1. Company Report

Banking Sector

19 July 2012

Sustainable Banking…

Derya Guzel

Research Analyst

dguzel@sekeryatirim.com

Advantageous funding ability...Low cost & long

term funding enables the bank to execute long term

lending, and hence less volatile loan yields should

result in resilient NIM, in our view. It is no

coincidence that medium and long term loans

account for 88.7% of TSKB’s total lending book, but

rather, part of a sustainable strategy. TSKB matches

funding with lending, and thus has no currency and

maturity mismatch on its loan book. We expect TSKB

to be one of the players within the Turkish banking

universe to maintain its NIM above 4%, at least over

the next two years, and it should even subsequently

be able to extend margins. We forecast 4.2% NIM in

2012 and estimate a sustainable NIM level of 4%

thereafter. Thanks to its long-standing relationships

with multilateral agencies backed by Turkish

Treasury Guarantee, TSKB has had the ability to

borrow funds even during crises. In 2009 it was able

to borrow USD 1,039mn from multilateral agencies in

total. The only risk in our view is the need to find

the right loan segments and project finance deals to

channel funds.

Superior asset quality... With a 0.40% NPL ratio

TSKB has the lowest NPL’s within the sector, vs. the

sector’s 2.7% NPL ratio (based on weekly BRSA data

as of 22nd June’12). TSKB’s superior asset quality is

mainly due to: 1) An extensive knowledge of the loan

segments the bank operates 2) Its involvement

throughout the project financing life cycle, and its

provision of advice to borrowers, hence any risk of

asset quality problems being discovered at an earlier

stage, 3) And finally a lack of exposure to retail

lending (i.e credit cards or mortgages).

Successful track record in delivering highest ROE...

TSKB has been one of the highest ROE earners of the

banking sector. Between 2005 and 2011 it managed

to deliver average ROE of 19.3% to its investors. And

we estimate it ending 2012 above 20% ROE followed

by 19.2% and 19% in 2013F and 2014F, respectively.

Valuation, recommendatation and risks... We rate

TSKB “Outperform” with a 12M target price of

TRY2.42. The stock trades on PBR of 1.29x and PER

of 6.8x on our 2012 estimate. Slower than expected

GDP growth is a downside risk to our loan growth,

earnings and NPL estimates, whereas moving into the

infrastructure segment is an upside risk to our loan

growth estimate as there are several still incomplete

infrastructure privatisation deals in the PA’s

pipeline.

TSKB- Türkiye Sinai Kalkınma Bankası

Şeker Securities Research

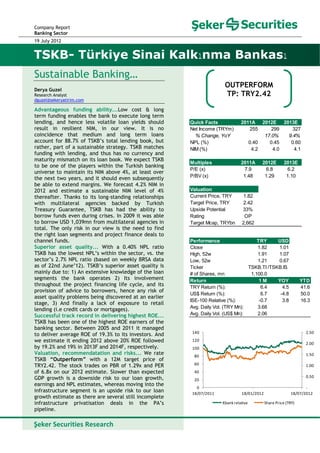

OUTPERFORM

TP: TRY2.42

‐

0.50

1.00

1.50

2.00

2.50

0

20

40

60

80

100

120

140

18/07/2011 18/01/2012 18/07/2012

Xbank relative Share Price (TRY)

Performance TRY USD

Close 1.82 1.01

High, 52w 1.91 1.07

Low, 52w 1.21 0.67

Ticker

# of Shares, mn 1,100.0

Return 1 M YOY YTD

TRY Return (%): 6.4 4.5 41.6

US$ Return (%): 6.7 -4.8 50.0

ISE-100 Relative (%): -0.7 3.8 16.3

Avg. Daily Vol. (TRY Mn): 3.68

Avg. Daily Vol. (US$ Mn): 2.06

TSKB.TI /TSKB.IS

Quick Facts 2011A 2012E 2013E

Net Income (TRYm) 255 299 327

% Change, YoY 17.0% 9.4%

NPL (%) 0.40 0.45 0.60

NIM (%) 4.2 4.0 4.1

Multiples 2011A 2012E 2013E

P/E (x) 7.9 6.8 6.2

P/BV (x) 1.48 1.29 1.10

Valuation

Current Price, TRY 1.82

Target Price, TRY 2.42

Upside Potential 33%

Rating OP

Target Mcap, TRYbn 2,662

2. 19 July 2012

Banking Sector | TSKB P a g e | 1

Investment Case

Low cost & long term funding allows the bank to lend at long term, and hence less

volatile loan yields should result in resilient NIM, while having no retail lending

exposure provides further margin immunity in our view. It is no coincidence that

medium and long term loans account for 88.7% of TSKB’s total lending book, but

rather part of a sustainable banking strategy. TSKB matches funding through

lending, and hence has no currency and maturity mismatch on its loan book. We

expect TSKB to be one of the players within the Turkish banking universe to

maintain its NIM level above 4%, at least over the next two years, and even to be

able to subsequently extend margins.

