Recommended

More Related Content

Similar to CFR - PART 1.docx

Similar to CFR - PART 1.docx (20)

Recently uploaded

Recently uploaded (20)

CFR - PART 1.docx

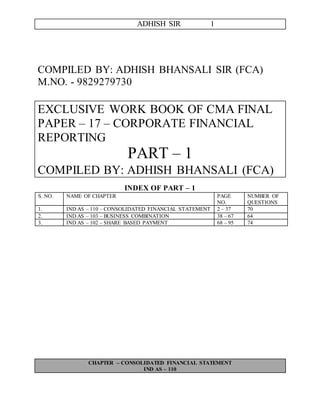

- 1. ADHISH SIR 1 COMPILED BY: ADHISH BHANSALI SIR (FCA) M.NO. - 9829279730 EXCLUSIVE WORK BOOK OF CMA FINAL PAPER – 17 – CORPORATE FINANCIAL REPORTING PART – 1 COMPILED BY: ADHISH BHANSALI (FCA) INDEX OF PART – 1 S. NO. NAME OF CHAPTER PAGE NO. NUMBER OF QUESTIONS 1. IND AS – 110 – CONSOLIDATED FINANCIAL STATEMENT 2 – 37 70 2. IND AS – 103 – BUSINESS COMBINATION 38 – 67 64 3. IND AS – 102 – SHARE BASED PAYMENT 68 – 95 74 CHAPTER – CONSOLIDATED FINANCIAL STATEMENT IND AS – 110

- 2. ADHISH SIR 2 TOPIC: BASIS CONSOLIDATIONS QUESTIONS Question: 1 On 1.1.2009, X paid ₹21,600 to acquire 90 % of equity shares of Y. At 31.12.2009, financial position of each of the following two companies were as follows: X Y Non – current assets 70,000 36,000 Investment in Y Limited 21,600 Current assets 27,000 15,000 Total 1,18,600 51,000 Share capital (` 1 per share) 62,000 24,000 Retained earnings 44,600 19,500 Current liabilities 12,000 7,500 1,18,600 51,000 Balance of Retained earnings on 1.1.2009 for YLimited was `8,000. Required: (i) Calculate amount of goodwill for consolidated statement (ii) Calculate value of NCI for consolidated statement (iii) Calculate retained earnings for consolidated statement Question: 2 On 1.1.2008, Yati Limited acquired 70 % of the ordinary shares of Dishita Limited, when the retained earnings of Dishita Limited stood at `15,000. The fair value of non – controlling interest on the date of acquisition was `40,000. At 31.12.2010 the statement of financial position of each of the two companies were as follows: Yati Limited Dishita Limited Non current assets 1,25,000 75,000 Investments in Dishita Ltd. (At cost) 50,000 Current assets 30,000 15,000 2,05,000 90,000 Share capital (` 1 each) 1,20,000 50,000 Retained earnings 65,000 32,000 Current liabilities 20,000 8,000 2,05,000 90,000 Required: (i) Goodwill to be shown in consolidated financial statement (ii) NCI to be shown in consolidated financial statement (iii) Retained earnings to be shown in consolidated financial statement. Question: 3 H Limited acquired 80 % Share capital of S Limited on 1.10.2019 for ₹4,25,000. Following information is available in respect of S Limited: Particulars 1.4.2019` 31.3.2020 Share Capital 6,50,000 6,50,000 Profit and Loss account 60,000 1,32,000 General reserve 40,000 1,00,000 Capital reserve 25,000 Preliminary expenses 5,000 H Limited decided to measure NCI at fair value. Required:

- 3. ADHISH SIR 3 (a) Goodwill to be shown in consolidated financial statement (b) NCI to be shown in consolidated financial statement (c) Other equity to be shown in consolidated financial statement. Question: 4 [IFRS - Adopted] M Limited paid ₹ 1,40,000 cash to acquire 60 % of ordinary shares of B Limited and use proportionate net asset approach to determine NCI. Additional information available at acquisition: Book value Fair value Cash 5,000 Inventory 10,000 32,000 Land 1,15,000 1,15,000 Equipment 20,600 20,600 Building 10,100 10,100 1,60,700 Accounts payable 40,000 40,000 Long term loans 20,700 20,700 Share capital 55,000 Retained earnings 45,000 1,60,700 (a) Calculate amount of Goodwill / Bargain purchase (b) Calculate amount of Goodwill / Bargain purchase if NCI is to be measured at fair value method. Question: 5 [IFRS - Adopted] The following statement of financial position were extracted from the books of two companies at 31.12.2019: H S I. Assets: Non – current assets 75,000 11,000 Investment in shares of S Limited 27,000 - Current assets 2,14,000 33,000 Total 3,16,000 44,000 II. Equity and Liabilities: Equity share capital 80,000 4,000 Security premium 20,000 6,000 Retained earnings 40,000 9,000 Current liabilities 1,76,000 25,000 Total 3,16,000 44,000 H Limited acquired all of the share capital of S one year ago. The retained earnings of S stood at 2,000 on the day of acquisition. Goodwill is calculated by using fair value method. Prepare consolidated Balance – sheet at 31.12.2019. Question: 6 [IFRS - adopted] The Following separate financial position have been prepared at 31.12.2018: H S I. Assets: Non – current assets PPE 85,000 18,000 Investment in S Limited 60,000 Current assets 1,60,000 84,000 Total 3,05,000 1,02,000 II. Equity and Liabilities:

- 4. ADHISH SIR 4 Equity share capital 65,000 20,000 Security premium 35,000 10,000 Retained earnings 70,000 25,000 Current liabilities 1,35,000 47,000 Total 3,05,000 1,02,000 H Limited acquired 80 % holding in S Limited on 1.1.2018, when retained earnings of S Limited stood at ₹ 20,000. On this date fair value of the NCI shareholding is S Limited was ₹12,500. The Hgroup uses the fair value method to value the NCI. Prepare Consolidated balance – sheet. Question: 7 [IFRS - Adopted] P acquired 75 % of the shares in S on 1.12017 when S had retained earnings of ₹ 15,000. The market price of S’s share just before the date of acquisition was ₹ 1.60. P value the NCI at fair value. The statements of financial position of P and S at 31.12.2017 were as follows: P S I. Assets: Non – current assets: PPE 60,000 50,000 Investment in S Limited 68,000 - Current assets 52,000 35,000 Total 1,80,000 85,000 II. Equity and Liabilities: Share capital 1,00,000 50,000 Retained earnings 70,000 25,000 Current liabilities 10,000 10,000 Total 1,80,000 85,000 Prepare Consolidated statement of financial position as on 31.12.2017. Question: 8 H Limited acquired 80 % share capital of S Limited on 1.10.2019. Financial positions of both the companies as on 31.3.2020 were as under: H S I. Assets: Non current assets 8,00,000 6,50,000 Investment (80 % shares of S Ltd. at cost) 5,25,000 - Current assets 2,75,000 3,50,000 Total 16,00,000 10,00,000 II. Equity and Liabilities: Equity share capital (₹ 10) 7,50,000 6,00,000 Profit and Loss account 1,20,000 1,00,000 General reserve 40,000 60,000 Non – current liabilities 4,40,000 80,000 Current Liabilities 2,50,000 1,60,000 Total 16,00,000 10,00,000 (i) Balances of Reserves of S Limited on 1.4.2019: Profit and Loss account = 34,000 (ii) There was an abnormal loss of ₹ 12,000 due to fire on 1.6.2019. (iii) Abnormal gain of ₹ 24,000 received on 1.1.2020. (iv) H Limited decided to value NCI at proportionate net asset method. Prepare consolidated Balance – sheet as on 31.3.2020.

- 5. ADHISH SIR 5 Question: 9 [CMA – Study Material] The following are the extract Balance – sheet of H and S Company as on 31.3.2016 Liabilities H S Assets H S Share capital (`10) 20,000 10,000 Fixed assets 30,000 15,000 General reserve 10,000 5,000 Current assets 35,000 25,000 Profit and loss account (1.4.2915) 5,000 4,000 Shares in S Limited (800 shares ) 10,000 12 % Debentures 20,000 10,000 Sundry creditors 10,000 5,000 Profit for the year 10,000 6,000 75,000 40,000 75,000 40,000 H Limited acquired shares in S Limited on 1.10.2015. S Limited has a balance of `4,000 in General reserve on 1.4.2015. On the account fire goods costing `2,000 of S Limited were destroyed in June, 2015. The loss has been charged to the profit and loss account for the year. Required to prepare consolidated Balance – sheet. Question: 10 Balance –sheet as on 31.3.2017 Liabilities H Ltd. S Ltd. Assets H Ltd S Ltd. Equity share capital (`10 each) 12,00,000 8,00,000 Fixed assets 9,00,000 10,80,000 General reserve 4,00,000 4,00,000 Investment (75 % shares) 9,62,000 - Profit and loss account 1,00,000 1,00,000 Current assets 2,20,000 5,00,000 10 % Debentures 2,00,000 1,50,000 Preliminary expenses 18,000 20,000 Current liabilities 2,00,000 1,50,000 21,00,000 16,00,000 21,00,000 16,00,000 Additional information: (i) There was an abnormal gain of `10,000 to S Limited on 1.1.2017 and abnormal loss of `5000 on 1.2.2017. (ii) Shares were purchased on 1.10.2016. (iii) Balance of reserves on 1.4.2016: General reserve - `2,20,000 Profit and loss account - `50,000 (iv) There was an abnormal loss of `15,000 on 1.4.2016. Prepare consolidated Balance – sheet as on 31.3.2017. Question: 11 Balance sheet as on 31.3.09 Liabilities H Ltd. S Ltd. Assets H Ltd. S Ltd. Equity share capital 5,00,000 1,50,000 Fixed assets 7,50,000 3,00,000 Profit and loss a/c 1,00,000 50,000 Investments in 60 % shares of S Ltd. 1,50,000 - General reserve 1,00,000 1,00,000 Current assets 2,00,000 1,00,000 Creditors 4,00,000 1,00,000 11,00,000 4,00,000 11,00,000 4,00,000 Shares were purchased on 1.12.08. As on 1.4.08 balance in profit and loss account – Rs. 15,000 and general reserve – Rs. 40,000. There were abnormal loss of Rs. 10,000 due to fire occurred in September, 08. There was abnormal gain of Rs. 5,000 in July, 08. There was a fire again in 1.1.09. Due to fire loss was Rs. 10,000 out of which insurance claim of Rs. 5,000 is received. Prepare consolidated balance sheet as on 31.3.09.

