Recommended

More Related Content

Similar to sueldos Yuli.pdf

Similar to sueldos Yuli.pdf (20)

Recently uploaded

Recently uploaded (20)

sueldos Yuli.pdf

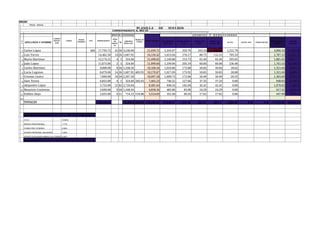

- 1. RROR! Potosi - Bolivia PLANILLA DE SUELDOS CORRESP0NDIENTE AL MES DE: ______________________________________________ CARNET IDENTI- DAD CARGO FECHA INGRESO NUA HABER BASICO BONO DE ANTIGÜEDAD TRABA- JO EXTRA TOTAL GANADO A P O R T E S Y D E D U C C I O N E S N o APELLIDOS Y NOMBRE AÑOS DE SERVIC IO % IMPORTE BONO ANT. CTA. PERSONAL PREV. 10% RIESGO COMUN 1,71% COMIS. AFP 0,50% APORTE NAL. SOLIDA- RIO RC-IVA ANTICI- POS OTROS DSCTOS TOTAL DESCU- ENTOS. LIQUIDO PAGABLE 1 Carlos López 466 17,793.72 41 50 3,246.00 21,039.72 2,103.97 359.78 105.20 185.60 1,251.79 4,006.34 17,033.38 2 Luis Torres 14,462.50 14 26 1,687.92 16,150.42 1,615.04 276.17 80.75 112.25 703.33 2,787.55 13,362.87 3 Maria Martínez 12,174.22 4 5 324.60 12,498.82 1,249.88 213.73 62.49 62.49 293.05 1,881.65 10,617.17 4 Julio López 11,675.00 2 5 324.60 11,999.60 1,199.96 205.19 60.00 60.00 236.40 1,761.55 10,238.05 5 Carlos Martínez 9,000.00 8 18 1,168.56 10,168.56 1,016.86 173.88 50.84 50.84 28.62 1,321.04 8,847.52 6 Lucia Lugones 8,079.00 14 26 1,687.92 403.95 10,170.87 1,017.09 173.92 50.85 50.85 28.88 1,321.60 8,849.27 7 Cristian Castro 7,890.00 18 34 2,207.28 10,097.28 1,009.73 172.66 50.49 50.49 20.53 1,303.89 8,793.39 8 Alex Torres 6,855.00 4 5 324.60 285.63 7,465.23 746.52 127.66 37.33 37.33 0.00 948.83 6,516.40 9 Alejandro López 5,755.00 22 42 2,726.64 8,481.64 848.16 145.04 42.41 42.41 0.00 1,078.02 7,403.62 10 Mauricio Contreras 3,690.00 9 18 1,168.56 4,858.56 485.86 83.08 24.29 24.29 0.00 617.52 4,241.04 11 Pablito Alejo 2,655.00 6 11 714.12 154.88 3,524.00 352.40 60.26 17.62 17.62 0.00 447.90 3,076.10 12 TOTALES 100,029.44 15,580.80844.46 116,454.70 11,645.47 1,991.38 582.27 694.17 2,562.60 0.00 0.00 17,475.89 98,978.81 APORTES PATRONALES % IMPORTES C N S 10.00% RIESGO PROFESIONAL 1.71% FONDO PRO VIVIENDA 2.00% APORTE PATRONAL SOLIDARIO 3.00% APORTE SOLIDARIO MINERO (SI CORRES 2.00% TOTAL APORTES

- 2. EMPRESA: EFCONTRI CONSULTORES NIT: 8786228012 DIRECCION: Calle Esteban Arce Nro. 432 PLANILLA TRIBUTARIA v 3 Correspondiente al Mes de FEBRERO de 2022 Periodo : September 2020 (Expresado en Bolivianos) Ufv Final: 28/02/2022 2.37712 Ufv Inicial: 31/01/2022 2.37562 SMN: DS 3890 2,164.00 NO VIGENTE No AÑO PERIODO CODIGO DEPENDIENTE RC-IVA NOMBRES PRIMER APELLIDO SEGUNDO APELLIDO NRO DOCUMENTO IDENTIDAD TIPO DE DOCUMENTO NOVEDADES (I= Incorporación V=Vigente D=Desvinculado) MONTO DE INGRESO NETO DOS (2) SMN NO IMPONIBLES IMPORTE SUJETO A IMPUESTO (BASE IMPONIBLE) IMPUESTO RC-IVA 13% de DOS (2) SMN IMPUESTO NETO RC-IVA F-110 CASILLA 693 SALDO A FAVOR DEL FISCO SALDO A FAVOR DEL DEPENDIENT E SALDO A FAVOR DEL DEPENDIENTE PERIODO ANTERIOR MNTTO DE VALOR SALDO PERIODO ANTERIOR SALDO DEL PERIODO ANTERIOR ACTUALIZADO SALDO UTILIZADO SALDO RC-IVA SUJETO A RETENCION PAGO A CUENTA SIETE -RG PERIODO ANTERIOR F-110 CASILLA 465 TOTAL SALDO PAGO A CUENTA SIETE-RG DEL PERIODO PAGO A CUENTA SIETE-RG UTILIZADO IMPUESTO RC-IVA RETENIDO SALDO DE CF-IVA A FAVOR DEL DEPENDIENTE PARA EL MES SIGUIENTE SALDO DE PAGO A CUENTA SIETE-RG A FAVOR DEL DEPENDIENTE PARA EL MES SIGUIENTE a b c d e f g h i j k l=j-k (si j>k) m=l*13% n o=m-n (si m>n) p q=o-p (si o>p) r=p-o (si p>o) s t u=s+t v=u (si u<=q) v=q (si q<u) w=q-v (si q>v) x y z=x+y aa=z(siW>=z); aa=w(siW˂z) ab=w-aa ac=r+u-v ad=z-aa 1 2022 2 ROBERTO CARLOS CI V 18,285.17 4,328.00 13,957.17 1,814.43 562.64 1,251.79 0.00 1,251.79 0.00 0.00 0.00 0.00 0.00 1,251.79 0.00 0.00 0.00 0.00 1,251.79 0.00 0.00 2 2022 2 JENNIFER LOPEZ CI V 14,066.20 4,328.00 9,738.20 1,265.97 562.64 703.33 0.00 703.33 0.00 0.00 0.00 0.00 0.00 703.33 0.00 0.00 0.00 0.00 703.33 0.00 0.00 3 2022 2 RICHARD COSSIANTE CI V 10,910.22 4,328.00 6,582.22 855.69 562.64 293.05 0.00 293.05 0.00 0.00 0.00 0.00 0.00 293.05 0.00 0.00 0.00 0.00 293.05 0.00 0.00 4 2022 2 ALBERTO PLAZA CI V 10,474.45 4,328.00 6,146.45 799.04 562.64 236.40 0.00 236.40 0.00 0.00 0.00 0.00 0.00 236.40 0.00 0.00 0.00 0.00 236.40 0.00 0.00 5 2022 2 PAULINA RUBIO CI V 8,876.14 4,328.00 4,548.14 591.26 562.64 28.62 0.00 28.62 0.00 0.00 0.00 0.00 0.00 28.62 0.00 0.00 0.00 0.00 28.62 0.00 0.00 6 2022 2 RICARDO MONTANER CI V 8,878.15 4,328.00 4,550.15 591.52 562.64 28.88 0.00 28.88 0.00 0.00 0.00 0.00 0.00 28.88 0.00 0.00 0.00 0.00 28.88 0.00 0.00 7 2022 2 MIGUEL BOSSE CI V 8,813.92 4,328.00 4,485.92 583.17 562.64 20.53 0.00 20.53 0.00 0.00 0.00 0.00 0.00 20.53 0.00 0.00 0.00 0.00 20.53 0.00 0.00 8 2022 2 MILTON CORTEZ CI V 6,516.40 4,328.00 2,188.40 284.49 562.64 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 9 2022 2 ALEJANDRO FERNANDEZ CI V 7,403.62 4,328.00 3,075.62 399.83 562.64 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 10 2022 2 PATRICIA VENEGAS CI V 4,241.04 4,328.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 11 2022 2 CRISTIAN CASTRO CI V 3,076.10 4,328.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 T O T A L E S 101,541.41 47,608.00 55,272.27 7,185.40 5,063.76 2,562.60 0.00 2,562.60 0.00 0.00 0.00 0.00 0.00 2,562.60 0.00 0.00 0.00 0.00 2,562.60 0.00 0.00 TOTALES REDONDEADOS 101,541 47,608 55,272 7,185 5,064 2,563 - 2,563 - - - - - 2,563 - - - - 2,563 - - CASILLAS FORMULARIO 608 v.4 C 13 C 26 C 27 C 2000 C 215 C 1215 C 202 C 2001 C 634 C 635 C 648 C 649 C 650 C 450 C 466 C465 C471 C472 C909 C592 C469

- 3. (A) CABECERA DE LA DECLARACION JURADA a Numero de Orden b NIT 8786228012 c Mes 9 d Año 2020 i Fecha DDJJ ORIGINAL DDJJ Original 534 (B) DATOS BASICOS DE LA DECLARACION JURADA QUE RECTIFICA a Nro. de Resolución Administrativa 518 b Formulario 537 c Nro. de Orden a Rectificar 521 (C) DETERMINACIÓN DEL SALDO A FAVOR DEL FISCO O DEL CONTRIBUYENTE a Monto de ingreso neto 13 101,541 b Dos (2) salarios mínimos nacionales no imponibles 26 47,608 c Importe sujeto a impuesto (Base Imponible) según planilla salarial 27 55,272 d Impuesto RC - IVA según planilla salarial 2000 7,185 e 13% de dos (2) Salarios Mínimos Nacionales 215 5,064 f Impuesto Neto RC-IVA según planilla salarial 1215 2,563 g Form 110 (C693) 13 % según planilla salarial 202 0