TSKB has one the highest ROE ratios among our banks coverage after Halkbank.

Between the years of 2005-2011 it managed to delivery its investors an average

ROE of 19.3%. We estimate TSKB ending 2012 above 20% ROE followed by 19.2%

and 19.0% in 2013F and 2014F, respectively. We expect our 20% ROE estimate in

2012F to be driven by 1) 16% loan growth in local currency terms, 2) estimated

4.2% NIM for 2012 and 4.0% sustainable NIM level thereafter, 3) 14% net interest

income growth, 4) 0.45% NPL ratio, 5) 10% fee growth and 6) opex growth of

around 9%.

Robust asset quality: the best within the sector....

With a 0.40% NPL ratio TSKB has the lowest NPL’s within the Banking sector in

Turkey, vs. the sector’s 2.7% (based on weekly BRSA data as of 22nd

June’12).

TSKB’s high NPL ratio from 2001 until 2004 was due to a legacy NPL portfolio

acquired via Isbank group companies. However, as of 2004 TSKB’s NPL ratio

evolution has fallen short of the banking sector. TSKB’s NPL ratio from 2008 to

Mar’12 averaged at 0.53%, one of the lowest in the sector.

TSKB has superior asset quality mainly due to: 1) Its extensive knowledge of the

segments it operates in, 2) its involvement throughout the project financing life

cycle and offering advice to borrowers, hence earlier capture of any asset quality

risks, 3) And finally a lack of exposure to retail lending (credit cards or

mortgages).

Figure 1: TSKB quarterly NPL ratio (%) evolution vs. sector

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Sector TSKB

TSKB has the lowest

NPL ratio in the

sector (TSKB 0.4%

vs. 2.7% sector)

Source: BRSA

3. 19 July 2012

Banking Sector | TSKB P a g e | 2

A better than sector NPL ratio may raise questions over its sustainability. However,

we believe that as the bank is not active in the retail segment the risk of sharp

NPL ratio deterioration is minimal. We expect TSKB to end the year with a 0.45%

NPL ratio, vs. our 3.2% expectation for the Turkish Banking sector. The downside

risk to our NPL ratio is that since TSKB’s ticket size in lending is quite large when

compared to the sector (especially in project finance), the addition of just one

corporate file to NPL would increase the NPL ratio sharply.

The Bank has a 100% provisioning policy for all non-performing loans regardless of

collateral attached to the loan. TSKB has had no NPL write-off or sale policy for

the past twenty years, and our impression from meetings with the bank is that it

has no plans to change its policy going forward.

Lending portfolio: long term & FX loans concentrated

Its aim, as a Turkish industrial Development Bank, is to assist enterprises in all

sectors, but with special emphasis on the industrial sector. Given this special focus

the bank is able to obtain long term & low cost funds from financial institutions. The

joint aim of these multilateral agencies is to offer financial aid to emerging market

economies, including Turkey. In that sense, TSKB is effectively an intermediary

between Turkish companies and multilaterals, hence funds borrowed by it from

these agencies receive a Turkish Treasury guaranty.

35% of TSKB’s total loan book as of March-2012 consists of loans provided to the

energy generation sector. In line with its overall mission of becoming the leading

financer of the renewable energy sector, the bank as of 2009 included energy

efficiency project financing in its portfolio. Indeed, as of end-Dec-11 it had financed

a total of 93 renewable energy projects. However, at our meetings with TSKB

management they have emphasized that going forward the focus would be on

infrastructure projects as the segment attracts more investors and offers long-term

business prospects. Please remember that based on the data published by the

Central Bank of the Republic of Turkey (CBT), Turkey’s privatisation efforts have

generated USD 44bn over the past eight years, and that there are numerous areas

i.e. Infrastructure and energy generation which remain partially executed.

