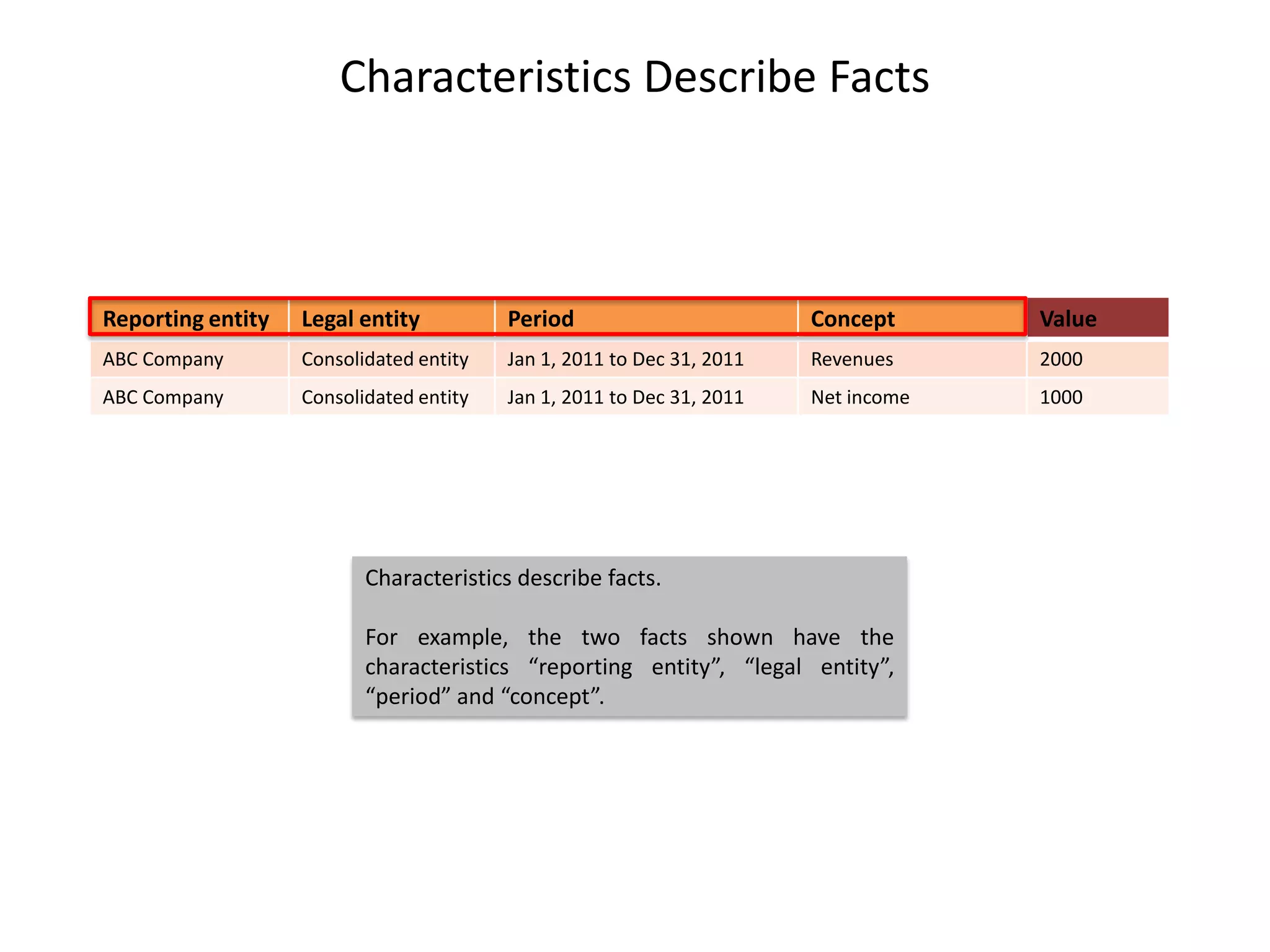

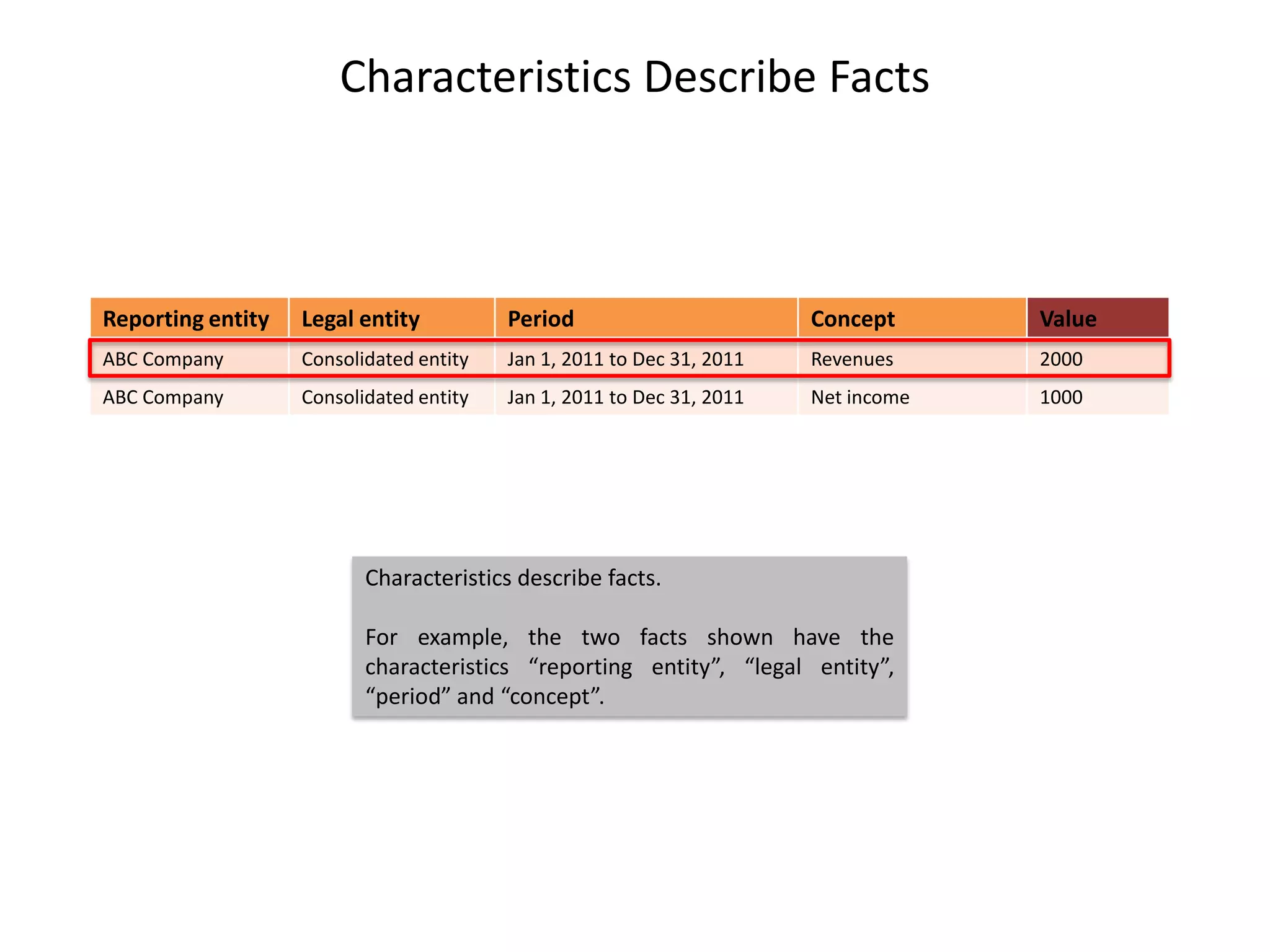