- 4. h Saldo a favor del Fisco según planilla salarial 2001 2,563 i Saldo a favor del Dependiente según planilla salarial 634 0 j Saldo a favor de los dependientes periodo anterior 635 0 k Mantenimiento de Valor del saldo a favor del dependiente del periodo anterior 648 0 l Saldo del periodo anterior actualizado (C635 + C648); Si > 0) 649 0 m Saldo Utilizado según planilla salarial 650 0 n Saldo RC-IVA sujeto a retención (C2001-C650); Si>0 450 2,563 o Pago a cuenta SIETE-RG periodo anterior según planilla salarial 466 0 p Formulario 110 (C465) según planilla salarial 465 0 q Total saldo pago a cuenta SIETE-RG del periodo (C466+C465); Si>0 471 0 r Pago a cuenta SIETE-RG utilizado según planilla salarial 472 0 s Impuesto RC-IVA retenido según planilla salarial 909 2,563 t Saldo de Crédito Fiscal a favor del dependiente para el mes siguiente según planilla salarial 592 0 u Saldo de pago a cuenta SIETE-RG a favor del dependiente para el mes siguiente (C471-C472); Si >0 469 0 v Retención RC-IVA de pagos en el periodo a Desvinculados y otros 748 0 (D) SALDOS DESPUÉS DE LA COMPENSACIÓN DE PAGOS A CUENTA a Pagos a cuenta realizados en F-608 Original y/o rectificatoria y/o en Boletas de Pago; por el periodo fiscal que se liquida en PlanillaTributaria. 622 0 b Pagos a cuenta realizados en F-608 Original y/o rectificatoria y/o en Boletas de Pago; por el periodo fiscal que se liquida a Desvinculados y otros. 623 0 c Saldo de pagos disponible del periodo anterior a compensar (C747 del F-608 del periodo anterior) 640 0 d Saldo de pagos disponible después de la compensación ((C622 + C640-C909);Si > 0)+((C623-C748);Si>0) 643 0 e Saldo de impuesto a favor del Fisco ((C909-C622-C640);Si>0)+((C748-C623);Si>0) 996 2,563 (E) LIQUIDACIÓN DEL ADEUDO TRIBUTARIO, MULTAS Y SANCIONES a Actualización de Valor sobre el monto declarado en la casilla (C996) 925 0 b Intereses sobre el Tributo Omitido Actualizado 938 0 c Multa por Incumplimiento a Deberes Formales por presentación Fuera de Plazo 954 0 e Saldo Definitivo a Favor del Fisco (C996+C925+C938+C954); Si>0 955 2,563 (F)COMPENSACIÓN O PAGO DE LA DEUDA TRIBUTARIA (EN EFECTIVO Y/O VALORES Y/O SIGEP)

- 5. a Saldo definitivo a favor del fisco (C955) 746 2,563 b Saldo de pagos disponible para el periodo siguiente (C643)(Se traslada al siguiente periodo a la casilla C640 del F-608) 747 0 c Imputación de crédito en valores (Sujeto a verificación y confirmación por parte del S.I.N.) 677 0 d Pago en efectivo (C746 - C677); Si > 0 576 2,563 e Total número de dependientes 127 11 f Total de Formularios 110 recibidos en el periodo que se liquida 130 0 DATOS INFORMATIVOS DE PAGO MEDIANTE SIGEP (SOLO SECTOR PÚBLICO) a Nro. C-31 8880 b N° de pago 8882 c Fecha de confirmación de pago 8881 d Importe pagado vía SIGEP 882 Material proporcionado por EFCONTRI CONSULTORES Solo para fines académicos Cel.: 67442768

- 7. NILLA DE APORTES PATRONALES AL SSO, PRO VIVIENDA Y PROVISION PARA BENEFICIOS SOCIA SEGURO S. O. PRO ROV. BENEF. SOCIALE Nro. NOMBRES TOTAL CNS R. PROF. AP.PAT. SOL VIVIENDA INDEM. GUINALDOS TOTAL GANADO 10% 1.71% 3% 2% 8.33% 8.33% 1 ROBERTO CARLOS 21,039.72 2,103.97 359.78 631.19 420.79 1,752.61 1,752.61 7,020.95 2 JENNIFER LOPEZ 16,150.42 1,615.04 276.17 484.51 323.01 1,345.33 1,345.33 5,389.40 3 RICHARD COSSIANTE 12,498.82 1,249.88 213.73 374.96 249.98 1,041.15 1,041.15 4,170.86 4 ALBERTO PLAZA 11,999.60 1,199.96 205.19 359.99 239.99 999.57 999.57 4,004.27 5 PAULINA RUBIO 10,168.56 1,016.86 173.88 305.06 203.37 847.04 847.04 3,393.25 6 RICARDO MONTANER 10,170.87 1,017.09 173.92 305.13 203.42 847.23 847.23 3,394.02 7 MIGUEL BOSSE 10,097.28 1,009.73 172.66 302.92 201.95 841.10 841.10 3,369.46 8 MILTON CORTEZ 7,465.23 746.52 127.66 223.96 149.30 621.85 621.85 2,491.15 9 ALEJANDRO FERNANDEZ 8,481.64 848.16 145.04 254.45 169.63 706.52 706.52 2,830.32 10 PATRICIA VENEGAS 4,858.56 485.86 83.08 145.76 97.17 404.72 404.72 1,621.30 11 CRISTIAN CASTRO 3,524.00 352.40 60.26 105.72 70.48 293.55 293.55 1,175.96 TOTALES 116,454.70 11,645.47 1,991.38 3,493.64 2,329.09 9,700.68 9,700.68 38,860.93

- 8. 1/1/2017 2.17281 1/2/2017 2.17303 1/3/2017 2.17325 1/4/2017 2.17347 1/5/2017 2.17369 1/6/2017 2.17391 1/7/2017 2.17413 1/8/2017 2.17435 1/9/2017 2.17457 1/10/2017 2.17479 1/11/2017 2.17502 1/12/2017 2.17525 1/13/2017 2.17548 1/14/2017 2.17571 1/15/2017 2.17594 1/16/2017 2.17617 1/17/2017 2.1764 1/18/2017 2.17663 1/19/2017 2.17686 1/20/2017 2.17709 1/21/2017 2.17732 1/22/2017 2.17755 1/23/2017 2.17778 1/24/2017 2.17801 1/25/2017 2.17824 1/26/2017 2.17847 1/27/2017 2.1787 1/28/2017 2.17893 1/29/2017 2.17916 1/30/2017 2.17939 1/31/2017 2.17962 2/1/2017 2.17987 2/2/2017 2.18012 2/3/2017 2.18037 2/4/2017 2.18062 2/5/2017 2.18087 2/6/2017 2.18112 2/7/2017 2.18137

- 9. 2/8/2017 2.18162 2/9/2017 2.18187 2/10/2017 2.18212 2/11/2017 2.18235 2/12/2017 2.18258 2/13/2017 2.18281 2/14/2017 2.18304 2/15/2017 2.18327 2/16/2017 2.1835 2/17/2017 2.18373 2/18/2017 2.18396 2/19/2017 2.18419 2/20/2017 2.18442 2/21/2017 2.18465 2/22/2017 2.18488 2/23/2017 2.18511 2/24/2017 2.18534 2/25/2017 2.18557 2/26/2017 2.1858 2/27/2017 2.18603 2/28/2017 2.18626 3/1/2017 2.18647 3/2/2017 2.18668 3/3/2017 2.18689 3/4/2017 2.1871 3/5/2017 2.18731 3/6/2017 2.18752 3/7/2017 2.18773 3/8/2017 2.18794 3/9/2017 2.18815 3/10/2017 2.18836 3/11/2017 2.18856 3/12/2017 2.18876 3/13/2017 2.18896 3/14/2017 2.18916 3/15/2017 2.18936 3/16/2017 2.18956 3/17/2017 2.18976

- 10. 3/18/2017 2.18996 3/19/2017 2.19016 3/20/2017 2.19036 3/21/2017 2.19056 3/22/2017 2.19076 3/23/2017 2.19096 3/24/2017 2.19116 3/25/2017 2.19136 3/26/2017 2.19156 3/27/2017 2.19176 3/28/2017 2.19196 3/29/2017 2.19216 3/30/2017 2.19236 3/31/2017 2.19256 4/1/2017 2.19277 4/2/2017 2.19298 4/3/2017 2.19319 4/4/2017 2.1934 4/5/2017 2.19361 4/6/2017 2.19382 4/7/2017 2.19403 4/8/2017 2.19424 4/9/2017 2.19445 4/10/2017 2.19466 4/11/2017 2.19486 4/12/2017 2.19506 4/13/2017 2.19526 4/14/2017 2.19546 4/15/2017 2.19566 4/16/2017 2.19586 4/17/2017 2.19606 4/18/2017 2.19626 4/19/2017 2.19646 4/20/2017 2.19666 4/21/2017 2.19686 4/22/2017 2.19706 4/23/2017 2.19726 4/24/2017 2.19746

- 11. 4/25/2017 2.19766 4/26/2017 2.19786 4/27/2017 2.19806 4/28/2017 2.19826 4/29/2017 2.19846 4/30/2017 2.19866 5/1/2017 2.19885 5/2/2017 2.19904 5/3/2017 2.19923 5/4/2017 2.19942 5/5/2017 2.19961 5/6/2017 2.1998 5/7/2017 2.19999 5/8/2017 2.20018 5/9/2017 2.20037 5/10/2017 2.20056 5/11/2017 2.20071 5/12/2017 2.20086 5/13/2017 2.20101 5/14/2017 2.20116 5/15/2017 2.20131 5/16/2017 2.20146 5/17/2017 2.20161 5/18/2017 2.20176 5/19/2017 2.20191 5/20/2017 2.20206 5/21/2017 2.20221 5/22/2017 2.20236 5/23/2017 2.20251 5/24/2017 2.20266 5/25/2017 2.20281 5/26/2017 2.20296 5/27/2017 2.20311 5/28/2017 2.20326 5/29/2017 2.20341 5/30/2017 2.20356 5/31/2017 2.20371 6/1/2017 2.20386