Figure 2: Sectoral distribution of TSKB’s loan book

35%

13%

10%

9%

7%

7%

6%

6%

5%

4%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Energy production

Finance

Other

Logistics

Non‐residential Real Estate

Metal and machinery

Electricity/Gas distribution

Chemistry and Plastics

Construction

Tourism

Source: Company data

APEX lending: TSKB is

acting as an

intermediary between

Turkish companies

and multilateral

agencies

4. 19 July 2012

Banking Sector | TSKB P a g e | 3

TSKB also has a unique way of lending to SMEs, namely APEX lending, whereby the

Bank operates as an agent between banks and multilateral agencies, whereby it

carries no NPL risk. And considering that the SME segment is one of the highest NPL

generators within the lending book in times of economic downturn, no direct

exposure to SMEs (in TSKBs case via Apex lending) provides an extra support to the

NPL ratio. Currently, 11% of TSKB’s total loan book comprises APEX loans, down from

18% in 2010. This year the bank obtained a USD300mn loan via the European

Development Bank for use in APEX lending, and we expect TSKB to use at least

USD200mn of it this year. Hence, we anticipate a slight increase in Apex lending

over the coming quarters.

In 2009 with the issuance of a Turkish Lira corporate bond the bank was able to lend

in local currency. Yet as there is currently no demand for Turkish Lira loans, TSKB is

inactive in such lending. However, we believe that with the rates on a gradual

decline there might be a business opportunity for TSKB to engage in long term local

currency borrowing and lending.

As of March’12 98% of TSKB’s loan book is foreign currency dominated, hence the

bank doesn’t carry any currency mismatch, unlike others. When considering the FX

lending portfolio in detail we see that 44% of total lending is in EUR and 54% in USD,

and that the lending portfolio has an average maturity of 5 years.

It is no coincidence that medium and long term loans account for 88.7% of TSKB’s

total lending book, but rather a part of its sustainable banking strategy. As of Dec-

11, 11.3% of the bank’s loan portfolio comprised loans of less than one year (down

from 14.9% a year earlier), 41.9% of loans are up to 5 years and 38.1% were longer

than 5 years, with 8.7% having maturities of over 10 years. The share of loans of

over 10 year maturity within the total loan book has been rising steadily over the

years (to 8.7% in 2011 from 4.7% in 2009).

Figure 3: Loan book maturity as of Mar’12 Figure 4: Funding maturity as of Mar’12

46.8% of loan book

consists of loans up

to longer than 5

years

46.8% of loan book

consists of loans of

longer than 5 year

maturity

Further increase in

Apex lending over

coming quarters

TSKB may become

more active in local

currency lending

going forward with

favorable rates

Demand

0%

Upto 1m

5%

1‐3m

4% 3‐12m

6%

1‐5yrs

35%

5yrs +

50%

Source: Company data, Seker estimates

Demand

0%

Upto 1m

2%

1‐3m

4%

3‐12m

16%

1‐5yrs

57%

5yrs +

21%

Source: Company data, Seker estimates

98% of TSKB’s LT

loan portfolio is FX

dominated

5. 19 July 2012

Banking Sector | TSKB P a g e | 4

Funding Structure: “Long Term & Low Cost Funding”

Of total funds borrowed, 93% are long term funds. As of 1Q’12 TSKB has USD3,525mn

of long term and USD282mn of short term funds available for utilization. Since 2009,

total funding agreements TSKB has signed amount to USD1,895mn. Short terms funds

are made up of syndication loan agreements and money market instruments.

Due to its investment and development bank status, TSKB by law is not permitted to

collect deposits, but rather, is able to obtain long term & low cost funds from

multilateral financial institutions such as World Bank (IBRD), European Investment

Bank (EIB), Council of Europe Development Bank (CEB), Kreditanstalt für

Wiederaufbau (KfW), Agence Francaise de Developpement (AFD), International

Finance Corporation (IFC) and European Bank for Reconstruction and Development

(EBRD). The joint aim of these multilateral agencies is to offer financial aid to

emerging market economies, including Turkey. In that sense TSKB acts as an

intermediary between Turkish companies and the above-mentioned agencies, which

means that 100% of long term funds obtained via multilateral agencies are Treasury

guaranteed.

