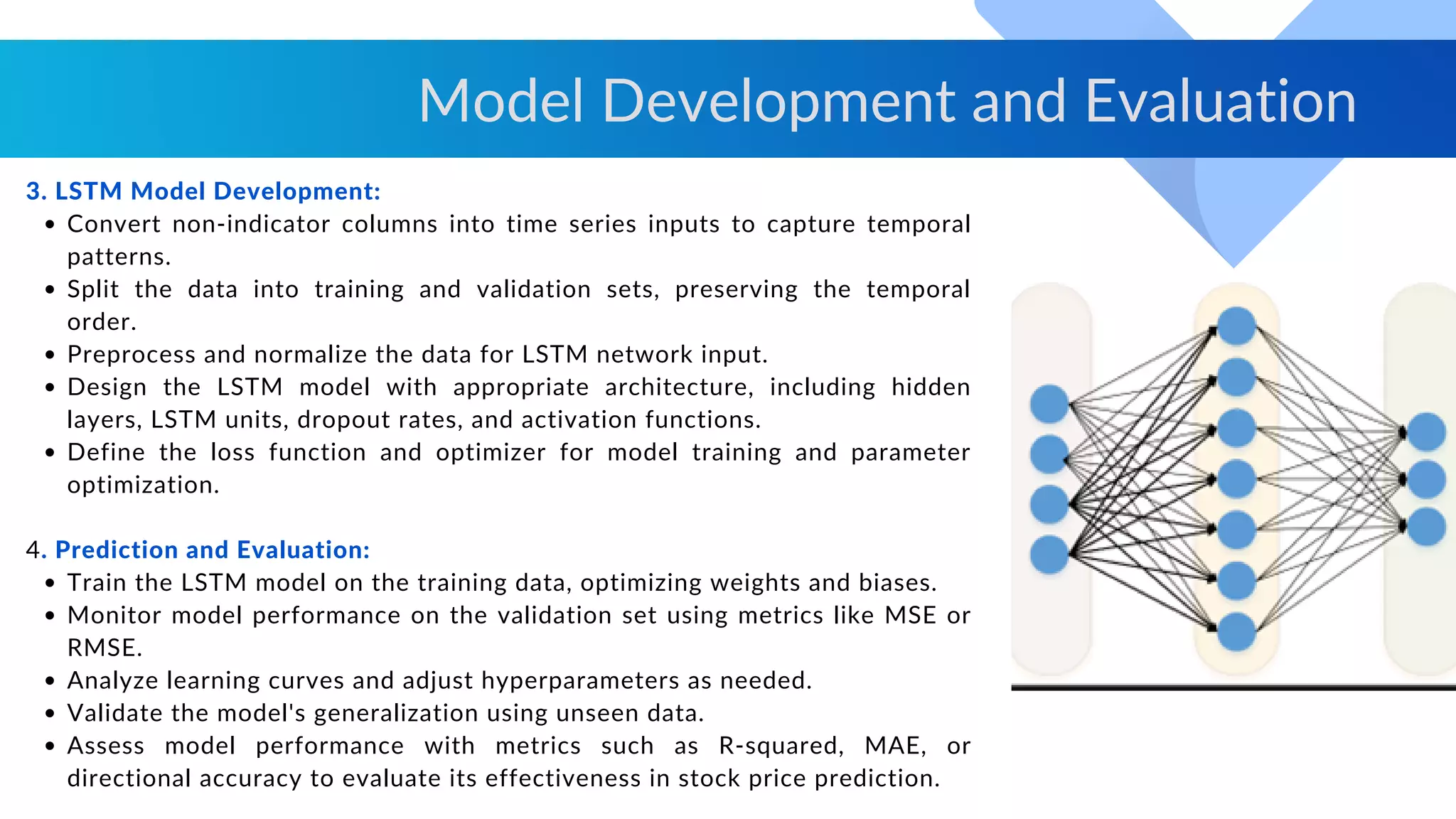

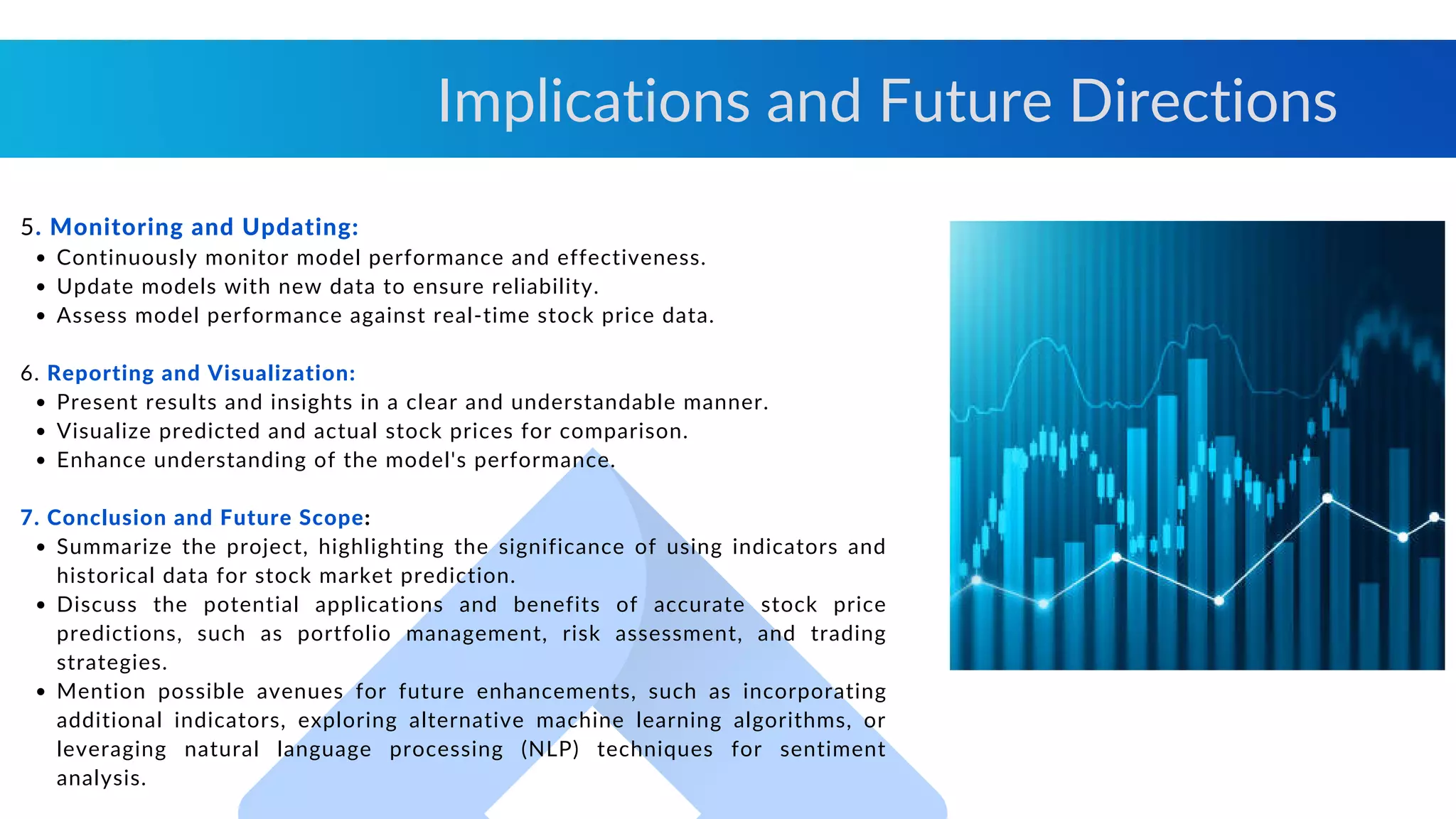

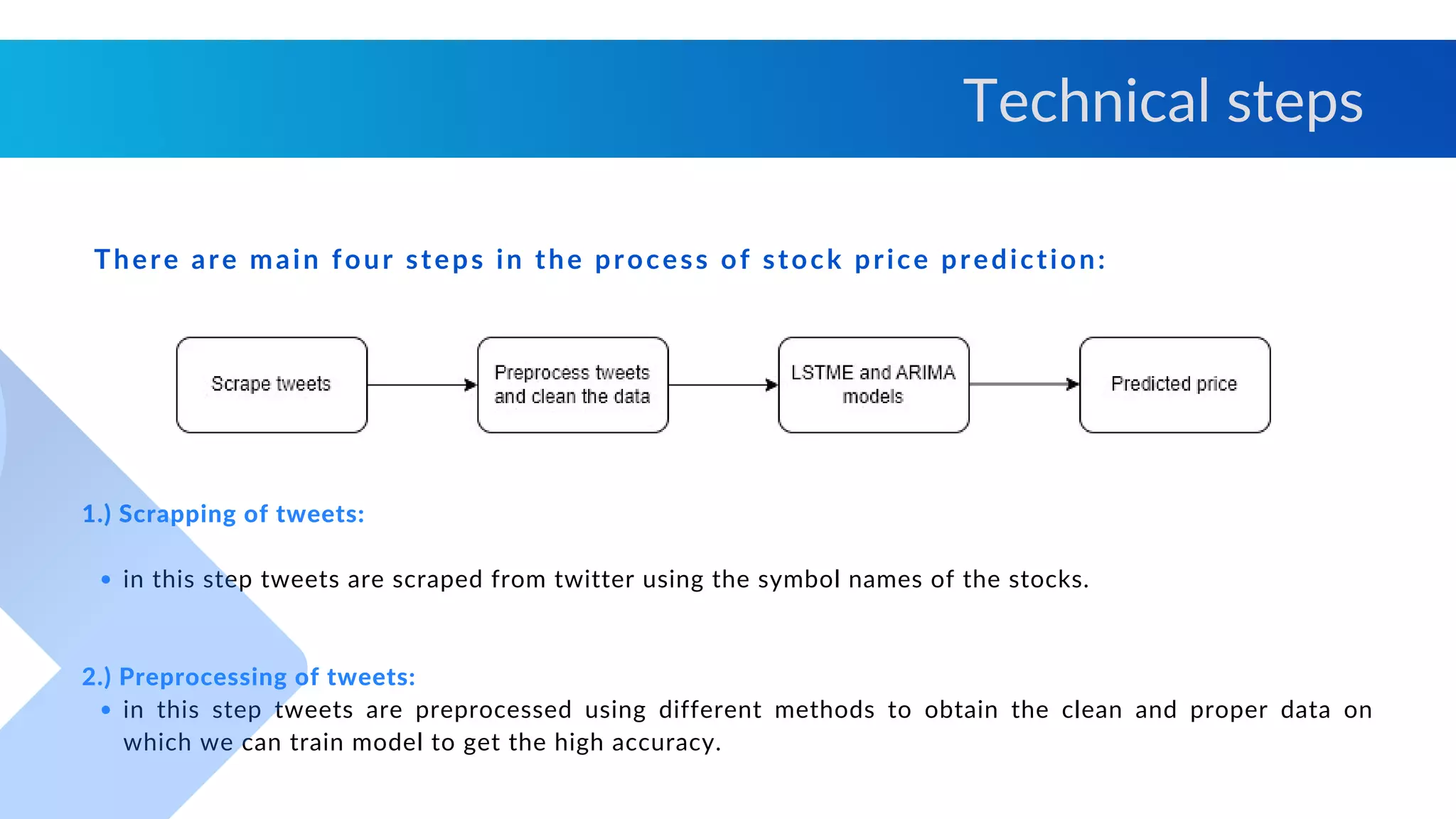

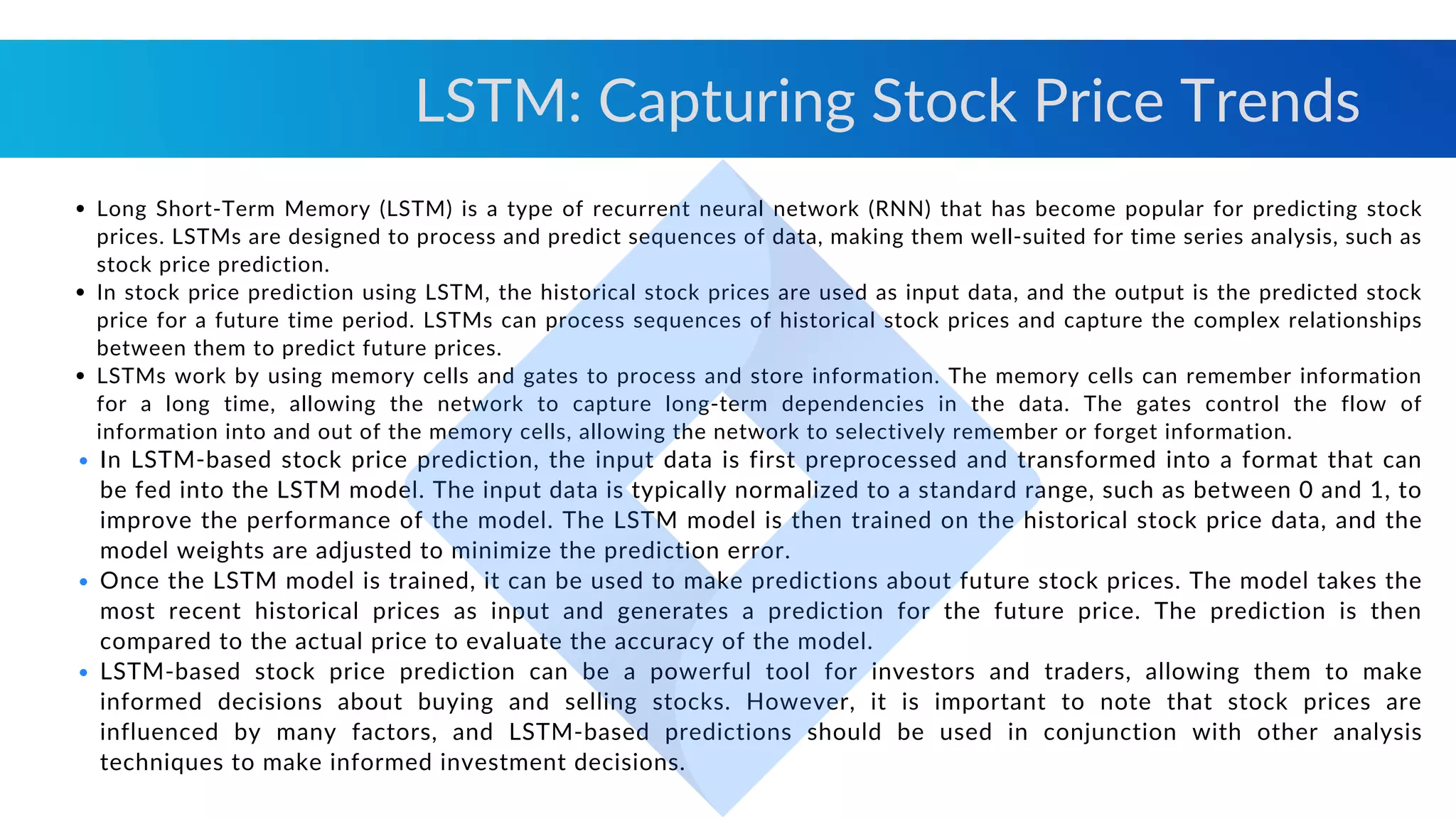

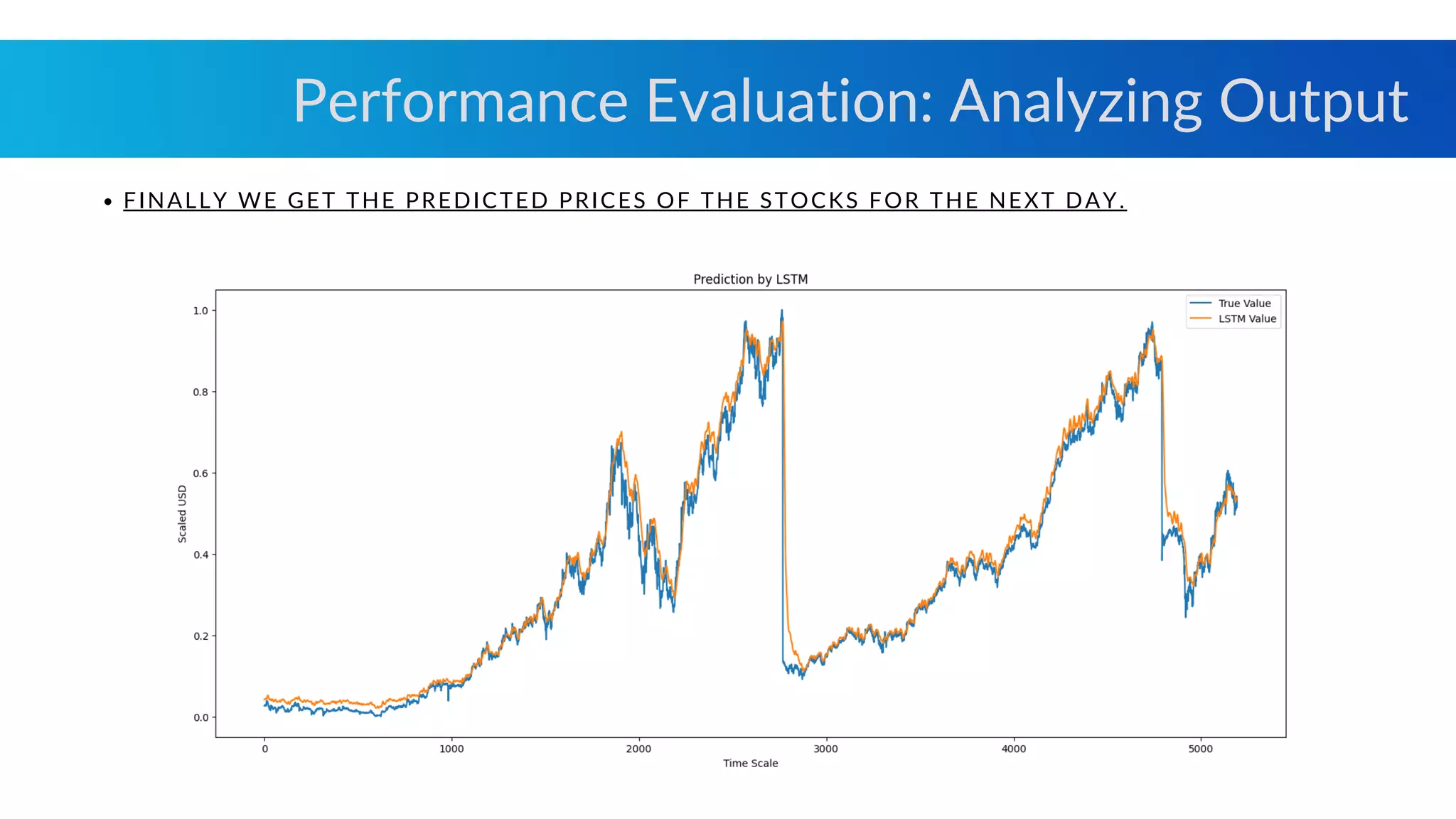

The document outlines a method for predicting stock prices using Long Short-Term Memory (LSTM) networks, focusing on data preparation, model development, and evaluation. It discusses the importance of market sentiment and the integration of historical data and indicators