2

Arbitrage with Payouts

Therecan be different types of payouts for

different securities and commodities. Positive

payouts can be there for financial assets, such

as dividends, and negative payouts such as

storage costs, insurance, spoilage etc. for

commodities

t t1 T

Enter Futures Payout of C1 Futures Expires

3.

3

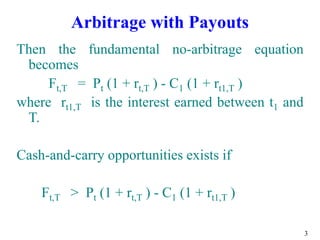

Arbitrage with Payouts

Thenthe fundamental no-arbitrage equation

becomes

Ft,T = Pt (1 + rt,T ) - C1 (1 + rt1,T )

where rt1,T is the interest earned between t1 and

T.

Cash-and-carry opportunities exists if

Ft,T > Pt (1 + rt,T ) - C1 (1 + rt1,T )

5

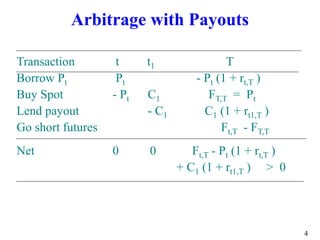

Arbitrage with Payouts

Reversecash-and-carry opportunities exists if

Ft,T < Pt (1 + rt,T ) - C1 (1 + rt1,T )

Transaction t t1 T

Short spot Pt - C1 - FT,T

Lend Pt - Pt Pt (1 + rt,T )

Borrow payout C1 - C1 (1 + rt1,T )

Go long futures FT,T - Ft,T

Net 0 0 Pt (1 + rt,T )

- C1 (1 + rt1,T ) - Ft,T > 0

6.

6

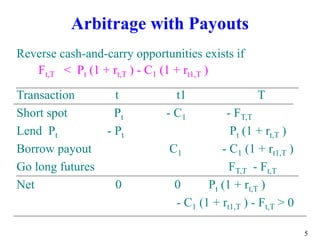

Arbitrage with dividends

Inthe earlier example, assume that XYZ share gives a

dividend of Rs.8, which is due six months from now. The

arbitrageur can borrow and lend at 7 % per annum. Is

there any arbitrage opportunity ?

The future value according to the fundamental no-arbitrage

equation is

= Spot price + interest - future value of payouts

= Rs.2500 + Rs.2500 * 0.07 - Rs.8 * (1+0.07*(6/12))

= Rs.2500 + Rs. 175 - Rs.8.28

= Rs.2666.72 < Rs.2700 = Futures price

Since futures price is higher than the no-arbitrage price, the

arbitrageur should perform a cash-and-carry arbitrage.

7.

7

Transaction Costs andArbitrage

Bid-Ask Spreads

Margins and Short-Selling Costs

Differential Borrowing and Lending Rates

Transaction Fees

8.

8

Cash-and-Carry and Reverse

Cash-and-CarryArbitrage

Transaction costs in the spot and futures markets affect

arbitrage trading through their influence on implied repo

and reverse repo rates.

Pt

b = bid price for spot security

Pt

a = ask price for spot security

Fb

t,T= bid price for futures contract (price for going

short)

Fa

t,T= ask price for futures contract (price for going

long)

TF = total transaction fees

rb

t,T = borrowing rate between t and T

rl

t,T = lending rate between t and T

9.

9

Cash-and-Carry and Reverse

Cash-and-CarryArbitrage

When transaction costs are included, the cash-and-carry

strategy is to buy the spot at the ask price and lock in

a sales price at the futures bid price. By

consolidating all transaction costs, the implied repo

rate is,

Cash inflow at T - Cash outflow at t

Implied repo rate =

Cash outflow at t

(Fb

t,T - TF) - Pa

t

=

Pa

t

10.

10

Cash-and-Carry and Reverse

Cash-and-CarryArbitrage

In the reverse cash-and-carry with transaction costs, the

arbitrageur sells the spot security short at the bid price

and covers the short position by locking in a futures ask

price. The implied reverse repo rate is

Implied Cash outflow at T - Cash inflow at t

reverse repo rate =

Cash infolw at t

(Fa

t,T + TF) - Pb

t

=

Pb

t

11.