- 12. 6/2/2017 2.20401 6/3/2017 2.20416 6/4/2017 2.20431 6/5/2017 2.20446 6/6/2017 2.20461 6/7/2017 2.20476 6/8/2017 2.20491 6/9/2017 2.20506 6/10/2017 2.20521 6/11/2017 2.20529 6/12/2017 2.20537 6/13/2017 2.20545 6/14/2017 2.20553 6/15/2017 2.20561 6/16/2017 2.20569 6/17/2017 2.20577 6/18/2017 2.20585 6/19/2017 2.20593 6/20/2017 2.20601 6/21/2017 2.20609 6/22/2017 2.20617 6/23/2017 2.20625 6/24/2017 2.20633 6/25/2017 2.20641 6/26/2017 2.20649 6/27/2017 2.20657 6/28/2017 2.20665 6/29/2017 2.20673 6/30/2017 2.20681 7/1/2017 2.20688 7/2/2017 2.20695 7/3/2017 2.20702 7/4/2017 2.20709 7/5/2017 2.20716 7/6/2017 2.20723 7/7/2017 2.2073 7/8/2017 2.20737 7/9/2017 2.20744

- 13. 7/10/2017 2.20751 7/11/2017 2.20762 7/12/2017 2.20773 7/13/2017 2.20784 7/14/2017 2.20795 7/15/2017 2.20806 7/16/2017 2.20817 7/17/2017 2.20828 7/18/2017 2.20839 7/19/2017 2.2085 7/20/2017 2.20861 7/21/2017 2.20872 7/22/2017 2.20883 7/23/2017 2.20894 7/24/2017 2.20905 7/25/2017 2.20916 7/26/2017 2.20927 7/27/2017 2.20938 7/28/2017 2.20949 7/29/2017 2.2096 7/30/2017 2.20971 7/31/2017 2.20982 8/1/2017 2.20993 8/2/2017 2.21004 8/3/2017 2.21015 8/4/2017 2.21026 8/5/2017 2.21037 8/6/2017 2.21048 8/7/2017 2.21059 8/8/2017 2.2107 8/9/2017 2.21081 8/10/2017 2.21092 8/11/2017 2.21107 8/12/2017 2.21122 8/13/2017 2.21137 8/14/2017 2.21152 8/15/2017 2.21167 8/16/2017 2.21182

- 14. 8/17/2017 2.21197 8/18/2017 2.21212 8/19/2017 2.21227 8/20/2017 2.21242 8/21/2017 2.21257 8/22/2017 2.21272 8/23/2017 2.21287 8/24/2017 2.21302 8/25/2017 2.21317 8/26/2017 2.21332 8/27/2017 2.21347 8/28/2017 2.21362 8/29/2017 2.21377 8/30/2017 2.21392 8/31/2017 2.21407 9/1/2017 2.21423 9/2/2017 2.21439 9/3/2017 2.21455 9/4/2017 2.21471 9/5/2017 2.21487 9/6/2017 2.21503 9/7/2017 2.21519 9/8/2017 2.21535 9/9/2017 2.21551 9/10/2017 2.21567 9/11/2017 2.21587 9/12/2017 2.21607 9/13/2017 2.21627 9/14/2017 2.21647 9/15/2017 2.21667 9/16/2017 2.21687 9/17/2017 2.21707 9/18/2017 2.21727 9/19/2017 2.21747 9/20/2017 2.21767 9/21/2017 2.21787 9/22/2017 2.21807 9/23/2017 2.21827

- 15. 9/24/2017 2.21847 9/25/2017 2.21867 9/26/2017 2.21887 9/27/2017 2.21907 9/28/2017 2.21927 9/29/2017 2.21947 9/30/2017 2.21967 10/1/2017 2.21986 10/2/2017 2.22005 10/3/2017 2.22024 10/4/2017 2.22043 10/5/2017 2.22062 10/6/2017 2.22081 10/7/2017 2.221 10/8/2017 2.22119 10/9/2017 2.22138 10/10/2017 2.22157 10/11/2017 2.22178 10/12/2017 2.22199 10/13/2017 2.2222 10/14/2017 2.22241 10/15/2017 2.22262 10/16/2017 2.22283 10/17/2017 2.22304 10/18/2017 2.22325 10/19/2017 2.22346 10/20/2017 2.22367 10/21/2017 2.22388 10/22/2017 2.22409 10/23/2017 2.2243 10/24/2017 2.22451 10/25/2017 2.22472 10/26/2017 2.22493 10/27/2017 2.22514 10/28/2017 2.22535 10/29/2017 2.22556 10/30/2017 2.22577 10/31/2017 2.22598

- 16. 11/1/2017 2.2262 11/2/2017 2.22642 11/3/2017 2.22664 11/4/2017 2.22686 11/5/2017 2.22708 11/6/2017 2.2273 11/7/2017 2.22752 11/8/2017 2.22774 11/9/2017 2.22796 11/10/2017 2.22818 11/11/2017 2.22836 11/12/2017 2.22854 11/13/2017 2.22872 11/14/2017 2.2289 11/15/2017 2.22908 11/16/2017 2.22926 11/17/2017 2.22944 11/18/2017 2.22962 11/19/2017 2.2298 11/20/2017 2.22998 11/21/2017 2.23016 11/22/2017 2.23034 11/23/2017 2.23052 11/24/2017 2.2307 11/25/2017 2.23088 11/26/2017 2.23106 11/27/2017 2.23124 11/28/2017 2.23142 11/29/2017 2.2316 11/30/2017 2.23178 12/1/2017 2.23196 12/2/2017 2.23214 12/3/2017 2.23232 12/4/2017 2.2325 12/5/2017 2.23268 12/6/2017 2.23286 12/7/2017 2.23304 12/8/2017 2.23322

- 17. 12/9/2017 2.2334 12/10/2017 2.23358 12/11/2017 2.23374 12/12/2017 2.2339 12/13/2017 2.23406 12/14/2017 2.23422 12/15/2017 2.23438 12/16/2017 2.23454 12/17/2017 2.2347 12/18/2017 2.23486 12/19/2017 2.23502 12/20/2017 2.23518 12/21/2017 2.23534 12/22/2017 2.2355 12/23/2017 2.23566 12/24/2017 2.23582 12/25/2017 2.23598 12/26/2017 2.23614 12/27/2017 2.2363 12/28/2017 2.23646 12/29/2017 2.23662 12/30/2017 2.23678 12/31/2017 2.23694 1/1/2018 2.2371 1/2/2018 2.23726 1/3/2018 2.23742 1/4/2018 2.23758 1/5/2018 2.23774 1/6/2018 2.2379 1/7/2018 2.23806 1/8/2018 2.23822 1/9/2018 2.23838 1/10/2018 2.23854 1/11/2018 2.2387 1/12/2018 2.23886 1/13/2018 2.23902 1/14/2018 2.23918 1/15/2018 2.23934

- 18. 1/16/2018 2.2395 1/17/2018 2.23966 1/18/2018 2.23982 1/19/2018 2.23998 1/20/2018 2.24014 1/21/2018 2.2403 1/22/2018 2.24046 1/23/2018 2.24062 1/24/2018 2.24078 1/25/2018 2.24094 1/26/2018 2.2411 1/27/2018 2.24126 1/28/2018 2.24142 1/29/2018 2.24158 1/30/2018 2.24174 1/31/2018 2.2419 2/1/2018 2.24208 2/2/2018 2.24226 2/3/2018 2.24244 2/4/2018 2.24262 2/5/2018 2.2428 2/6/2018 2.24298 2/7/2018 2.24316 2/8/2018 2.24334 2/9/2018 2.24352 2/10/2018 2.2437 2/11/2018 2.24389 2/12/2018 2.24408 2/13/2018 2.24427 2/14/2018 2.24446 2/15/2018 2.24465 2/16/2018 2.24484 2/17/2018 2.24503 2/18/2018 2.24522 2/19/2018 2.24541 2/20/2018 2.2456 2/21/2018 2.24579 2/22/2018 2.24598

- 19. 2/23/2018 2.24617 2/24/2018 2.24636 2/25/2018 2.24655 2/26/2018 2.24674 2/27/2018 2.24693 2/28/2018 2.24712 3/1/2018 2.24729 3/2/2018 2.24746 3/3/2018 2.24763 3/4/2018 2.2478 3/5/2018 2.24797 3/6/2018 2.24814 3/7/2018 2.24831 3/8/2018 2.24848 3/9/2018 2.24865 3/10/2018 2.24882 3/11/2018 2.24899 3/12/2018 2.24916 3/13/2018 2.24933 3/14/2018 2.2495 3/15/2018 2.24967 3/16/2018 2.24984 3/17/2018 2.25001 3/18/2018 2.25018 3/19/2018 2.25035 3/20/2018 2.25052 3/21/2018 2.25069 3/22/2018 2.25086 3/23/2018 2.25103 3/24/2018 2.2512 3/25/2018 2.25137 3/26/2018 2.25154 3/27/2018 2.25171 3/28/2018 2.25188 3/29/2018 2.25205 3/30/2018 2.25222 3/31/2018 2.25239 4/1/2018 2.25257

- 20. 4/2/2018 2.25275 4/3/2018 2.25293 4/4/2018 2.25311 4/5/2018 2.25329 4/6/2018 2.25347 4/7/2018 2.25365 4/8/2018 2.25383 4/9/2018 2.25401 4/10/2018 2.25419 4/11/2018 2.25436 4/12/2018 2.25453 4/13/2018 2.2547 4/14/2018 2.25487 4/15/2018 2.25504 4/16/2018 2.25521 4/17/2018 2.25538 4/18/2018 2.25555 4/19/2018 2.25572 4/20/2018 2.25589 4/21/2018 2.25606 4/22/2018 2.25623 4/23/2018 2.2564 4/24/2018 2.25657 4/25/2018 2.25674 4/26/2018 2.25691 4/27/2018 2.25708 4/28/2018 2.25725 4/29/2018 2.25742 4/30/2018 2.25759 5/1/2018 2.25775 5/2/2018 2.25791 5/3/2018 2.25807 5/4/2018 2.25823 5/5/2018 2.25839 5/6/2018 2.25855 5/7/2018 2.25871 5/8/2018 2.25887 5/9/2018 2.25903

