IL SISTEMA BANCARIO BULGARO E UNICREDIT BULBANK

•Download as PPT, PDF•

1 like•811 views

Aldo AndreoniHead of International Department @Unicredit Bulbank Italian Festival in Bulgaria 2010 Forum economico “Bulgaria-Italia: insieme per uscire dalla crisi” Sofia, 7 giugno 2010

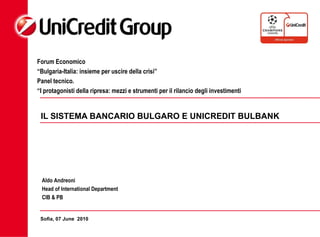

![Credit growth has stalled Bulgarian banking sector: Loans growth (Jun`2006 – Mar`2010, yoy) ,[object Object],[object Object],Source: BNB Bulgarian banking sector: Loans growth forecast (2007- 2015 f, yoy ) Source : BNB, UniCredit Bulbank forecast](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (8)

Similar to IL SISTEMA BANCARIO BULGARO E UNICREDIT BULBANK

Similar to IL SISTEMA BANCARIO BULGARO E UNICREDIT BULBANK (20)

More from Italian Festival

More from Italian Festival (6)

Recently uploaded

Recently uploaded (20)

IL SISTEMA BANCARIO BULGARO E UNICREDIT BULBANK

- 1. IL SISTEMA BANCARIO BULGARO E UNICREDIT BULBANK Sofia, 07 June 2010 Aldo Andreoni Head of International Department CIB & PB Forum Economico “ Bulgaria-Italia: insieme per uscire della crisi” Panel tecnico. “ I protagonisti della ripresa: mezzi e strumenti per il rilancio degli investimenti

- 4. Although indebtedness remain moderate for the economy as a whole, some deleveraging pressure is likely in the most overheated sectors such as real estate and construction. Source: NSI, UniCredit Bulbank Economic Research

- 6. Despite challenging profitability backdrop banks in Bulgaria continued cutting loan-to-deposit interest rate spread Loan-to-deposit interest rate spread (Feb 2004 – Mar 2010) Source: BNB, UniCredit Bulbank Economic Research Retail loan-to-deposit interest rate spread Corporate loan-to-deposit interest rate spread

- 10. Position of UniCredit Bulbank

- 15. AWARDS OF UNICREDIT BULBANK 2009 Best Bank in BG Bank of the year in BG Best Bank in BG Best Custodian in BG CSR Award CSR Award