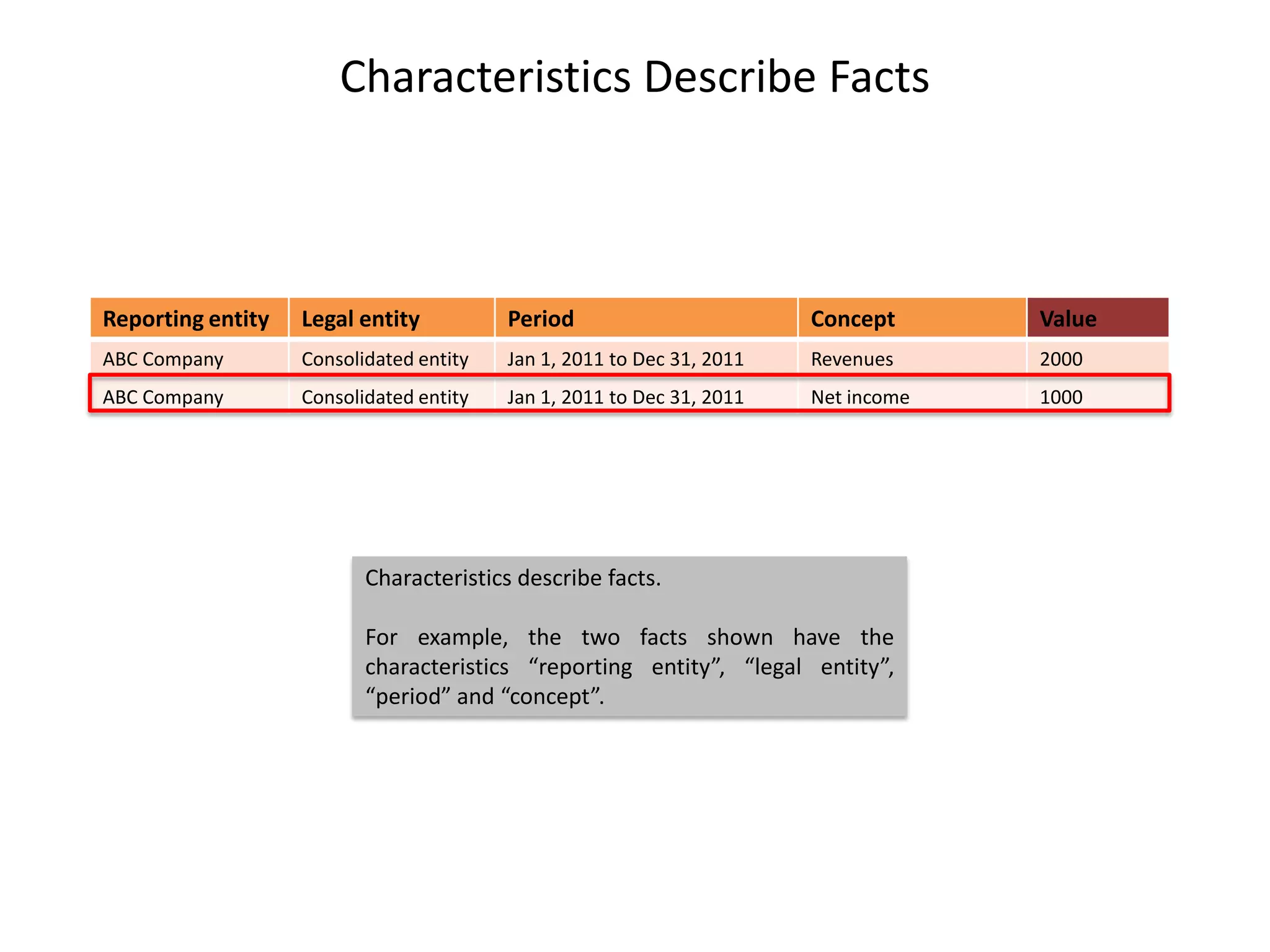

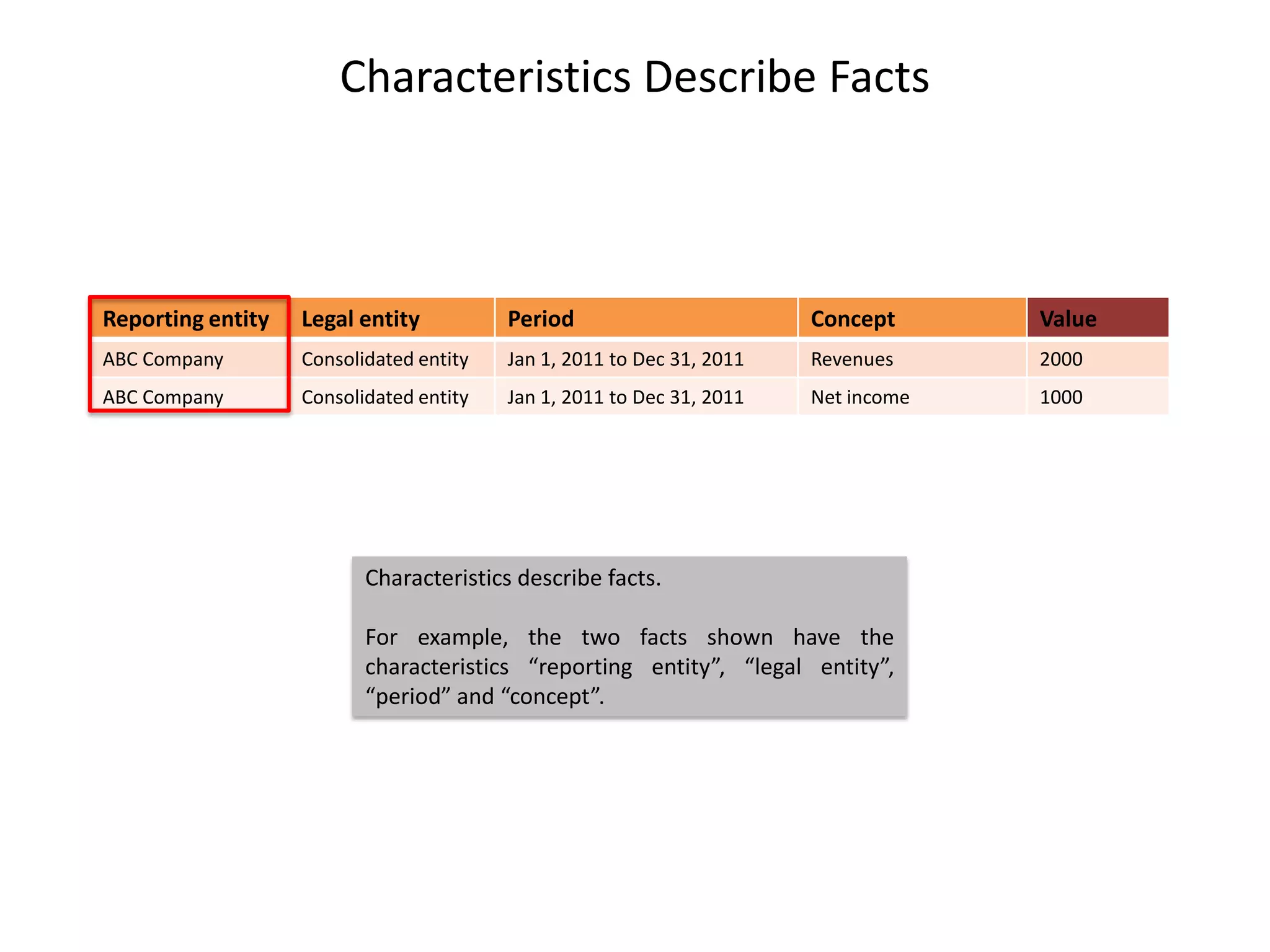

