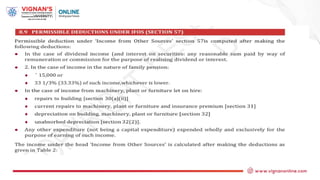

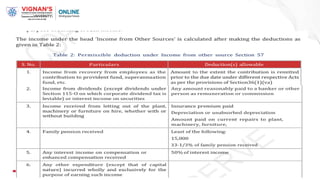

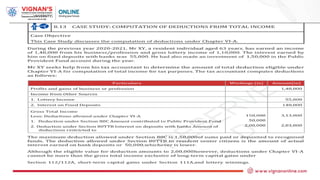

Title of theUnit

Unit 8: Income from Other Sources (Section 56 to 59) Incomes

3.

• Income fromOther Sources (Section 56 to 59) Incomes Taxable under

the head Income from Other Sources, Incomes Taxable under this head

if not taxable under PGBP, Taxation of Dividends, Casual Income

Section 56(2) (ib), Interest Received on Securities Section 56 (2)(id),

Gross up Concept, Taxation of Gift Section 56 (2)(x), Interest on

Compensation for Compulsory Acquisition of L&B Section 56 (viii),

Permissible Deductions under IFOS Section 57, Inadmissible

Deductions from IFOS Section 58

5.

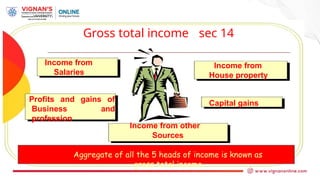

Gross total incomesec 14

Income from

Salaries

Income from

House property

Profits and gains of

Business and

profession

Capital gains

Income from other

Sources

Aggregate of all the 5 heads of income is known as

gross total income

6.

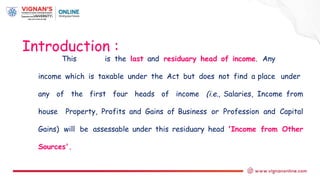

This is thelast and residuary head of income. Any

income which is taxable under the Act but does not find a place under

any of the first four heads of income (i.e., Salaries, Income from

house Property, Profits and Gains of Business or Profession and Capital

Gains) will be assessable under this residuary head 'Income from Other

Sources'.

Introduction :

7.

Basis of Charge: [ Sec 28 ]

Income from Other Sources

Charging Section

Sec 56 (1)

There is an income

Income is not exempt From tax

Such income is not

Chargeable under

Salary, HP. PGBP & Capital Gains

8.

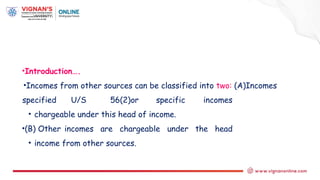

•Introduction….

•Incomes from othersources can be classified into two: (A)Incomes

specified U/S 56(2)or specific incomes

• chargeable under this head of income.

•(B) Other incomes are chargeable under the head

• income from other sources.

9.

(A) SPECIFIC INCOMESCHARGEABLE UNDER THIS HEAD OF INCOME

[Sec. 56(2)]

The following incomes shall be chargeable to income tax under the head

'Income from Other Sources' :

(1) Dividends.

(2)Income from winnings from lotteries, crossword puzzles, races including horse races,

card games and other games of any sort or from gambling or betting of any form or nature

whatsoever. •

(3)Any sum received by the assessee from his employees as contributions to any provident

fund or superannuation fund or any fund set-up under

Employees' State Insurance Act, 1948.

(4) Income by way of interest on securities.

(5) Income from machinery, plant or furniture let on hire if the income is not

chargeable to income tax under the head 'Profits and Gains of Business or Profession'.

10.

(A) SPECIFIC INCOMESCHARGEABLE UNDER THIS HEAD OF INCOME

[Sec. 56(2)]

(6)Income from letting on hire machinery, plant or furniture and also buildings, and

the letting of the buildings is inseparable from

the letting of the said machinery, plant or furniture, if it is not chargeable to income

tax under the head 'Profits and Gains of Business or Profession'.

(7)Income received under a Keyman insurance policy including bonus on such

policy, if such income is not chargeable to income tax under the head 'Profits and

Gains of Business or Profession'

or under the head 'Salaries'.

(8) Sum of money in excess of Rs.50,000/- received without consideration.

(Gifts)

11.

