Stat Arb Performance

•

0 likes•169 views

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. However, it has experienced lower drawdowns than the S&P 500 and has a very low correlation and beta to the index, demonstrating that it performs differently than broad market movements.

Report

Share

Report

Share

Download to read offline

Recommended

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. However, it has experienced smaller drawdowns and has a very low correlation and beta to the index, demonstrating that it performs differently than the broader market.

Stat Arb Performance

The statistical arbitrage fund reported lower returns than the S&P 500 since inception in March 2011, with annualized returns of -6.52% compared to -9.13% for the S&P 500. The fund exhibited much lower volatility than the market with an annualized volatility of 8.57% versus 26.37% for the S&P 500. While the fund lagged the sharply rising market in December, its maximum drawdown was lower than the S&P 500's at -9.39% versus -19.39%.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. It shows that the stat arb strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. Specifically, the stat arb strategy has returned -4.45% since inception compared to -6.15% for the S&P 500. The strategy also has lower correlation and beta to the market compared to the S&P 500.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. Some key points:

- The stat arb strategy has underperformed the S&P 500 since inception, with returns of -2.87% versus -8.33% for the index. It has lower annualized volatility and maximum drawdown.

- On a monthly basis the strategy is up 0.55% in October, compared to a 7.42% gain for the S&P 500.

- The strategy has experienced negative returns on its worst days but outperformed the market, while underperforming on the index's best days.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. It shows that the stat arb strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. Specifically, the stat arb strategy has returned -3.65% since inception compared to -3.07% for the S&P 500. It also has significantly lower risk than the overall market as measured by its beta of 0.07.

Stat Arb Performance

The statistical arbitrage strategy has underperformed the S&P 500 index since inception in March 2011, with lower annualized and monthly returns. However, the strategy has significantly lower risk measures like volatility, beta, and maximum drawdown. While the S&P 500 had its best days, the strategy either had small negative returns or gains on those same days, showing it can provide downside protection in strong market moves.

Stat Arb Performance

The statistical arbitrage fund (StatArb) has underperformed the S&P 500 index since inception in March 2011. StatArb has an annualized return of -3.57% compared to -16.74% for the S&P 500. In the past month, StatArb returned 1.54% while the S&P 500 returned 6.70%. StatArb has lower risk than the S&P 500 as measured by annualized volatility of 8.48% versus 25.59% for the S&P 500.

Stat Arb Performance

The statistical arbitrage strategy has outperformed the S&P 500 since inception in March 2011, with lower volatility and maximum drawdown. It has an annualized return of -2.08% compared to -17.2% for the S&P 500. While it has a low correlation of 0.3 to the index, it has also achieved positive returns on several of the S&P 500's worst days through hedging strategies.

Recommended

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. However, it has experienced smaller drawdowns and has a very low correlation and beta to the index, demonstrating that it performs differently than the broader market.

Stat Arb Performance

The statistical arbitrage fund reported lower returns than the S&P 500 since inception in March 2011, with annualized returns of -6.52% compared to -9.13% for the S&P 500. The fund exhibited much lower volatility than the market with an annualized volatility of 8.57% versus 26.37% for the S&P 500. While the fund lagged the sharply rising market in December, its maximum drawdown was lower than the S&P 500's at -9.39% versus -19.39%.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. It shows that the stat arb strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. Specifically, the stat arb strategy has returned -4.45% since inception compared to -6.15% for the S&P 500. The strategy also has lower correlation and beta to the market compared to the S&P 500.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. Some key points:

- The stat arb strategy has underperformed the S&P 500 since inception, with returns of -2.87% versus -8.33% for the index. It has lower annualized volatility and maximum drawdown.

- On a monthly basis the strategy is up 0.55% in October, compared to a 7.42% gain for the S&P 500.

- The strategy has experienced negative returns on its worst days but outperformed the market, while underperforming on the index's best days.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. It shows that the stat arb strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. Specifically, the stat arb strategy has returned -3.65% since inception compared to -3.07% for the S&P 500. It also has significantly lower risk than the overall market as measured by its beta of 0.07.