- 6. ADHISH SIR 6 Question: 12 Following are the Balance – sheet of H Ltd. and S Ltd. as on 31.3.2012: Liabilities H Ltd. S Ltd. Assets H Ltd. S Ltd. Equity share capital 1,00,000 80,000 Plant 1,00,000 90,000 Profit and loss account 1,30,000 40,000 Furniture 2,00,000 40,000 General reserve 70,000 10,000 Investment (70 % shares) 1,00,000 - Current liabilities 1,50,000 60,000 Current assets 50,000 60,000 4,50,000 1,90,000 4,50,000 1,90,000 Additional information: (i) Shares were purchased on 1.10.2011. (ii) Balance in profit and loss account and general reserve of S Ltd. was 18,000 and 4,000 on 1.4.2011. (iii) There was an abnormal loss of Rs. 3,000 on 1.5.2011 (iv) There was an abnormal gain of Rs. 1,800 on 1.1.2012. (v) Market value of plant and furniture as on 1.10.2011 was Rs. 1,20,000 and Rs. 70,000 respectively. (vi) Rate of depreciation on plant and furniture is 10 % and 20 % respectively. (vii) Group company decide to measure NCI at proportionate net asset method. Prepare consolidated Balance – sheet as on 31.3.2012. Question: 13 Balance – sheet as on 31.3.2009 Liabilities H Ltd. S Ltd. Assets H Ltd. S Ltd. Equity share capital 6,00,000 2,00,000 Plant and machinery 3,90,000 1,35,000 Profit and loss account 1,00,000 60,000 Furniture 80,000 40,000 General reserve 3,40,000 80,000 Investment in S Ltd. (80 % ) 3,40,000 - Creditors 70,000 35,000 Stock 1,80,000 1,20,000 Debtors 50,000 30,000 Cash at bank 70,000 50,000 11,10,000 3,75,000 11,10,000 3,75,000 (i) As on 1.4.08 balance of profit and loss account – `30,000 and general reserve – `80,000. (ii) Shares were acquired on 1.10.08. (ii) Plant and machinery of S Ltd. as on 1.4.08 `1,50,000 was considered worth `1,80,000 as on 1.10.08. (iv) Group Company decide to value NCI at fair value method. Prepare consolidated Balance – sheet as on 31.3.2009. Question: 14 The Balance –sheet of Small Limited as on 31.3.2020 was as under: Liabilities Amount (in lakhs) Assets Amount (In lakhs) Equity shares of `100 each 6.00 Land and building 4.00 General reserve 3.00 Machine (B/F) 3.50 Profit and loss account (on 1.4.2019) 1.20 Depreciation for the year 0.50 3.00 Profits for the year 0.60 Stock 2.00 Creditors 1.20 Debtors 1.50 Cash and bank balance 0.50 Preliminary expenses 0.50 12.00 12.00

- 7. ADHISH SIR 7 Big Limited purchased 4,000 equity shares of `100 each on 1st October, 2019 on which date it was found that land and building were undervalued by `1 lakh and machinery was worth only `2.75 lakhs. In preparing the consolidated Balance – sheet, it was decided to value NCI by using proportionate net asset method. Required: (a) Value of NCI on consolidation date (b) Goodwill / Bargain purchase Question: 15 Balance – sheet of P and S as on 30th June, 2008 are given below: P S I. Assets Non – current assets PPE 15,000 9,500 Investment 5,000 Current assets 7,500 5,000 27,500 14,500 II. Equity and Liabilities: Share capital (` 1 each) 6,000 5,000 Security premium 4,000 - Retained earnings 12,500 7,200 Non current liabilities 1,000 500 Current liabilities 4,000 1,800 27,500 14,500 P acquired 60 % of S on 1st July, 2007 when the retained earnings of S were `5,800. P paid `5,000 in cash. P also issued 2 shares for every 5 acquired in S and agreed to pay a further `2,000 in 3 years time. The market value of P’s shares at 1st July, 2007 was 1.80. P has only recorded the cash paid in respect of investment in S. Current interest rates are 6 %. P group company use fair value method to value the NCI. Fair value of NCI on acquisition date was ` 5,750. Prepare Consolidated Balance – sheet. Question: 16 Balance – sheet as on 31.3.2020 A B I. Assets Non – current assets PPE 25,00,000 20,00,000 Investment 5,00,000 Current assets: Cash and cash equivalent 16,00,000 3,00,000 Other current asset 5,00,000 4,00,000 51,00,000 27,00,000 II. Equity and Liabilities: Equity share capital (`10 each) 30,00,000 10,00,000 Other equity: Security premium 10,00,000 1,00,000 General reserve 2,00,000 1,00,000 Non – current liabilities 4,00,000 6,00,000 Current liabilities 5,00,000 9,00,000 51,00,000 27,00,000

- 8. ADHISH SIR 8 (i) On 31st March 2019, A Limited purchased 50,000 shares of BLimited and agreed to pay: (a) Cash of ` 3 per share (b) 3 shares for every 2 shares held (c) `60,000 after 3 years. Discount rate is 10 %. (d) ` 90,000, if EPS of A Limited is `20 after 3 years. Fair value of contingent consideration is ` 20,000. (ii) A Limited held 10,000 shares of B Limited on 31.3.2019, which were purchased for `19 per share. fair value of shares on 31.3.2019 for A Limited is ` 18. (iii) A Limited had not journalised entry for Purchases or revaluation of shares on 31.3.2019. Prepare Consolidated Balance – sheet . Question: 17 [CMA – Study Material] Prepare consolidated Balance – sheet of a group of P Limited, Q Limited and R Limited for which abstracts of Balance – sheets on 31.3.200x6 are given below. (` in lakhs) P Q R PPE 400 500 320 Investment in Q (80 %) 480 Investment in R (75 %) 300 Current assets: Inventory 250 80 60 Trade receivables 280 120 200 Bills receivables 70 50 Cash and bank 180 50 60 Total assets 1,660 1,050 690 Equity and Liabilities: Share capital (`10 each) 600 500 300 Other equity 460 160 120 Current liabilities: Trade payables 500 300 200 Bills payables 100 90 70 Total 1,660 1,050 690 Control was acquired on 30.9.20x5 the balances: Q R Other equity 100 50 (i) NCI is measured at fair value. (ii) Inventory of Q included 16 lakhs purchased from R at cost of 33.33 %. (iii) Bills receivables of R include 30 from P and Bills receivable of R includes 40 from Q. Question: 18 Prepare the consolidated Balance – sheet as on 31.3.2018 of a group of companies comprising Usha Limited, Nisha Limited and Sandhya Limited, their summarized balance – sheet on that date are given below: (` in Lakhs) Usha Limited Nisha limited Sandhya Limited I. Assets Non – current assets Tangible assets 160 180 150 Investment: 16 L shares in Nisha Limited 170 - -

- 9. ADHISH SIR 9 12 L shares in Sandhya Limited - 140 - Current assets: Cash in hand and at bank 114 20 20 Bills receivables 36 - 15 Trade receivables 130 50 110 Inventories 110 35 25 720 425 320 II. Equity and Liabilities Share capital (`10 each) 300 200 160 Reserves 90 50 40 Retained earnings 80 25 30 Current liabilities: Trade payables 235 115 90 Bills payable Usha Limited - 35 - Sandhya Limited 15 - - 720 425 320 The following additional information is available: (i) Usha Limited holds 80 % shares in Nisha Limited and Nisha Limited hold 75 % shares in Sandhya Limited. Their holdings were acquired on 30th September, 2017. (ii) The business activities of all the companies are not seasonal in nature and therefore, it can be assumed that profits are earned evenly throughout the year. (iii) On 1st April, 2017, the following balances stood in the books of Nisha Limited and Sandhya Limited Nisha Ltd. (` in lakhs) Sandhya Ltd. (` in lakhs) Reserves 40 30 Retained earnings 10 15 (iv) ` 5 Lakh included in the inventory figure of Nisha Ltd. which has been purchased from Sandhya Ltd. at cost plus 25 %. (v) The parent company has adopted an accounting policy to measure non – controlling interest at fair value (quoted market price) applying IND AS – 103. Assume prices of Nisha Limited and Sandhya Limited are the same as respective face values. (vi) The Capital profit preferably is to be adjusted against cost of control. Question: 19 Prepare the consolidated balance – sheet as on 31.3.20x2 of a group of companies comprising P Limited, S Limited and SS Limited. Their Balance – sheet on that date are given below: (` in lakhs) P S SS I. Assets Non – current assets PPE 320 360 300 Investment: 16 L shares in S Limited 340 - - 12 L shares in SS Limited - 280 - Current assets: Inventories 220 70 50

- 10. ADHISH SIR 10 Financial assets: Trade receivables 260 100 220 Bills receivables 72 - 30 Cash at bank 228 40 40 1440 850 640 II. Equity and Liabilities Share capital (`10 each) 600 400 320 Other equity Reserves 180 100 80 Retained earnings 160 50 60 Current Liabilities: Trade payables 470 230 180 Bills payable P Ltd. - 70 - SS Ltd. 30 - - 1440 850 640 The following additional information is available: (i) P Limited holds 80 % shares in S Limited and S Limited holds 75 % shares in SS Limited. Their holdings were acquired on 30th September, 20x1. (ii) The business activities of all the companies are not seasonal in nature and therefore, it can be assumed that profits are earned evenly throughout the year. (iii) On 1st April, 20x1 the following balances stood in the books of S and SS Limited. S Limited SS Limited Reserves 80 60 Retained earnings 20 30 (iv) `10 lakhs included in the inventories figure of S limited is inventory which has been purchased from SS Limited at cost plus 25 %. (v) The parent company has adopted an accounting policy to measure NCI at fair value (quoted market price) applying IND AS – 103. Assume market prices of S Limited and SS Limited are the same as respective face value. Question: 20 Below are the statements of financial position of three companies as at 31.12.20x9: B (` in 000) J (` in 000) G (` in 000) I. Assets: Non – current assets PPE 720 60 70 Investment in group companies 185 100 - Current assets 175 95 90 1,080 255 160 II. Equity and Liabilities Equity share capital (` 1) 400 100 50 Retained earnings 560 90 65 Current liabilities 120 65 45 1,080 255 160 You are given the following information: (i) B acquired 60 % of share capital of J on 1.1.20x2 and 10 % in G on 1.1.20x3. The cost of combinations were ` 1,42,000 and `43,000 respectively. J acquired 70 % of the share capital of G on 1.1.20x3.

