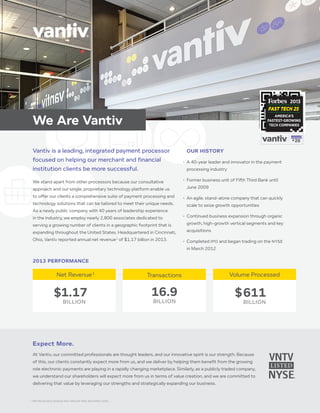

Vantiv is a leading payment processor focused on helping merchant and financial institution clients succeed by offering comprehensive payment processing and technology solutions. As a 40-year industry leader, Vantiv has 1,400 financial institution relationships and processes transactions for over 130,000 merchant locations across the United States. Vantiv aims to deliver more value to its clients and shareholders by leveraging its innovative spirit and strategic expansion.

![[Slideshare] Evolution of B2B Payments](https://cdn.slidesharecdn.com/ss_thumbnails/slideshareevolutionofb2bpayments-150327100722-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)