Stat Arb Performance

The statistical arbitrage strategy has underperformed the S&P 500 index since inception in March 2011, with lower annualized and monthly returns. However, the strategy has significantly lower risk measures like volatility, beta, and maximum drawdown. While the S&P 500 had its best days, the strategy either had small negative returns or gains on those same days, showing it can provide downside protection in strong market moves.

Stat Arb Performance

The statistical arbitrage fund (StatArb) has underperformed the S&P 500 index since inception in March 2011. StatArb has an annualized return of -3.57% compared to -16.74% for the S&P 500. In the past month, StatArb returned 1.54% while the S&P 500 returned 6.70%. StatArb has lower risk than the S&P 500 as measured by annualized volatility of 8.48% versus 25.59% for the S&P 500.

Stat Arb Performance

The statistical arbitrage strategy has outperformed the S&P 500 since inception in March 2011, with lower volatility and maximum drawdown. It has an annualized return of -2.08% compared to -17.2% for the S&P 500. While it has a low correlation of 0.3 to the index, it has also achieved positive returns on several of the S&P 500's worst days through hedging strategies.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 on a cumulative and annualized return basis, but has significantly lower volatility, beta, and maximum drawdown. It has experienced negative returns on the S&P 500's best up days and positive returns on some of the S&P 500's worst down days, demonstrating an ability to achieve alpha in volatile markets.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and lower risk as measured by volatility, beta, and maximum drawdown. On its best days, the strategy failed to outperform the market's gains, but on the market's worst days, the strategy either gained or had smaller losses than the S&P 500.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. Some key points:

- The stat arb strategy has underperformed the S&P 500 since inception with returns of -2.07% versus -7.30% for the index. However, it has significantly lower risk as measured by volatility and maximum drawdown.

- On a daily basis, the strategy has generally had slightly negative or positive returns on good and bad days for the market, resulting in an annualized alpha of -2.40% versus the index.

- Risk measures like beta, correlation, and volatility are much lower for the strategy compared

Stat Arb Performance

The statistical arbitrage fund has underperformed the S&P 500 index since inception in March 2011. It has lower annualized returns, lower monthly returns currently, and a larger maximum drawdown than the S&P 500. However, it also has significantly lower risk measures like volatility, beta, and correlation to the stock market. The statistical arbitrage strategy experienced its best days on different dates than large down days in the stock market, indicating it may provide diversification during market downturns.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has outperformed the S&P 500 with lower volatility, beta, correlation and maximum drawdown. Specifically, the statistical arbitrage strategy has returned -3.24% annually compared to -12.61% for the S&P 500.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. However, it has experienced lower drawdowns than the S&P 500 and has a low correlation and beta, demonstrating that it performs differently than the broader market.

Stat Arb Performance

The statistical arbitrage fund has underperformed the S&P 500 since inception in March 2011, with returns of -3.04% compared to -8.27% for the S&P 500. The fund has lower risk metrics like volatility, beta, and maximum drawdown. It has daily alpha of -2 basis points and annualized alpha of -4.06% compared to the S&P 500. The best and worst days for the fund differ from the S&P 500 on those same days.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. It shows that the stat arb strategy has outperformed the S&P 500 with lower volatility, beta, and maximum drawdown, though it has a negative annualized return. Specifically, it provides the best and worst 3 market days for both the index and strategy.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The stat arb strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. However, it has experienced lower drawdowns and has a low correlation to the index, providing some diversification during down markets.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy called StatArb compared to the S&P 500 index since inception on March 31, 2011. Some key points:

- StatArb has underperformed the S&P 500 since inception, with returns of -2.83% versus -7.58% for the S&P 500. Its annualized returns and volatility have also been lower.

- StatArb has experienced less volatility, drawdown, and correlation to the market than the S&P 500 as evidenced by its lower beta, correlation, and maximum drawdown.

- On the best 3 days for the market, StatArb underperformed or had small positive returns

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 on a cumulative and annualized return basis but with lower volatility, beta, and maximum drawdown. It has experienced negative returns on the S&P 500's best up days but gains on some of its worst down days.