- 11. ADHISH SIR 11 (ii) The retained earnings balances of J and G were: 1.1.20x2 1.1.20x3 J 45 60 G 30 40 (iii) It is the group policy to value NCI at acquisition at its proportionate share of fair value of subsidiary ‘s net asset. Prepare consolidated Balance – sheet of group company. Question: 21 Entity A acquired 60% of entity B two years ago for ` 6,000. At the time entity B’s fair value was ` 10,000. It had net assets with a fair value of ` 6,000 (which for the purposes of this example was the same as book value). Goodwill of ` 2,400 was recorded (being ` 6,000 – (60% * ` 6,000). On 1 October 20X0, entity A acquires a further 20% interest in entity B, taking its holding to 80%. At that time the fair value of entity B is ` 20,000 and entity A pays ` 4,000 for the 20% interest. At the time of the purchase the fair value of entity B’s net assets is ` 12,000 and the carrying amount of the non- controlling interest is ` 4,000. Pass journal entries to record the transaction. Question: 22 A Ltd. acquired 10% additional shares of its 70% subsidiary. The following relevant information is available in respect of the change in non-controlling interest on the basis of Balance sheet finalized as on 1.4.20X0: ` in thousand Separate financial statement: As on 31.3.20x0 Investment in subsidiary (70 % interest) – at cost 14,000 Purchase price for additional 10 % Interest 2,600 Consolidated financial statement: Non – controlling interest (30 %) 6,600 Consolidated profit and loss account 2,000 Goodwill 600 The reporting date of the subsidiary and the parent is 31 March, 20X0. Prepare note showing adjustment for change of non-controlling interest. Should goodwill be adjusted for the change? Question: 23 A ltd. acquired 70% of shares of B ltd. On 1.4.20X0 when fair value of net assets of B Ltd. was ` 200 lakh. During 20X0-20X1, B ltd. made profit of ` 100 lakh. Individual and consolidated balance sheets as on 31.3. 20X1 are as follows: (` in lakhs) A B Group Assets: Goodwill 10 PPE 627 200 827 Financial assets: Investment 150 Cash 200 30 230 Other current assets 23 70 93 1,000 300 1,160 Equity and Liabilities: Share capital 200 100 200 Other equity 800 200 870 Non – controlling interest 90 1,000 300 1,160

- 12. ADHISH SIR 12 A ltd. acquired another 10% stake in B ltd on 1.4. 20X1 at ` 32 lakh. The proportionate carrying amount of the non-controlling interest is ` 30 lakh. Show the consolidated balance sheet of the group immediately after the change in non-controlling interest. Question: 24 [CMA – Study Material - 15] DQ Limited acquired 60 % shares of RK Limited on 10.4.20017. Fair value of net assets at the time of acquisition was 3,00,000. In 2017 – 18 RK made a profit of 60,000. Individual and consolidated balance – sheet as at 31.3.2018: DQ RK Consolidated Goodwill 50,000 PPE 5,00,000 2,80,000 7,80,000 Investment in RK 2,30,000 Current assets 2,00,000 1,80,000 3,80,000 9,30,000 4,60,000 12,10,000 Equity share capital 4,00,000 2,00,000 4,00,000 Other equity 4,10,000 1,60,000 4,46,000 Non – controlling interest 1,44,000 Current Liabilities 1,20,000 1,00,000 2,20,000 9,30,000 4,60,000 12,10,000 On 1.4.2018 DQ acquired further 10 % shares of RK at 46,000. NCI is measured at proportionate carrying amount. Pass journal entry for change in holding and prepare separate and consolidated balance – sheet as at 1.4.2018. Question: 25 [CMA – Study Material] Company P Ltd. (a listed company) acquires 60% shares in company Q Ltd. on 1-4-17 at a cost of (` Lakhs) 1,38,000, paid by issue of shares of ` 10 at par, when fair value of identifiable net assets of Q was (` Lakhs) 2,20,000. The abstract of balance sheets of Q (along with fair values at the acquisition date) and P at the beginning and at the end of the year are as follows: (a) Pass journal entries in consolidated accounts of P and show consolidated balance sheet of P on 1-4-17 based on Ind AS 103 and Ind AS 110. (b) Prepare consolidated balance sheet and separate balance sheet of P on 31-3-18 based on Ind AS 110. Question: 26 [CMA – Study Material] Company P Ltd. acquires 60% shares of company S Ltd. on 1/4/17 by issue of equity shares at fair value of 360, paid up value 100. The book values and fair values of the assets and liabilities of the companies at the

- 13. ADHISH SIR 13 date of acquisition and at the end of the year are stated below. The total comprehensive income of P and S in the year ending 31-03-2018 amounted to 60 and 70 respectively. (` Lakhs) Pass entries for business combination under acquisition method and prepare CBS on 1-4-17 and on 31-3-18. Question: 27 [CMA – Study Material] X Ltd. acquires 80% of equity of Y Ltd. on 31-03-20x3 at cost of (` Lakhs) 100, when the Equity Share Capital and Other Equity of Y Ltd. were 40 and 80 respectively. For the years ending on 31-03-20x4 and 31-03-20x5, Y Ltd accounted Total Comprehensive income of (15) and 25. Find NCI (Proportionate Net Asset Method), X Ltd’s share in post-acquisition profits of Y Ltd. and Goodwill to be shown in CFS of X Ltd. at the end of the years. Question: 28 [CMA – Study Material] Z Ltd. purchased 80% shares in C Ltd. on 1-10-20x1 at 240000. C Ltd. at 31-03-20x1 had Issued Share Capital 200000 and Other Equity 60000. For year ending on 31-03-20x2 C Ltd. made profits 30000 and declared dividend 40000. Other information: A. NCI measured at fair value. or B. NCI measured at proportionate net assets. Or C. On the date of acquisition fair value of identified net assets measured at 250000 and NCI measured (I) at fair value; (II) at proportionate net assets value. For each of A, B and C: (a) (i) Find NCI on date of acquisition and on 31-03-20x2. (ii) Find Goodwill and (iii) pass journal entry (in consolidated accounts). (b) Pass journal entries for Separate financial statements. (c) Show relevant parts in Consolidated Balance sheet and Separate Balance Sheet Question: 29 H Limited acquired 80 % equity shares of S Limited on 1.4.2019 and agreed to pay: (a) Immediate cash payment of `5,00,000. (b) 2 shares for every 4 shares held at a fair value of `14. (c) ` 3,00,000 after 2 year’s time. Appropriate discount rate is 12 %. Financial position of both the companies on 31.3. 2020 were as under: Particulars H S I. Assets Non current assets 12,00,000 10,00,000 Investments 5,00,000 Current assets 8,00,000 5,00,000 25,00,000 15,00,000 II. Equity and Liabilities: Equity share capital (`10 each) 10,00,000 8,00,000 Profit and loss account 3,00,000 1,48,000 General reserve 2,00,000 1,52,000

- 14. ADHISH SIR 14 Non current liabilities 7,00,000 2,25,000 Current liabilities 3,00,000 1,75,000 25,00,000 15,00,000 Additional information: (a) Balances of reserves of S Limited on 1.4.2019 were: Profit and loss account - `80,000 General reserve - ` 50,000 (b) Consideration in form of shares and deferred consideration have not yet been recorded. (c) Group company decided to measure NCI at proportionate NA method. Prepare Consolidated Balance – sheet as on 31.3.2020 Question: 30 Yati Limited acquired 75 % Equity interest of Dishita Limited on 1.4.2019 and agreed to pay: (a) Immediate cash payment of `2,25,000 (b) 1 share for every 2 shares held at a fair value of `12. (c) Cash payment of `1,25,000 in 2year’s time. Appropriate discount rate is 10 %. Financial position of both the companies on 31.3.2020 were as under: Yati Dishita I. Assets Non – current assets: PPE 10,00,000 7,20,000 Furniture 2,00,000 1,70,000 Investment 2,25,000 Current assets: Debtors 2,00,000 1,50,000 Stock 3,00,000 1,70,000 Other current assets 3,75,000 2,30,000 23,00,000 14,40,000 II. Equity and Liabilities: Equity share capital (` 10 each) 10,00,000 8,00,000 Profit and loss account 2,00,000 1,32,000 General reserve 1,50,000 96,000 Securities premium 1,00,000 50,000 Non – current liabilities 6,35,000 2,75,000 Current liabilities 2,15,000 87,000 23,00,000 14,40,000 Additional information: (a) Balances of reserves of Dishita Limited as on 1.4.2019 were: Profit and loss account = 84,000 General reserve = 72,000 (b) Consideration in form of shares and deferred consideration have not yet been recorded. (c) Yati Limited revalue assets of Dishita Limited as under: PPE - `8,40,000 Furniture - `1,75,000 (d) Dishita Limited follow SLM of depreciation for non – current assets. Rate of depreciation is 10 % for PPE and 15 % for Furniture.. (e) There was a fire in premises of Dishita Limited on 1.7.2019 and due to fire loss of ` 15,000 occurred. (f) Yati Group company decide to measure NCI by using proportionate net asset method. Prepare Consolidated Balance – sheet.

