Wabco India Q1FY15: Higher OEM revenues lead to top line beat; accumulate

•

1 like•238 views

Wabco’s (WIL’s) Q1FY15 results were above our estimates on account of better‐ than‐expected top‐line. Top‐line grew by 23.1% YoY to Rs3.2bn (PLe: Rs2.8bn), mainly led by strong traction in the OEM segment (grew 43% YoY).

Recommended

Recommended

More Related Content

More from IndiaNotes.com

More from IndiaNotes.com (20)

Recently uploaded

Recently uploaded (20)

Wabco India Q1FY15: Higher OEM revenues lead to top line beat; accumulate

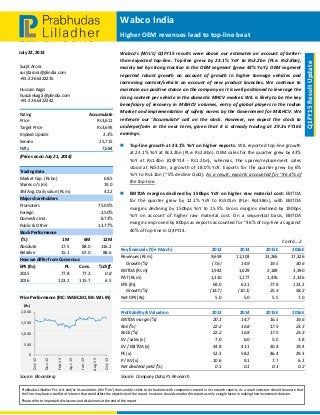

- 1. Wabco India Higher OEM revenues lead to top‐line beat July 22, 2014 Prabhudas Lilladher Pvt. Ltd. and/or its associates (the 'Firm') does and/or seeks to do business with companies covered in its research reports. As a result investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision. Please refer to important disclosures and disclaimers at the end of the report Q1FY15 Result Update Surjit Arora surjitarora@plindia.com +91‐22‐66322235 Hussain Kagzi hussainkagzi@plindia.com +91‐22‐66322242 Rating Accumulate Price Rs3,611 Target Price Rs3,695 Implied Upside 2.3% Sensex 25,715 Nifty 7,684 (Prices as on July 21, 2014) Trading data Market Cap. (Rs bn) 68.5 Shares o/s (m) 19.0 3M Avg. Daily value (Rs m) 42.2 Major shareholders Promoters 75.00% Foreign 2.50% Domestic Inst. 8.73% Public & Other 13.77% Stock Performance (%) 1M 6M 12M Absolute 17.5 88.0 116.2 Relative 15.1 67.0 88.6 How we differ from Consensus EPS (Rs) PL Cons. % Diff. 2015 77.8 77.2 0.8 2016 123.2 115.7 6.5 Price Performance (RIC: WABC.BO, BB: WIL IN) Source: Bloomberg 0 500 1,000 1,500 2,000 Oct‐12 Dec‐12 Feb‐13 Apr‐13 Jun‐13 Aug‐13 Oct‐13 (Rs) Wabco’s (WIL’s) Q1FY15 results were above our estimates on account of better‐ than‐expected top‐line. Top‐line grew by 23.1% YoY to Rs3.2bn (PLe: Rs2.8bn), mainly led by strong traction in the OEM segment (grew 43% YoY). OEM segment reported robust growth on account of growth in higher tonnage vehicles and increasing content/vehicle on account of new product launches. We continue to maintain our positive stance on the company as it is well positioned to leverage the rising content per vehicle in the domestic MHCV market. WIL is likely to be the key beneficiary of recovery in M&HCV volumes, entry of global players in the Indian Market and implementation of safety norms by the Government for M&HCV. We reiterate our ‘Accumulate’ call on the stock. However, we expect the stock to underperform in the near term, given that it is already trading at 29.3x FY16E earnings. Top‐line growth at 23.1% YoY on higher exports: WIL reported top‐line growth at 23.1% YoY at Rs3.2bn (PLe: Rs2.8bn). OEM sales for the quarter grew by 43% YoY at Rs1.4bn (Q4FY14 ‐ Rs1.2bn), whereas, the spares/replacement sales stood at Rs532m, a growth of 18.0% YoY. Exports for the quarter grew by 6% YoY to Rs1.1bn (~5% decline QoQ). As a result, exports accounted for ~36.4% of the top‐line. EBITDA margins declined by 150bps YoY on higher raw material cost: EBITDA for the quarter grew by 12.1% YoY to Rs501m (PLe: Rs438m), with EBITDA margins declining by 150bps YoY to 15.5%. Gross margins declined by 190bps YoY on account of higher raw material cost. On a sequential basis, EBITDA margins improved by 80bps as exports accounted for ~36% of top‐line as against 40% of top‐line in Q4FY14. Contd…2 Key financials (Y/e March) 2013 2014 2015E 2016E Revenues (Rs m) 9,659 11,103 13,265 17,326 Growth (%) (7.6) 14.9 19.5 30.6 EBITDA (Rs m) 1,942 1,629 2,189 3,390 PAT (Rs m) 1,310 1,177 1,476 2,336 EPS (Rs) 69.0 62.1 77.8 123.2 Growth (%) (14.7) (10.1) 25.4 58.2 Net DPS (Rs) 5.0 5.0 5.0 7.0 Profitability & Valuation 2013 2014 2015E 2016E EBITDA margin (%) 20.1 14.7 16.5 19.6 RoE (%) 22.2 16.8 17.9 23.3 RoCE (%) 22.2 16.8 17.9 23.3 EV / sales (x) 7.0 6.0 5.0 3.8 EV / EBITDA (x) 34.8 41.1 30.4 19.4 PE (x) 52.3 58.2 46.4 29.3 P / BV (x) 10.6 9.1 7.7 6.2 Net dividend yield (%) 0.1 0.1 0.1 0.2 Source: Company Data; PL Research