Thanks to its long standing relations with multilateral agencies and Turkish Treasury

Guarantee, TSKB has enjoyed the ability to borrow funds even in times of crisis. In

2009 the bank was able to borrow USD1,039mn in total from multilateral agencies.

The sole risk in our view involves finding the right loan segments and project finance

deals to channel funds. As of March-2012 repo funding comprises 12% of TSKB’s

liabilities, with 65% made up of long term funds, 15% equity and the remaining 8%

other liabilities.

Figure 5: Multilateral funding agreements signed by year (USDm)

279

549

1,039

121

660

‐

200

400

600

800

1,000

1,200

2007 2008 2009 2010 2011

Since 2009 total

funding agreements

signed by TSKB

amount to

USD1,895mn.

Thanks to its long

standing relations,

TSKB has had the

ability to borrow

funds even during

crises.

Source: Company data, Seker estimates

6. 19 July 2012

Banking Sector | TSKB P a g e | 5

Since TSKB borrows long term in FX, (the average maturity of its long term funding

base is 12 years) and it lends long in FX (medium and long term loans account for

88.7% of TSKB’s total lending book), hence TSKB doesn’t carry maturity or currency

mismatch between its funds and loan book.

Figure 6: Duration of TSKB’s funding base Figure 7: Outstanding funding base (USDm)

Figure 8: TR Banks balance sheet maturity mismatch as at Mar-12

Akbank Garanti Halk Isbank Vakif YKB TSKB Akbank Garanti Halk Isbank Vakif YKB TSKB

Assets

Demand 15.1 7.5 2.1 17.6 11.6 8.3 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Upto 1m 17.4 22.5 8.2 23.6 6.1 16.5 0.3 0.1 0.1 0.0 0.1 0.0 0.1 0.0

1-3m 10.0 8.0 7.3 9.2 3.4 7.4 0.3 0.1 0.1 0.2 0.1 0.1 0.1 0.1

3-12m 18.6 13.2 23.3 25.3 14.2 18.1 1.5 1.0 0.7 1.8 1.2 1.1 1.3 1.2

1-5yrs 54.0 65.3 40.7 55.4 41.5 26.2 5.3 14.1 15.8 15.5 12.3 15.8 8.9 20.1

5yrs + 20.3 28.0 9.5 21.3 15.2 24.3 1.8 7.1 9.0 4.8 6.3 7.7 11.0 9.2

Not specified 2.1 4.2 3.4 10.2 2.8 5.1 0.3 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Total 137.7 148.6 94.5 162.6 94.6 106.0 9.5 22.4 25.7 22.4 19.9 24.7 21.4 30.5

Liabilities

Demand 9.7 16.4 16.1 17.2 8.9 12.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Upto 1m 64.3 71.7 43.6 78.1 47.0 44.1 1.4 0.2 0.2 0.2 0.2 0.2 0.2 0.1

1-3m 19.7 14.4 11.4 25.1 16.7 15.7 0.3 0.3 0.2 0.2 0.3 0.4 0.3 0.1

3-12m 14.5 10.9 9.3 12.9 6.9 9.2 0.4 0.8 0.6 0.7 0.6 0.5 0.6 0.3

1-5yrs 8.8 9.5 2.3 4.4 1.8 9.0 2.4 2.3 2.3 0.9 1.0 0.7 3.1 9.0

5yrs + 2.5 4.4 1.8 1.1 1.7 2.6 3.4 0.9 1.4 0.9 0.3 0.8 1.2 17.1

Not specified 18.2 21.3 9.9 23.7 11.7 13.3 1.7 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Total 137.7 148.6 94.5 162.6 94.6 106.0 9.5 4.5 4.7 3.0 2.5 2.7 5.4 26.5

18.0 21.0 19.4 17.4 22.0 16.0 4.1

TLbn Months

Maturity GAP

Long term

funding , 93%

Short term

funding, 7%

2,036

2,513

2,848

3,016

3,351

3,525

640

413

94

258 296 282

‐

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2007 2008 2009 2010 2011 1Q 2012

Long term funds Short term funds

Source: Company data Source: Company data

7. 19 July 2012

Banking Sector | TSKB P a g e | 6

Fee & Commission generation: we see limited growth potential...

The share of TSKB’s fee & commission business within total banking revenues, at

2% is rather small when compared to Tier 1 banks. TSKB’s main source of fee

income stems from non-cash lending activities, which account for around 69% of

fee & commission income.