- 15. ADHISH SIR 15 Question: 31 Balance –sheet as on 31.3.2017 Liabilities H Limited S Limited Assets H Limited S Limited Equity share capital 12,00,000 8,00,000 Non – current assets 12,00,000 8,00,000 General reserve 4,00,000 3,00,000 Investment in S Limited (70 %) 7,25,000 - Profit and loss account 3,00,000 2,00,000 Current assets 2,60,000 7,30,000 10 % Debentures 1,50,000 1,00,000 Fictitious assets 15,000 20,000 Current liabilities 1,50,000 1,50,000 22,00,000 15,50,000 22,00,000 15,50,000 Additional information: (i) Shares were purchased by H Limited on 1.10.2016. (ii) Balances of reserves of S Limited on 1.4.2016 were: Profit and loss account - `1,20,000 General reserve - `1,00,000 (iii) There was an abnormal loss of `12,000 on 1.4.2016 and abnormal gain of `15,000 on 1.1.2017. (iv) Non – current asset of S Limited were revalued at ` 9,52,000. Rate of depreciation is 20 % on SLM. (v) H Limited incurred `500 per month towards an expense on behalf of S Limited and debited the same to the profit and loss account. No rectification entries has been passed. Prepare consolidated balance – sheet. Question: 32 On 1st October,2009 Poddar Ltd. acquired 12,000 equity shares of Bhansali Ltd. of the face value of `10 each at a price of `1,70,000. The balance sheet of two companies as on 31st March, 2010 are as follows: Liabilities Poddar Ltd. Bhansali Ltd. Assets Poddar Ltd. Bhansali Ltd. Equity shares of Rs. 10 each 10,00,000 2,00,000 Goodwill 3,00,000 70,000 General reserve (1.4.09) 4,20,000 1,00,000 Land and building 4,00,000 1,00,000 Profit and loss account (1.4.09) 90,000 40,000 Plant and machinery 5,00,000 1,00,000 Profit for the year 1,70,000 45,000 Stock 2,00,000 40,500 Creditors 2,40,000 92,000 Debtors 3,00,000 1,34,500 Bills payable 80,000 60,000 Investment 2,00,000 - Bills receivables 20,000 30,000 Bank 60,000 50,000 Cash 20,000 12,000 20,00,000 5,37,000 20,00,000 5,37,000 Out of the debtors and bills receivable of Poddar Ltd. Rs. 50,000 and Rs. 16,000 respectively represented those due from Bhansali Ltd. The stock in the hands of Bhanslai Ltd. includes goods purchased from Poddar Ltd. at Rs. 20,000 which includes profit charged by latter company @ 25 % at cost. Prepare a consolidated balance sheet as on 31st March, 2010 and also show your workings. Question: 33 Balance – sheet as on 31.3.2017 Liabilities H Ltd. S Ltd. Assets H Ltd. S Ltd. Equity share capital 12,00,000 8,00,000 Fixed assets 12,00,000 8,10,000 General reserve 5,00,000 4,00,000 Investment in shares (70 %) 6,85,000 - Profit and loss account 4,00,000 2,00,000 Investment in 1,15,000 -

- 16. ADHISH SIR 16 debentures (1000 debentures) 10 % Debentures 3,00,000 1,00,000 Debtors 80,000 50,000 Creditors 1,20,000 40,000 Bills receivables 70,000 50,000 Bills payables 80,000 60,000 Stock 2,00,000 1,00,000 Cash 2,30,000 5,75,000 Preliminary expenses 20,000 15,000 26,00,000 16,00,000 26,00,000 16,00,000 (i) Shares were acquired on 1.10.2016. (ii) Balances of reserves of S Ltd. are as under General reserve - `1,00,000 Profit and loss account - `1,20,000 (iii) There was abnormal loss of `15,000 due to fire on 1.7.2016. (iv) H Limited revalued fixed asset of S Limited on 1.10.2016 as `9,85,000. S Limited followed straight line method of depreciation. Rate of depreciation is 10 %. (v) Bills payable of S Limited includes bills worth `20,000 drawn by H Limited out of which H Limited discounted bills of `4,000 and endorsed `2,000. (vi) Creditors of S Limited includes `15,000 in respect of goods purchased from HLimited. (vii) H Limited sold goods of `15,000 at a profit of 20 % on cost. At the year end, 80 % of goods were unsold with S Limited. Prepare consolidated balance – sheet as on 31.3.2017. Question: 34 [Adopted - ACCA] P Co regularly sells goods to its one subsidiary company, S Co, which it has owned since S Co's incorporation. The statement of financial position of the two companies on 31 December 20X6 are given below. STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 20X6 P Co. S Co. I. Assets Non – current assets Property, plant and equipment 35,000 45,000 Investment in 40,000 shares of `1 each in S at cost 40,000 - Current assets: Inventories 16,000 12,000 Receivables: S Co. 2,000 - Other receivables 6,000 9,000 Cash at bank 1,000 - 1,00,000 66,000 II. Equity and Liabilities: Share capital of `1 each 70,000 40,000 Retained earnings 16,000 19,000 Current Liabilities: Bank overdraft - 3,000 Payables: P Co. 2,000 Other payables 14,000 2,000 1,00,000 66,000 Required Prepare the consolidated statement of financial position of P Co at 31 December 20X6.

- 17. ADHISH SIR 17 Question: 35 [Adopted - ACCA] The statements of financial position of P Co and of its subsidiary S Co have been made up to 30 June. P Co has owned all the ordinary shares and 40% of the loan stock of S Co since its incorporation. STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE P Co S Co. I. Assets Non – current assets PPE 1,20,000 1,00,000 Investment in S Co at cost: 80,000 Equity shares @ ` 1 80,000 20,000 of 12 % loan stock in S Co. 20,000 Current assets: Inventories 50,000 60,000 Receivables 40,000 30,000 Current account with S 18,000 Cash 4,000 6,000 Total 3,32,000 1,96,000 II. Equity and Liabilities: Equity share capital of ` 1 each 1,00,000 80,000 Retained earnings 95,000 28,000 Non – current liabilities: 10 % Loan stock 75,000 12 % Loan stock 50,000 Current liabilities: Payables 47,000 16,000 Taxation 15,000 10,000 Current account with P Co. 12,000 3,32,000 1,96,000 The difference on current account arises because of goods in transit. Required: Prepare the consolidated statement of financial position of P Co. Question: 36 [Adopted - ACCA] Statement of Financial position on 31.3 .2015 Teddy Limited Bear Limited I. Assets: Non – current assets PPE 12,50,000 4,50,000 Investment in Bear Limited 4,50,000 - Current assets: Inventory 1,25,000 25,000 Receivables 1,30,000 90,000

- 18. ADHISH SIR 18 Cash 89,000 1,00,000 20,44,000 6,65,000 II. Equity and Liabilities: Equity share capital (`1 each ) 5,00,000 1,00,000 Securities premium 25,000 50,000 Retained earnings 10,96,000 3,66,000 Non – Current liabilities: Loan 3,20,000 50,000 Current Liabilities: Trade payables 78,000 89,000 Tax 25,000 10,000 20,44,000 6,65,000 The Following information is also available: (a) Teddy Limited acquired 75,000 shares of Bear Limited on 1st April, 2013 and at that date the retained earnings of Bear Limited was ` 2,50,000. (b) At acquisition, the fair value of Bear’s Limited PPE was 95,000 above book value. This has not been reflected in the financial statement. The additional depreciation on this would be 3,000 per year. (c) Teddy Limited is accounting for NCI by valuing it at fair value. The fair value of goodwill attributable to NCI is `18,250. (d) Included with in the receivables of Teddy Limited is 45,000 that is owed by Bear Limited. (e) At the year end the directors decide that the goodwill relating to Bear Limited needs to be impaired by 35,000. Prepare Consolidated Balance – sheet. Question: 37 [Adopted - ACCA] Alpha Company purchased 14,50,000 shares in Beta Co. in 20X0 when the reserves stood at `4,00,000 and there was no retained earnings. The statement of financial position of the two companies as at 31.12.20X4 are as under: Alpha (‘000) Beta (‘000) I. Assets Non – current assets: PPE 8,868 1,787 Investment in Beta Limited at cost 1,450 - Current assets: Inventories 1,983 1,425 Receivables 1,462 1,307 Cash 25 16 13,788 4,535 II. Equity and Liabilities: Equity share capital (`0.50 each) 5,500 1,000 General reserve 1,200 800 Retained earnings 485 100 Non – Current liabilities: 10 % borrowings 4,000 - 15 % Borrowings - 500 Current Liabilities:

- 19. ADHISH SIR 19 Bank overdraft 1,176 840 Trade payables 887 1,077 Taxation 540 218 13,788 4,535 (i) At the end of reporting period the current account of Alpha with Beta was agreed at `23,000 owed by Beta. This account is included in receivables and payables. (ii) It is the group policy to value the NCI at its proportionate share of fair value of subsidiary’s net assets. Required: Prepare Consolidated Balance – sheet. Question: 38 [Adopted - ACCA] You are provided with the following statements of financial position of S and M S (` ‘000) M (` ‘000) I. Assets Non current assets: Plant 325 70 Fixtures 200 50 Investment in shares of M Limited at cost 200 - Current assets: Inventory 220 70 Receivables 145 105 Bank 100 - 1,190 295 II. Equity and Liabilities: Equity share capital (` 1) 700 170 Retained earnings 215 50 Current Liabilities: Payables 275 55 Bank overdraft - 20 1,190 295 The following information is also available: (i) S Purchased 70 % of the issued share capital of M, four years ago, when the retained earnings of M were `20,000. (ii) For the purpose of the acquisition Plant of M with a book value of `50,000 was revalued to its fair value of `60,000. The revaluation was not recorded in the accounts of M. Depreciation is charged at 20 % using SLM. (iii) S sell goods to M at a mark – up of 25 %. At the year end, the inventories of M include `45,000 of goods purchased from S. (iv) M owes S ` 35,000 for goods purchased and S owes M ` 15,000. (v) It is the group policy to value NCI at fair value. (vi) The market price of the shares of M before acquisition was `1.50. Prepare Consolidated Balance – sheet of S. Question: 39 [ACCA - Adopted] P Co has owned 75% of the share capital of S Co since the date of S Co's incorporation. Their latest statements of financial position are given below. Statement of financial position P Co. S Co. I. Assets: Non – current assets Property, plant and equipment 50,000 35,000 30,000 ` 1 ordinary shares in S Co. at cost 30,000 -

- 20. ADHISH SIR 20 Current assets 45,000 35,000 1,25,000 70,000 II. Equity and Liabilities: `1 Equity shares 80,000 40,000 Retained earnings 25,000 10,000 Current liabilities 20,000 20,000 1,25,000 70,000 Required Prepare the consolidated statement of financial position. Question: 40 [Adopted - ACCA] Sing Co acquired the ordinary shares of Wing Co on 31 March when the draft statements of financial position of each company were as follows. SING CO STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH I. Assets: Non – current assets: Investment in 50,000 shares of Wing Co. at cost 80,000 Current assets 40,000 1,20,000 II: Equity and Liabilities: Equity share capital (`1 each) 75,000 Retained earnings 45,000 1,20,000 WING CO STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH Current assets 60,000 60,000 Equity share capital (` 1 each) 50,000 Retained earnings 10,000 60,000 Prepare the consolidated statement of financial position as at 31 March. Question: 41 [Adopted - ACCA] The draft statements of financial position of Ping Co and Pong Co on 30 June 20X8 were as follows. STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 20X8 Ping Co. Pong Co. I. Assets: Non – current assets: PPE 50,000 40,000 20,000 equity shares in Pong Co. at cost 30,000 - Current assets: Inventory 3,000 8,000 Owed by Ping Co. - 10,000 Receivables 16,000 7,000 Cash 2,000 - 1,01,000 65,000