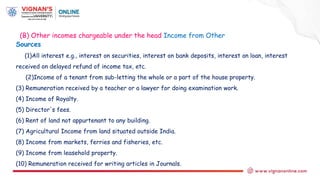

Sources

(1)All interest e.g.,interest on securities, interest on bank deposits, interest on loan, interest

received on delayed refund of income tax, etc.

(2)Income of a tenant from sub-letting the whole or a part of the house property.

(3) Remuneration received by a teacher or a lawyer for doing examination work.

(4) Income of Royalty.

(5) Director's fees.

(6) Rent of land not appurtenant to any building.

(7) Agricultural Income from land situated outside India.

(8) Income from markets, ferries and fisheries, etc.

(9) Income from leasehold property.

(10) Remuneration received for writing articles in Journals.

(B) Other incomes chargeable under the head Income from Other

12.

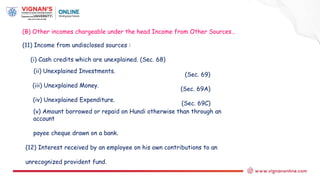

(B) Other incomeschargeable under the head Income from Other Sources…

(11) Income from undisclosed sources :

(i) Cash credits which are unexplained. (Sec. 68)

(ii) Unexplained Investments.

(iii) Unexplained Money.

(iv) Unexplained Expenditure.

(Sec. 69)

(Sec. 69A)

(Sec. 69C)

(v) Amount borrowed or repaid on Hundi otherwise than through an

account

payee cheque drawn on a bank.

(12) Interest received by an employee on his own contributions to an

unrecognized provident fund.

13.

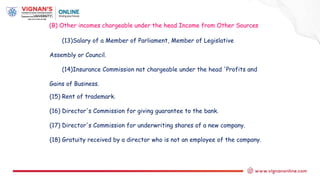

(B) Other incomeschargeable under the head Income from Other Sources

(13)Salary of a Member of Parliament, Member of Legislative

Assembly or Council.

(14)Insurance Commission not chargeable under the head 'Profits and

Gains of Business.

(15) Rent of trademark.

(16) Director's Commission for giving guarantee to the bank.

(17) Director's Commission for underwriting shares of a new company.

(18) Gratuity received by a director who is not an employee of the company.

14.

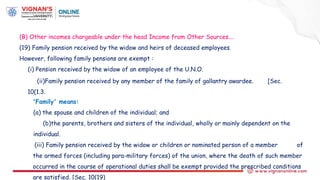

(B) Other incomeschargeable under the head Income from Other Sources….

(19) Family pension received by the widow and heirs of deceased employees.

However, following family pensions are exempt :

(i) Pension received by the widow of an employee of the U.N.O.

(ii)Family pension received by any member of the family of gallantry awardee. [Sec.

10(1.3.

'Family' means:

(a) the spouse and children of the individual; and

(b)the parents, brothers and sisters of the individual, wholly or mainly dependent on the

individual.

(iii) Family pension received by the widow or children or nominated person of a member of

the armed forces (including para-military forces) of the union, where the death of such member

occurred in the course of operational duties shall be exempt provided the prescribed conditions

are satisfied. [Sec. 10(19)

15.

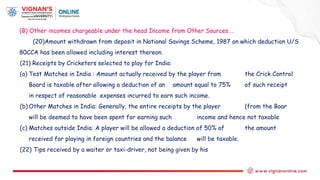

(B) Other incomeschargeable under the head Income from Other Sources….

(20)Amount withdrawn from deposit in National Savings Scheme, 1987 on which deduction U/S

80CCA has been allowed including interest thereon.

(21) Receipts by Cricketers selected to play for India:

(a) Test Matches in India : Amount actually received by the player from the Crick Control

Board is taxable after allowing a deduction of an amount equal to 75% of such receipt

in respect of reasonable expenses incurred to earn such income.

(b) Other Matches in India: Generally, the entire receipts by the player (from the Boar

will be deemed to have been spent for earning such income and hence not taxable

(c) Matches outside India: A player will be allowed a deduction of 50% of the amount

received for playing in foreign countries and the balance will be taxable.

(22) Tips received by a waiter or taxi-driver, not being given by his

16.

