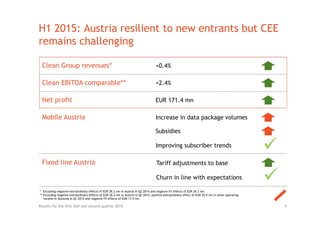

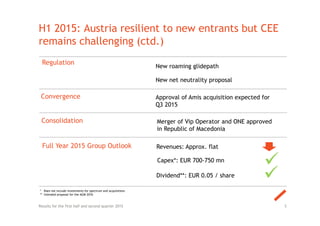

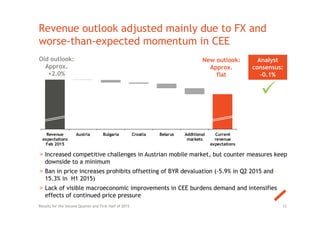

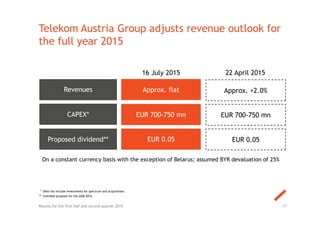

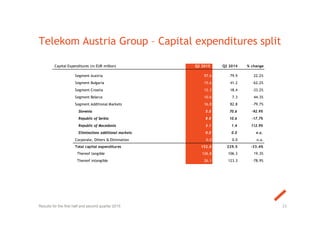

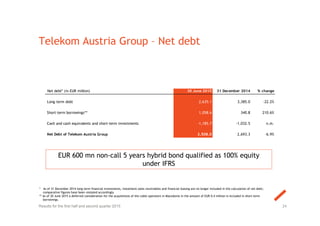

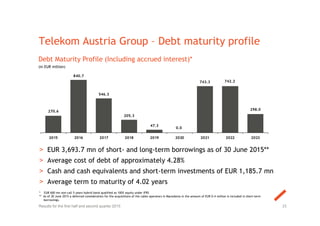

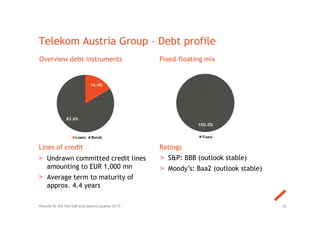

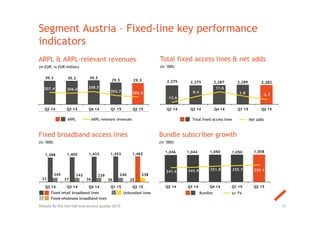

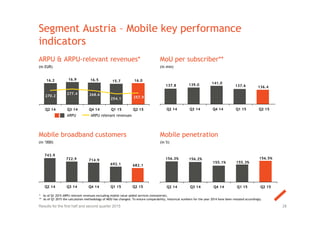

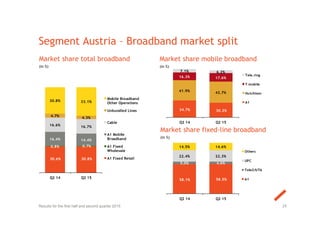

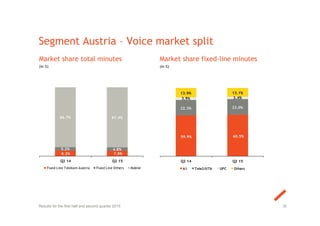

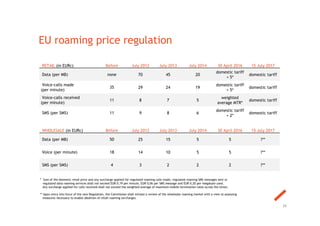

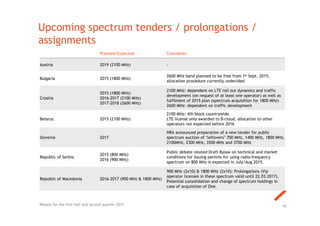

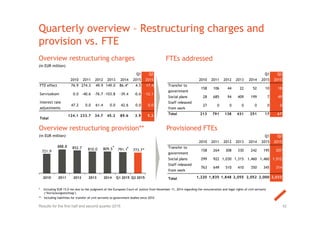

Telekom Austria Group reported results for the first half and second quarter of 2015. Revenue growth was 0.4% for the first half and 2.1% for the second quarter, driven by a positive performance in Austria that offset challenges in Central and Eastern Europe. EBITDA comparable grew 2.4% for the first half and 9.1% for the second quarter. The company adjusted its full year revenue outlook to approximately flat revenues, citing increased competitive pressures and foreign exchange impacts. Key strategic initiatives included the planned acquisition of Amis in Slovenia and the merger of operators in Macedonia.