- 21. 5/10/2018 2.25919 5/11/2018 2.25937 5/12/2018 2.25955 5/13/2018 2.25973 5/14/2018 2.25991 5/15/2018 2.26009 5/16/2018 2.26027 5/17/2018 2.26045 5/18/2018 2.26063 5/19/2018 2.26081 5/20/2018 2.26099 5/21/2018 2.26117 5/22/2018 2.26135 5/23/2018 2.26153 5/24/2018 2.26171 5/25/2018 2.26189 5/26/2018 2.26207 5/27/2018 2.26225 5/28/2018 2.26243 5/29/2018 2.26261 5/30/2018 2.26279 5/31/2018 2.26297 6/1/2018 2.26316 6/2/2018 2.26335 6/3/2018 2.26354 6/4/2018 2.26373 6/5/2018 2.26392 6/6/2018 2.26411 6/7/2018 2.2643 6/8/2018 2.26449 6/9/2018 2.26468 6/10/2018 2.26487 6/11/2018 2.26507 6/12/2018 2.26527 6/13/2018 2.26547 6/14/2018 2.26567 6/15/2018 2.26587 6/16/2018 2.26607

- 22. 6/17/2018 2.26627 6/18/2018 2.26647 6/19/2018 2.26667 6/20/2018 2.26687 6/21/2018 2.26707 6/22/2018 2.26727 6/23/2018 2.26747 6/24/2018 2.26767 6/25/2018 2.26787 6/26/2018 2.26807 6/27/2018 2.26827 6/28/2018 2.26847 6/29/2018 2.26867 6/30/2018 2.26887 7/1/2018 2.26906 7/2/2018 2.26925 7/3/2018 2.26944 7/4/2018 2.26963 7/5/2018 2.26982 7/6/2018 2.27001 7/7/2018 2.2702 7/8/2018 2.27039 7/9/2018 2.27058 7/10/2018 2.27077 7/11/2018 2.27096 7/12/2018 2.27115 7/13/2018 2.27134 7/14/2018 2.27153 7/15/2018 2.27172 7/16/2018 2.27191 7/17/2018 2.2721 7/18/2018 2.27229 7/19/2018 2.27248 7/20/2018 2.27267 7/21/2018 2.27286 7/22/2018 2.27305 7/23/2018 2.27324 7/24/2018 2.27343

- 23. 7/25/2018 2.27362 7/26/2018 2.27381 7/27/2018 2.274 7/28/2018 2.27419 7/29/2018 2.27438 7/30/2018 2.27457 7/31/2018 2.27476 8/1/2018 2.27495 8/2/2018 2.27514 8/3/2018 2.27533 8/4/2018 2.27552 8/5/2018 2.27571 8/6/2018 2.2759 8/7/2018 2.27609 8/8/2018 2.27628 8/9/2018 2.27647 8/10/2018 2.27666 8/11/2018 2.27681 8/12/2018 2.27696 8/13/2018 2.27711 8/14/2018 2.27726 8/15/2018 2.27741 8/16/2018 2.27756 8/17/2018 2.27771 8/18/2018 2.27786 8/19/2018 2.27801 8/20/2018 2.27816 8/21/2018 2.27831 8/22/2018 2.27846 8/23/2018 2.27861 8/24/2018 2.27876 8/25/2018 2.27891 8/26/2018 2.27906 8/27/2018 2.27921 8/28/2018 2.27936 8/29/2018 2.27951 8/30/2018 2.27966 8/31/2018 2.27981

- 24. 9/1/2018 2.27996 9/2/2018 2.28011 9/3/2018 2.28026 9/4/2018 2.28041 9/5/2018 2.28056 9/6/2018 2.28071 9/7/2018 2.28086 9/8/2018 2.28101 9/9/2018 2.28116 9/10/2018 2.28131 9/11/2018 2.28142 9/12/2018 2.28153 9/13/2018 2.28164 9/14/2018 2.28175 9/15/2018 2.28186 9/16/2018 2.28197 9/17/2018 2.28208 9/18/2018 2.28219 9/19/2018 2.2823 9/20/2018 2.28241 9/21/2018 2.28252 9/22/2018 2.28263 9/23/2018 2.28274 9/24/2018 2.28285 9/25/2018 2.28296 9/26/2018 2.28307 9/27/2018 2.28318 9/28/2018 2.28329 9/29/2018 2.2834 9/30/2018 2.28351 10/1/2018 2.28362 10/2/2018 2.28373 10/3/2018 2.28384 10/4/2018 2.28395 10/5/2018 2.28406 10/6/2018 2.28417 10/7/2018 2.28428 10/8/2018 2.28439

- 25. 10/9/2018 2.2845 10/10/2018 2.28461 10/11/2018 2.28467 10/12/2018 2.28473 10/13/2018 2.28479 10/14/2018 2.28485 10/15/2018 2.28491 10/16/2018 2.28497 10/17/2018 2.28503 10/18/2018 2.28509 10/19/2018 2.28515 10/20/2018 2.28521 10/21/2018 2.28527 10/22/2018 2.28533 10/23/2018 2.28539 10/24/2018 2.28545 10/25/2018 2.28551 10/26/2018 2.28557 10/27/2018 2.28563 10/28/2018 2.28569 10/29/2018 2.28575 10/30/2018 2.28581 10/31/2018 2.28587 11/1/2018 2.28593 11/2/2018 2.28599 11/3/2018 2.28605 11/4/2018 2.28611 11/5/2018 2.28617 11/6/2018 2.28623 11/7/2018 2.28629 11/8/2018 2.28635 11/9/2018 2.28641 11/10/2018 2.28647 11/11/2018 2.28655 11/12/2018 2.28663 11/13/2018 2.28671 11/14/2018 2.28679 11/15/2018 2.28687

- 26. 11/16/2018 2.28695 11/17/2018 2.28703 11/18/2018 2.28711 11/19/2018 2.28719 11/20/2018 2.28727 11/21/2018 2.28735 11/22/2018 2.28743 11/23/2018 2.28751 11/24/2018 2.28759 11/25/2018 2.28767 11/26/2018 2.28775 11/27/2018 2.28783 11/28/2018 2.28791 11/29/2018 2.28799 11/30/2018 2.28807 12/1/2018 2.28815 12/2/2018 2.28823 12/3/2018 2.28831 12/4/2018 2.28839 12/5/2018 2.28847 12/6/2018 2.28855 12/7/2018 2.28863 12/8/2018 2.28871 12/9/2018 2.28879 12/10/2018 2.28887 12/11/2018 2.28896 12/12/2018 2.28905 12/13/2018 2.28914 12/14/2018 2.28923 12/15/2018 2.28932 12/16/2018 2.28941 12/17/2018 2.2895 12/18/2018 2.28959 12/19/2018 2.28968 12/20/2018 2.28977 12/21/2018 2.28986 12/22/2018 2.28995 12/23/2018 2.29004

- 27. 12/24/2018 2.29013 12/25/2018 2.29022 12/26/2018 2.29031 12/27/2018 2.2904 12/28/2018 2.29049 12/29/2018 2.29058 12/30/2018 2.29067 12/31/2018 2.29076 1/1/2019 2.29085 1/2/2019 2.29094 1/3/2019 2.29103 1/4/2019 2.29112 1/5/2019 2.29121 1/6/2019 2.2913 1/7/2019 2.29139 1/8/2019 2.29148 1/9/2019 2.29157 1/10/2019 2.29166 1/11/2019 2.29175 1/12/2019 2.29184 1/13/2019 2.29193 1/14/2019 2.29202 1/15/2019 2.29211 1/16/2019 2.2922 1/17/2019 2.29229 1/18/2019 2.29238 1/19/2019 2.29247 1/20/2019 2.29256 1/21/2019 2.29265 1/22/2019 2.29274 1/23/2019 2.29283 1/24/2019 2.29292 1/25/2019 2.29301 1/26/2019 2.2931 1/27/2019 2.29319 1/28/2019 2.29328 1/29/2019 2.29337 1/30/2019 2.29346

- 28. 1/31/2019 2.29355 2/1/2019 2.29365 2/2/2019 2.29375 2/3/2019 2.29385 2/4/2019 2.29395 2/5/2019 2.29405 2/6/2019 2.29415 2/7/2019 2.29425 2/8/2019 2.29435 2/9/2019 2.29445 2/10/2019 2.29455 2/11/2019 2.29465 2/12/2019 2.29475 2/13/2019 2.29485 2/14/2019 2.29495 2/15/2019 2.29505 2/16/2019 2.29515 2/17/2019 2.29525 2/18/2019 2.29535 2/19/2019 2.29545 2/20/2019 2.29555 2/21/2019 2.29565 2/22/2019 2.29575 2/23/2019 2.29585 2/24/2019 2.29595 2/25/2019 2.29605 2/26/2019 2.29615 2/27/2019 2.29625 2/28/2019 2.29635 3/1/2019 2.29644 3/2/2019 2.29653 3/3/2019 2.29662 3/4/2019 2.29671 3/5/2019 2.2968 3/6/2019 2.29689 3/7/2019 2.29698 3/8/2019 2.29707 3/9/2019 2.29716

- 29. 3/10/2019 2.29725 3/11/2019 2.29731 3/12/2019 2.29737 3/13/2019 2.29743 3/14/2019 2.29749 3/15/2019 2.29755 3/16/2019 2.29761 3/17/2019 2.29767 3/18/2019 2.29773 3/19/2019 2.29779 3/20/2019 2.29785 3/21/2019 2.29791 3/22/2019 2.29797 3/23/2019 2.29803 3/24/2019 2.29809 3/25/2019 2.29815 3/26/2019 2.29821 3/27/2019 2.29827 3/28/2019 2.29833 3/29/2019 2.29839 3/30/2019 2.29845 3/31/2019 2.29851 4/1/2019 2.29857 4/2/2019 2.29863 4/3/2019 2.29869 4/4/2019 2.29875 4/5/2019 2.29881 4/6/2019 2.29887 4/7/2019 2.29893 4/8/2019 2.29899 4/9/2019 2.29905 4/10/2019 2.29911 4/11/2019 2.29918 4/12/2019 2.29925 4/13/2019 2.29932 4/14/2019 2.29939 4/15/2019 2.29946 4/16/2019 2.29953