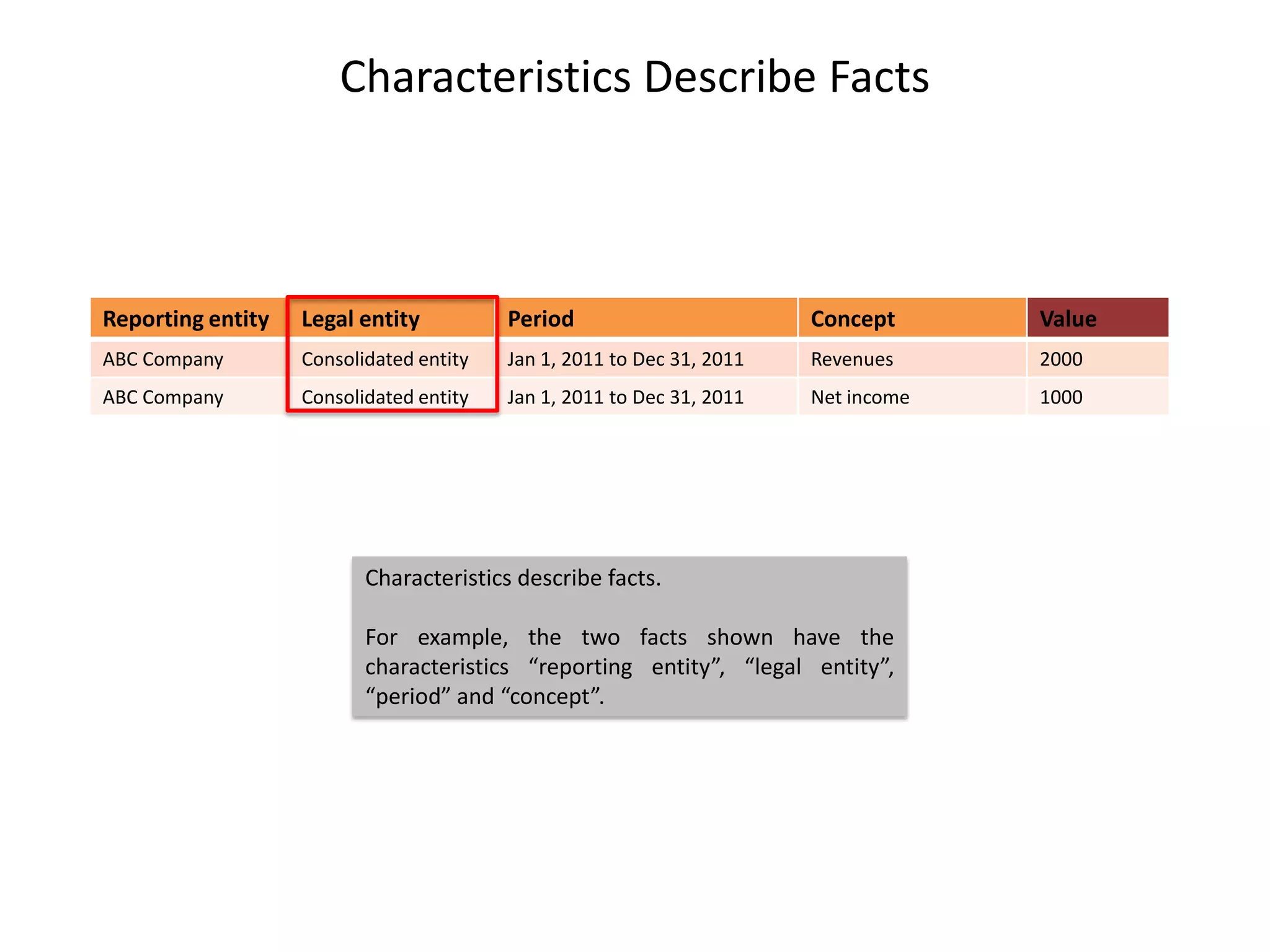

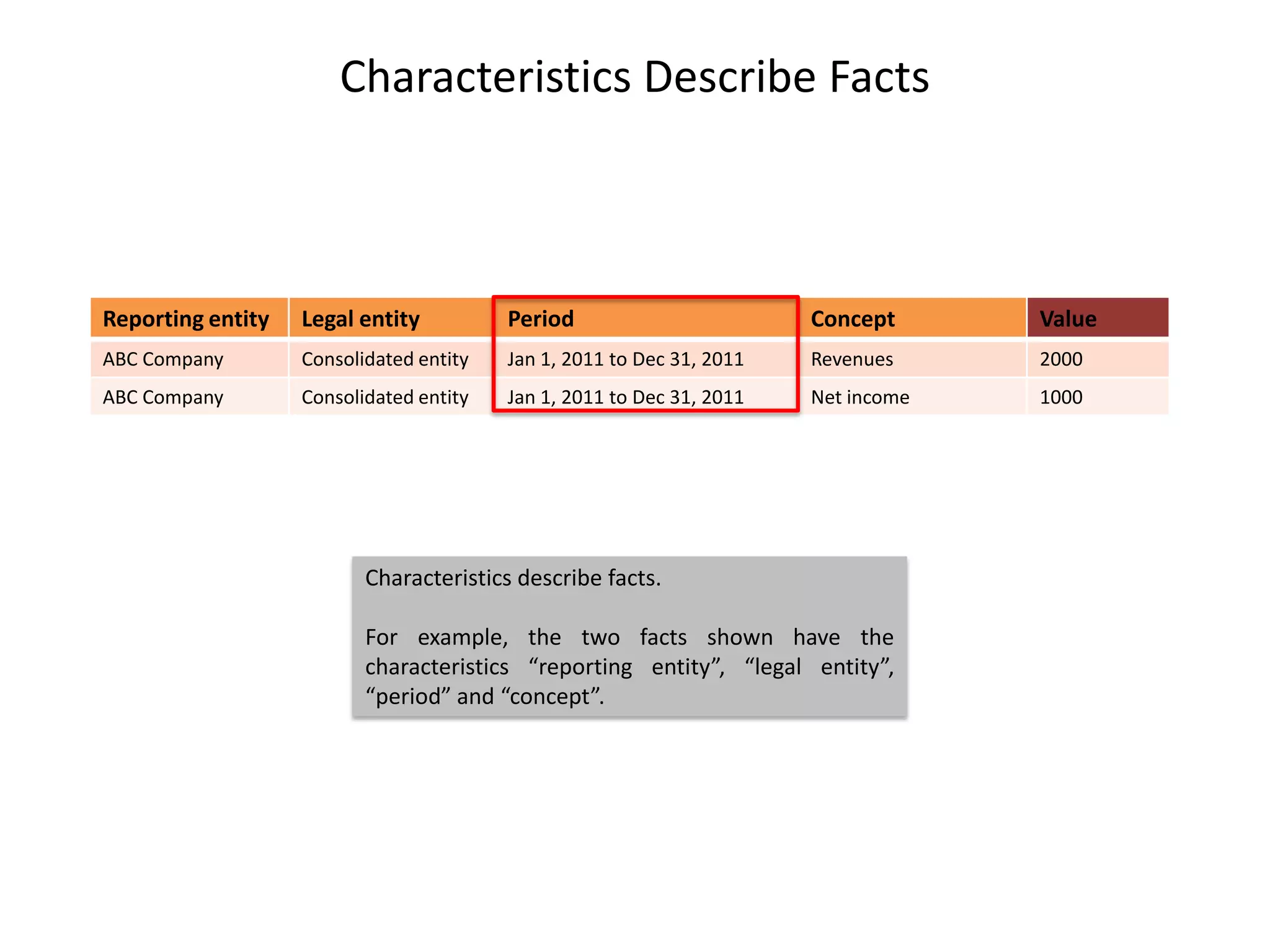