Other contributors to fee & commission income are brokerage (19%), fund

management (4%), and the corporate finance business (8%). Due to the regulatory

cap on fund management fees, its share within total fee & commission income

declined to 4% in 1Q12 from 15% in 2010. Corporate finance related fees are also

subject to volatility depending on market conditions and GDP growth. Mainly

stemming from IPO and fixed income related deals, TSKB’s corporate finance

related fees fell to 8% in 1Q12 from 36% in 2010. Recall that in 2010 TSKB was

involved in a number of high profile IPOs, including Emlak REIT, the largest IPO of

2010, and the fifth largest in the ISE’s history.

As mentioned above, driven by corporate finance activities in 2010, TSKB managed

to grow its fee income base by 93.9%, although slower GDP growth decreases fee

income. We foresee TSKB growing its fee & commission income by 10.6% in 2012

driven mainly by non-cash loans.

We foresee limited growth in TSKB’s fee & commission income over the coming

few years. We forecast fee income stabilizing at around 3% of total banking

revenues from 2013F onwards, and the non-cash loan segment remaining the

largest contributor to fee income. The upside risk to our fee income estimate

would be TSKB involvement in another major IPO, or else further infrastructure

segment privatisation activities in the coming years.

Figure 9: Fee & commission income growth estimates

Fee & commission

income currently

accounts for 2% of

total banking

revenues.

We estimate fee

income stabilizing

at around 3% of

total banking

revenues from

2013F onwards

‐10.6 ‐9.9

‐36.1

‐19.9

81.5

93.9

‐26.8

10.6

11.4

23.0

‐60.0

‐40.0

‐20.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2005 2006 2007 2008 2009 2010 2011 2012F 2013F 2014F

Source: Company data, Seker estimates

8. 19 July 2012

Banking Sector | TSKB P a g e | 7

OPEX: Low cost to income due to lack of branch network

For the past three years, TSKB’s opex growth has averaged at 8%, and in 2011 the

bank managed meagre growth of 4% in this item. We estimate around 9% higher

costs for the bank in 2012F, and 13% in 2013F, mainly driven by HR costs. Staff-

related cost make up 62% of TSKB’s total operating expenditure as of March 2012.

Due to its corporate and development bank status TSKB doesn’t collect deposits,

or operate in the retail segment. Hence it has just 3 branches and a headquarters

based in Istanbul, and as of 1Q12 employs 347 personnel. Duly, TSKB’s cost to

income ratio of around 18% is well below the average of 50% for deposit banks.

Foreign ownership of free float

While during the crisis TSKB experienced some decline in its foreign ownership in

free float as of 2010, we now observe a steady rise in foreign interest in the stock.

As of June 2012, foreign ownership stands at 52.2%, vs. 51.8% in the same period a

year ago.

Figure 10: TKSB Expense ratios forecasts 2012-2014F

Figure 11: TSKB’s foreign ownership of free float 2005- March 2012 (%)

Expense ratios (%) 2010 2011 2012F 2013F 2014F

Cost/income 20.4 17.9 18.8 17.9 18.9

Cost/NII plus fees 20.1 17.3 18.4 17.7 18.8

Fees coverage of Opex 21.6 15.2 19.7 20.4 20.0

Cost/Total assets 0.9 0.7 0.8 0.7 0.7

Source: Company data and Seker estimates

Source: ISE and Company data

52.70%

49.40%

41.80% 41.50%

37.80%

53.40%

50.10%

52.20%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

As of Jun’12 the

foreign ownership of

TSKB’s free float

stands at 52.2%, vs.

51.8% in the same

period a year ago

HR cost makes up

62% of Opex in

March 2012

TSKB’s has a cost

income ratio of

around 18%, vs. 50%

in deposit banks

9. 19 July 2012

Banking Sector | TSKB P a g e | 8

Summary of 1Q’12 results

During 1Q12, TSKB announced net income of TRY 81mn, up +12% QoQ and +22%

YoY, thus beating the consensus estimate by 7%, driven by better than expected

net interest income (6% QoQ). Loan growth in EUR/USD basket terms came in at

4.5% QoQ. The bank managed to sustain its superior asset quality with no NPL

inflows during 1Q12, and its low NPL ratio of 0.4%, precluded the need to set aside

specific provisions.

