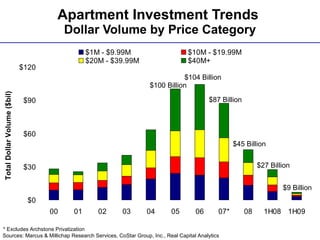

The document summarizes trends in the US apartment market in 2009. It finds that the market diverged into two camps based on long-term investment value versus short-term transactional value. Fundamentals remained solid, but debt markets were challenging and investors were cautious. It predicts that multi-family capital markets will remain difficult in 2009 with low transaction volumes and rising cap rates, especially for lower quality properties.

![10 5 09 Forecast Results Update[1]](https://cdn.slidesharecdn.com/ss_thumbnails/10509forecastresultsupdate1-12794898440143-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)