Downloaded 67 times

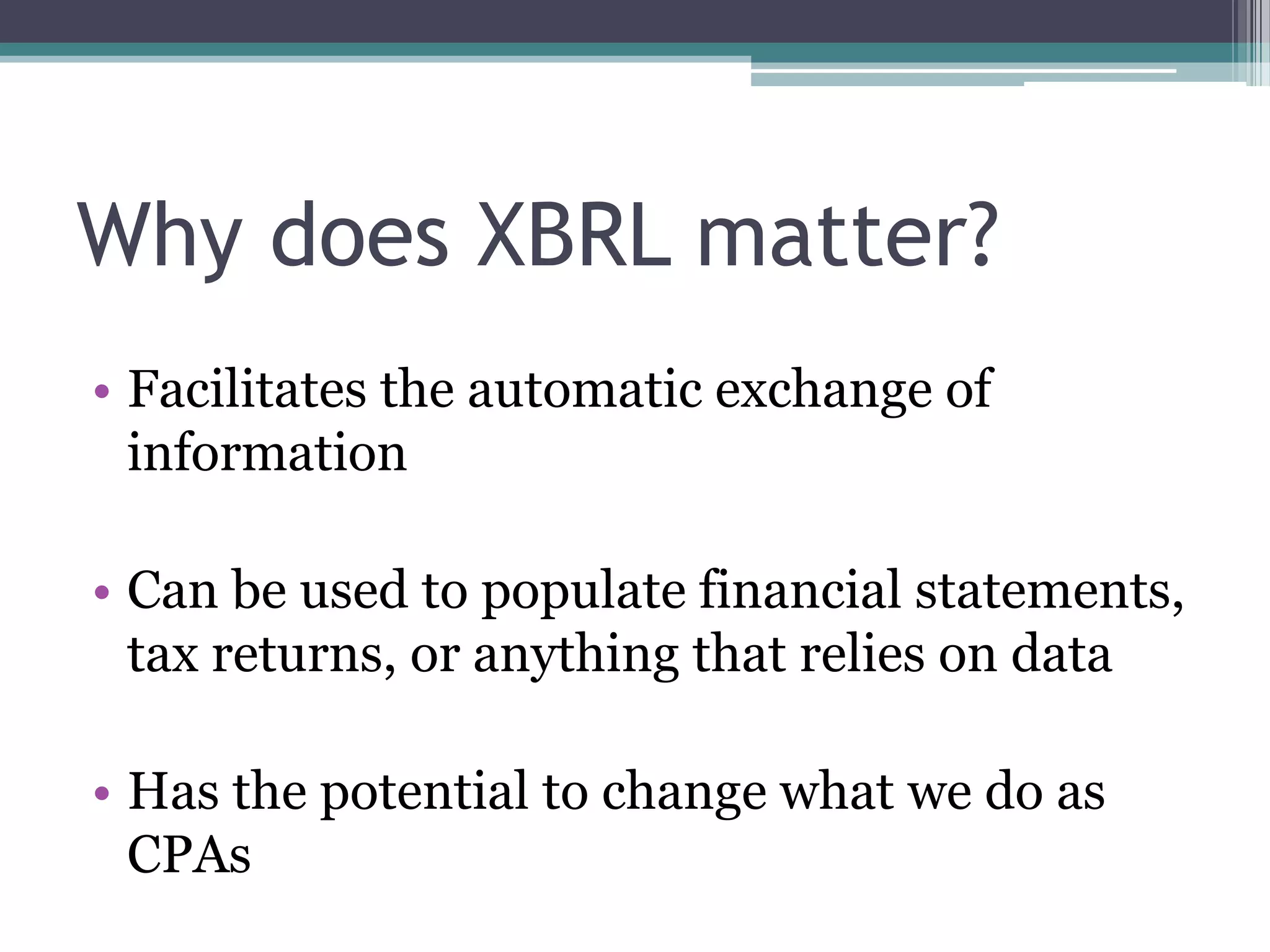

XBRL (Extensible Business Reporting Language) is an open standard tagging language used internationally for financial reporting, including a requirement from the SEC in the US. The document discusses its benefits, specifically how it facilitates the exchange of information and aids in financial data analysis, and highlights ongoing XBRL projects and taxonomies. The document also covers various implementations, challenges, and the importance of adapting XBRL for different sectors, including non-profits.