Stat Arb Performance

The statistical arbitrage strategy has underperformed the S&P 500 since inception in March 2011, with lower annualized returns and higher volatility. However, it has experienced smaller drawdowns than the market and has a near-zero correlation and beta to the S&P 500, demonstrating its ability to act as a hedge against general market moves.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. It shows that the stat arb strategy has lower overall returns, volatility, maximum drawdown and beta than the S&P 500 over this period. Specifically, the stat arb strategy has returned -2.79% since inception compared to -5.48% for the S&P 500. It also has an annualized alpha of -3.98% compared to the S&P 500.

Stat Arb Performance

The statistical arbitrage fund has outperformed the S&P 500 index since inception in March 2011, with returns of -3.38% compared to -12.37% for the S&P 500. The fund has lower risk metrics like volatility, beta, and maximum drawdown. It has experienced positive returns on the S&P 500's worst days and negative returns on some of the S&P 500's best days, demonstrating its ability to produce returns independent of the overall market direction.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception in March 2011. The stat arb strategy has underperformed the index with lower annualized returns and higher volatility. However, it has experienced smaller drawdowns and has a very low correlation to the index, indicating it provides diversification during market downturns. The strategy lagged on the index's best days but outperformed on some of its worst days.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. However, it has experienced much smaller drawdowns than the S&P 500 and has a very low correlation and beta, indicating it performs differently than the broader market.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. However, it has experienced lower drawdowns than the S&P 500 and has a low correlation and beta, demonstrating it can act as a hedge in falling markets.

Stat Arb Performance

This statistical arbitrage strategy has underperformed the S&P 500 since its inception in March 2011, with annualized returns of -4.74% compared to -8.06% for the S&P. It has lower volatility, beta, correlation, and maximum drawdown than the market. While it had negative returns on three of the S&P's best days, it was positive on two of the market's worst three days over the period.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and volatility. However, it has experienced smaller drawdowns and has had positive performance on some of the market's worst days, showing it may provide a hedge in falling markets.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. Some key points:

- The statistical arbitrage strategy has underperformed the S&P 500 since inception, with returns of -1.47% annualized vs -7.64% for the index.

- However, the strategy has significantly lower risk than the index, with annualized volatility of 8.44% vs 25.52% for the S&P 500.

- On its best days, the strategy has outperformed or kept pace with the S&P 500's gains, while on down days it has held up better or gained relative to sharp

FICCI's Voice - From the desk of Dr Didar Singh, SG, FICCI

FICCI's Voice - From the desk of Dr Didar Singh, SG, FICCIFederation of Indian Chambers of Commerce & Industry (FICCI)

The document discusses the results of FICCI's latest Business Confidence Survey. It finds that business confidence has declined significantly, with companies reporting moderate to substantially worse performance over the last six months and being not too optimistic about near term performance. The Overall Business Confidence Index declined to its lowest level in 17 quarters. Expectations for key indicators like sales, profits, investments, exports and employment are subdued. Access to credit also emerged as a major issue, with more companies reporting high credit costs and limited availability. Measures like improving infrastructure, expediting stalled projects, simplifying business policies and procedures, and interest rate cuts are suggested to revive growth.The Changing Landscape of Educational Standards in the Accountancy Profession

The Changing Landscape of Educational Standards in the Accountancy Profession International Federation of Accountants

This document discusses the International Accounting Education Standards Board's (IAESB) role in establishing standards for accounting education and professional development. The IAESB aims to strengthen the global accountancy profession through high-quality education standards, promoting adoption of International Education Standards, and monitoring implementation of standards. It also discusses emerging trends impacting accounting education, key stakeholders, the IES revision project, and consequences of revising the standards.More Related Content

What's hot

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 on a cumulative and annualized return basis, but has significantly lower volatility, beta, and maximum drawdown. It has experienced negative returns on the S&P 500's best up days and positive returns on some of the S&P 500's worst down days, demonstrating an ability to achieve alpha in volatile markets.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and lower risk as measured by volatility, beta, and maximum drawdown. On its best days, the strategy failed to outperform the market's gains, but on the market's worst days, the strategy either gained or had smaller losses than the S&P 500.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. Some key points:

- The stat arb strategy has underperformed the S&P 500 since inception with returns of -2.07% versus -7.30% for the index. However, it has significantly lower risk as measured by volatility and maximum drawdown.