- 30. 4/17/2019 2.2996 4/18/2019 2.29967 4/19/2019 2.29974 4/20/2019 2.29981 4/21/2019 2.29988 4/22/2019 2.29995 4/23/2019 2.30002 4/24/2019 2.30009 4/25/2019 2.30016 4/26/2019 2.30023 4/27/2019 2.3003 4/28/2019 2.30037 4/29/2019 2.30044 4/30/2019 2.30051 5/1/2019 2.30058 5/2/2019 2.30065 5/3/2019 2.30072 5/4/2019 2.30079 5/5/2019 2.30086 5/6/2019 2.30093 5/7/2019 2.301 5/8/2019 2.30107 5/9/2019 2.30114 5/10/2019 2.30121 5/11/2019 2.30129 5/12/2019 2.30137 5/13/2019 2.30145 5/14/2019 2.30153 5/15/2019 2.30161 5/16/2019 2.30169 5/17/2019 2.30177 5/18/2019 2.30185 5/19/2019 2.30193 5/20/2019 2.30201 5/21/2019 2.30209 5/22/2019 2.30217 5/23/2019 2.30225 5/24/2019 2.30233

- 31. 5/25/2019 2.30241 5/26/2019 2.30249 5/27/2019 2.30257 5/28/2019 2.30265 5/29/2019 2.30273 5/30/2019 2.30281 5/31/2019 2.30289 6/1/2019 2.30298 6/2/2019 2.30307 6/3/2019 2.30316 6/4/2019 2.30325 6/5/2019 2.30334 6/6/2019 2.30343 6/7/2019 2.30352 6/8/2019 2.30361 6/9/2019 2.3037 6/10/2019 2.30379 6/11/2019 2.3039 6/12/2019 2.30401 6/13/2019 2.30412 6/14/2019 2.30423 6/15/2019 2.30434 6/16/2019 2.30445 6/17/2019 2.30456 6/18/2019 2.30467 6/19/2019 2.30478 6/20/2019 2.30489 6/21/2019 2.305 6/22/2019 2.30511 6/23/2019 2.30522 6/24/2019 2.30533 6/25/2019 2.30544 6/26/2019 2.30555 6/27/2019 2.30566 6/28/2019 2.30577 6/29/2019 2.30588 6/30/2019 2.30599 7/1/2019 2.30609

- 32. 7/2/2019 2.30619 7/3/2019 2.30629 7/4/2019 2.30639 7/5/2019 2.30649 7/6/2019 2.30659 7/7/2019 2.30669 7/8/2019 2.30679 7/9/2019 2.30689 7/10/2019 2.30699 7/11/2019 2.3071 7/12/2019 2.30721 7/13/2019 2.30732 7/14/2019 2.30743 7/15/2019 2.30754 7/16/2019 2.30765 7/17/2019 2.30776 7/18/2019 2.30787 7/19/2019 2.30798 7/20/2019 2.30809 7/21/2019 2.3082 7/22/2019 2.30831 7/23/2019 2.30842 7/24/2019 2.30853 7/25/2019 2.30864 7/26/2019 2.30875 7/27/2019 2.30886 7/28/2019 2.30897 7/29/2019 2.30908 7/30/2019 2.30919 7/31/2019 2.3093 8/1/2019 2.30941 8/2/2019 2.30952 8/3/2019 2.30963 8/4/2019 2.30974 8/5/2019 2.30985 8/6/2019 2.30996 8/7/2019 2.31007 8/8/2019 2.31018

- 33. 8/9/2019 2.31029 8/10/2019 2.3104 8/11/2019 2.31052 8/12/2019 2.31064 8/13/2019 2.31076 8/14/2019 2.31088 8/15/2019 2.311 8/16/2019 2.31112 8/17/2019 2.31124 8/18/2019 2.31136 8/19/2019 2.31148 8/20/2019 2.3116 8/21/2019 2.31172 8/22/2019 2.31184 8/23/2019 2.31196 8/24/2019 2.31208 8/25/2019 2.3122 8/26/2019 2.31232 8/27/2019 2.31244 8/28/2019 2.31256 8/29/2019 2.31268 8/30/2019 2.3128 8/31/2019 2.31292 9/1/2019 2.31304 9/2/2019 2.31316 9/3/2019 2.31328 9/4/2019 2.3134 9/5/2019 2.31352 9/6/2019 2.31364 9/7/2019 2.31376 9/8/2019 2.31388 9/9/2019 2.314 9/10/2019 2.31412 9/11/2019 2.31426 9/12/2019 2.3144 9/13/2019 2.31454 9/14/2019 2.31468 9/15/2019 2.31482

- 34. 9/16/2019 2.31496 9/17/2019 2.3151 9/18/2019 2.31524 9/19/2019 2.31538 9/20/2019 2.31552 9/21/2019 2.31566 9/22/2019 2.3158 9/23/2019 2.31594 9/24/2019 2.31608 9/25/2019 2.31622 9/26/2019 2.31636 9/27/2019 2.3165 9/28/2019 2.31664 9/29/2019 2.31678 9/30/2019 2.31692 10/1/2019 2.31706 10/2/2019 2.3172 10/3/2019 2.31734 10/4/2019 2.31748 10/5/2019 2.31762 10/6/2019 2.31776 10/7/2019 2.3179 10/8/2019 2.31804 10/9/2019 2.31818 10/10/2019 2.31832 10/11/2019 2.31846 10/12/2019 2.3186 10/13/2019 2.31874 10/14/2019 2.31888 10/15/2019 2.31902 10/16/2019 2.31916 10/17/2019 2.3193 10/18/2019 2.31944 10/19/2019 2.31958 10/20/2019 2.31972 10/21/2019 2.31986 10/22/2019 2.32 10/23/2019 2.32014

- 35. 10/24/2019 2.32028 10/25/2019 2.32042 10/26/2019 2.32056 10/27/2019 2.3207 10/28/2019 2.32084 10/29/2019 2.32098 10/30/2019 2.32112 10/31/2019 2.32126 11/1/2019 2.3214 11/2/2019 2.32154 11/3/2019 2.32168 11/4/2019 2.32182 11/5/2019 2.32196 11/6/2019 2.3221 11/7/2019 2.32224 11/8/2019 2.32238 11/9/2019 2.32252 11/10/2019 2.32266 11/11/2019 2.32282 11/12/2019 2.32298 11/13/2019 2.32314 11/14/2019 2.3233 11/15/2019 2.32346 11/16/2019 2.32362 11/17/2019 2.32378 11/18/2019 2.32394 11/19/2019 2.3241 11/20/2019 2.32426 11/21/2019 2.32442 11/22/2019 2.32458 11/23/2019 2.32474 11/24/2019 2.3249 11/25/2019 2.32506 11/26/2019 2.32522 11/27/2019 2.32538 11/28/2019 2.32554 11/29/2019 2.3257 11/30/2019 2.32586

- 36. 12/1/2019 2.32602 12/2/2019 2.32618 12/3/2019 2.32634 12/4/2019 2.3265 12/5/2019 2.32666 12/6/2019 2.32682 12/7/2019 2.32698 12/8/2019 2.32714 12/9/2019 2.3273 12/10/2019 2.32746 12/11/2019 2.32767 12/12/2019 2.32788 12/13/2019 2.32809 12/14/2019 2.3283 12/15/2019 2.32851 12/16/2019 2.32872 12/17/2019 2.32893 12/18/2019 2.32914 12/19/2019 2.32935 12/20/2019 2.32956 12/21/2019 2.32977 12/22/2019 2.32998 12/23/2019 2.33019 12/24/2019 2.3304 12/25/2019 2.33061 12/26/2019 2.33082 12/27/2019 2.33103 12/28/2019 2.33124 12/29/2019 2.33145 12/30/2019 2.33166 12/31/2019 2.33187 1/1/2020 2.33208 1/2/2020 2.33229 1/3/2020 2.3325 1/4/2020 2.33271 1/5/2020 2.33292 1/6/2020 2.33313 1/7/2020 2.33334

- 37. 1/8/2020 2.33355 1/9/2020 2.33376 1/10/2020 2.33397 1/11/2020 2.33406 1/12/2020 2.33415 1/13/2020 2.33424 1/14/2020 2.33433 1/15/2020 2.33442 1/16/2020 2.33451 1/17/2020 2.3346 1/18/2020 2.33469 1/19/2020 2.33478 1/20/2020 2.33487 1/21/2020 2.33496 1/22/2020 2.33505 1/23/2020 2.33514 1/24/2020 2.33523 1/25/2020 2.33532 1/26/2020 2.33541 1/27/2020 2.3355 1/28/2020 2.33559 1/29/2020 2.33568 1/30/2020 2.33577 1/31/2020 2.33586 2/1/2020 2.33596 2/2/2020 2.33606 2/3/2020 2.33616 2/4/2020 2.33626 2/5/2020 2.33636 2/6/2020 2.33646 2/7/2020 2.33656 2/8/2020 2.33666 2/9/2020 2.33676 2/10/2020 2.33686 2/11/2020 2.33694 2/12/2020 2.33702 2/13/2020 2.3371 2/14/2020 2.33718

- 38. 2/15/2020 2.33726 2/16/2020 2.33734 2/17/2020 2.33742 2/18/2020 2.3375 2/19/2020 2.33758 2/20/2020 2.33766 2/21/2020 2.33774 2/22/2020 2.33782 2/23/2020 2.3379 2/24/2020 2.33798 2/25/2020 2.33806 2/26/2020 2.33814 2/27/2020 2.33822 2/28/2020 2.3383 2/29/2020 2.33838 3/1/2020 2.33846 3/2/2020 2.33854 3/3/2020 2.33862 3/4/2020 2.3387 3/5/2020 2.33878 3/6/2020 2.33886 3/7/2020 2.33894 3/8/2020 2.33902 3/9/2020 2.3391 3/10/2020 2.33918 3/11/2020 2.33926 3/12/2020 2.33934 3/13/2020 2.33942 3/14/2020 2.3395 3/15/2020 2.33958 3/16/2020 2.33966 3/17/2020 2.33974 3/18/2020 2.33982 3/19/2020 2.3399 3/20/2020 2.33998 3/21/2020 2.34006 3/22/2020 2.34014 3/23/2020 2.34022