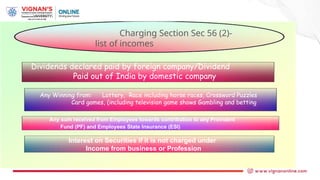

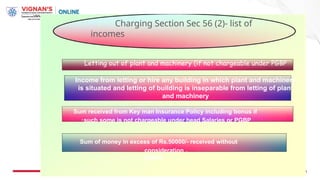

Charging Section Sec56 (2)-

list of incomes

Dividends declared paid by foreign company/Dividend

Paid out of India by domestic company

Any Winning from: Lottery, Race including horse races, Crossword Puzzles

Card games, (including television game shows Gambling and betting

Any sum received from Employees towards contribution to any Provident

Fund (PF) and Employees State Insurance (ESI)

Interest on Securities if it is not charged under

Income from business or Profession

17.

Charging Section Sec56 (2)- list of

incomes

Letting out of plant and machinery (if not chargeable under PGBP

Income from letting or hire any building in which plant and machinery

is situated and letting of building is inseparable from letting of plant

and machinery

Sum received from Key man Insurance Policy including bonus if

•such some is not chargeable under head Salaries or PGBP

Sum of money in excess of Rs.50000/- received without

consideration .

(Gifts)

18.

Dividends:

Meaning of Dividendin

received by a shareholder of a company on the distribution

of its profits, whether out of taxable income or tax-free

income.It is immaterial whether it is received in cash or in

kind.

common

ordinary language, dividend means

use:

In the

sum

19.

Definition of Dividend:[Sec. 2(22)] The following distributions or payments by a company

to its shareholders are deemed .as dividends to the extent of accumulated profits of the

company:

(a) Any distribution which entails the release of all or any of the assets of the

company;

(b) Any distribution of debentures or deposit certificates or bonus shares

to preference shareholders;

(c) Any distribution on its liquidation;

(d) Any distribution on the reduction of its capital;

(e) Any payment by a closely-held company by way of advance or loan to a

shareholder (being a person who is the beneficial owner of shares) having at least 10%

of the voting power or to any concern in which such shareholder is a member or a

partner and in which he has a substantial interest.

If trade advance is given to shareholder or concern out of accumulated profits, it

20.

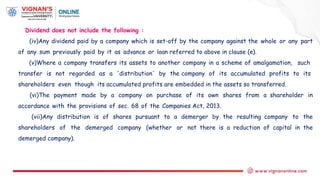

Dividend does notinclude the following :

(iv)Any dividend paid by a company which is set-off by the company against the whole or any part

of any sum previously paid by it as advance or loan referred to above in clause (e).

(v)Where a company transfers its assets to another company in a scheme of amalgamation, such

transfer is not regarded as a 'distribution' by the company of its accumulated profits to its

shareholders even though its accumulated profits are embedded in the assets so transferred.

(vi)The payment made by a company on purchase of its own shares from a shareholder in

accordance with the provisions of sec. 68 of the Companies Act, 2013.

(vii)Any distribution is of shares pursuant to a demerger by the resulting company to the

shareholders of the demerged company (whether or not there is a reduction of capital in the

demerged company).

21.

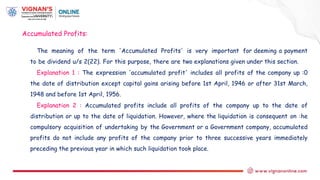

The meaning ofthe term 'Accumulated Profits' is very important for deeming a payment

to be dividend u/s 2(22). For this purpose, there are two explanations given under this section.

Explanation 1 : The expression 'accumulated profit' includes all profits of the company up :0

the date of distribution except capital gains arising before 1st April, 1946 or after 31st March,

1948 and before 1st April, 1956.

Explanation 2 : Accumulated profits include all profits of the company up to the date of

distribution or up to the date of liquidation. However, where the liquidation is consequent on :he

compulsory acquisition of undertaking by the Government or a Government company, accumulated

profits do not include any profits of the company prior to three successive years immediately

preceding the previous year in which such liquidation took place.

Accumulated Profits:

22.

Thus, if acompany goes into liquidation on 30th September, 2019 on account of compulsory

acquisition of the accumulated profits prior to 1.4.2016 shall not be included in accumulated profits

for clause (c) of section 2(22).

Explanation 2A : Accumulated profits or loss of amalgamating company

(whether capitalised or not) on the date of amalgamation, shall be included in

the accumulated profits of amalgamated company.'

Accumulated Profits:

23.

Some other aspectsrelating to Dividends

(1) Normal Dividend: Any dividend declared by a company at its annual general meeting shall be

deemed to be the income of the previous year in which it is so declared. It is a normal dividend.