- 2. July 22, 2014 2 Wabco India Higher depreciation charge led to a decline in PAT: Depreciation charge for the quarter increased by 61.2% YoY to Rs107m (Rs55m was the charge on account of New Companies Act, where the life of assets has been reduced). As a result, PAT for the quarter de‐grew by 13.4% YoY to Rs307m. ABS implementation likely by 2015: Management indicated that ABS is likely to be implemented in the M&HCV segment by Oct 2015. Though the margins could be lower in ABS, we are building in an incremental revenue of Rs1.7bn in FY16E. Management indicated that as compared to earlier expectation of ABS implementation in certain segments of M&HCV, it is likely to be implemented across the board. Strong balance sheet and free cash flow to support higher valuations: Given that the profitability is likely to grow at a CAGR of ~41% with a moderate capex for the next couple of years, we expect free cash generation of Rs448m in FY15E and Rs1.0bn in FY16E. The stock has traded at an average P/E of 20‐25x and Average P/BV of 3.5‐5x 1 year forward. At the current market price, the stock is trading at 46.4x FY15E and 29.3x FY16E earnings. In the near term, the stock could be range‐bound, though we are positive on the stock from a long term perspective, given the strong parentage and robust earnings growth trajectory. Delay in ABS implementation in M&HCV space is a key risk to our call. Exhibit 1: Q1FY15 Result Overview (Rs m) Y/e March Q1FY15 Q1FY14 YoY gr. (%) Q4FY14 FY15E FY14 YoY gr. (%) Net Sales 3,236 2,628 23.1 3,156 13,265 11,103 19.5 Expenditure Raw Material 1,860 1,461 27.3 1,829 7,496 6,337 18.3 % of Net Sales 57.5 55.6 58.0 56.5 57.1 Salaries & Wages 350 296 18.1 333 1,414 1,249 13.2 % of Net Sales 10.8 11.3 10.6 10.7 11.2 Other Exp. 525 424 23.8 531 2,165 1,888 14.7 % of Net Sales 16.2 16.1 16.8 16.3 17.0 Total Expenditure 2,734 2,181 25.4 2,694 11,076 9,474 16.9 EBITDA 501 447 12.1 462 2,189 1,629 34.4 EBITDA Margin (%) 15.5 17.0 14.7 16.5 14.7 Depreciation 107 66 61.2 96 389 318 22.2 Net interest 0 ‐ 0 ‐ 3 Non Operative Income 33 129 (73.9) 16 250 304 (17.8) PBT 428 509 (16.0) 383 2,051 1,612 27.2 Tax Total 121 155 (22.0) 55 574 435 32.0 Tax Rate‐Total (%) 28.3 30.5 14.3 28.0 27.0 Reported Profit 307 354 (13.4) 328 1,476 1,177 25.4 Adj. PAT 307 354 (13.4) 328 1,476 1,177 25.4 Source: Company Data, PL Research