for effective predictions. Additionally, it highlights steps for data scraping, preprocessing, and enhancing model accuracy through continuous monitoring and updates.

![[DSC Europe 25] Ivan Peric - Intelligence Swarm Logic and Techno-Functional M...](https://cdn.slidesharecdn.com/ss_thumbnails/7my7c97fsduiccadgavw-2-251212103249-5a03f7c6-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Uros Pesic - The Reality of AI in Marketing.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/rtkodnmtycovsllvzsyn-9-251215095918-b0c6bfe3-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Nikolay Burlutskiy - Best Practices for Building Enterprise M...](https://cdn.slidesharecdn.com/ss_thumbnails/uirvaiuvq8y1w8hzd9tx-7-251212103249-2619edb4-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Debmalya Biswas - Agentification: the art of transforming man...](https://cdn.slidesharecdn.com/ss_thumbnails/r5azlggvtqiaiiusrqdr-4-251212103249-5a12c89b-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Hans Kleinsman - The Compliance Gearbox: How Tax Tech Mediate...](https://cdn.slidesharecdn.com/ss_thumbnails/dxdytie1toel0hr90bjs-2-251212103250-174fdbe7-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Djordje Hirs - Revolutionizing Telco Customer Experience with...](https://cdn.slidesharecdn.com/ss_thumbnails/zif75aur3qscnckv6tnc-djordje-hirs-cc-dsc2025-1-251219145617-679178aa-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Dobrica Cosic - From Electrons to Innovation: How Granular Da...](https://cdn.slidesharecdn.com/ss_thumbnails/h4qk69zereaumbceubgr-dobrica-cosic-from-electrons-to-innovation-how-granular-data-and-analytics-are--251218085301-b982fb14-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Maria Kokiasmenos - AI Governance US Perspective.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/eszqnbzlsqa2vch6dmci-6-251215095918-6fcdf45f-thumbnail.jpg?width=640&height=640&fit=bounds)