Valuation of shares & bonds NOTES @ BECDOMS

•

1 like•571 views

Valuation of shares & bonds NOTES @ BECDOMS

Recommended

More Related Content

What's hot

What's hot (18)

Similar to Valuation of shares & bonds NOTES @ BECDOMS

Similar to Valuation of shares & bonds NOTES @ BECDOMS (20)

More from Babasab Patil

More from Babasab Patil (20)

Recently uploaded

Recently uploaded (20)

Valuation of shares & bonds NOTES @ BECDOMS

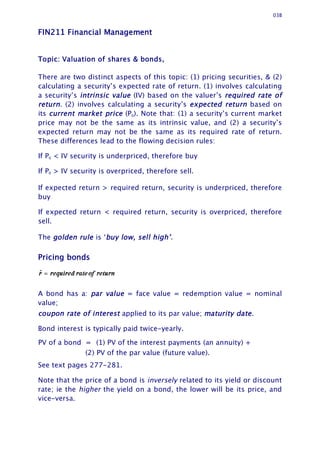

- 1. 03B FIN211 Financial Management Topic: Valuation of shares & bonds, There are two distinct aspects of this topic: (1) pricing securities, & (2) calculating a security’s expected rate of return. (1) involves calculating a security’s intrinsic value (IV) based on the valuer’s required rate of return. (2) involves calculating a security’s expected return based on its current market price (P0). Note that: (1) a security’s current market price may not be the same as its intrinsic value, and (2) a security’s expected return may not be the same as its required rate of return. These differences lead to the flowing decision rules: If P0 < IV security is underpriced, therefore buy If P0 > IV security is overpriced, therefore sell. If expected return > required return, security is underpriced, therefore buy If expected return < required return, security is overpriced, therefore sell. The golden rule is ‘buy low, sell high’. Pricing bonds A bond has a: par value = face value = redemption value = nominal value; coupon rate of interest applied to its par value; maturity date . Bond interest is typically paid twice-yearly. PV of a bond = (1) PV of the interest payments (an annuity) + (2) PV of the par value (future value). See text pages 277-281. Note that the price of a bond is inversely related to its yield or discount rate; ie the higher the yield on a bond, the lower will be its price, and vice-versa.

- 2. FIN211 03B When the yield on a bond is lower than its coupon rate, its price will be higher than its par value. When the yield on a bond is higher than its coupon rate, its price will be lower than its par value. 2

- 3. FIN211 03B Example A bond has a par value of $100, a coupon rate of 10.75% and matures in 5 years. If interest is paid annually and the required rate of return is 10%, what is the bond’s IV? Answer PV of the annuity: $10.75 [1 − (1.1)-5] / 0.1 = $40.75 PV of par value: $100 / (1.1)5 = 62.09 Total PV = IV = $102.84 Pricing preference shares IV = annual dividend ÷ required rate of return = Dp / RROR = Dp/Rp Example A preference share has a par value of $100 and a dividend rate of 10.75%. If the required rate of return is 10%, what is the share’s IV? Answer PV = IV = $10.75 / 0.1 = $107.50 Pricing ordinary shares D1 = D0(1 + g) g = expected growth rate. Can be defined in terms of growth in the book value (BV) of shareholders’ funds = BV1 / BV0 − 1 = return on equity (ROE) profit retention ratio. Example A share has just paid an annual dividend of $0.54. The book value of shareholder’s funds is currently $11,020,801. One year ago the book value of shareholders’ funds was $10,699,807. During the past year there were no changes to paid-up capital. The risk-free rate of return is currently 5%. A risk premium of 8% is required for investing in the share. What is its PV? Answer Required rate of return = 5% + 8% = 13% 3

- 4. FIN211 03B Growth rate = 11,020,801/10,699,807 − 1 = 0.03 D0 = $0.54 D1 = $0.54 1.03 = $0.5562, or D1 = $0.54 11,020,801/10,699,807 = $0.5562 PV = $0.5562 / (0.13 − 0.03) = $5.56 Expected rates of return Shares = D 1 / P0 + g Example If the share in the previous example has a current market price of $5.02, what is its expected rate of return? Answer D 1 / P0 + g = 0.5562/5.02 + 0.03 = 14.08% Is this share worth buying? Yes: its market price is below its intrinsic value and its expected rate of return is higher than its required rate of return. Bonds Expected return = yield to maturity = internal rate of return (IRR - interest symbol i on the calculator). The IRR is the discount rate that equates the PV of a bond’s future cash flows with its current market price. This rate can be identified either through a process of iteration or by using an electronic device such as a financial calculator or an Excel spreadsheet. Note that if the price of a bond is below its par value, its yield will be higher than its coupon rate, and vice-versa. Example 4

- 5. FIN211 03B A bond has a par value of $100, a coupon rate of 10.5% payable semi-annually and has 4.5 years to maturity. If its current price is $117.52, what is its expected rate of return? 5

- 6. FIN211 03B Answer Because the current market price is above par value, we know that the expected return must be less than the coupon rate. This calculation is best done using a financial calculator (or spreadsheet). The key strokes are: 9 n 117.52 +/- PV 5.25 PMT 100 FV COMP i x 2 = 6.00% Calculating bonds yields without a financial calculator If we know the price of a bond, we can calculate its yield to maturity (YTM); i.e. the discount rate that equates the present value of the bond’ s future cash flows with its current price. The textbook sometimes refers to a bond’s YTM as the bondholder’s expected rate of return. However, whether or not a bond’s YTM will be the rate of return actually realised by the bondholder will depend on the rate at which the bond’s coupons can be reinvested. Remember that a bond YTM is an annual percentage rate (APR), as opposed to an effective annual rate (EAR). Example What is the YTM of a three-year bond with a face value of $100 and a 14% coupon paid twice per year, if the price of the bond is $110.15? Solution The time line is shown below. -110.1 7 7 7 7 7 107 5 0 1 2 3 4 5 6 We need to find the value of i such that: 110.15 = For equations of this type there is no algebraic solution for i when the exponent is greater than 4. In all such cases an approximation method needs to be used for determining the value of i. The routine is a two-part process involving first using an equation for determining an approximate value of i and then using a solution algorithm to bring the approximate value of i closer and closer to its true value through 6

