Download as PDF, PPTX

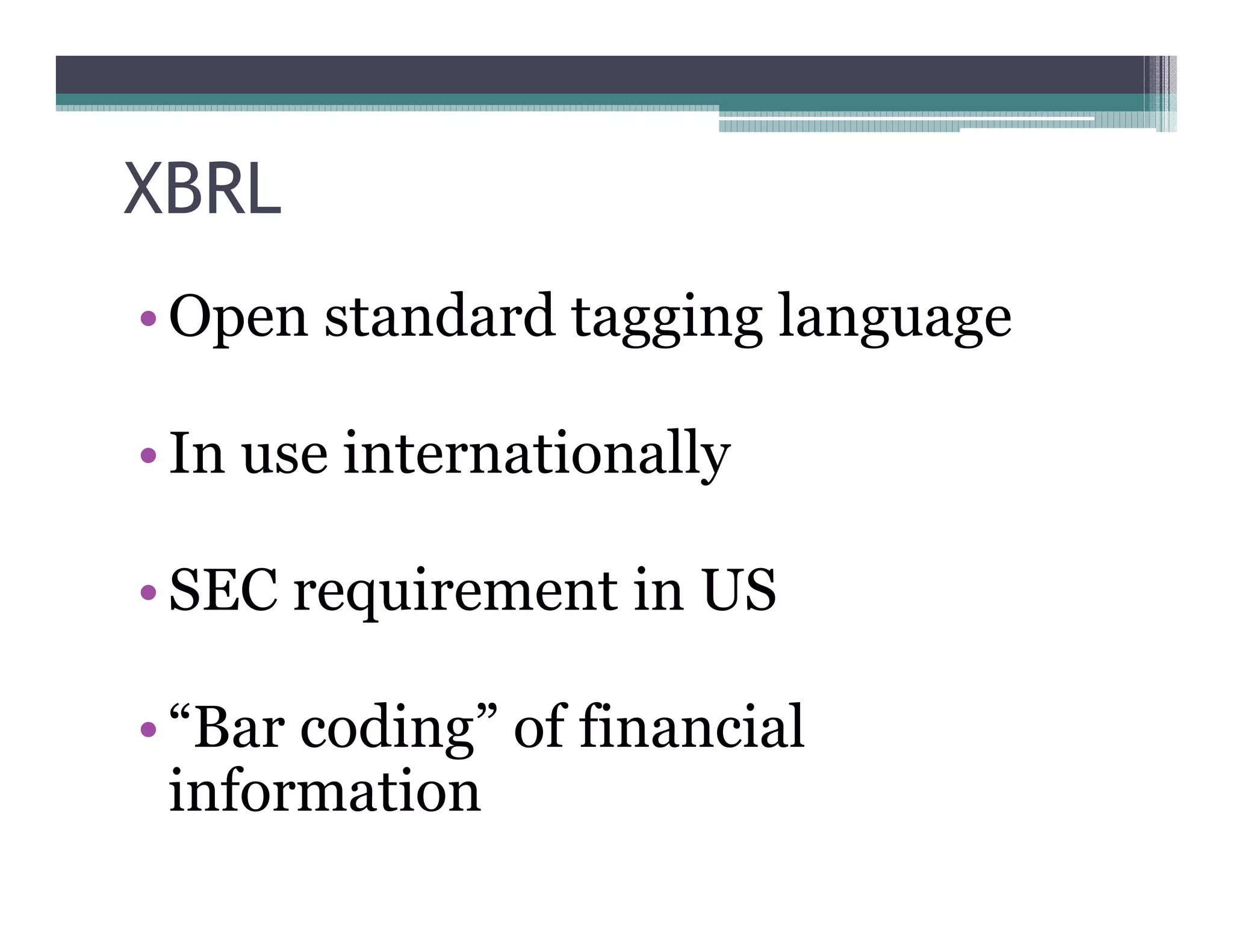

The document discusses XBRL (Extensible Business Reporting Language), an open standard for tagging financial information that facilitates data exchange and compliance, particularly for CPAs and organizations like MACPA. It details the importance of taxonomies for organizing data, challenges in implementation, and how XBRL can improve efficiency in financial reporting and auditing. The document also highlights ongoing XBRL initiatives and resources available for professionals interested in this technology.