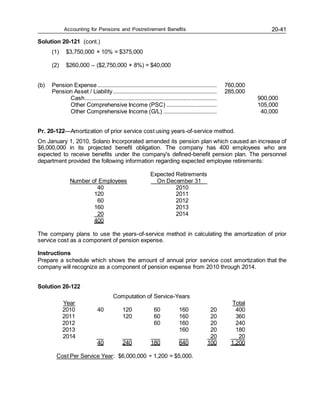

This document provides an overview of accounting for pensions and postretirement benefits, including:

- Key terms and concepts related to defined benefit and defined contribution pension plans.

- Methods for measuring pension obligations and determining pension expense.

- Accounting for plan amendments, gains and losses, and funding requirements.

- Disclosures required in financial statements for pension and other postretirement benefit plans.

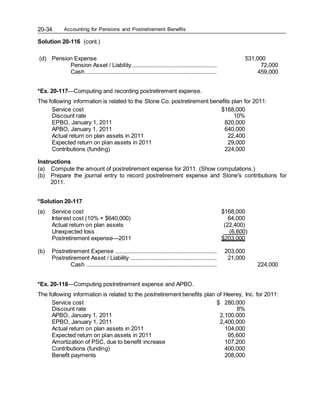

![Accounting for Pensions and Postretirement Benefits

20-30

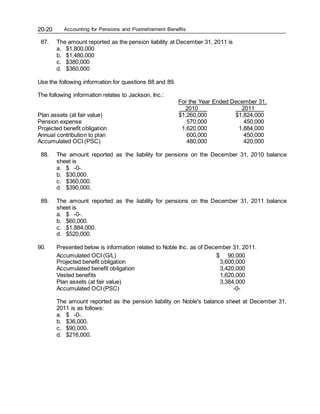

Ex. 20-110— Recording pension asset / liability.

Miles Co. had the following selected balances at December 31, 2011:

Projected benefit obligation $4,700,000

Accumulated benefit obligation 4,550,000

Fair value of plan assets 4,340,000

Accumulated OCI (PSC) 170,000

Instructions

Calculate the pension asset / liability to be recorded at December 31, 2011.

Solution 20-110

$4,700,000 - $ 4,340,000 = $360,000.

Ex. 20-111—Pension calculations.

Montoya Company has available the following information about its defined-benefit pension plan

for the year ending December 31, 2011:

Service cost for 2011 $ 25,000

Accumulated benefit obligation 683,000

Plan assets at fair value 630,000

Accumulated OCI (PSC) 300,000

Vested benefit obligation 505,000

Market-related asset value 725,000

Projected benefit obligation 865,000

Accumulated OCI net gain 90,000

Interest on projected benefit obligation 64,000

Instructions

(a) Calculate the pension asset / liability to be recorded at December 31, 2011.

(b) Calculate the 2012 amortization of the net gain. The average remaining service life of

employees is 10 years.

Solution 20-111

(a) $865,000 - $630,000 = $235,000 Pension liability.

(b) [$90,000 – ($865,000 X 10%)] ÷ 10 = $350.

Ex. 20-112—Pension plan calculations.

The following information is for the pension plan for the employees of Payne, Inc.

12/31/10 12/31/11

Accumulated benefit obligation $2,800,000 $3,760,000

Projected benefit obligation 3,040,000 4,000,000

Fair value of plan assets 3,080,000 3,520,000

AOCI – Net (gain) or loss (425,000) (480,000)

Settlement rate 8% 8%

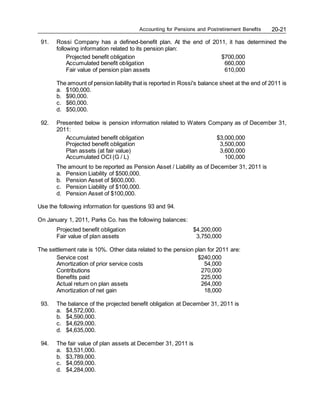

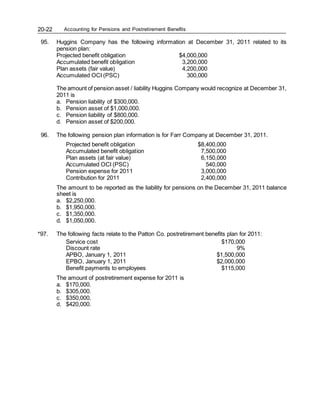

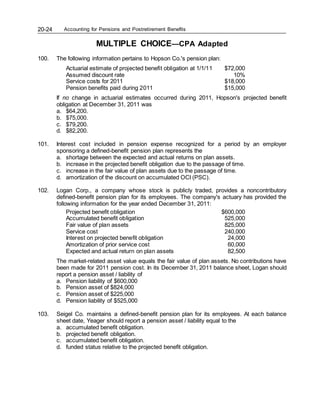

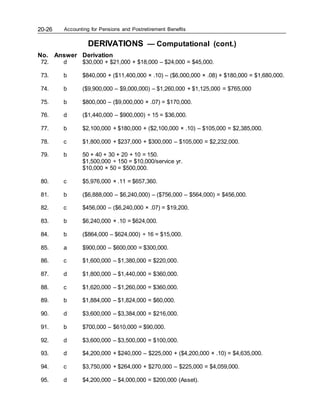

Expected rate of return 7% 6%](https://image.slidesharecdn.com/yehoisabkene16-220510071822-23de001b/85/yehoisab-kene16-doc-30-320.jpg)