[Sec. 8(a)]

(2)Deemed Dividend: Deemed dividend u/s 2(22) is deemed to be the income of the previous

year in which it is so distributed or paid.

(3) Interim Dividend: An interim dividend is one which is declared by a company at any time prior to

its annual general meeting for the year. Any interim dividend shall be deemed to be the income of the

previous year in which the amount of such dividend is unconditionally made available by the

company to the member who is entitled to it. It means that the date of declaration of such dividends

is immaterial so long as the amount is not released for disbursement. [Sec. 8(b)]

(4)Place of accrual: Under section 9( l)(iv), the dividend paid by an Indian company outside India

shall be deemed to accrue or arise in India.

24.

Some other aspectsrelating to Dividends….

(5)Dividend paid by a foreign company outside India is not deemed to accrue or

arise in India.

(6)In the case of dividend received by an Indian shareholder from a foreign

company which has deducted tax at source; but has not paid the deducted amount of

tax to the Government of India, the amount deducted as tax at source shall not be

included in the dividend income of the Indian

shareholder.

However, where the assessee is entitled to double taxation relief'(u/s 91), the

gross dividend shall be included in income. [CIT VB. Amalgamations

Ltd. (1998) 232 ITR 608 (Mad.)]

(7)If dividend for several years is declared in some later year and paid in lump-

sum in that later year, the dividend shall be deemed to be the income of the

previous year in which they are declared.

25.

Taxation of Dividends(the Assessment Year 2020 - 21)

•(1) Dividends (including deemed dividends) distributed by a domestic company: Sec. 115BBDA and

1115-0.

(2) Dividends from a Co-operative Society : The amount received as dividends from the Co-

operative Society shall be included in the income. However, the co-operative society is not

empowered to deduct tax at source. Hence, the question of grossing up of dividends does not arise.

(3) Dividends from a Foreign Company: The dividend received from a foreign company is to be

included 'net' in the income. However, where an assessee claims double taxation relief, the gross

amount shall be included in income. [Sec. 8(b)]

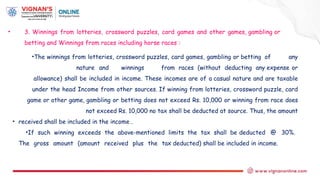

26.

• 3. Winningsfrom lotteries, crossword puzzles, card games and other games, gambling or

betting and Winnings from races including horse races :

•The winnings from lotteries, crossword puzzles, card games, gambling or betting of any

nature and winnings from races (without deducting any expense or

allowance) shall be included in income. These incomes are of a casual nature and are taxable

under the head Income from other sources. If winning from lotteries, crossword puzzle, card

game or other game, gambling or betting does not exceed Rs. 10,000 or winning from race does

not exceed Rs. 10,000 no tax shall be deducted at source. Thus, the amount

• received shall be included in the income .

•If such winning exceeds the above-mentioned limits the tax shall be deducted @ 30%.

The gross amount (amount received plus the tax deducted) shall be included in income.

![Basis of Charge : [ Sec 28 ]

Income from Other Sources

Charging Section

Sec 56 (1)

There is an income

Income is not exempt From tax

Such income is not

Chargeable under

Salary, HP. PGBP & Capital Gains](https://image.slidesharecdn.com/unit-8incoth-250426135631-1136a954/85/UNIT-8-INCoth-pptxfgdvvxcadxccccffffffff-7-320.jpg)

![(A) SPECIFIC INCOMES CHARGEABLE UNDER THIS HEAD OF INCOME

[Sec. 56(2)]

The following incomes shall be chargeable to income tax under the head

'Income from Other Sources' :

(1) Dividends.

(2)Income from winnings from lotteries, crossword puzzles, races including horse races,

card games and other games of any sort or from gambling or betting of any form or nature

whatsoever. •

(3)Any sum received by the assessee from his employees as contributions to any provident

fund or superannuation fund or any fund set-up under

Employees' State Insurance Act, 1948.

(4) Income by way of interest on securities.

(5) Income from machinery, plant or furniture let on hire if the income is not

chargeable to income tax under the head 'Profits and Gains of Business or Profession'.](https://image.slidesharecdn.com/unit-8incoth-250426135631-1136a954/85/UNIT-8-INCoth-pptxfgdvvxcadxccccffffffff-9-320.jpg)

![(A) SPECIFIC INCOMES CHARGEABLE UNDER THIS HEAD OF INCOME

[Sec. 56(2)]

(6)Income from letting on hire machinery, plant or furniture and also buildings, and

the letting of the buildings is inseparable from

the letting of the said machinery, plant or furniture, if it is not chargeable to income

tax under the head 'Profits and Gains of Business or Profession'.