- 21. ADHISH SIR 21 II. Equity and Liabilities: Equity share capital (` 1 each) 45,000 25,000 Revaluation surplus 12,000 5,000 Retained earnings 26,000 28,000 Current Liabilities: Owed to Pong Co. 8,000 - Trade payables 10,000 7,000 1,01,000 65,000 Ping Co acquired its investment in Pong Co on 1 July 20X7 when the retained earnings of Pong Co stood at `6,000. The agreed consideration was `30,000 cash and a further `10,000 on 1 July 20X9. Ping Co's cost of capital is 7%. Pong Co has an internally-developed brand name – 'Pongo' – which was valued at `5,000 at the date of acquisition. There have been no changes in the share capital or revaluation surplus of Pong Co since that date. At 30 June 20X4 Pong Co had invoiced Ping Co for goods to the value of `2,000 which had not been received by Ping Co. There is no impairment of goodwill. It is group policy to value non-controlling interest at full fair value. At the acquisition date the non-controlling interest was valued at `9,000. Prepare the consolidated statement of financial position of Ping Co as at 30 June 20X8. Question: 42 [Adopted - ACCA] P Co acquired 80% of the shares in S Co one year ago when the reserves of S Co stood at $10,000. Draft statements of financial position for each company are as follows. P Co. S Co. I. Assets: Non – current assets PPE 80,000 40,000 Investment in S Co. 46,000 - Current assets 40,000 30,000 1,66,000 70,000 II. Equity and Liabilities: Equity shares of `1 each 1,00,000 30,000 Retained earnings 45,000 22,000 Current Liabilities 21,000 18,000 1,66,000 70,000 During the year S Co sold goods to P Co for `50,000, the profit to S Co being 20% of selling price. At the end of the reporting period, `15,000 of these goods remained unsold in the inventories of P Co. At the same date, P Co owed S Co `12,000 for goods bought and this debt is included in the trade payables of P Co and the receivables of S Co. Non-controlling interest is valued at full fair value. It was valued at `9,000 at the date of acquisition. Required: Prepare a draft consolidated statement of financial position for P Co. Question: 43 [Adopted - ACCA] P Co has owned 75% of the shares of S Co since the incorporation of that company. During the year to 31 December 20X2, S Co sold goods costing `16,000 to P Co at a price of `20,000 and these goods were still unsold by P Co at the end of the year. Draft statements of financial position of each company at 31 December 20X2 were as follows. P Co. S Co. I. Assets Non – Current assets PPE 1,25,000 1,20,000 Investment: 75,000 shares in S Co. at cost 75,000 -

- 22. ADHISH SIR 22 Current assets: Inventories 50,000 48,000 Receivables 20,000 16,000 2,70,000 1,84,000 II. Equity and Liabilities: Equity share capital (` 1 each) 80,000 1,00,000 Retained earnings 1,50,000 60,000 Current Liabilities 40,000 24,000 2,70,000 1,84,000 Required: Prepare the consolidated statement of financial position of P Co at 31 December 20X2. The fair value of the non-controlling interest at acquisition was `25,000. Question: 44 [Adopted - ACCA] Hinge Co acquired 80% of the ordinary shares of Singe Co on 1 April 20X5. On 31 December 20X4 Singe Co's accounts showed a share premium account of `4,000 and retained earnings of `15,000. The statements of financial position of the two companies at 31 December 20X5 are set out below. Neither company has paid any dividends during the year. Non-controlling interest should be valued at full fair value. The market price of the subsidiary's shares was `2.50 prior to acquisition by the parent. You are required to prepare the consolidated statement of financial position of Hinge Co at 31 December 20X5. There has been no impairment of goodwill. STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 20X5 HINGE CO. SINGE CO. I. Assets: Non – current assets: PPE 32,000 30,000 16,000 equity shares of ` 0.50 each 50,000 - Current assets 85,000 43,000 1,67,000 73,000 II. Equity and Liabilities: Equity shares of `1 each 1,00,000 Equity shares of ` 0.50 each 10,000 Securities premium account 7,000 4,000 Retained earnings 40,000 39,000 Current liabilities 20,000 20,000 1,67,000 73,000 Question: 45 [Adopted - ACCA] P Co acquired 75% of the ordinary shares of S Co on 1 September 20X5. At that date the fair value of S Co's non-current assets was `23,000 greater than their net book value, and the balance of retained earnings was `21,000. The statements of financial position of both companies at 31 August 20X6 are given below. S Co has not incorporated any revaluation in its books of account. Non-controlling interest is valued at full fair value which was deemed to be `18,000 at the acquisition date. STATEMENT OF FINANCIAL POSITION AS AT 31 AUGUST 20X6 P Co. S Co. I. Assets: Non – current assets PPE 63,000 28,000 Investment in S at cost 51,000 -

- 23. ADHISH SIR 23 Current assets 82,000 43,000 1,96,000 71,000 II. Equity and Liabilities: Equity shares of ` 1 80,000 20,000 Retained earnings 96,000 41,000 Current Liabilities 20,000 10,000 1,96,000 71,000 If S Co had revalued its non-current assets at 1 September 20X5, an addition of `3,000 would have been made to the depreciation charged for 20X5/X6. Required Prepare P Co's consolidated statement of financial position as at 31 August 20X6. Question: 46 [Work book of CMA] Following are the abstracts of balance sheets of two companies A and B when A acquired control of B. Amounts are in ` crores. A acquired 80% shares of B at 720, paid by shares issued at par. Fair Value of PPE is 640 and Current Assets 580. • Pass journal entries in the books of A (a. for consolidated accounts and b. for separate financial statements) and B for the business combination. • Prepare Separate Balance Sheet and Consolidated Balance Sheet after business combination. Question: 47 [Work book of CMA] Following are the abstracts of balance sheets of two companies A and B when A acquired control of B. Amounts are in ` crores. A acquired 80% shares of B at 640, paid by shares of ` 10 issued at ` 25. 12% Debentures of A were issued in exchange of Debentures of B. Fair Value of PPE is 640 and Current Assets 580 (of B).

- 24. ADHISH SIR 24 • Pass journal entries in the books of A (for consolidated accounts) and B for the business combination. NCI is recognized at proportionate to net assets. • Prepare Consolidated Balance Sheet after business combination. Question: 48 [Work book of CMA] X holds 20% shares of B on 1-2-20X1 at a cost of `80000. On 01-04-20X1 X further acquires 60% shares of B at a consideration of 560000 in cash and by issue of 10000 shares of ` 10 (market price). Non-Controlling Interest is recognized at ` 120000. The fair value of shares previously held in B amounts to ` 120000. The fair values of assets and liabilities of B are stated below: The abstracts of separate balance sheet of A and individual balance sheet of B on 31-03-20X1 are given below: Pass journal entries in the books of A for business combination and show the consolidated balance sheet. Question: 49 [Work book of CMA] X Ltd. acquires 20% shares of B Ltd. on 01-04-20X1. X Ltd. further acquires on 01-04-20x2 60% shares of B Ltd. at a consideration of `3,60,000 in cash and by issue of 10000 shares of ` 10 (market price `15). Debentures of B Ltd. are exchanged for 12% Debenture of X Ltd. A contingent consideration is also payable, fair value of which at the date of acquisition is estimated at `60,000. A pays transaction cost ` 20000. Non-Controlling Interest is recognized at `1,20,000. The fair value of shares previously held in B Ltd. amounts to `1,10,000. The fair values of assets and liabilities of B Ltd. are stated below: The abstracts of consolidated balance sheet of A and individual balance sheet of B on 31-03-20X2 are given below:

- 25. ADHISH SIR 25 Pass journal entries in the books of X Ltd. for business combination and show the Separate and Consolidated balance sheet as at 1-04-20X2. Question: 50 [Work book of CMA] P Ltd. shares are quoted at ` 20 and Q Ltd. shares are quoted at ` 60. P Ltd. issues shares for acquiring all the shares of Q Ltd. in the exchange ratio based on the quoted price. The statement of financial position immediately before business combination: Fair value of assets and liabilities at the acquisition date:

- 26. ADHISH SIR 26 Pass journal entries for business combination and show consolidated balance sheet of the group. Question: 51 [Work book of CMA] The financial data of the companies P and S at 31-3-2017 and at 31-3-2018 are stated below. Prepare Consolidated Balance Sheet. Question: 52 [Work book of CMA] Company Sky Ltd. (a listed company) acquires 60% shares in company Cloud Ltd. on 1-4-17 at a cost of (`Lakhs) 150000, paid by issue of shares of ` 10 (market price ` 25). The abstract of balance sheets of Cloud (along with fair values at the acquisition date) and Sky at the end of the year 2016-17 and 2017-18 are as follows:

- 27. ADHISH SIR 27 (a) Pass journal entries in consolidated accounts of P and show consolidated balance sheet on 1-4-17 based on Ind AS 103 and Ind AS 110 and separate balance sheet of P on 01-04-17 based on Ind AS 27. (b) Prepare consolidated balance sheet of P on 31-3-18 based on Ind AS 110. Question: 53 [Work book of CMA] X Ltd. acquires 80% of equity of Y Ltd. on 31-03-20x5 at cost of (` Lakhs) 110, when the Equity Share Capital and Other Equity of Y Ltd. were 40 and 80 respectively. For the years ending on 31-03-20x6 and 31-03-20x7, Y Ltd accounted Total Comprehensive income of (15) and 25. Recognise NCI at Proportionate Net Asset Mesure. X Ltd’s share in post-acquisition profits of Y Ltd. and Goodwill to be shown in CFS of X Ltd. at the end of the years. The revaluation profit/loss for the difference between fair value and carrying amount of assets and liabilities of Y Ltd. at acquisition date and the abstracts of separate balance sheet of X Ltd. and individual balance sheet of Y Ltd. as at 31-03-20x8 are as follows: Prepare the consolidated balance sheet at 31-03-20X8.

