Downloaded 19 times

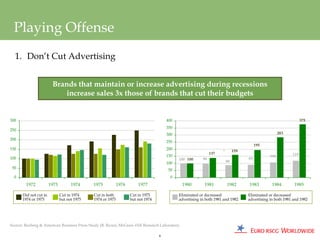

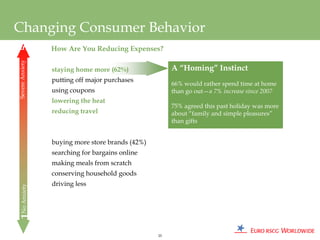

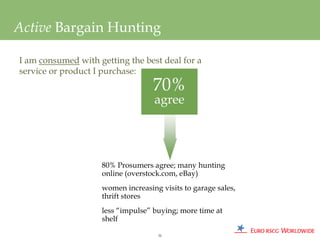

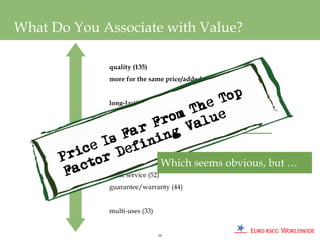

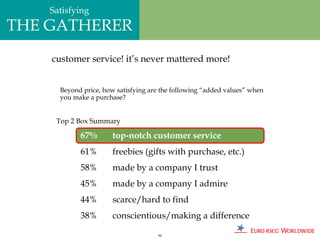

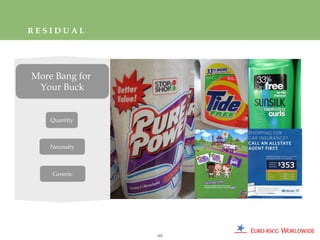

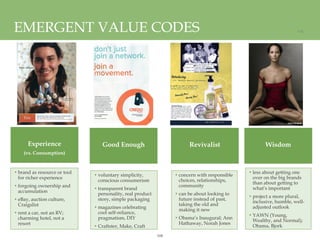

![Playing Offense

1. Don’t Cut Advertising

2. Don’t Cut Prices

3. Innovate, Innovate, Innovate

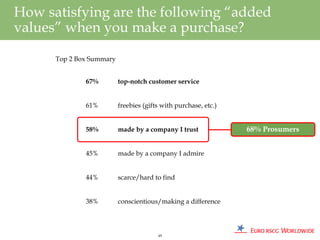

“Categories that grow the most [during recessions] are those that

show the highest level of product introduction”*

1930s 1970s

Source: * Ehrenberg-Bass Institute (B. Sharp)

10](https://image.slidesharecdn.com/thefutureofvalue-110726172128-phpapp01/85/The-Future-of-Value-Presentation-10-320.jpg)

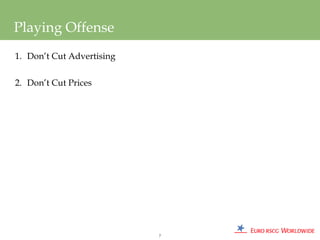

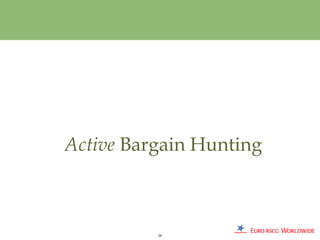

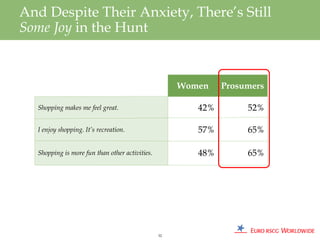

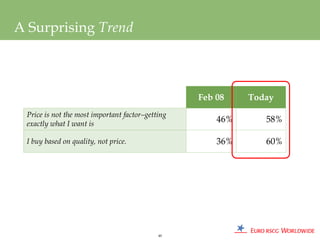

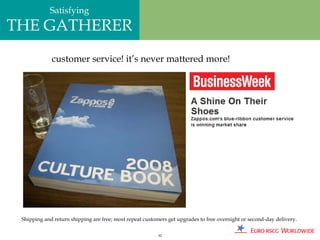

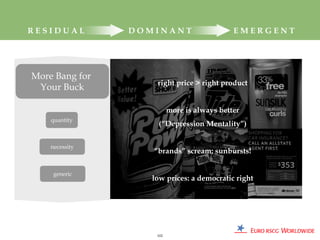

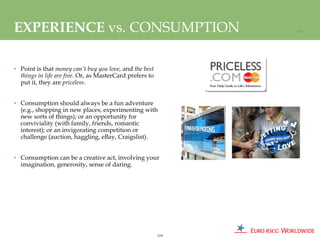

![Playing Offense

1. Don’t Cut Advertising

2. Don’t Cut Prices

3. Innovate, Innovate, Innovate

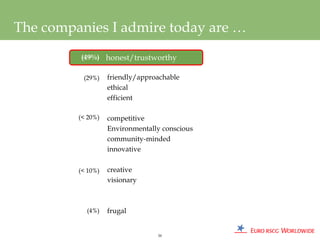

“Categories that grow the most [during recessions] are those that

show the highest level of product introduction”*

1930s 1970s

During the 1970s, 50% of supermarket

categories grew more than 15%.

Source: * Ehrenberg-Bass Institute (B. Sharp)

11](https://image.slidesharecdn.com/thefutureofvalue-110726172128-phpapp01/85/The-Future-of-Value-Presentation-11-320.jpg)

The document provides marketing advice for companies during an economic recession, suggesting that brands should maintain or increase advertising, avoid cutting prices, and focus on innovation. It also examines changing consumer behavior, finding that many consumers are anxious about the future and actively hunting for bargains and value. The research indicates that consumers now associate value more with quality, trustworthiness, and customer service rather than just low price.