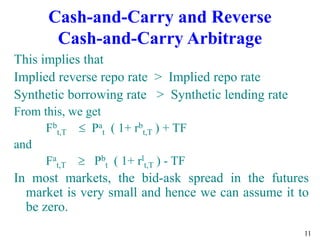

11

Cash-and-Carry and Reverse

Cash-and-CarryArbitrage

This implies that

Implied reverse repo rate > Implied repo rate

Synthetic borrowing rate > Synthetic lending rate

From this, we get

Fb

t,T Pa

t ( 1+ rb

t,T ) + TF

and

Fa

t,T Pb

t ( 1+ rl

t,T ) - TF

In most markets, the bid-ask spread in the futures

market is very small and hence we can assume it to

be zero.

12.

12

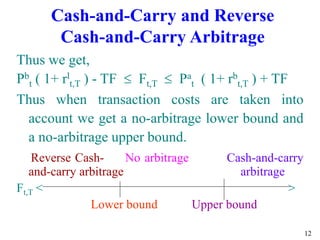

Cash-and-Carry and Reverse

Cash-and-CarryArbitrage

Thus we get,

Pb

t ( 1+ rl

t,T ) - TF Ft,T Pa

t ( 1+ rb

t,T ) + TF

Thus when transaction costs are taken into

account we get a no-arbitrage lower bound and

a no-arbitrage upper bound.

Reverse Cash- No arbitrage Cash-and-carry

and-carry arbitrage arbitrage

Ft,T < >

Lower bound Upper bound

13.

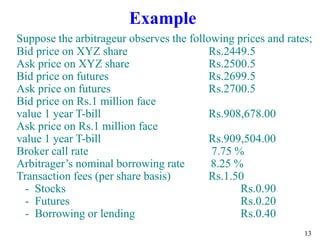

13

Example

Suppose the arbitrageurobserves the following prices and rates;

Bid price on XYZ share Rs.2449.5

Ask price on XYZ share Rs.2500.5

Bid price on futures Rs.2699.5

Ask price on futures Rs.2700.5

Bid price on Rs.1 million face

value 1 year T-bill Rs.908,678.00

Ask price on Rs.1 million face

value 1 year T-bill Rs.909,504.00

Broker call rate 7.75 %

Arbitrager’s nominal borrowing rate 8.25 %

Transaction fees (per share basis) Rs.1.50

- Stocks Rs.0.90

- Futures Rs.0.20

- Borrowing or lending Rs.0.40

14.

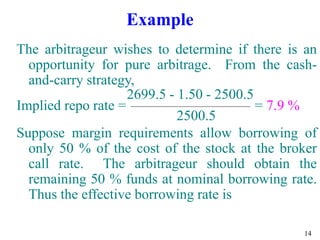

14

Example

The arbitrageur wishesto determine if there is an

opportunity for pure arbitrage. From the cash-

and-carry strategy,

2699.5 - 1.50 - 2500.5

Implied repo rate = = 7.9 %

2500.5

Suppose margin requirements allow borrowing of

only 50 % of the cost of the stock at the broker

call rate. The arbitrageur should obtain the

remaining 50 % funds at nominal borrowing rate.

Thus the effective borrowing rate is

15.

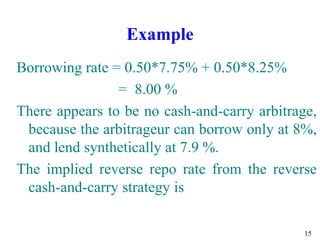

15

Example

Borrowing rate =0.50*7.75% + 0.50*8.25%

= 8.00 %

There appears to be no cash-and-carry arbitrage,

because the arbitrageur can borrow only at 8%,

and lend synthetically at 7.9 %.

The implied reverse repo rate from the reverse

cash-and-carry strategy is

16.

16

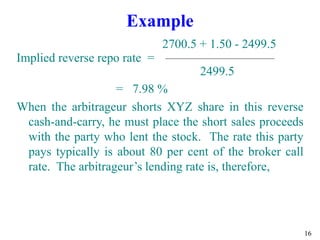

Example

2700.5 + 1.50- 2499.5

Implied reverse repo rate =

2499.5

= 7.98 %

When the arbitrageur shorts XYZ share in this reverse

cash-and-carry, he must place the short sales proceeds

with the party who lent the stock. The rate this party

pays typically is about 80 per cent of the broker call

rate. The arbitrageur’s lending rate is, therefore,

17.