- 28. ADHISH SIR 28 Question: 54 [Work book of CMA] P acquires 60% shares in Q on 1- 10 - 2017 at 30000. Q makes profits 20000 in the year 20X7-X8 and declared dividend 9000. NCI is valued at proportionate net assets. Abstracts of Separate Balance Sheet of P (Dividend from subsidiary not accounted) and Individual Balance Sheet of Q as at 31-03-20X8: Show Consolidated Balance Sheet and Separate Balance Sheet of P. Question: 55 [Work book of CMA] On 1-4-x6 BB Ltd. acquired 90% share of CM Ltd. at 1080000, when the fair value of its net assets was 1000000. During 1-4-x6 to 31-3-x7 CM Ltd made TCI 200000. On that date BM sold 15% holding to outsiders at 220000. Pass journal entries for sale of partial holding retaining control. Question: 56 [CA – STUDY MATERIAL] A Ltd. acquired 70% of equity shares of B Ltd. on 1.04.20X1 at cost of ` 10,00,000 when B Ltd. had an equity share capital of ` 10,00,000 and other equity of ` 80,000. In the four consecutive years B Ltd. fared badly and suffered losses of ` 2,50,000, ` 4,00,000, ` 5,00,000 and ` 1,20,000 respectively. Thereafter in 20X5 - 20X6, B Ltd. experienced turnaround and registered an annual profit of ` 50,000. In the next two years i.e. 20X6-20X7 and 20X7-20X8, B Ltd. recorded annual profits of ` 1,00,000 and ` 1,50,000 respectively. Show the non- controlling interests and goodwill at the end of each year for the purpose of consolidation. Assume that the assets are at fair value. Question: 57 [CA – STUDY MATERIAL] On 31 March 20X2, Blue Heavens Ltd. acquired 100% ordinary shares carrying voting rights of Orange County Ltd. for Rs. 6,000 lakh in cash and it controlled Orange County Ltd. From that date. The acquisition- date statements of financial position of Blue Heavens Ltd. And Orange County Ltd. and the fair values of the assets and liabilities recognised on Orange County Ltd. statement of financial position were:

- 29. ADHISH SIR 29 Prepare the Consolidated Balance Sheet as on March 31, 20X2 of group of entities Blue Heavens Ltd. and Orange County Ltd. Question: 58 [CA – Study material] The facts are the same as in Question 57 above. However, Blue Heavens Ltd. acquires only 75% of the ordinary shares, to which voting rights are attached of Orange County Ltd. Blue Heavens Ltd. pays Rs. 4,500 lakhs for the shares. Prepare the Consolidated Balance Sheet as on March 31, 20X2 of group of entities Blue Heavens Ltd. and Orange County Ltd. Question 59 ABC acquired 75% of the equity interest in XYZ at 1 January 2017 for Rs. 50 million. The Statement of Financial Position as at 1 January 2017 were as follows: ABC (`000) XYZ (`000) I. Assets Non – current assets: PPE 30,000 35,000 Investment in XYZ 50,000 - Current assets 45,000 35,000 Total 1,25,000 70,000 II. Equity and Liabilities: Equity share capital 80,000 40,000 Retained earnings 25,000 10,000 Current liabilities 20,000 20,000

- 30. ADHISH SIR 30 Total 1,25,000 70,000 Additional information. (1) At the date of acquisition all the assets and liabilities of XYZ PLC were reflected at fair value except land which had a fair value of Rs.5,000,000 in excess of its carrying amount. (2) ABC Group measures the NCI at its proportionate share of the acquiree’s net identifiable assets. Required: Prepare the Consolidated Statement of Financial Position as at 1 January 2017. Question: 60 Assume all the information in the above question 59 is same except NCI is measured at its fair value as at 1 January 2017. The market value per share as at 1 January 2017, was Rs.1.50. Required: Prepare the Consolidated Statement of Financial Position as at 1 January 2017. Question: 61 [IFRS – Diploma - Adopted] ABC acquired 75% of the equity interest in XYZ at 1 January 2017 for Rs. 50 million. The Statement of Financial Position as at 31 March 2018 were as follows: ABC (`000) XYZ (`000) I. Assets Non – current assets PPE 35,000 25,000 Investment in XYZ 50,000 Current assets: Inventory 10,000 5,000 Receivables 30,000 20,000 Cash 10,000 10,000 Total 1,35,000 60,000 II. Equity and Liabilities: Equity share capital of ` 1 80,000 40,000 Retained earnings 35,000 15,000 Current Liabilities 20,000 5,000 Total 1,35,000 60,000 Additional information. (1) At the date of acquisition all the assets and liabilities of XYZ PLC were reflected at fair value except land which had a fair value of Rs.5,000,000 in excess of its carrying amount. (2) The retained earnings at the date of acquisition was Rs. 10,000,000 (3) ABC Group measures the NCI at its proportionate share of the acquiree’s net identifiable assets. (4) During the year ended 31 March 2018, XYZ Purchased Rs.1,000,000 worth of goods from ABC. Out of these goods half (1/2) of them remained unsold in the premises of company XYZ. The sales policy of ABC is to add 25% of mark up to its cost. (5) During the year ended 31 March 2018, ABC Purchased Rs.1,500,000 worth of goods fromXYZ.Out of these goods one third (1/3) of them remained unsold in the premises of company ABC. The sales policy of XYZ is to keep 25% margin from sales price. (6) On 1 April 2017, XYZ sold a motor vehicle to ABC for Rs.600,000, the carrying amount of the motor vehicle at the date of sale stood at Rs.400,000. The remaining useful life of motor vehicle at the date of sale was 4 years. (7) As at 31 March 2018, the intra group receivables stood at Rs.1,000,000 and group payables stood at

- 31. ADHISH SIR 31 Rs.800,000. The difference was due to the cash in transit. (8) As at 31 March 2018, goodwill had been impaired by Rs.750,000. Required: Prepare the Consolidated Statement of Financial Position as at 31 March 2018. Question: 62 [CA – Study Material] P Pvt. Ltd. has a number of wholly-owned subsidiaries including S Pvt. Ltd. at 31st March 20X2. P Pvt. Ltd. consolidated statement of financial position and the group carrying amount of S Pvt. Ltd. assets and liabilities (ie the amount included in that consolidated statement of financial position in respect of S Pvt. Ltd. assets and liabilities) at 31st March 20X2 are as follows: Prepare consolidated Balance Sheet after disposal as on 31st March, 20X2 when P Pvt. Ltd group sold 100% shares of S Pvt. Ltd. to independent party for Rs. 3,000 millions. Question: 63 Reliance Ltd. has a number of wholly-owned subsidiaries including Reliance Jio Infocomm Ltd. at 31st March 20X2. Reliance Ltd. consolidated statement of financial position and the group carrying amount of Reliance Jio Infocomm Ltd. assets and liabilities (ie the amount included in that consolidated statement of financial position in respect of Reliance Jio Infocomm Ltd. assets and liabilities) at 31st March 20X2 are as follows:

- 32. ADHISH SIR 32 Prepare consolidated Balance Sheet after disposal as on 31st March, 20X2 when Reliance Ltd. group sold 90% shares of Reliance Jio Infocomm Ltd. to independent party for Rs. 1000 thousand.

- 33. ADHISH SIR 33 Question: 64 [CA – May, 2018] Hold Limited acquired 100% ordinary shares of Rs. 100 each of Sub Limited on 1st October, 2017. On 31st March, 2018 the summarized Balance Sheets of the two companies were as given below: The retained earnings of Sub Limited showed a credit balance of Rs. 6,00,000 on 1st April, 2017 out of which a dividend of 10% was paid on 1st November 2017. Hold Limited has credited the dividend received to retained earnings account. There was no fresh addition to other reserves in case of both companies during the current financial year. There was no opening balance in the retained earnings in the books of Hold Limited. Following are the changes in fair value as per respective Ind AS from the book value as on 1st October, 2017 in the books of Sub Limited which is to be considered while consolidating the Balance Sheets. (i) Fair value of Plant and Machinery was Rs. 40,00,000. (Rate of depreciation on Plant and Machinery is 10% p.a.) (ii) Land and Building appreciated by Rs. 20,00,000. (iii) Inventories increased by Rs. 3,00,000. (i) Fair value of Plant and Machinery was Rs. 40,00,000. (Rate of depreciation on Plant and Machinery is 10% p.a.) (ii) Land and Building appreciated by Rs. 20,00,000. (iii) Inventories increased by Rs. 3,00,000. (iv) Trade payable increased by Rs. 2,00,000. Prepare Consolidated Balance Sheet as on 31st March, 2018. The Balance Sheet should comply with the relevant lnd AS and Schedule III of the Companies Act, 2013.

- 34. ADHISH SIR 34 Question: 65 [CA – May, 2019] Summarised Balance Sheets of PN Ltd. and SR Ltd. as on 31st March, 2018 were given as below: (Amount is Rs.) (i) PN Ltd. acquired 70% equity shares of Rs. 100 each of SR Ltd. on 1st October, 2017. (ii) The Retained Earnings of SR Ltd. showed a credit balance of Rs. 93,600 on 1st April, 2017 out of which a dividend of 12% was paid on 15th December, 2017. (iii) PN Ltd. has credited the dividend received to its Retained Earnings. (iv) Fair value of Plant & Machinery of SR Ltd. as on 1st October, 2017 was Rs. 6,24,000. The rate of depreciation on Plant & Machinery was 10% p.a. (v) Following are the increases on comparison of Fair Value as per respective Ind AS with book value as on 1st October, 2017 of SR Ltd. which are to be considered while consolidating the Balance Sheets: (a) Land & Buildings Rs. 3,12,000 (b) Inventories Rs. 46,800 (c) Trade Payables Rs. 31,200. (vi) The inventory is still unsold on Balance Sheet date and the Trade Payables are not yet settled. (vii) Other Reserves as on 31st March, 2018 are the same as was on 1st April, 2017. (viii) The business activities of both the company are not seasonal in nature and therefore, it can be assumed that profits are earned evenly throughout the year. Prepare the Consolidated Balance Sheet as on 31st March, 2018 of the group of entities PN Ltd. and SR Ltd. as per Ind AS.