Unlike the sector trend , TSKB managed to contain cost growth. Opex on a YoY

basis declined by 5% driven by non-HR cost. Accordingly, its cost to income ratio

improved to 14.5% from 18.0% a year ago.

CAR ratio improved by 30bps from a quarter ago to 19.4%, while ROE on a 12M

rolling basis came in at 19.9%, vs. 19.4% in Dec-11 and 18.8% in Mar-11.

Figure 12: 1Q’12 results summary

TSKB Bank-only results summary

Income Statement (TRYm) 1Q11 4Q11 1Q12 QoQ (%) YoY (%)

Gross interest income 124 137 143 4.6 15.5

Interest expense -36 -38 -39 2.1 9.3

Net interest income 88 99 104 6 18

Net fees 3 1 3 89.8 -26.1

Net trading and currency gains 1 -1 3 N/M 165.9

Revenues 93 99 110 10.2 18.1

Cost -17 -20 -16 -21.6 -4.9

Operating income 76 79 94 18.4 23.2

Other income 13 13 9 -29.9 -29.1

Provisions -7 -1 -4 N/M -52.6

Pre tax income 82 91 100 9.3 21.7

Taxes -15 -19 -18 -2.1 20.3

Net income 67 72 81 12.3 22.0

Balance Sheet (TRYm) Mar-11 Dec-11 Mar-12 QoQ (%) YoY (%)

Cash and liquid assets 112 121 175 44.7 56.3

AFS securities 2,130 2,321 2,601 12.1 22.1

HTM securities 308 127 0 N/M N/M

Customer loans 5,110 6,367 6,318 -0.8 23.6

Non performing loans 24 26 26 -0.6 7.9

Total assets 8,329 9,456 9,500 0.5 14.1

Borrow ed funds 5,267 6,779 6,605 -2.6 25.4

Shareholders' funds 1,279 1,366 1,436 5.2 12.3

Selected ratios (%) Mar-11 Dec-11 Mar-12 QoQ (%) YoY (%)

NIM 4.0 4.1 4.2 1.0 3.3

ROA 2.9 2.9 2.9 2.4 -0.1

ROE 18.5 19.4 19.9 2.7 7.8

LDR 97.0 93.9 95.7 1.9 -1.4

Leverage (x) 6.5 6.9 6.6 -4.5 1.6

Cost income 18.0 17.9 14.5 -19.0 -19.5

Fee coverage of cost 20.9 15.2 16.2 6.6 -22.3

Tier-1 CAR 18.1 17.0 17.1 1.0 -5.5

Total CAR 21.0 19.1 19.4 1.9 -7.5

NPL 0.5 0.4 0.4 0.1 -12.7

Cost of risk 0.6 0.1 0.2 N/M -63.0

Source: Company data, Seker estimates

10. 19 July 2012

Banking Sector | TSKB P a g e | 9

Valuation and Estimates

We use the residual earnings (RE) methodology to value TSKB and other banks

within our coverage when setting target prices. RE methodology can be viewed as

a dividend discount model. Residual earnings are the return on common equity,

expressed as a TL return, rather than a ratio. For each earnings period we restate

residual earnings as Residual Earnings = (Return on Equity – Cost of Equity)*BV per

share.

We rate the stock “Outperform” with a 12M target price of TRY2.42. There are

several reasons behind our recommendation (in order or importance):

1. We like TSKBs superior asset quality compared to sector,

2. Turkish Treasury guarantee ensures the bank has no funding constraints in

tighter liquidity periods, and the ability to borrow long term and low cost,

hence higher spreads,

3. We believe that the shift away from energy sector lending to

infrastructure is an upside risk to our loan growth estimate, as there are

several incomplete infrastructure privatisation deals in the pipeline,

4. TSKB has been one of the highest ROE earners of the banking sector.

Between 2005 and 2011 TSKB managed to deliver its investors an average

ROE of 19.3%. We estimate the bank delivering average 19.5% ROE in our

forecast period of 2012-2014F.

