State Bank of India - Flat/House/Plot Registration Request Form

•

0 likes•704 views

Guidelines for property registration at Bangalore, India and list of documents to be submitted to Retail Assets Central Processing Centre (RACPC)

More Related Content

Similar to State Bank of India - Flat/House/Plot Registration Request Form

Similar to State Bank of India - Flat/House/Plot Registration Request Form (20)

Recently uploaded

Recently uploaded (17)

State Bank of India - Flat/House/Plot Registration Request Form

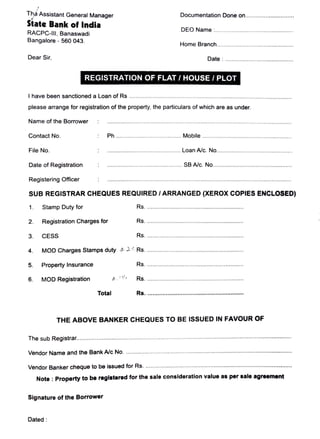

- 1. T~ Assistant General Manager State Bank of India RACPC-I11 , Banaswadi Bangalore - 560 043. Dear Sir, Documentation Done on............................. DEO Name :............................................... Home Branch.............................................. Date : ......................................... REGISTRATION OF FLAT/ HOUSE/ PLOT I have been sanctioned a Loan of Rs ·································································································· please arrange for registration of the property, the particulars of which are as under. Name of the Borrower Contact No. File No. Date of Registration Registering Officer Ph ....................................... Mobile ...................................................... ............................................ Loan Ale. No.............................................. ............................................. SB Ale. No................................................ SUB REGISTRAR CHEQUES REQUIRED/ ARRANGED (XEROX COPIES ENCLOSED) 1. Stamp Duty for Rs. ......... .. .. ... ......... ....... ........ ... ............. .. 2. Registration Charges for Rs. .......... ........ ...... .. .. .. ........... .. ............... 3. CESS Rs........ ............ .. ... .... ............... ............... 4. MOD Charges Stamps duty ~-:i.._.,, Rs........................................................... 5. Property Insurance Rs.......... .......................,......................... 6. MOD Registration ~.''I' Rs. ........... .. ............................................. Total Rs........................................................... THE ABOVE BANKER CHEQUES TO BE ISSUED IN FAVOUR OF The sub Registrar...............................................................••••••• ....•• .. •..•..•• ..•• ........··..·...··..·..•··•·•.....•·.. • Vendor Name and the Bank Ale No. .. .................................................................... .. ............................ Vendor Banker cheque to be issued for Rs. ........................................................................................ Note : Property to be registered for the sale consideration value as per sale agreement Signature of the Borrower Dated :

- 2. The Assistant General Manager State Bank of India RACPC-111, Banaswadi Bangalore - 560 043. UNDERTAKING PENAL INTEREST ON NON-COMPLIANCE TO AGREED TERMS AND CONDITIONS Penal Interest@ 2% over and above the agreed interest rate will be recovered from the customers for the delayed period on the entire outstanding in cases where valid mortgage is not created by the borrowers in favour of the Bank within 60 days of execution of Sale deed or issue of possession letter by builders / Occupation certificate, whichever is earlier. NAME : Address : Loan Account No. File No. Registration Date : I / We hereby undertake to submit the Sale deed and the related documents, after registration, to create a Valid Mortgage, within 60 days of execution of Sale deed or issue of possession letter by builders / Occupation certificate, whichever is earlier, failing which the Bank may charge Penal Interest @ 2% over and above the agreed interest rate will be recovered from the customers for the delayed period on the entire outstanding For State Bank of.India Asst General Manager RACPC-111, Banaswadi Signature of Customer

- 3. 0 State Bank of India R.A.C.P.C. - Ill GUIDELINES FOR REGISTRATION AND LIST OF DOCUMENTS TO BE SUBMITTED AT RACPC BANASWADI AFTER REGISTRATION FOR NEW FLATS REGISTERED 1.< SALE DEED 2.r SALE AGREEMENT 3.' REGISTERED MOD (APPLICABLE FOR LOANS ABOVE 25 LACS) 4. I LATEST ENCUMBERANCE CERTIFICATE AFTER REGISTRATION (FROM REGISTRAR OFFICE) FOR REGISTERED PLOTS OR RESOLD FLATS 1. ALL THE ABOVE FOUR DOCUMENTS AND 2. ALL DOCUMENTS IN ORIGINALS FROM THE SELLERS AS LAID DOWN IN TITLE INVESTIGATION REPORT BY LAWYER (LEGAL OPINION) FOR TAKEOVER LOANS FROM OTHER BANKS : 1. LOAN CLOSURE LETTER FR0 M THE RESPECTIVE BANKS 2. ALL DOCUMENTS AS PER THE LIST OF DOCUMENTS HANDED OVER TO THE CUSTOMER FROM THE PREVIOUS BANK. MOD TO BE REGISTERED AND LATEST EC TO BE OBTAINED AFTER MOD REGISTERED MOD (APPLICABLE FOR LOANS ABOVE 25 LACS) NOTE: 1. SALE DEED TO BE REGISTERED FOR THE SALE VALUE AS AGREED UPON IN THE SALE AGREEMENT AT THE TIME OF SANCTION. 2. THE REGISTRATION HAS TO BE DONE IN SINGLE OR JOINT NAMES AS AGREED UPON IN THE SALE AGREEMENT, NO ADDITION OR DELETION OF NAMES IS ALLOWED 3. ACKNOWLEDGMENT FOR THE RECEIPT OF DOCUMENTS AND THE MAXGAIN ACTIVATION LETTER WILL BE GIVEN ON RECEIPT OF ALL DOCUMENTS. PLEASE ACCOMPANY THE BUILDER WHERE THE BUILDER INSISTS TO HANDOVER THE DOCUMENTS BY HIMSELF.