- 39. 3/24/2020 2.3403 3/25/2020 2.34038 3/26/2020 2.34046 3/27/2020 2.34054 3/28/2020 2.34062 3/29/2020 2.3407 3/30/2020 2.34078 3/31/2020 2.34086 4/1/2020 2.34094 4/2/2020 2.34102 4/3/2020 2.3411 4/4/2020 2.34118 4/5/2020 2.34126 4/6/2020 2.34134 4/7/2020 2.34142 4/8/2020 2.3415 4/9/2020 2.34158 4/10/2020 2.34166 4/11/2020 2.34175 4/12/2020 2.34184 4/13/2020 2.34193 4/14/2020 2.34202 4/15/2020 2.34211 4/16/2020 2.3422 4/17/2020 2.34229 4/18/2020 2.34238 4/19/2020 2.34247 4/20/2020 2.34256 4/21/2020 2.34265 4/22/2020 2.34274 4/23/2020 2.34283 4/24/2020 2.34292 4/25/2020 2.34301 4/26/2020 2.3431 4/27/2020 2.34319 4/28/2020 2.34328 4/29/2020 2.34337 4/30/2020 2.34346

- 40. 5/1/2020 2.34355 5/2/2020 2.34364 5/3/2020 2.34373 5/4/2020 2.34382 5/5/2020 2.34391 5/6/2020 2.344 5/7/2020 2.34409 5/8/2020 2.34418 5/9/2020 2.34427 5/10/2020 2.34436 5/11/2020 2.34447 5/12/2020 2.34458 5/13/2020 2.34469 5/14/2020 2.3448 5/15/2020 2.34491 5/16/2020 2.34502 5/17/2020 2.34513 5/18/2020 2.34524 5/19/2020 2.34535 5/20/2020 2.34546 5/21/2020 2.34557 5/22/2020 2.34568 5/23/2020 2.34579 5/24/2020 2.3459 5/25/2020 2.34601 5/26/2020 2.34612 5/27/2020 2.34623 5/28/2020 2.34634 5/29/2020 2.34645 5/30/2020 2.34656 5/31/2020 2.34667 6/1/2020 2.34678 6/2/2020 2.34689 6/3/2020 2.347 6/4/2020 2.34711 6/5/2020 2.34722 6/6/2020 2.34733 6/7/2020 2.34744

- 41. 6/8/2020 2.34755 6/9/2020 2.34766 6/10/2020 2.34777 6/11/2020 2.34785 6/12/2020 2.34793 6/13/2020 2.34801 6/14/2020 2.34809 6/15/2020 2.34817 6/16/2020 2.34825 6/17/2020 2.34833 6/18/2020 2.34841 6/19/2020 2.34849 6/20/2020 2.34857 6/21/2020 2.34865 6/22/2020 2.34873 6/23/2020 2.34881 6/24/2020 2.34889 6/25/2020 2.34897 6/26/2020 2.34905 6/27/2020 2.34913 6/28/2020 2.34921 6/29/2020 2.34929 6/30/2020 2.34937 7/1/2020 2.34945 7/2/2020 2.34953 7/3/2020 2.34961 7/4/2020 2.34969 7/5/2020 2.34977 7/6/2020 2.34985 7/7/2020 2.34993 7/8/2020 2.35001 7/9/2020 2.35009 7/10/2020 2.35017 7/11/2020 2.35026 7/12/2020 2.35035 7/13/2020 2.35044 7/14/2020 2.35053 7/15/2020 2.35062

- 42. 7/16/2020 2.35071 7/17/2020 2.3508 7/18/2020 2.35089 7/19/2020 2.35098 7/20/2020 2.35107 7/21/2020 2.35116 7/22/2020 2.35125 7/23/2020 2.35134 7/24/2020 2.35143 7/25/2020 2.35152 7/26/2020 2.35161 7/27/2020 2.3517 7/28/2020 2.35179 7/29/2020 2.35188 7/30/2020 2.35197 7/31/2020 2.35206 8/1/2020 2.35215 8/2/2020 2.35224 8/3/2020 2.35233 8/4/2020 2.35242 8/5/2020 2.35251 8/6/2020 2.3526 8/7/2020 2.35269 8/8/2020 2.35278 8/9/2020 2.35287 8/10/2020 2.35296 8/11/2020 2.35305 8/12/2020 2.35314 8/13/2020 2.35323 8/14/2020 2.35332 8/15/2020 2.35341 8/16/2020 2.3535 8/17/2020 2.35359 8/18/2020 2.35368 8/19/2020 2.35377 8/20/2020 2.35386 8/21/2020 2.35395 8/22/2020 2.35404

- 43. 8/23/2020 2.35413 8/24/2020 2.35422 8/25/2020 2.35431 8/26/2020 2.3544 8/27/2020 2.35449 8/28/2020 2.35458 8/29/2020 2.35467 8/30/2020 2.35476 8/31/2020 2.35485 9/1/2020 2.35494 9/2/2020 2.35503 9/3/2020 2.35512 9/4/2020 2.35521 9/5/2020 2.3553 9/6/2020 2.35539 9/7/2020 2.35548 9/8/2020 2.35557 9/9/2020 2.35566 9/10/2020 2.35575 9/11/2020 2.35584 9/12/2020 2.35593 9/13/2020 2.35602 9/14/2020 2.35611 9/15/2020 2.3562 9/16/2020 2.35629 9/17/2020 2.35638 9/18/2020 2.35647 9/19/2020 2.35656 9/20/2020 2.35665 9/21/2020 2.35674 9/22/2020 2.35683 9/23/2020 2.35692 9/24/2020 2.35701 9/25/2020 2.3571 9/26/2020 2.35719 9/27/2020 2.35728 9/28/2020 2.35737 9/29/2020 2.35746

- 44. 9/30/2020 2.35755 10/1/2020 2.35764 10/2/2020 2.35773 10/3/2020 2.35782 10/4/2020 2.35791 10/5/2020 2.358 10/6/2020 2.35809 10/7/2020 2.35818 10/8/2020 2.35827 10/9/2020 2.35836 10/10/2020 2.35845 10/11/2020 2.35848 10/12/2020 2.35851 10/13/2020 2.35854 10/14/2020 2.35857 10/15/2020 2.3586 10/16/2020 2.35863 10/17/2020 2.35866 10/18/2020 2.35869 10/19/2020 2.35872 10/20/2020 2.35875 10/21/2020 2.35878 10/22/2020 2.35881 10/23/2020 2.35884 10/24/2020 2.35887 10/25/2020 2.3589 10/26/2020 2.35893 10/27/2020 2.35896 10/28/2020 2.35899 10/29/2020 2.35902 10/30/2020 2.35905 10/31/2020 2.35908 11/1/2020 2.35911 11/2/2020 2.35914 11/3/2020 2.35917 11/4/2020 2.3592 11/5/2020 2.35923 11/6/2020 2.35926

- 45. 11/7/2020 2.35929 11/8/2020 2.35932 11/9/2020 2.35935 11/10/2020 2.35938 11/11/2020 2.3594 11/12/2020 2.35942 11/13/2020 2.35944 11/14/2020 2.35946 11/15/2020 2.35948 11/16/2020 2.3595 11/17/2020 2.35952 11/18/2020 2.35954 11/19/2020 2.35956 11/20/2020 2.35958 11/21/2020 2.3596 11/22/2020 2.35962 11/23/2020 2.35964 11/24/2020 2.35966 11/25/2020 2.35968 11/26/2020 2.3597 11/27/2020 2.35972 11/28/2020 2.35974 11/29/2020 2.35976 11/30/2020 2.35978 12/1/2020 2.3598 12/2/2020 2.35982 12/3/2020 2.35984 12/4/2020 2.35986 12/5/2020 2.35988 12/6/2020 2.3599 12/7/2020 2.35992 12/8/2020 2.35994 12/9/2020 2.35996 12/10/2020 2.35998 12/11/2020 2.35991 12/12/2020 2.35984 12/13/2020 2.35977 12/14/2020 2.3597

- 46. 12/15/2020 2.35963 12/16/2020 2.35956 12/17/2020 2.35949 12/18/2020 2.35942 12/19/2020 2.35935 12/20/2020 2.35928 12/21/2020 2.35921 12/22/2020 2.35914 12/23/2020 2.35907 12/24/2020 2.359 12/25/2020 2.35893 12/26/2020 2.35886 12/27/2020 2.35879 12/28/2020 2.35872 12/29/2020 2.35865 12/30/2020 2.35858 12/31/2020 2.35851 1/1/2021 2.35844 1/2/2021 2.35837 1/3/2021 2.3583 1/4/2021 2.35823 1/5/2021 2.35816 1/6/2021 2.35809 1/7/2021 2.35802 1/8/2021 2.35795 1/9/2021 2.35788 1/10/2021 2.35781 1/11/2021 2.35785 1/12/2021 2.35789 1/13/2021 2.35793 1/14/2021 2.35797 1/15/2021 2.35801 1/16/2021 2.35805 1/17/2021 2.35809 1/18/2021 2.35813 1/19/2021 2.35817 1/20/2021 2.35821 1/21/2021 2.35825