- 35. ADHISH SIR 35 Question: 66 In 20X1, Entity A acquired 100 % equity interest in entity B for cash consideration of `1,25,000. Fair value of Identifiable net asset of B were ` 1,00,000. In the subsequent years, Entity B earns ` 20,000. Entity A then disposed off 30 % of its equity interest for `40,000. Pass journal entry for sale of partial holding. Question: 67 The summarized balance sheets of Kush Ltd. and Shuk Ltd. as at 31st March, 2010 are as follows: (` In lakhs) Liabilities Kush Ltd. Shuk Ltd. Assets Kush Ltd. Shuk Ltd. Equity share capital of Rs. 10 each 216 108 Plant 86.4 72.9 Securities premium 32.4 - Furniture 23.4 7.2 Capital reserve as on 1.4.09 - 7.2 Stock 18 13.5 General reserve as on 1.4.09 13.5 9 Debtors 73.8 47.6 Profit and loss account 70.2 21.6 Trade investment 2.7 Creditors 29.7 19.7 Goodwill at cost 45 13.6 Investment in Shuk Ltd. – 8.64 lakhs shares at cost 97.2 Balance at bank 18 8 361.8 165.5 361.8 165.5 Additional information: (i) On 1st April, 2009 Kush Ltd. acquired from the shareholders of Shuk Ltd. 8.64 lakhs shares of `10 each in Shuk Ltd. and allotted in consideration thereof 6.48 lakhs of its own shares of Rs.10 each at a premium of `5 per share. (ii) The consideration for the shares of Shuk Ltd. was arrived at inter – alia by valuing certain assets of Shuk Ltd. on 1st April, 2009 as under – (a) Plant at ` 90 lakhs (b) Furniture at `8 lakhs. (c) No value on trade investment and goodwill. No adjustments were made in the books of accounts of Shuk Ltd. in respect of the above valuation. During 2009 – 10 there was no purchase or sale of these assets. It is desired that such adjustments should however be made in the consolidated accounts. (iii) The figures for plant and furniture at 31.3.2010 shown in the balance sheet are after providing depreciation for 2009 – 2010 at the rate of 10 % p.a. and 20 % p.a. respectively, on the book values as at 1.4.09. (iv) The profit and loss account of Shuk Ltd. showed a credit balance of `27 lakhs on 1.4.09. A dividend of 10 % was paid in January, 2010 for the year 2008 – 09. This dividend was credited to profit and loss account of Kush Ltd. (v) The following point was not considered in making out the accounts: During the year, expenses of `4,500 per month were incurred by Kush Ltd. on behalf of Shuk Ltd. It was by mistake debited to profit and loss account of Kush Ltd. and nothing has been done in the accounts of Shuk Ltd. (vi) The stock of Shuk Ltd. included `4.5 lakhs of goods received from Kush Ltd. invoiced at cost plus 25 %.

- 36. ADHISH SIR 36 (vii) Debtors of Shuk Ltd. include `3.5 lakhs due from Kush Ltd. whereas creditors of Kush Ltd. include `3.1 lakhs due to Shuk Ltd. the difference being represented by a cheque in transit. (viii) Group company decided to measure NCI at proportionate net asset method. You are required to consolidate the account of the two companies and prepare a consolidated balance sheet of Kush Ltd. and its subsidiary as at 31st March, 2010. Question: 68 [CMA – Dec. 2019] War Ltd. purchased on 31st March, 1997, 48,000 shares in Peace Ltd. at 50 % premium over face value by issue of 8 % debentures at 20 % premium. The balance sheets of War and Peace Ltd. as on 31.3.1997, the date of purchase were as under: Liabilities War Ltd. Peace Ltd. Assets War Ltd. Peace Ltd. Share capital (Rs. 10) 10,50,000 6,00,000 Fixed assets 6,50,000 2,00,000 General reserve 1,20,000 40,000 Stock in trade 3,00,000 1,80,000 Profit and loss account 80,000 - Sundry debtors 3,20,000 2,00,000 Sundry creditors 1,00,000 60,000 Cash in hand 60,000 30,000 Preliminary expenses 20,000 10,000 Profit and loss account - 80,000 13,50,000 7,00,000 13,50,000 7,00,000 Particulars of War Ltd.: (i) Profit made: 1997 – 98 Rs. 1,60,000 1998 – 99 Rs. 2,00,000 (ii) The above profit was made after charging depreciation of Rs. 60,000 and Rs. 40,000 respectively. (iii) Out of profit shown above every year Rs. 20,000 had been transferred to general reserve. (iv) 10 % dividend had been paid in both the years. (v) It has been decided to write down investment to face value of shares in 10 years and to provide for shares of loss to subsidiary. Particulars of Peace Ltd: The company incurred losses of Rs. 40,000 and Rs. 60,000 in 1997 - 98 and 1998 – 99 after charging depreciation of 10 %p.a. of the book value as on 1.4.97. Prepare consolidated balance sheet as at 31.3.99 of War Ltd. and its subsidiary. Question: 69 The Balance Sheet of Big Ltd., Small Ltd. and Little Ltd. as at 1st March, 2013 are given below: Particulars Big Limited Small Limited Little Limited I. Assets: Non – current assets: Plant and machinery 80,000 1,10,000 1,15,000 Non – current investment: Equity shares in Small 90,000 Equity shares in Little 40,000 60,000 Current assets: Inventories 60,000 35,000 35,000 Trade receivables 35,000 20,000 15,000 Small Limited 18,000 - - Little Limited 7,000 Cash and cash equivalent 15,000 10,000 10,000 Total 3,45,000 2,35,000 1,75,000

- 37. ADHISH SIR 37 II. Equity and Liabilities: Equity share capital of 10 each 2,00,000 1,00,000 60,000 Other equity: General reserve 60,000 50,000 40,000 Profit and loss account 50,000 40,000 30,000 Current Liabilities: Trade payables 35,000 30,000 40,000 Big Limited 15,000 5,000 Total 3,45,000 2,35,000 1,75,000 (i) Big Ltd. held 8000 shares of Small Ltd. and 1800 shares of Little Ltd. (ii) Small Ltd. held 3600 shares of Little Ltd. (iii) All investments were made on July 2012 (iv) The following balances were there on July 2012: Small Limited Little Limited Reserves 25,000 15,000 Profit and Loss account 30,000 25,000 (v) Small Ltd. invoiced goods to Big Ltd. at cost + 25% in December 2012. The closing stock of Big Ltd. includes goods with invoice value `6,000. (vi) Little Ltd. sold to Small Ltd. an equipment costing 24,000 at a profit of 25% on selling price on January 2013. Depreciation at 10% p.a. was provided by Small Ltd. on this equipment. (vii) Big Ltd. proposes dividend at 10%. Prepare the Consolidated Balance Sheet of the group as at 31 March 2013. Question: 70 [CMA – Study material - 13] P acquires 60% shares in Q on 1- 10 - 2017. Q makes profits 10000 in the year 2017-18 and declared dividend 6000. NCI is valued at 12000 at acquisition. (` lakhs) Show consolidated and Separate Balance sheet in books of P. Question 71 [CMA – Study material -14] On 1-4-x6 BM Ltd. acquired 80% share of CM Ltd. at 1000000, when the fair value of its net assets was 1000000. During 1-4-x6 to 31-3-x7 CM Ltd made TCI 120000. On that date BM sold 20% holding to outsiders at 280000. Pass journal entries for sale of partial holding retaining control.

- 38. ADHISH SIR 38 ADHISH SIR CLASSES EXCLUSIVE QUESTION BANK FOR IND AS -103 FOR CMA FINAL STUDENTS

- 39. ADHISH SIR 39 CMA FINAL – IND AS- 103 “BUSINESS COMBINATION” QUESTION BANK PART – 1 – ACCOUNTING FOR BUSINESS COMBINATION WHERE TARGET COMPANY DOES NOT CEASE TO EXIST Question: 1 A Ltd. acquires 100% of B Ltd. for `9,60,000. Fair Value (FV) of B’s net assets at time of acquisition amounts ` 8,00,000. Required: 1. Calculate Goodwill. 2. Journal Entries in the books of A. Question: 2 On March 31, 201X, K Ltd. acquired L Ltd. K Ltd. issued 60,000 equity shares (`10 par value) that were trading at `240 on March 31. The book value of L Ltd.’s net assets was `72,00,000 on March 31. The fair value of net assets was assessed at `1,35,00,000. Show acquisition journal entry under Ind AS 103. Question: 3 A Ltd. acquires 80% of B Ltd. for `9,60,000 paid by equity at par. Fair Value (FV) of B’s net assets at time of acquisition amounts ` 8,00,000. Required: 1. Calculate Non-Controlling-Interest (NCI) and Goodwill. 2. Journal Entries in the books of A. Question: 4 Z Ltd. acquired a 60% interest in P Ltd. on January 1, 2017. Z Ltd. paid `700 Lakhs in cash for their interest in P Ltd. The fair value of P Ltd.’s assets is `1,800 Lakhs, and the fair value of its liabilities is `900 Lakhs. Provide the journal entry for the acquisition using Ind AS, assuming that P Ltd. does not wish to report the NCI at fair value. Question: 5 On 1 January 20X5 M Ltd. acquires 80 per cent of the equity interests of P Ltd in exchange of cash of `250. The identifiable assets are measured at `350 and the liabilities assumed are measured at `50. The fair value of the 20 per cent non controlling interest in P is `43. Question: 6