- 7. FIN211 03B successive iterations. This is the solution method used by electronic devices and may also be used manually. Using a financial calculator, the YTM in this example is easily found to be 10.00%. Using the Sharp EL-735, the key-strokes are: 6 n 110.15 +/- PV 7 PMT 100 FV COMP i × 2 = Without a financial calculator, the following equation defines an approximate bond YTM: Bond YTM (8) Where a = Vb/M 1 Applied to the current example, a = 110.15/100 1 = 0.1015. Equation (8) then defines an approximate yield of 10.007%, as follows: Bond YTM 0.100072 10.0072% In this case the approximation equation has yielded a reasonable result. But if we do not know that 10.00% is the actual YTM, we cannot assess the accuracy of 10.0072%. However, in all cases such as this we can obtain a better approximation of the actual YTM by using an appropriate solution algorithm, such as Newton's Method. Alternatively, if we designate the first approximation as ia, a second approximation, designated ib, can be defined in either of the following two ways: (1) ib = ia × (2) ib = where PVa = the present value of the bond’ s cash flows per dollar of bond when discounted at ia FVa = the future value of the bond’ s cash flows per dollar of bond when compounded at ia Using the first method, we find: 7

- 8. FIN211 03B PVa = $ + $1(1 + ia/m)-nm =$ + $1(1 + 0.100072/2)-6 = $0.355257543 + $0.746061907 = $1.1013 ib = 10.0072% × = 10.0054% Using the second method (which was developed by Chris Deeley in 2005), we find: FVa = FV of coupons per dollar of bond + $1 =$ + $1 = $0.14 + $1 = $0.14 3.4012645 + $1 = $1.476177 ib = = 0.10001466 = 10.001466% Either of the foregoing methods can be repeated until the actual YTM is identified when in = in 1 to the required degree of accuracy. The second method (“ Deeley’ s Method” ) is recommended, despite its greater complexity, on the grounds that it approaches the actual YTM far more quickly than the first method. Using Deeley’s Method, the second iteration gives us a YTM of 10.0006%, calculated as follows: FVb = FV of coupons per dollar of bond + $1 =$ + $1 8

- 9. FIN211 03B = $0.14 + $1 = $0.14 3.401019135 + $1 = $1.47614268 ic = = 0.100006 = 10.0006% Repeating this routine with 10.0006% as the reinvestment rate will confirm that the actual YTM is 10.00% (to two decimals). The following equation also confirms 10.00% as the actual YTM: Vb = = $7 = $7 5.075692 + $100 0.7462 = $35.53 + $74.62 = $110.15 = the given price of the bond. Note that although the method just demonstrated is of a type often described as one of trial and error, it is nevertheless a systematic routine of repetition or iteration. Each repetition of the routine will always generate a more accurate approximation of the YTM until the actual YTM is identified to the required degree of accuracy. It is, of course, your understanding of the concepts that is important, not that you can necessarily calculate the precise answer. Depending upon the nature of the question, it is often sufficient to calculate a range within which the YTM falls. Nevertheless, now that you’ve seen the hassles involved in calculating a YTM without a financial calculator, you may appreciate the value of having one, and knowing how to use it. Preference shares Expected return = D / P0 Example 9

- 10. FIN211 03B A preference share has a par value of $100 and a dividend rate of 10.5% payable annually. If its current price is $117.52, what is its expected rate of return? Answer 10.5 / 117.52 = 8.9% Financial calculations without using a financial calculator Rate of interest If $1 grows to $10 over 10 years, what is the rate of interest? Ans. i = 101/10 1 = 0.2589 = 25.89% Check: $1 (1.2589)10 = $1 9.998 = $10.00 10

- 11. FIN211 03B Number of periods If $1 grows to $10 at 10% pa, how long does it take? Ans. n = log 10/ log 1.1 = 24.16 years Check: $1 (1.1)24.16 = $1 10.0011 = $10.00 Calculating periodic payments when paying off a debt or saving for a future amount, without using a financial calculator or tables Paying off a debt A debt which is paid off in equal periodic instalments may be referred to as a credit foncier loan. It is a present value (PV) that needs to be paid off and the amount of each instalment (or payment) can be calculated by dividing the PV by equation 4-12a, which is on page 79 of the text. Note that this is a ‘double-decker’ equation in which i is the denominator. Because the PV (the numerator) is to be divided by this equation, the equation should be inverted and then multiplied by the PV. Example See problem 4-15 at page 98. Payment (PMT) = 60,000 0.09/(1 1.09-25) = 60,000 0.10180625 = $6,108.38 Saving for a future amount It is a future value (FV) that needs to be saved for and the amount of each instalment (or payment) can be calculated by dividing the FV by equation 4-11a, which is on page 81 of the text. Note that this is a ‘double-decker’ equation in which i is the denominator. Because the FV (the numerator) is to be divided by this equation, the equation should be inverted and then multiplied by the FV. Example See problem 4-18 at page 98. Payment (PMT) = 100,000 1.0510 0.1/(1.110 − 1) = 162,889.46 0.62745394 = $10,220.56 Note that the first part of this answer calculates the expected future value of the property, which is expected to increase in value at the rate of 5% per year for 10 years. 11

- 12. FIN211 03B Note also that with this sort of calculation, you should not round-off until completion of the calculation. 12