- 47. 1/22/2021 2.35829 1/23/2021 2.35833 1/24/2021 2.35837 1/25/2021 2.35841 1/26/2021 2.35845 1/27/2021 2.35849 1/28/2021 2.35853 1/29/2021 2.35857 1/30/2021 2.35861 1/31/2021 2.35865 2/1/2021 2.3587 2/2/2021 2.35875 2/3/2021 2.3588 2/4/2021 2.35885 2/5/2021 2.3589 2/6/2021 2.35895 2/7/2021 2.359 2/8/2021 2.35905 2/9/2021 2.3591 2/10/2021 2.35915 2/11/2021 2.35923 2/12/2021 2.35931 2/13/2021 2.35939 2/14/2021 2.35947 2/15/2021 2.35955 2/16/2021 2.35963 2/17/2021 2.35971 2/18/2021 2.35979 2/19/2021 2.35987 2/20/2021 2.35995 2/21/2021 2.36003 2/22/2021 2.36011 2/23/2021 2.36019 2/24/2021 2.36027 2/25/2021 2.36035 2/26/2021 2.36043 2/27/2021 2.36051 2/28/2021 2.36059

- 48. 3/1/2021 2.36066 3/2/2021 2.36073 3/3/2021 2.3608 3/4/2021 2.36087 3/5/2021 2.36094 3/6/2021 2.36101 3/7/2021 2.36108 3/8/2021 2.36115 3/9/2021 2.36122 3/10/2021 2.36129 3/11/2021 2.36138 3/12/2021 2.36147 3/13/2021 2.36156 3/14/2021 2.36165 3/15/2021 2.36174 3/16/2021 2.36183 3/17/2021 2.36192 3/18/2021 2.36201 3/19/2021 2.3621 3/20/2021 2.36219 3/21/2021 2.36228 3/22/2021 2.36237 3/23/2021 2.36246 3/24/2021 2.36255 3/25/2021 2.36264 3/26/2021 2.36273 3/27/2021 2.36282 3/28/2021 2.36291 3/29/2021 2.363 3/30/2021 2.36309 3/31/2021 2.36318 4/1/2021 2.36327 4/2/2021 2.36336 4/3/2021 2.36345 4/4/2021 2.36354 4/5/2021 2.36363 4/6/2021 2.36372 4/7/2021 2.36381

- 49. 4/8/2021 2.3639 4/9/2021 2.36399 4/10/2021 2.36408 4/11/2021 2.36416 4/12/2021 2.36424 4/13/2021 2.36432 4/14/2021 2.3644 4/15/2021 2.36448 4/16/2021 2.36456 4/17/2021 2.36464 4/18/2021 2.36472 4/19/2021 2.3648 4/20/2021 2.36488 4/21/2021 2.36496 4/22/2021 2.36504 4/23/2021 2.36512 4/24/2021 2.3652 4/25/2021 2.36528 4/26/2021 2.36536 4/27/2021 2.36544 4/28/2021 2.36552 4/29/2021 2.3656 4/30/2021 2.36568 5/1/2021 2.36575 5/2/2021 2.36582 5/3/2021 2.36589 5/4/2021 2.36596 5/5/2021 2.36603 5/6/2021 2.3661 5/7/2021 2.36617 5/8/2021 2.36624 5/9/2021 2.36631 5/10/2021 2.36638 5/11/2021 2.36642 5/12/2021 2.36646 5/13/2021 2.3665 5/14/2021 2.36654 5/15/2021 2.36658

- 50. 5/16/2021 2.36662 5/17/2021 2.36666 5/18/2021 2.3667 5/19/2021 2.36674 5/20/2021 2.36678 5/21/2021 2.36682 5/22/2021 2.36686 5/23/2021 2.3669 5/24/2021 2.36694 5/25/2021 2.36698 5/26/2021 2.36702 5/27/2021 2.36706 5/28/2021 2.3671 5/29/2021 2.36714 5/30/2021 2.36718 5/31/2021 2.36722 6/1/2021 2.36726 6/2/2021 2.3673 6/3/2021 2.36734 6/4/2021 2.36738 6/5/2021 2.36742 6/6/2021 2.36746 6/7/2021 2.3675 6/8/2021 2.36754 6/9/2021 2.36758 6/10/2021 2.36762 6/11/2021 2.36766 6/12/2021 2.3677 6/13/2021 2.36774 6/14/2021 2.36778 6/15/2021 2.36782 6/16/2021 2.36786 6/17/2021 2.3679 6/18/2021 2.36794 6/19/2021 2.36798 6/20/2021 2.36802 6/21/2021 2.36806 6/22/2021 2.3681

- 51. 6/23/2021 2.36814 6/24/2021 2.36818 6/25/2021 2.36822 6/26/2021 2.36826 6/27/2021 2.3683 6/28/2021 2.36834 6/29/2021 2.36838 6/30/2021 2.36842 7/1/2021 2.36845 7/2/2021 2.36848 7/3/2021 2.36851 7/4/2021 2.36854 7/5/2021 2.36857 7/6/2021 2.3686 7/7/2021 2.36863 7/8/2021 2.36866 7/9/2021 2.36869 7/10/2021 2.36872 7/11/2021 2.36873 7/12/2021 2.36874 7/13/2021 2.36875 7/14/2021 2.36876 7/15/2021 2.36877 7/16/2021 2.36878 7/17/2021 2.36879 7/18/2021 2.3688 7/19/2021 2.36881 7/20/2021 2.36882 7/21/2021 2.36883 7/22/2021 2.36884 7/23/2021 2.36885 7/24/2021 2.36886 7/25/2021 2.36887 7/26/2021 2.36888 7/27/2021 2.36889 7/28/2021 2.3689 7/29/2021 2.36891 7/30/2021 2.36892

- 52. 7/31/2021 2.36893 8/1/2021 2.36894 8/2/2021 2.36895 8/3/2021 2.36896 8/4/2021 2.36897 8/5/2021 2.36898 8/6/2021 2.36899 8/7/2021 2.369 8/8/2021 2.36901 8/9/2021 2.36902 8/10/2021 2.36903 8/11/2021 2.36904 8/12/2021 2.36905 8/13/2021 2.36906 8/14/2021 2.36907 8/15/2021 2.36908 8/16/2021 2.36909 8/17/2021 2.3691 8/18/2021 2.36911 8/19/2021 2.36912 8/20/2021 2.36913 8/21/2021 2.36914 8/22/2021 2.36915 8/23/2021 2.36916 8/24/2021 2.36917 8/25/2021 2.36918 8/26/2021 2.36919 8/27/2021 2.3692 8/28/2021 2.36921 8/29/2021 2.36922 8/30/2021 2.36923 8/31/2021 2.36924 9/1/2021 2.36925 9/2/2021 2.36926 9/3/2021 2.36927 9/4/2021 2.36928 9/5/2021 2.36929 9/6/2021 2.3693

- 53. 9/7/2021 2.36931 9/8/2021 2.36932 9/9/2021 2.36933 9/10/2021 2.36934 9/11/2021 2.36935 9/12/2021 2.36936 9/13/2021 2.36937 9/14/2021 2.36938 9/15/2021 2.36939 9/16/2021 2.3694 9/17/2021 2.36941 9/18/2021 2.36942 9/19/2021 2.36943 9/20/2021 2.36944 9/21/2021 2.36945 9/22/2021 2.36946 9/23/2021 2.36947 9/24/2021 2.36948 9/25/2021 2.36949 9/26/2021 2.3695 9/27/2021 2.36951 9/28/2021 2.36952 9/29/2021 2.36953 9/30/2021 2.36954 10/1/2021 2.36955 10/2/2021 2.36956 10/3/2021 2.36957 10/4/2021 2.36958 10/5/2021 2.36959 10/6/2021 2.3696 10/7/2021 2.36961 10/8/2021 2.36962 10/9/2021 2.36963 10/10/2021 2.36964 10/11/2021 2.3697 10/12/2021 2.36976 10/13/2021 2.36982 10/14/2021 2.36988

- 54. 10/15/2021 2.36994 10/16/2021 2.37 10/17/2021 2.37006 10/18/2021 2.37012 10/19/2021 2.37018 10/20/2021 2.37024 10/21/2021 2.3703 10/22/2021 2.37036 10/23/2021 2.37042 10/24/2021 2.37048 10/25/2021 2.37054 10/26/2021 2.3706 10/27/2021 2.37066 10/28/2021 2.37072 10/29/2021 2.37078 10/30/2021 2.37084 10/31/2021 2.3709 11/1/2021 2.37097 11/2/2021 2.37104 11/3/2021 2.37111 11/4/2021 2.37118 11/5/2021 2.37125 11/6/2021 2.37132 11/7/2021 2.37139 11/8/2021 2.37146 11/9/2021 2.37153 11/10/2021 2.3716 11/11/2021 2.37163 11/12/2021 2.37166 11/13/2021 2.37169 11/14/2021 2.37172 11/15/2021 2.37175 11/16/2021 2.37178 11/17/2021 2.37181 11/18/2021 2.37184 11/19/2021 2.37187 11/20/2021 2.3719 11/21/2021 2.37193

- 55. 11/22/2021 2.37196 11/23/2021 2.37199 11/24/2021 2.37202 11/25/2021 2.37205 11/26/2021 2.37208 11/27/2021 2.37211 11/28/2021 2.37214 11/29/2021 2.37217 11/30/2021 2.3722 12/1/2021 2.37223 12/2/2021 2.37226 12/3/2021 2.37229 12/4/2021 2.37232 12/5/2021 2.37235 12/6/2021 2.37238 12/7/2021 2.37241 12/8/2021 2.37244 12/9/2021 2.37247 12/10/2021 2.3725 12/11/2021 2.37256 12/12/2021 2.37262 12/13/2021 2.37268 12/14/2021 2.37274 12/15/2021 2.3728 12/16/2021 2.37286 12/17/2021 2.37292 12/18/2021 2.37298 12/19/2021 2.37304 12/20/2021 2.3731 12/21/2021 2.37316 12/22/2021 2.37322 12/23/2021 2.37328 12/24/2021 2.37334 12/25/2021 2.3734 12/26/2021 2.37346 12/27/2021 2.37352 12/28/2021 2.37358 12/29/2021 2.37364