(7)Income received under a Keyman insurance policy including bonus on such

policy, if such income is not chargeable to income tax under the head 'Profits and

Gains of Business or Profession'

or under the head 'Salaries'.

(8) Sum of money in excess of Rs.50,000/- received without consideration.

(Gifts)](https://image.slidesharecdn.com/unit-8incoth-250426135631-1136a954/85/UNIT-8-INCoth-pptxfgdvvxcadxccccffffffff-10-320.jpg)

![Definition of Dividend: [Sec. 2(22)] The following distributions or payments by a company

to its shareholders are deemed .as dividends to the extent of accumulated profits of the

company:

(a) Any distribution which entails the release of all or any of the assets of the

company;

(b) Any distribution of debentures or deposit certificates or bonus shares

to preference shareholders;

(c) Any distribution on its liquidation;

(d) Any distribution on the reduction of its capital;

(e) Any payment by a closely-held company by way of advance or loan to a

shareholder (being a person who is the beneficial owner of shares) having at least 10%

of the voting power or to any concern in which such shareholder is a member or a

partner and in which he has a substantial interest.

If trade advance is given to shareholder or concern out of accumulated profits, it](https://image.slidesharecdn.com/unit-8incoth-250426135631-1136a954/85/UNIT-8-INCoth-pptxfgdvvxcadxccccffffffff-19-320.jpg)

![Some other aspects relating to Dividends

(1) Normal Dividend: Any dividend declared by a company at its annual general meeting shall be

deemed to be the income of the previous year in which it is so declared. It is a normal dividend.

[Sec. 8(a)]

(2)Deemed Dividend: Deemed dividend u/s 2(22) is deemed to be the income of the previous

year in which it is so distributed or paid.

(3) Interim Dividend: An interim dividend is one which is declared by a company at any time prior to

its annual general meeting for the year. Any interim dividend shall be deemed to be the income of the

previous year in which the amount of such dividend is unconditionally made available by the

company to the member who is entitled to it. It means that the date of declaration of such dividends

is immaterial so long as the amount is not released for disbursement. [Sec. 8(b)]

(4)Place of accrual: Under section 9( l)(iv), the dividend paid by an Indian company outside India

shall be deemed to accrue or arise in India.](https://image.slidesharecdn.com/unit-8incoth-250426135631-1136a954/85/UNIT-8-INCoth-pptxfgdvvxcadxccccffffffff-23-320.jpg)

![Some other aspects relating to Dividends….

(5)Dividend paid by a foreign company outside India is not deemed to accrue or

arise in India.

(6)In the case of dividend received by an Indian shareholder from a foreign

company which has deducted tax at source; but has not paid the deducted amount of

tax to the Government of India, the amount deducted as tax at source shall not be

included in the dividend income of the Indian

shareholder.

However, where the assessee is entitled to double taxation relief'(u/s 91), the

gross dividend shall be included in income. [CIT VB. Amalgamations

Ltd. (1998) 232 ITR 608 (Mad.)]

(7)If dividend for several years is declared in some later year and paid in lump-

sum in that later year, the dividend shall be deemed to be the income of the

previous year in which they are declared.](https://image.slidesharecdn.com/unit-8incoth-250426135631-1136a954/85/UNIT-8-INCoth-pptxfgdvvxcadxccccffffffff-24-320.jpg)

![Taxation of Dividends (the Assessment Year 2020 - 21)

•(1) Dividends (including deemed dividends) distributed by a domestic company: Sec. 115BBDA and

1115-0.

(2) Dividends from a Co-operative Society : The amount received as dividends from the Co-

operative Society shall be included in the income. However, the co-operative society is not

empowered to deduct tax at source. Hence, the question of grossing up of dividends does not arise.

(3) Dividends from a Foreign Company: The dividend received from a foreign company is to be

included 'net' in the income. However, where an assessee claims double taxation relief, the gross

amount shall be included in income. [Sec. 8(b)]](https://image.slidesharecdn.com/unit-8incoth-250426135631-1136a954/85/UNIT-8-INCoth-pptxfgdvvxcadxccccffffffff-25-320.jpg)