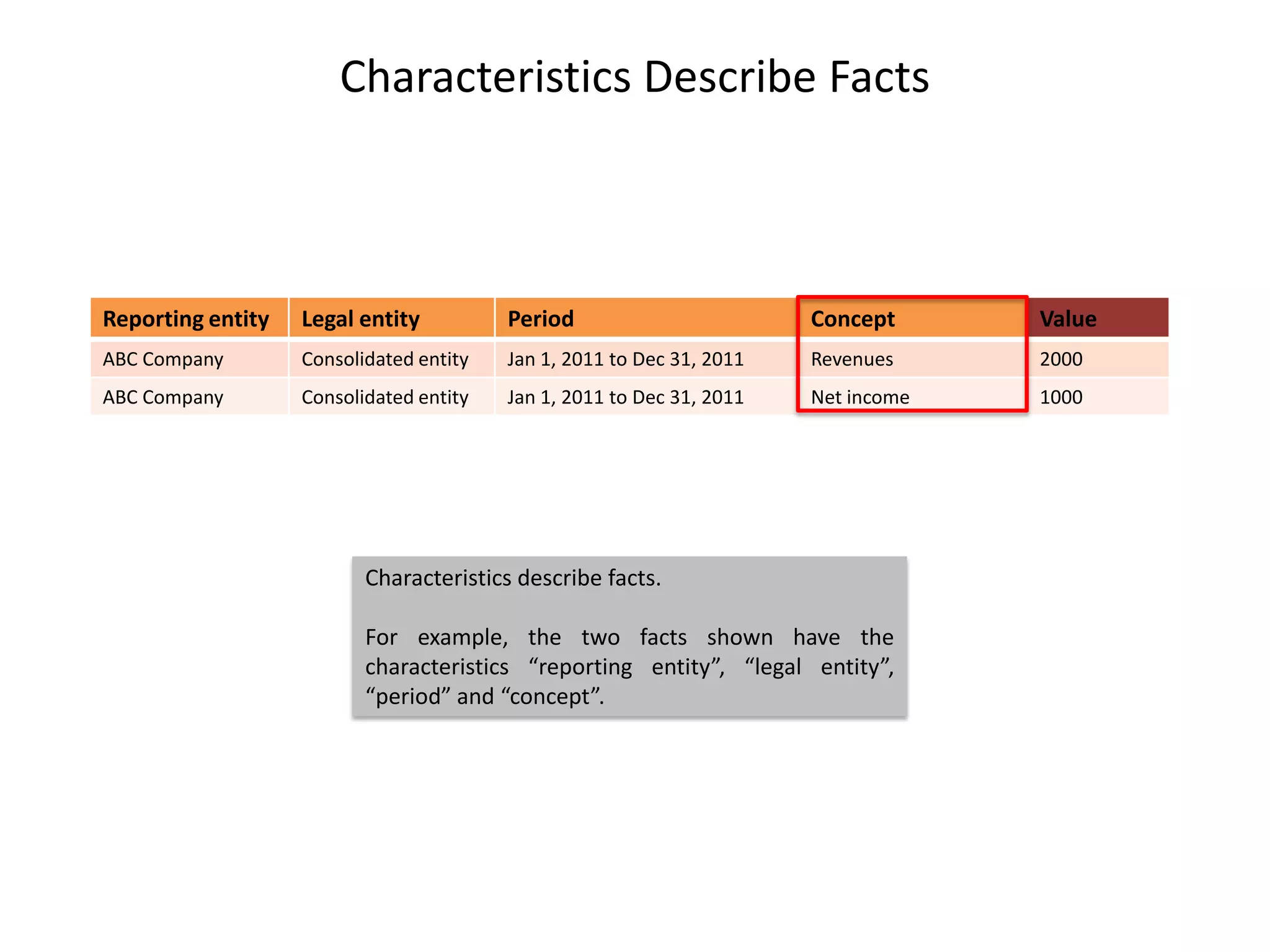

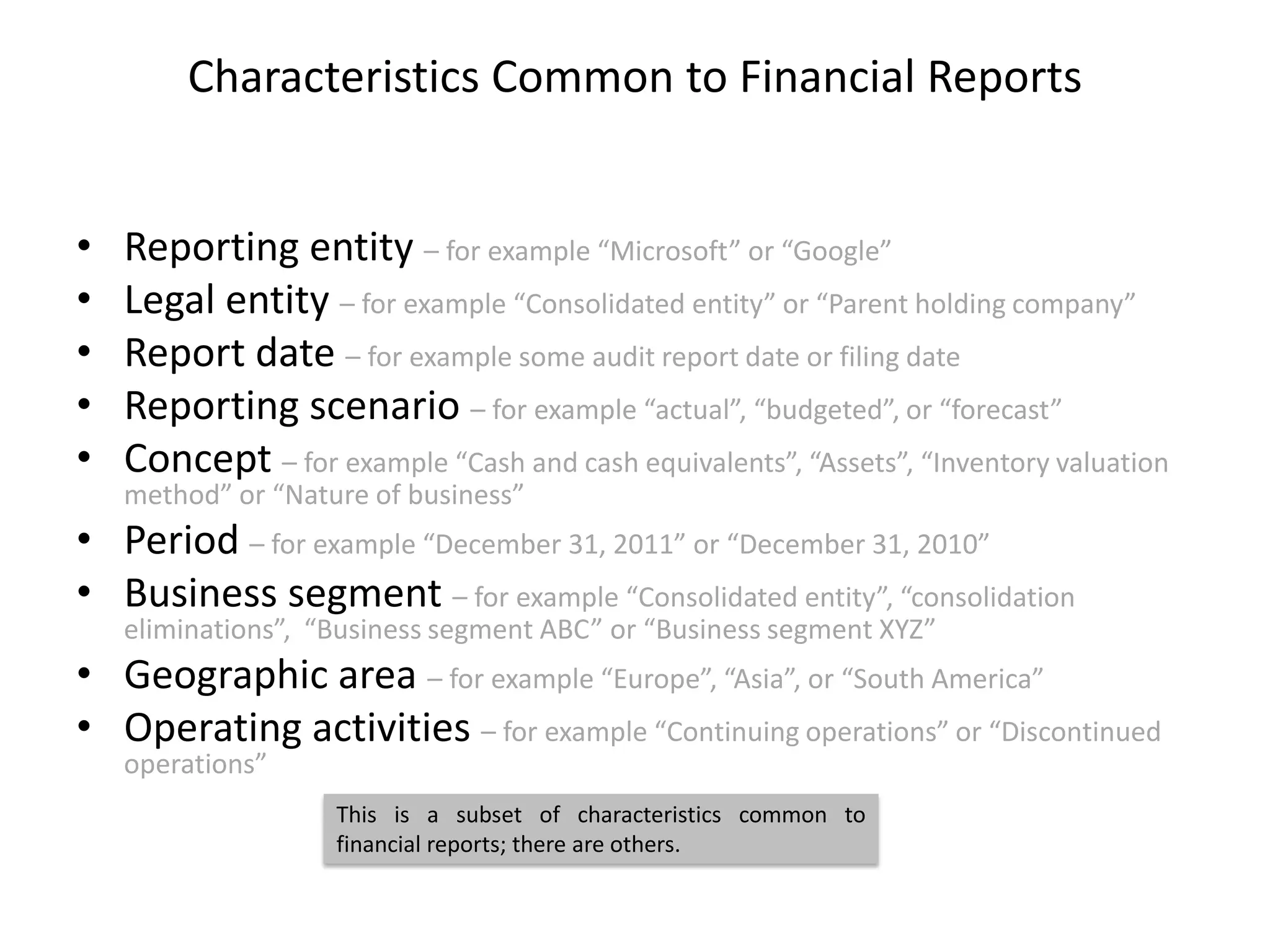