17

Cash-and-Carry and Reverse

Cash-and-CarryArbitrage

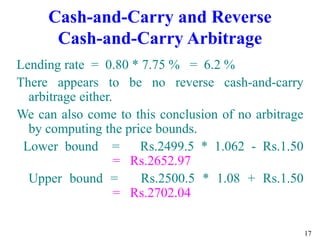

Lending rate = 0.80 * 7.75 % = 6.2 %

There appears to be no reverse cash-and-carry

arbitrage either.

We can also come to this conclusion of no arbitrage

by computing the price bounds.

Lower bound = Rs.2499.5 * 1.062 - Rs.1.50

= Rs.2652.97

Upper bound = Rs.2500.5 * 1.08 + Rs.1.50

= Rs.2702.04

18.

18

Value of aForward Contract

That Began Earlier

At start, value of a forward, V0 = 0

At maturity, value of a forward to Long is

VT = [PT – F0,T] and opposite to Short. Long

gains, Short loses if spot soars.

At intermediate date t, value of a forward to

Long is Vt = present value of [PT – F0,T]

= Pt – F0,T / (1+r t,T)

19.

19

Forward Contracts

on Commodities

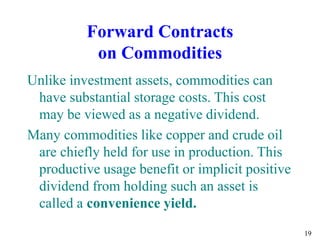

Unlikeinvestment assets, commodities can

have substantial storage costs. This cost

may be viewed as a negative dividend.

Many commodities like copper and crude oil

are chiefly held for use in production. This

productive usage benefit or implicit positive

dividend from holding such an asset is

called a convenience yield.

20.

20

Cost-of-Carry with StorageCosts

and Convenience Yields

When storage costs (G) and convenience

yields [Y 0,T ] are included (paid upfront in

our formula), then cash-and-carry is better

described as cost-of-carry relationship.

At time 0, cost-of-carry gives

F0,T = [P0+ G – Y 0,T ] (1 + i T)

21.

21

Forward and FuturesPrices

Forward and futures prices are equal if

interest rate remains constant till maturity.

In reality, marking-to-market and default risk

can make the forward and futures prices

different.

Empirical results are mixed.

22.

22

Forward and FuturesPrices

Forward Versus Futures Prices

Forward and futures prices will be equal

One day prior to expiration

More than one day prior to expiration if

Interest rates are certain

Futures prices and interest rates are uncorrelated

Futures prices will exceed forward prices if futures

prices are positively correlated with interest rates.

Default risk can also affect the difference between

futures and forward prices.

23.

23

Conclusion

Forwards and futuresare similar contracts

except for some institutional features.

A forward price can be easily determined

from the spot by cash-and-carry and cost-

of-carry relationships.

“No-arbitrage” principle also helped to value

a contract that began earlier and exploit an

arbitrage opportunity.

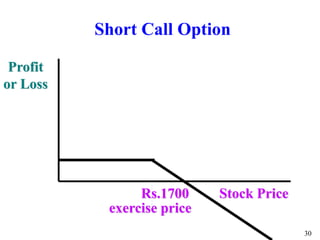

25

Option contract: givesthe owner the right to

buy or sell a fixed number of shares of stock

at a specified price over a limited time.

Call

Put

Options

26.

26

1800s or earlier

1900sPut and Call Brokers and Dealers

Association created an options market.

1973, The Chicago Board of Trade, organized

an exchange exclusively for trading options

on stocks, namely Chicago Board Options

Exchange (CBOE).

It opened its doors for call option trading on

April 26, 1973, and the first puts were added

in June 1977.

History

27.

27

Option buyer, optionholder or long

Option seller, option writer, or short

Option price, option premium or just premium

Exercise price, strike price, striking price, or

strike.

Exercise or exercising the option.

Expiration date

Time to expiration.

Expire worthless

Option Terminologies

28.

28

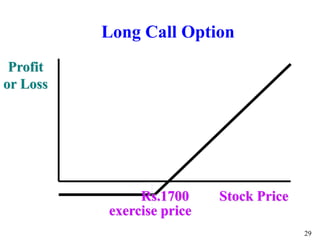

Call Option: givesthe owner the right to buy a

fixed number of shares of stock at a specified

price over a limited time.