Figure 13: Target Price Model

Figure 14: TSKB bank only forecasts and ratios

Source: Company data, Seker estimates

Year to Dec 2007 2008 2009 2010 2011 2012F 2013F 2014F

Loans (TLm) 2,554 3,668 3,820 4,773 6,367 7,395 8,726 10,297

Revenue (TLm) 146 220 264 307 363 417 455 527

NII (TLm) 137 244 255 298 364 415 445 516

Net income (TLm) 147 119 175 212 255 299 327 378

BVPS (TL) 0.67 0.68 0.95 1.15 1.24 1.43 1.67 1.94

EPS (TL) 0.13 0.11 0.16 0.19 0.23 0.27 0.30 0.34

PER (x) 13.7 17.0 11.6 9.6 7.9 6.8 6.2 5.4

Yield (%) 0.00 0.00 1.48 1.56 1.88 2.27 2.66 2.90

PBR (x) 2.74 2.70 1.94 1.60 1.48 1.29 1.10 0.95

ROE (%) 22.2 16.0 18.7 18.0 19.4 20.3 19.2 19.0

TSKB Target Price assumption- Residual Earnings Estimate

2008 2009 2010 2011 2012F 2013F 2014F

EPS 0.11 0.16 0.19 0.23 0.27 0.30 0.34

DPS 0.04 0.02 0.03 0.04 0.05 0.05 0.06

BVPS 0.68 0.95 1.15 1.24 1.43 1.67 1.94

ROE 0.16 0.19 0.18 0.19 0.20 0.19 0.19

Cost of Equity 0.13 0.13 0.13 0.13 0.13 0.13 0.13

Growth in RE 0.47 0.21 0.21 0.17 0.09 0.09

13.3 % on RE 0.02 0.04 0.04 0.07 0.09 0.08 0.10

Present Value of RE 0.02 0.04 0.04 0.07 0.09 0.08 0.10

Total PV of RE 0.48

Continuing value (CV) 1.08

Present Value of CV 0.51

Target Price (TRY) 2.42

11. 19 July 2012

Banking Sector | TSKB P a g e | 10

TSKB Investor Multiples in Context

Figure 15: PBR (x) 2012F and 2013F

Figure 16: PER (x) 2012F and 2013F

Source: Company data, Seker estimates

Source: Company data, Seker estimates

1.65

1.47

1.36

1.29 1.27

1.15

1.07

0.90

1.37

1.28

1.20

1.10 1.11

1.00 0.97

0.82

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Halkbank Garanti Akbank TSKB Industry Yapi Kredi Isbank Vakifbank

2012F 2013F

10.1

9.0

8.6

8.3

7.9 7.7 7.6

6.8

8.5

7.7 7.5

7.1

6.5 6.7 6.7

6.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Akbank Garanti Isbank Industry Vakifbank Yapi Kredi Halkbank TSKB

2012F 2013F

12. 19 July 2012

Banking Sector | TSKB P a g e | 11

Company Profile

A bank on a “mission”

TSKB is Turkey’s only listed corporate and development bank, as well as its first

private investment and development institution. The bank was established in 1950

with World Bank assistance (its first CEO was also a World Bank veteran) along with

the collaboration of the Turkish Government, Central Bank of Turkey (CBT) and

leading domestic commercial banks.

The aim of the bank as a Turkish industrial development entity is to assist

enterprises across all sectors with special attention to industry. The bank also

facilitates domestic and international investment in local companies. As well as

providing financial support to companies, TSKB offers consultation, technical

support and sector expertise.

TSKB is the 16th

largest bank by asset size as of Mar’12. The banks’ headquarters is

located in Istanbul and it has only three other branches, in Ankara, Izmir, and

Bahrain (which is in the process of closing down). As of the end of 1Q12 TSKB

employs 347 personnel. The bank does not collect deposits, but funds itself via long-

term borrowings from multinational corporations.

Isbank Group companies own 50% of TSKB, while 8% is owned by Vakifbank and the

remaining 42% is traded on the ISE. Isbank has 8 members on TSKB’s board, while

Vakifbank is represented with one board member.

Figure 17: Ownership structure

Isbank

50%Free Float

42%

Vakifbank

8%

Detailed ownership %

Isbank 40.52%

Camis Yatırım Holding 5.80%

Milli Reasurans 1.90%

Anadolu Hayat Emeklilik 0.89%

Anadolu Sigorta 0.89%

Isbank Group 50.00%

Vakifbank 8.38%

Istanbul Ticaret Odası 0.52%

Istanbul Ticaret Borsası 0.21%

Istanbul Sanayii Odası 0.12%

Other 2.89%

Free Float 37.88%

TOTAL 100.00%

Source: Company data