- 3. July 22, 2014 3 Wabco India Income Statement (Rs m) Y/e March 2013 2014 2015E 2016E Net Revenue 9,659 11,103 13,265 17,326 Raw Material Expenses 5,172 6,337 7,496 9,772 Gross Profit 4,487 4,766 5,769 7,554 Employee Cost 1,070 1,249 1,414 1,584 Other Expenses 1,475 1,888 2,165 2,579 EBITDA 1,942 1,629 2,189 3,390 Depr. & Amortization 217 318 389 445 Net Interest — 3 — — Other Income 126 304 250 300 Profit before Tax 1,852 1,612 2,051 3,245 Total Tax 542 435 574 909 Profit after Tax 1,310 1,177 1,476 2,336 Ex‐Od items / Min. Int. — — — — Adj. PAT 1,310 1,177 1,476 2,336 Avg. Shares O/S (m) 19.0 19.0 19.0 19.0 EPS (Rs.) 69.0 62.1 77.8 123.2 Cash Flow Abstract (Rs m) Y/e March 2013 2014 2015E 2016E C/F from Operations 984 1,527 1,499 1,834 C/F from Investing (701) (857) (1,051) (799) C/F from Financing (109) (109) (109) (152) Inc. / Dec. in Cash 175 561 340 883 Opening Cash 819 993 1,555 1,894 Closing Cash 993 1,555 1,894 2,777 FCFF 434 737 589 1,234 FCFE 434 737 589 1,234 Key Financial Metrics Y/e March 2013 2014 2015E 2016E Growth Revenue (%) (7.6) 14.9 19.5 30.6 EBITDA (%) (11.7) (16.1) 34.4 54.9 PAT (%) (14.7) (10.1) 25.4 58.2 EPS (%) (14.7) (10.1) 25.4 58.2 Profitability EBITDA Margin (%) 20.1 14.7 16.5 19.6 PAT Margin (%) 13.6 10.6 11.1 13.5 RoCE (%) 22.2 16.8 17.9 23.3 RoE (%) 22.2 16.8 17.9 23.3 Balance Sheet Net Debt : Equity (0.2) (0.2) (0.2) (0.2) Net Wrkng Cap. (days) 93 56 55 64 Valuation PER (x) 52.3 58.2 46.4 29.3 P / B (x) 10.6 9.1 7.7 6.2 EV / EBITDA (x) 34.8 41.1 30.4 19.4 EV / Sales (x) 7.0 6.0 5.0 3.8 Earnings Quality Eff. Tax Rate 29.3 27.0 28.0 28.0 Other Inc / PBT 6.8 18.9 12.2 9.2 Eff. Depr. Rate (%) 5.5 6.7 6.9 7.1 FCFE / PAT 33.1 62.6 39.9 52.8 Source: Company Data, PL Research. *adj. for Rs18/share for insurance value Balance Sheet Abstract (Rs m) Y/e March 2013 2014 2015E 2016E Shareholder's Funds 6,488 7,552 8,920 11,104 Total Debt 9 9 9 9 Other Liabilities 117 161 161 161 Total Liabilities 6,614 7,722 9,090 11,275 Net Fixed Assets 2,889 3,175 3,636 3,791 Goodwill — — — — Investments 255 502 702 902 Net Current Assets 3,471 4,046 4,752 6,581 Cash & Equivalents 991 1,554 1,894 2,776 Other Current Assets 3,804 4,255 4,981 6,398 Current Liabilities 1,325 1,764 2,123 2,593 Other Assets — — — — Total Assets 6,614 7,723 9,090 11,274 Quarterly Financials (Rs m) Y/e March Q2FY14 Q3FY14 Q4FY14 Q1FY15 Net Revenue 2,726 2,597 3,156 3,236 EBITDA 360 360 462 501 % of revenue 13.2 13.9 14.7 15.5 Depr. & Amortization 74 85 96 107 Net Interest — — — — Other Income 129 30 16 33 Profit before Tax 415 304 383 428 Total Tax 123 102 55 121 Profit after Tax 292 202 328 307 Adj. PAT 292 202 328 307 Source: Company Data, PL Research.

- 4. July 22, 2014 4 Wabco India Prabhudas Lilladher Pvt. Ltd. 3rd Floor, Sadhana House, 570, P. B. Marg, Worli, Mumbai‐400 018, India Tel: (91 22) 6632 2222 Fax: (91 22) 6632 2209 Rating Distribution of Research Coverage 29.0% 51.4% 19.6% 0.0% 0% 10% 20% 30% 40% 50% 60% BUY Accumulate Reduce Sell % of Total Coverage PL’s Recommendation Nomenclature BUY : Over 15% Outperformance to Sensex over 12‐months Accumulate : Outperformance to Sensex over 12‐months Reduce : Underperformance to Sensex over 12‐months Sell : Over 15% underperformance to Sensex over 12‐months Trading Buy : Over 10% absolute upside in 1‐month Trading Sell : Over 10% absolute decline in 1‐month Not Rated (NR) : No specific call on the stock Under Review (UR) : Rating likely to change shortly This document has been prepared by the Research Division of Prabhudas Lilladher Pvt. Ltd. Mumbai, India (PL) and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of PL. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, PL has not independently verified the accuracy or completeness of the same. Neither PL nor any of its affiliates, its directors or its employees accept any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient's particular circumstances and, in case of doubt, advice should be sought from an independent expert/advisor. Either PL or its affiliates or its directors or its employees or its representatives or its clients or their relatives may have position(s), make market, act as principal or engage in transactions of securities of companies referred to in this report and they may have used the research material prior to publication. We may from time to time solicit or perform investment banking or other services for any company mentioned in this document.