This document is a certificate from Sintech Precision Product Limited certifying that the summer training project titled "WORKING CAPITAL MANAGEMENT and ITS APPRAISAL" completed by Bulbul Sharma from 1st June, 2009 to 31st July, 2009 is an original work. It includes an acknowledgement thanking various people who helped with the project. The table of contents provides an outline of the project including sections on industry profile, company overview, conceptual framework, working capital analysis and findings. The abstract introduces the project as a study of working capital management at Mondelez India Foods Pvt Ltd evaluating inventory, working capital ratios, trends and short term financing.

![C-189 & 190, Site No. 1, B.S. Road, Ind. Area, Ghaziabad [U.P.]

Phone No.: 0120-2866320/21,3290635/37/38Fax No. 0120-2867715

E-mail: marketing@sintechpumps.com Web Site: www.sintechpumps.com

CERTIFICATE

This is to certify that the Summer-Training Project of FINANCE Titled

“WORKING CAPITAL MANAGEMENT and ITS APPRAISAL” is an original

work and that this work has not been submitted anywhere in any form. My

indebtedness to other works/publications has been duly acknowledged at the

relevant places. The project workwas carriedfrom 1st June, 2009 to 31st July 2009

in SINTECH PRECISION PRODUCT LIMITED.

Date: 31st July 2009

Signature

(Bulbul Sharma)

PGDM ( 2009-10)

Signature

(Mr. Sanjeev Garg)

Sintech Precision Product Limited](https://image.slidesharecdn.com/summer-training-finance-project-on-working-capital-management2-180204140437/85/Summer-training-finance-project-on-working-capital-management-2-1-320.jpg)