If you buy a call option on Infosys stock, and the

stock price rises enough, you can profit on the

call option contract.

If the stock price does not rise enough, or falls,

your call option contract expires worthless.

Option Contracts

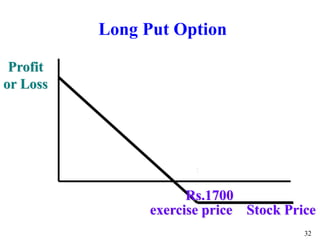

31

Put Option: givesthe owner the right to sell a

fixed number of shares of stock at a specified

price over a limited time.

If you buy a put option on Infosys stock, and the

stock price falls enough, you can profit on the

put option contract.

If the stock price does not fall enough, or rises,

your put option contract expires worthless.

Option Contracts

34

Option contracts canbe written on:

Common stocks

Stock Indices

Interest rates

Foreign currency

Commodities

Futures

Innovations in Options

35.

35

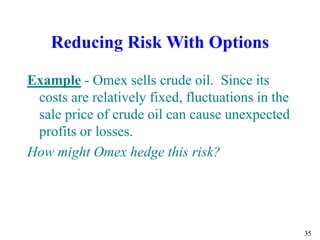

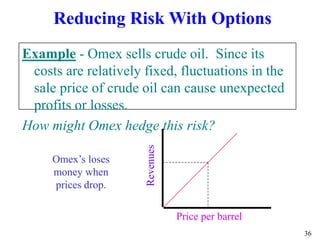

Reducing Risk WithOptions

Example - Omex sells crude oil. Since its

costs are relatively fixed, fluctuations in the

sale price of crude oil can cause unexpected

profits or losses.

How might Omex hedge this risk?

36.

36

Reducing Risk WithOptions

Example - Omex sells crude oil. Since its

costs are relatively fixed, fluctuations in the

sale price of crude oil can cause unexpected

profits or losses.

How might Omex hedge this risk?

Price per barrel

Omex’s loses

money when

prices drop.

Revenues

37.

37

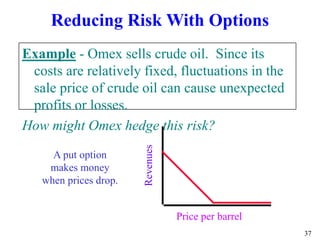

Reducing Risk WithOptions

Example - Omex sells crude oil. Since its

costs are relatively fixed, fluctuations in the

sale price of crude oil can cause unexpected

profits or losses.

How might Omex hedge this risk?

Price per barrel

A put option

makes money

when prices drop.

Revenues

38.

38

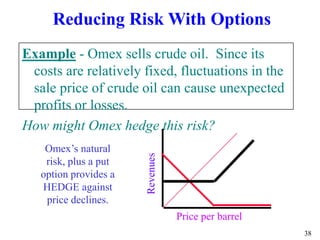

Reducing Risk WithOptions

Example - Omex sells crude oil. Since its

costs are relatively fixed, fluctuations in the

sale price of crude oil can cause unexpected

profits or losses.

How might Omex hedge this risk?

Price per barrel

Omex’s natural

risk, plus a put

option provides a

HEDGE against

price declines.

Revenues

![18

Value of a Forward Contract

That Began Earlier

At start, value of a forward, V0 = 0

At maturity, value of a forward to Long is

VT = [PT – F0,T] and opposite to Short. Long

gains, Short loses if spot soars.

At intermediate date t, value of a forward to

Long is Vt = present value of [PT – F0,T]

= Pt – F0,T / (1+r t,T)](https://image.slidesharecdn.com/drm05-250730182055-dd5aa29b/85/veru-knowledgable-slides-on-derivatives-18-320.jpg)

![20

Cost-of-Carry with Storage Costs

and Convenience Yields

When storage costs (G) and convenience

yields [Y 0,T ] are included (paid upfront in

our formula), then cash-and-carry is better

described as cost-of-carry relationship.

At time 0, cost-of-carry gives

F0,T = [P0+ G – Y 0,T ] (1 + i T)](https://image.slidesharecdn.com/drm05-250730182055-dd5aa29b/85/veru-knowledgable-slides-on-derivatives-20-320.jpg)

![Derivatives.ppt [autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/derivatives-pptautosaved-121028072053-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)