- 40. ADHISH SIR 40 D has acquired 100% of the equity of F on March 31, 20X7. The purchase consideration comprises of an immediate payment of `10 lakhs and two further payments of `1.21 lakhs if the Return on Equity exceeds 20% in each of the subsequent two financial years. A discount rate of 10% is used. Compute the value of total consideration at the acquisition date. Question: 7 C Ltd acquires 60% share in D Ltd. for cash payment of `200,000. The fair value of non-controlling interest is `1,00,000. This amount was determined with reference of market price of D’s ordinary shares before the acquisition date. Calculate NCI and goodwill following: i. Fair Value approach ii. Proportionate shares of identified net asset in acquiree approach when on the acquisition date, the aggregate value of D’s identifiable net assets is: (a) `2,40,000; (b) `3,30,000. Question: 8 Z Company acquired C Company on April 1, 201X. For a lawsuit contingency C has a present obligation as on April 1, 201X and the fair value of the obligation can be reliably measured as `50,000. As of the acquisition date it is not believed that an out flow of cash or other assets will be required to settle this matter. What amount should be recorded by Z Company under Ind AS for this contingent liability of C Company? Question: 9 Entity A acquired 35 % of Entity B in 2015 for `35,000. In 2016, fair value of shares of entity B is `42,000, thus `7,000 reported under OCI In 2016, A further acquired 40% stake in B. Consideration paid `60,000. Entity A identifies the net assets of B as `120,000, value 35% shares at `45,000. NCI is valued at proportionate net assets. Show workings and Journal entries. Question: 10 Acquirer obtained 75 % of the equity interests of acquiree in a forced sale. Acquires has no prior equity interest in acquire. Acquirer determined that the following are appropriate fair value measures to be used in accounting for this combination: Consideration (`3,00,000 of cash and `2,50,000 of other assets) transferred by acquirer `5,50,000 Acquiree’s identifiable assets acquired `10,00,000 Acquiree’s liabilities assumed `2,00,000 Non – controlling interest in acquire `2,10,000 Required: (i) Calculate goodwill / Bargain purchase. (ii) Record journal entry. Question: 11 Following is the Balance – sheet for Yati Limited at 1st January, 2018 is as follows: Current assets 9,20,000 Liabilities 12,00,000 Non – current assets 18,00,000 Capital (`10 each) 8,00,000

- 41. ADHISH SIR 41 Retained earnings 7,20,000 27,20,000 27,20,000 Yati’s assets and liabilities are fairly valued except non – current assets that are undervalued by 2,00,000. On January, 2, 2018, Dishita Limited issues 80,000 shares of its `10 per value for all of the Yati Limited’s net assets and Yati Limited is dissolved. Market quotations for the two stocks on this date are: Yati Limited = `19 Dishita Limited = `28 Dishita Limited pays the following fees and costs in connection with the combination: Finder’s fees `10,000 Cost of registering and issuing stock `5,000 Legal and accounting fees `6,000 Required: (a) Calculate Dishita Limited’s cost of investment in Yati Limited. (b) Calculate any goodwill from the business combination. Question: 12 Dishita Limited purchased the net assets of Yati Limited on January 2, 2005 for `2,80,000 and also paid `10,000 as direct acquisition costs. Balance – sheet of Yati Limited as on 2nd January was as follows: Accounts receivables – Net 90,000 Current Liabilities 35,000 Inventory 1,80,000 Long term debts 80,000 Land 20,000 Common stock 2,25,000 Building – Net 30,000 Retained earnings 20,000 Equipment – Net 40,000 3,60,000 3,60,000 Fair values agree with book values except for inventory, land and equipment, that have fair values of `2,00,000; `2,50,000 and `35,000 respectively. Yati Limited has patent rights valued at `10,000. Required: Pass journal entry for the cash purchases of Yati Limited’s net assets. Question: 13 MAJ Corporation acquired 90% of the common stock of Min Co. for `420,000. MAJ previously held no equity interest in Min. On the date of acquisition, the carrying amount of Min’s identifiable net assets equal to `300,000. The acquisition-date fair values of Min’s inventory and equipment exceeded their carrying amounts by `60,000 and `40,000, respectively. The carrying amounts of the other assets and liabilities were equal to their acquisitiondate fair values. What amount should MAJ recognize as goodwill immediately after the acquisition? Question: 14 On 1 January 2009 A Ltd acquired all the assets and liabilities of B Ltd. Details of the consideration transferred are as follows: • Cash of $400,000, half to be paid on 1 January 2009, with the balance due on 1 January 2010. The incremental borrowing rate for A Ltd is 10% • 100,000 shares in A Ltd were issued. The share price on 1 January 2009 was $1.50 per share. This price represented a six-month high. Costs of issuing the shares was $1,000.

- 42. ADHISH SIR 42 • Due to doubts as to whether the share price would remain at or above the $1.50 level, A Ltd agreed to supply cash to the value of any decrease in the share price below $1.50. This guarantee was valid for a period of 3 months (to 31 March 2009). A Ltd believed that there was a 75% chance that the share price would remain at or above $1.50 until 31 March 2009 (and a 25% chance that it would fall to $1.40) • Supply of a patent to B Ltd. The FV of the patent is $60,000. As the patent was internally generated it has not been recognised in A Ltd’s books. • Legal fees and associated with the acquisition totalled $5,000. Required: Calculate the amount of consideration transferred. Question: 15 Yati Limited is seeking to expand its market share and has negotiated to take over the operations of Dishita Limited on 1st April, 2018. The statement of financial position of the two companies as on 31st March, 2018 were as follows: Particulars Yati Limited Dishita Limited Share capital (`1each) 1,00,000 60,000 Other reserves 28,500 26,800 Retained earnings 49,000 23,900 Debentures 1,00,000 52,500 Loans 50,000 44,000 Accounts payable 56,000 45,100 Total 3,83,500 2,52,300 Goodwill 25,000 2,000 Plant and equipment (net) 65,000 46,000 Building (net) 60,000 30,000 Freehold land 1,50,000 1,00,000 Inventories 35,500 27,600 Accounts receivable 25,000 34,700 Cash 23,000 12,000 Total 3,83,500 2,52,300 Howard Ltd is to acquire all the identifiable assets, except cash, of Falcon Ltd. The assets of Falcon Ltd are all recorded at fair value except the following. Fair value (`) Inventories 39,000 Freehold land 1,30,000 Buildings 40,000 In exchange, Howard Ltd is to provide sufficient extra cash to allow Falcon Ltd to repay all of its outstanding debts and its liquidation costs of `2400, plus two fully paid shares in Howard Ltd for every three shares held in Falcon Ltd. The fair value of a share in Howard Ltd is `3.20.Costs of issuing the shares were `1200. Required: Prepare the acquisition analysis and journal entries to record the business combination in the records of Yati Ltd. Question: 16 D Limited agreed to acquire the business of a rival company, T Limited, taking over all assets and liabilities as at 1.4.2017. The price agreed on was `60,000, payable `20,000 in cash and the balance by the issue to the selling company of 16,000 fully paid shares in D Limited, these shares having a fair value of `2.50 per share.

- 43. ADHISH SIR 43 At 1.4.2017, the assets and liabilities of T Limited consisted of the following: Plant (net) `30,000 Inventories `26,000 Accounts receivable `20,000 Accounts payable `20,000 All the identifiable net assets of T Limited were recorded by T Limited at fair value except for the inventories, which were considered to be worth `28,000 (assume no tax effect). The business combination was completed and T Limited went into liquidation. D Limited incurred incidental costs of `500 in relation to acquisition. Prepare the journal entries in the books of D Limited to record the business combination. Question: 17 Mr. J acquired 40 % of the equity interest of Yati Limited for `40 million several years ago. On 1st January, 2015, Mr. J acquired an additional 35 % for `45 million, when the fair value of identifiable net assets were 105 million. The fair value of non – controlling interest on 1st January, 2015 was `32 million and the fair value of the original 40 % holding was `52 million. Calculate value of goodwill. Question: 18 Emma Limited acquires the net assets of Swan Limited for a consideration of `80,000. One half is to be paid on acquisition date and other half is payable in one year’s time. The appropriate discount rate is 8 %. Acquired assets and Liabilities are: Equipment `48,000 Inventories `18,000 Accounts receivables `12,000 Patent `12,000 Accounts payable `14,000 Calculate value of goodwill or Bargain purchase. Question: 19 J acquires 100 % of equity of B on 31st December, 2018. There are 3 elements to the purchase consideration: (a) An immediate payment of `50,00,000 (b) Two further payments of `10,00,000 if the return on capital employed exceeds 10 % in each of the subsequent financial years ending December. All indicators have suggested that this target will be met. J uses a discount rate of 7 %. Calculate consideration. Question: 20 On January 1, 2018 Yati Limited purchased Dishita Limited on the following terms: (i) Cash payment of `5,00,000 immediately. (ii) Cash payment of `1,10,000 after 1 year. Appropriate discount rate is 10 %. (iii) By issuing 1,50,000 equity shares having market value of `25 each.

- 44. ADHISH SIR 44 (iv) Yati Limited agree to pay additional cash if share price falls below from `25 in 3 months time. Yati Limited estimate that there is 20 % chance that market price will fall to `22. On that day Balance – sheet of Dishita Limited is as under: Share capital 23,50,000 Land 4,00,000 Accounts payable 20,00,000 Building 7,50,000 Equipment 7,00,000 Trademark 1,00,000 Inventory 10,00,000 Receivables 9,00,000 Cash 5,00,000 43,50,000 43,50,000 All amounts are at fair value except the following: Inventory `12,50,000 Land `6,00,000 Trade mark `1,50,000 Calculate goodwill or bargain purchase. Question: 21 Company P held 25 % equity interest in company Q on 1.1.2015 for `50 M. It purchased 20 % additional holding in company Q on 31.12.2016 for `30 M. Company P purchased 15 % additional holding on 31.12.2017 for 32 M. The book value of P’s total investment just before acquisition was ` 85 M and fair value of net asset is `200 M as at acquisition date. NCI should be measured at fair value. Calculate goodwill / Bargain purchase. Question: 22 On 1.1.2008, Aacquired 50 % interest in B for `60 M. A already held a 20 % interest which had been acquired for `20 M but which was valued at `24 M on 1.1.2008. The fair value of NCI at 1.1.08 was `40 M and the fair value of net asset of B was `110 M. Calculate goodwill or bargain purchase. Question: 23 V Limited acquires 80 % of equity shares of S Limited at a cost of `40,00,000. Fair value of non – controlling interest is `10,00,000. On the acquisition date the fair value of identifiable net asset is `45,00,000. Calculate goodwill / Bargain purchase if – (a) NCI measured at fair value (b) NCI measured at proportionate net asset basis. Question: 24 Entity A acquired 15 % of Entity B in 2009 for `10,000. In 2010, fair value of shares of entity B is `12,000, thus `2,000 reported under OCI. In 2010, further acquired 60 % stake, consideration paid for `60,000. Entity A identifies the net asset of B as `80,000. Value of 15 % shares is `12,500. Required: (a) Calculate Goodwill / Bargain purchase. (b) Pass necessary journal entries.