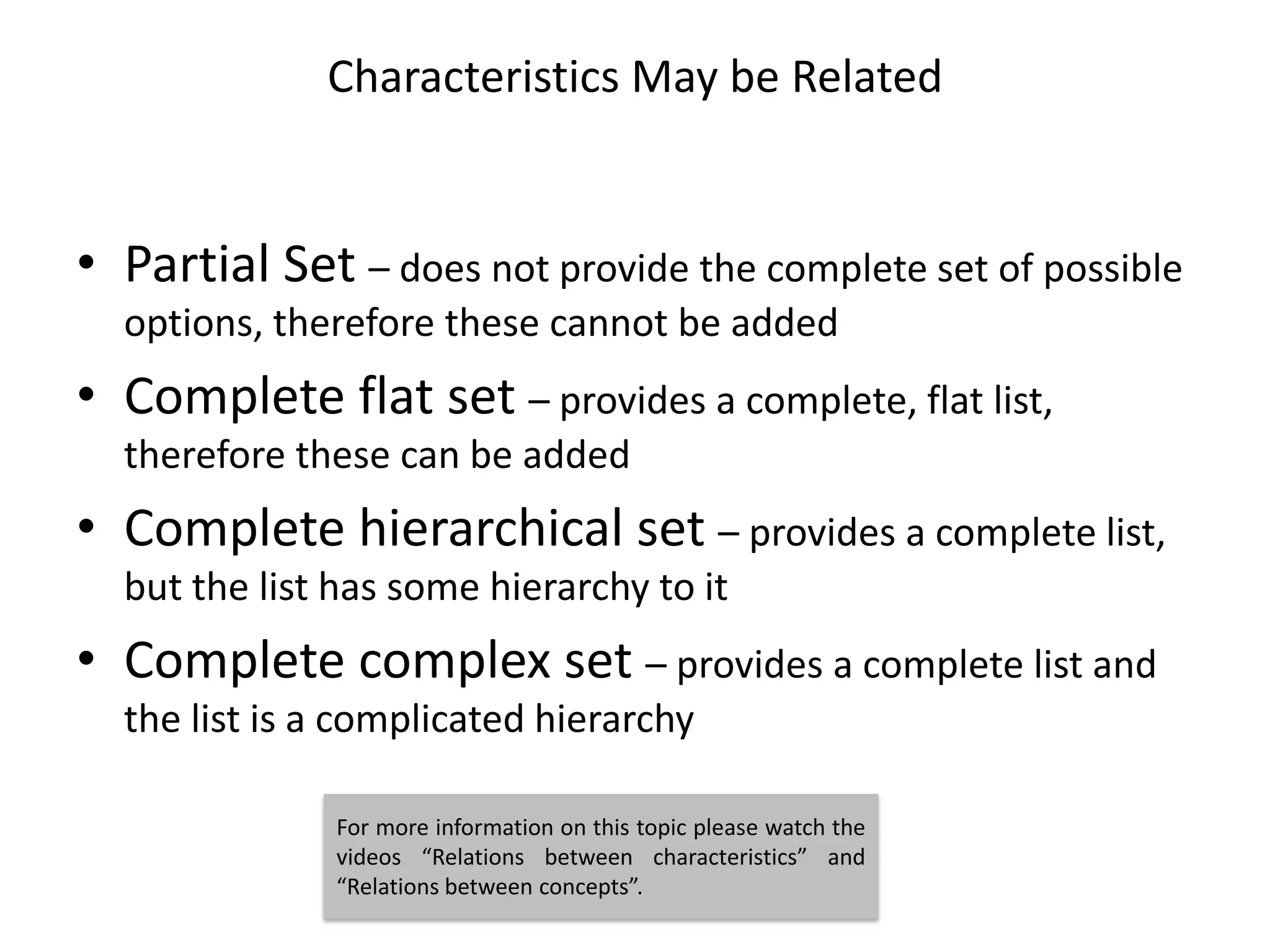

The document discusses characteristics in financial reports. It states that characteristics describe facts and lists some common characteristics like reporting entity, legal entity, period, and concept. Characteristics can also be related to each other in complex ways through hierarchies and partial/complete sets.