of these

works on site and supervise the contractor. The phase one of

this work is nearing completion following 12 months of

scheduled work. (Bloomberg)

Bahrain reviews subsidies that cause over-consumption –

Bahrain’s Central Bank Governor Rasheed al-Maraj said the

country will revamp those subsidies that have led to excessive

consumption of energy and foods. He stated that the

government is very much aware of the unsustainable levels of

consumption in energy and some foods, and has realized the

need to direct subsidies toward the needy, which is now getting

reflected in its programs. al-Maraj said the changes may begin

as early as this month and will include certain mitigations for

preventing higher inflation, which stood at 3.8% in October. alMaraj expects inflation to be close to the IMF’s forecast of 2.7%

by the year-end. (Bloomberg)

Page 5 of 6

6. Rebased Performance

Daily Index Performance

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

1.3%

149.0

0.6%

0.7%

130.0

0.0%

0.0%

118.1

(0.7%)

0.3%

0.2%

(0.1%)

(0.3%)

(1.3%)

S&P Pan Arab

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Dubai

Oman

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

1,223.42

0.3

(2.4)

(27.0)

DJ Industrial

19.13

(0.2)

(4.3)

(37.0)

112.62

1.0

2.7

1.4

3.83

(0.3)

1.0

11.8

STOXX 600

123.25

2.7

5.3

37.7

137.00

(0.2)

(0.2)

(20.8)

1.36

0.3

(0.0)

3.0

102.51

(0.4)

0.1

18.2

GBP

1.64

0.2

0.1

0.8

CHF

1.11

0.5

0.2

1.2

AUD

0.91

0.3

0.3

(12.1)

USD Index

80.59

(0.4)

(0.1)

RUB

33.26

0.1

0.4

BRL

0.42

(0.8)

(1.7)

(13.7)

Yen

Bahrain

Jul-13

Kuwait

May-12 Dec-12

Abu Dhabi

QE Index

Oct-11

Qatar

Jan-10 Aug-10 Mar-11

Saudi Arabia

(1.3%)

(2.0%)

Close

1D%

WTD%

YTD%

15,914.62

(0.6)

(1.1)

21.4

S&P 500

1,795.15

(0.3)

(0.6)

25.9

NASDAQ 100

4,037.20

(0.2)

(0.6)

33.7

319.13

(1.5)

(1.9)

14.1

DAX

9,223.40

(1.9)

(1.9)

21.2

FTSE 100

6,532.43

(1.0)

(1.8)

10.8

4,172.44

(2.6)

(2.9)

14.6

15,749.66

0.6

0.6

51.5

MSCI EM

1,002.71

(1.1)

(1.5)

(5.0)

SHANGHAI SE Composite

2,222.67

0.7

0.1

(2.0)

HANG SENG

23,910.47

(0.5)

0.1

5.5

1.0

BSE SENSEX

20,854.92

(0.2)

0.3

7.4

9.0

Bovespa

50,348.89

(1.7)

(4.1)

(17.4)

1,372.44

(1.9)

(2.2)

(10.1)

Source: Bloomberg

CAC 40

Nikkei

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6