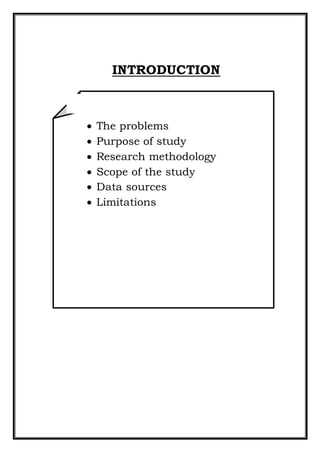

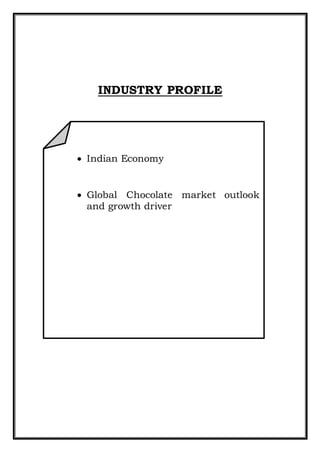

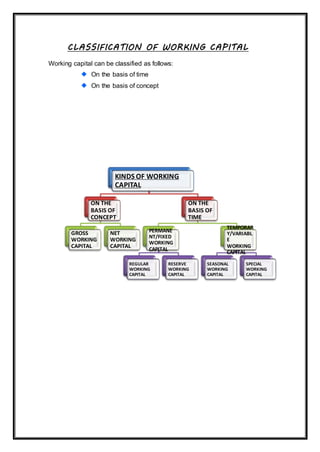

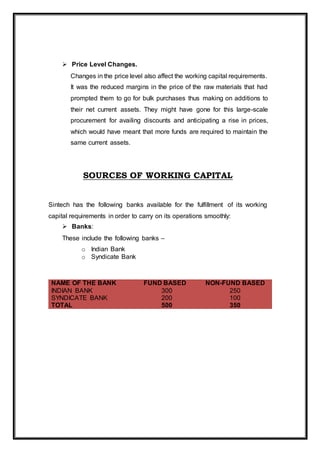

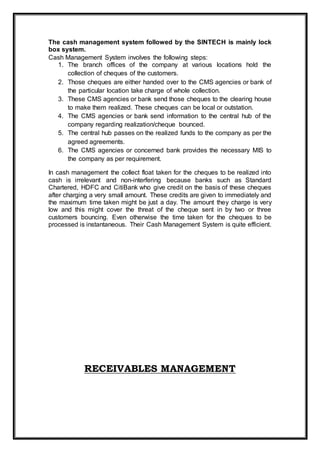

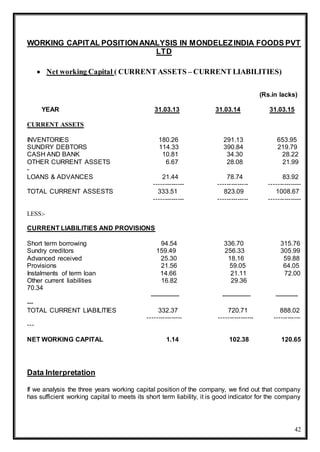

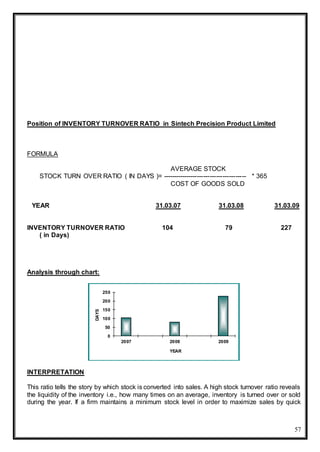

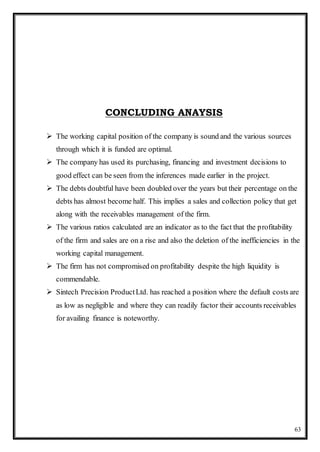

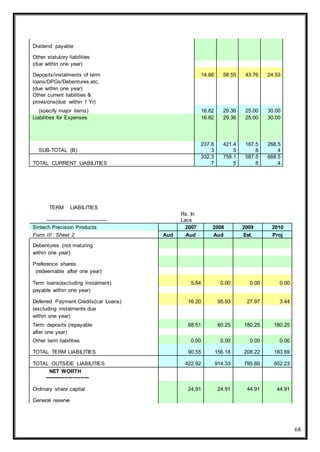

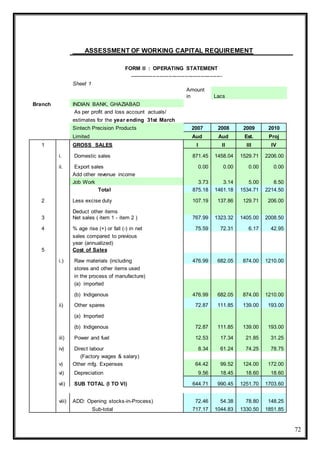

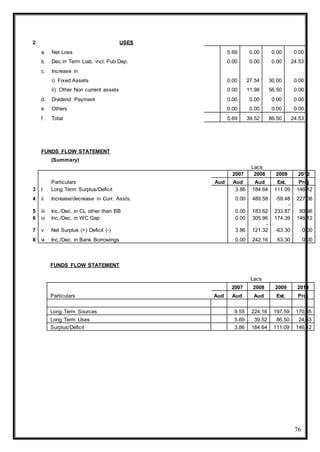

![73

Form II : Sheet 2 2007 2008 2009 2010

Sintech Precision Products Aud Aud Est. Proj

ix) Deduct : Closing stocks-in-

Process 54.38 78.80 148.25 205.75

x) Cost of Production 662.79 966.03 1182.25 1646.10

xi) Add : Opening stock of

finished goods 3.19 37.04 26.93 71.35

SUB-TOTAL 665.98 1003.07 1209.18 1717.45

xii) Deduct closing stock of

finished goods 37.04 26.93 71.35 100.88

xiii) SUB-TOTAL (Total cost of Sales) 628.94 976.14 1137.83 1616.57

6 Selling general and administrative

Expenses 82.59 143.09 158.00 190.00

7 SUB-TOTAL (5+6) 711.53 1119.23 1295.83 1806.57

8 Operating profit before interest 56.46 204.09 109.17 201.93

( 3-7 )

9 Interest 12.31 60.23 76.17 81.20

10 Operating profit after interest (8-9) 44.15 143.86 33.00 120.73

11 (i) Add other non-operating income

(a) Bank Interest on FDRs 0.15 1.43 2.00 2.00

(b)

(c)

(d)

Sub-total ( income ) 0.15 1.43 2.00 2.00

(ii) Deduct other non-operating expenses

(a) P&P expense inncluding 0.09 0.00 0.00 0.00

all book entries written off

(b)

Sub-total ( expenses ) 0.09 0.00 0.00 0.00

(iii) Net of other non-operating 0.06 1.43 2.00 2.00

income/expenses

12 Profit before tax/loss[10+11(iii)] 44.21 145.29 35.00 122.73

13 Provision for taxes 17.13 12.62 8.05 30.68

14 Prior Years Adjustment(if any)# 0.00 0.00 0.00 0.00

15 Net profit/loss for the year ( 12-13 ) 27.08 132.67 26.95 92.05

16 (a) Equity dividend paid-amt

(Already paid+ B.S. provision)

(b) Dividend Rate

17 Retained profit ( 14-15 ) 27.08 132.67 26.95 92.05

18 Retained profit/Net profit (% age) 100.00 100.00 100.00 100.00

# (-)ve for expense/provisions and (+) ve for gains](https://image.slidesharecdn.com/summer-training-finance-project-on-working-capital-management2-180204140437/85/Summer-training-finance-project-on-working-capital-management-2-73-320.jpg)

![Manoj_RM[1].docxbddddddddddddddddddddddddddddd](https://cdn.slidesharecdn.com/ss_thumbnails/manojrm1-240714132239-8f901766-thumbnail.jpg?width=640&height=640&fit=bounds)