- 56. 12/30/2021 2.3737 12/31/2021 2.37376 1/1/2022 2.37382 1/2/2022 2.37388 1/3/2022 2.37394 1/4/2022 2.374 1/5/2022 2.37406 1/6/2022 2.37412 1/7/2022 2.37418 1/8/2022 2.37424 1/9/2022 2.3743 1/10/2022 2.37436 1/11/2022 2.37442 1/12/2022 2.37448 1/13/2022 2.37454 1/14/2022 2.3746 1/15/2022 2.37466 1/16/2022 2.37472 1/17/2022 2.37478 1/18/2022 2.37484 1/19/2022 2.3749 1/20/2022 2.37496 1/21/2022 2.37502 1/22/2022 2.37508 1/23/2022 2.37514 1/24/2022 2.3752 1/25/2022 2.37526 1/26/2022 2.37532 1/27/2022 2.37538 1/28/2022 2.37544 1/29/2022 2.3755 1/30/2022 2.37556 1/31/2022 2.37562 2/1/2022 2.37568 2/2/2022 2.37574 2/3/2022 2.3758 2/4/2022 2.37586 2/5/2022 2.37592

- 57. 2/6/2022 2.37598 2/7/2022 2.37604 2/8/2022 2.3761 2/9/2022 2.37616 2/10/2022 2.37622 2/11/2022 2.37627 2/12/2022 2.37632 2/13/2022 2.37637 2/14/2022 2.37642 2/15/2022 2.37647 2/16/2022 2.37652 2/17/2022 2.37657 2/18/2022 2.37662 2/19/2022 2.37667 2/20/2022 2.37672 2/21/2022 2.37677 2/22/2022 2.37682 2/23/2022 2.37687 2/24/2022 2.37692 2/25/2022 2.37697 2/26/2022 2.37702 2/27/2022 2.37707 2/28/2022 2.37712 3/1/2022 2.37717 3/2/2022 2.37722 3/3/2022 2.37727 3/4/2022 2.37732 3/5/2022 2.37737 3/6/2022 2.37742 3/7/2022 2.37747 3/8/2022 2.37752 3/9/2022 2.37757 3/10/2022 2.37762 3/11/2022 2.37766 3/12/2022 2.3777 3/13/2022 2.37774 3/14/2022 2.37778 3/15/2022 2.37782

- 58. 3/16/2022 2.37786 3/17/2022 2.3779 3/18/2022 2.37794 3/19/2022 2.37798 3/20/2022 2.37802 3/21/2022 2.37806 3/22/2022 2.3781 3/23/2022 2.37814 3/24/2022 2.37818 3/25/2022 2.37822 3/26/2022 2.37826 3/27/2022 2.3783 3/28/2022 2.37834 3/29/2022 2.37838 3/30/2022 2.37842 3/31/2022 2.37846 4/1/2022 2.37851 4/2/2022 2.37856 4/3/2022 2.37861 4/4/2022 2.37866 4/5/2022 2.37871 4/6/2022 2.37876 4/7/2022 2.37881 4/8/2022 2.37886 4/9/2022 2.37891 4/10/2022 2.37896 4/11/2022 2.37901 4/12/2022 2.37906 4/13/2022 2.37911 4/14/2022 2.37916 4/15/2022 2.37921 4/16/2022 2.37926 4/17/2022 2.37931 4/18/2022 2.37936 4/19/2022 2.37941 4/20/2022 2.37946 4/21/2022 2.37951 4/22/2022 2.37956

- 59. 4/23/2022 2.37961 4/24/2022 2.37966 4/25/2022 2.37971 4/26/2022 2.37976 4/27/2022 2.37981 4/28/2022 2.37986 4/29/2022 2.37991 4/30/2022 2.37996 5/1/2022 2.38001 5/2/2022 2.38006 5/3/2022 2.38011 5/4/2022 2.38016 5/5/2022 2.38021 5/6/2022 2.38026 5/7/2022 2.38031 5/8/2022 2.38036 5/9/2022 2.38041 5/10/2022 2.38046 5/11/2022 2.38052 5/12/2022 2.38058 5/13/2022 2.38064 5/14/2022 2.3807 5/15/2022 2.38076 5/16/2022 2.38082 5/17/2022 2.38088 5/18/2022 2.38094 5/19/2022 2.381 5/20/2022 2.38106 5/21/2022 2.38112 5/22/2022 2.38118 5/23/2022 2.38124 5/24/2022 2.3813 5/25/2022 2.38136 5/26/2022 2.38142 5/27/2022 2.38148 5/28/2022 2.38154 5/29/2022 2.3816 5/30/2022 2.38166

- 60. 5/31/2022 2.38172 6/1/2022 2.38178 6/2/2022 2.38184 6/3/2022 2.3819 6/4/2022 2.38196 6/5/2022 2.38202 6/6/2022 2.38208 6/7/2022 2.38214 6/8/2022 2.3822 6/9/2022 2.38226 6/10/2022 2.38232 6/11/2022 2.38241 6/12/2022 2.3825 6/13/2022 2.38259 6/14/2022 2.38268 6/15/2022 2.38277 6/16/2022 2.38286 6/17/2022 2.38295 6/18/2022 2.38304 6/19/2022 2.38313 6/20/2022 2.38322 6/21/2022 2.38331 6/22/2022 2.3834 6/23/2022 2.38349 6/24/2022 2.38358 6/25/2022 2.38367 6/26/2022 2.38376 6/27/2022 2.38385 6/28/2022 2.38394 6/29/2022 2.38403 6/30/2022 2.38412 7/1/2022 2.38421 7/2/2022 2.3843 7/3/2022 2.38439 7/4/2022 2.38448 7/5/2022 2.38457 7/6/2022 2.38466 7/7/2022 2.38475

- 61. 7/8/2022 2.38484 7/9/2022 2.38493 7/10/2022 2.38502 7/11/2022 2.38513 7/12/2022 2.38524 7/13/2022 2.38535 7/14/2022 2.38546 7/15/2022 2.38557 7/16/2022 2.38568 7/17/2022 2.38579 7/18/2022 2.3859 7/19/2022 2.38601 7/20/2022 2.38612 7/21/2022 2.38623 7/22/2022 2.38634 7/23/2022 2.38645 7/24/2022 2.38656 7/25/2022 2.38667 7/26/2022 2.38678 7/27/2022 2.38689 7/28/2022 2.387 7/29/2022 2.38711 7/30/2022 2.38722 7/31/2022 2.38733 8/1/2022 2.38744 8/2/2022 2.38755 8/3/2022 2.38766 8/4/2022 2.38777 8/5/2022 2.38788 8/6/2022 2.38799 8/7/2022 2.3881 8/8/2022 2.38821 8/9/2022 2.38832 8/10/2022 2.38843 8/11/2022 2.38856 8/12/2022 2.38869 8/13/2022 2.38882 8/14/2022 2.38895

- 62. 8/15/2022 2.38908 8/16/2022 2.38921 8/17/2022 2.38934 8/18/2022 2.38947 8/19/2022 2.3896 8/20/2022 2.38973 8/21/2022 2.38986 8/22/2022 2.38999 8/23/2022 2.39012 8/24/2022 2.39025 8/25/2022 2.39038 8/26/2022 2.39051 8/27/2022 2.39064 8/28/2022 2.39077 8/29/2022 2.3909 8/30/2022 2.39103 8/31/2022 2.39116 9/1/2022 2.39129 9/2/2022 2.39142 9/3/2022 2.39155 9/4/2022 2.39168 9/5/2022 2.39181 9/6/2022 2.39194 9/7/2022 2.39207 9/8/2022 2.3922 9/9/2022 2.39233 9/10/2022 2.39246 9/11/2022 2.39256 9/12/2022 2.39266 9/13/2022 2.39276 9/14/2022 2.39286 9/15/2022 2.39296 9/16/2022 2.39306 9/17/2022 2.39316 9/18/2022 2.39326 9/19/2022 2.39336 9/20/2022 2.39346 9/21/2022 2.39356

- 63. 9/22/2022 2.39366 9/23/2022 2.39376 9/24/2022 2.39386 9/25/2022 2.39396 9/26/2022 2.39406 9/27/2022 2.39416 9/28/2022 2.39426 9/29/2022 2.39436 9/30/2022 2.39446 10/1/2022 2.39456 10/2/2022 2.39466 10/3/2022 2.39476 10/4/2022 2.39486 10/5/2022 2.39496 10/6/2022 2.39506 10/7/2022 2.39516 10/8/2022 2.39526 10/9/2022 2.39536 10/10/2022 2.39546 10/11/2022 10/12/2022 10/13/2022 10/14/2022 10/15/2022 10/16/2022 10/17/2022 10/18/2022 10/19/2022 10/20/2022 10/21/2022 10/22/2022 10/23/2022 10/24/2022 10/25/2022 10/26/2022 10/27/2022 10/28/2022 10/29/2022

- 68. LLA DE APORTES PATRONALES AL SSO, PRO VIVIENDA Y PROVISION PARA BENEFICIOS SOC SEGURO S. O. PRO ROV. BENEF. SOCIALE Nro. NOMBRES TOTAL CNS R. PROF.AP.PAT. SOLVIVIENDA INDEM. GUINALDO TOTAL GANADO 10% 1.71% 3% 2% 8.33% 8.33% 1 ROBERTO CARLOS 0.00 0.00 0.00 0.00 0.00 0.00 0.00 2 JENNIFER LOPEZ 0.00 0.00 0.00 0.00 0.00 0.00 0.00 3 RICHARD COSSIANTE 0.00 0.00 0.00 0.00 0.00 0.00 0.00 4 ALBERTO PLAZA 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5 PAULINA RUBIO 0.00 0.00 0.00 0.00 0.00 0.00 0.00 6 RICARDO MONTANER 0.00 0.00 0.00 0.00 0.00 0.00 0.00 7 MIGUEL BOSSE 0.00 0.00 0.00 0.00 0.00 0.00 0.00 8 MILTON CORTEZ 0.00 0.00 0.00 0.00 0.00 0.00 0.00 9 ALEJANDRO FERNANDEZ 0.00 0.00 0.00 0.00 0.00 0.00 0.00 10 PATRICIA VENEGAS 0.00 0.00 0.00 0.00 0.00 0.00 0.00 11 CRISTIAN CASTRO 0.00 0.00 0.00 0.00 0.00 0.00 0.00 TOTALES 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00