- On a daily basis, the strategy has generally had slightly negative or positive returns on good and bad days for the market, resulting in an annualized alpha of -2.40% versus the index.

- Risk measures like beta, correlation, and volatility are much lower for the strategy compared

Stat Arb Performance

The statistical arbitrage fund has underperformed the S&P 500 index since inception in March 2011. It has lower annualized returns, lower monthly returns currently, and a larger maximum drawdown than the S&P 500. However, it also has significantly lower risk measures like volatility, beta, and correlation to the stock market. The statistical arbitrage strategy experienced its best days on different dates than large down days in the stock market, indicating it may provide diversification during market downturns.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has outperformed the S&P 500 with lower volatility, beta, correlation and maximum drawdown. Specifically, the statistical arbitrage strategy has returned -3.24% annually compared to -12.61% for the S&P 500.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. However, it has experienced lower drawdowns than the S&P 500 and has a low correlation and beta, demonstrating that it performs differently than the broader market.

Stat Arb Performance

The statistical arbitrage fund has underperformed the S&P 500 since inception in March 2011, with returns of -3.04% compared to -8.27% for the S&P 500. The fund has lower risk metrics like volatility, beta, and maximum drawdown. It has daily alpha of -2 basis points and annualized alpha of -4.06% compared to the S&P 500. The best and worst days for the fund differ from the S&P 500 on those same days.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. It shows that the stat arb strategy has outperformed the S&P 500 with lower volatility, beta, and maximum drawdown, though it has a negative annualized return. Specifically, it provides the best and worst 3 market days for both the index and strategy.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The stat arb strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. However, it has experienced lower drawdowns and has a low correlation to the index, providing some diversification during down markets.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy called StatArb compared to the S&P 500 index since inception on March 31, 2011. Some key points:

- StatArb has underperformed the S&P 500 since inception, with returns of -2.83% versus -7.58% for the S&P 500. Its annualized returns and volatility have also been lower.

- StatArb has experienced less volatility, drawdown, and correlation to the market than the S&P 500 as evidenced by its lower beta, correlation, and maximum drawdown.

- On the best 3 days for the market, StatArb underperformed or had small positive returns

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 on a cumulative and annualized return basis but with lower volatility, beta, and maximum drawdown. It has experienced negative returns on the S&P 500's best up days but gains on some of its worst down days.

Stat Arb Performance

The statistical arbitrage strategy has underperformed the S&P 500 since inception in March 2011, with lower annualized returns and higher volatility. However, it has experienced smaller drawdowns than the market and has a near-zero correlation and beta to the S&P 500, demonstrating its ability to act as a hedge against general market moves.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. It shows that the stat arb strategy has lower overall returns, volatility, maximum drawdown and beta than the S&P 500 over this period. Specifically, the stat arb strategy has returned -2.79% since inception compared to -5.48% for the S&P 500. It also has an annualized alpha of -3.98% compared to the S&P 500.

Stat Arb Performance

The statistical arbitrage fund has outperformed the S&P 500 index since inception in March 2011, with returns of -3.38% compared to -12.37% for the S&P 500. The fund has lower risk metrics like volatility, beta, and maximum drawdown. It has experienced positive returns on the S&P 500's worst days and negative returns on some of the S&P 500's best days, demonstrating its ability to produce returns independent of the overall market direction.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception in March 2011. The stat arb strategy has underperformed the index with lower annualized returns and higher volatility. However, it has experienced smaller drawdowns and has a very low correlation to the index, indicating it provides diversification during market downturns. The strategy lagged on the index's best days but outperformed on some of its worst days.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. However, it has experienced much smaller drawdowns than the S&P 500 and has a very low correlation and beta, indicating it performs differently than the broader market.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and higher volatility. However, it has experienced lower drawdowns than the S&P 500 and has a low correlation and beta, demonstrating it can act as a hedge in falling markets.

Stat Arb Performance

This statistical arbitrage strategy has underperformed the S&P 500 since its inception in March 2011, with annualized returns of -4.74% compared to -8.06% for the S&P. It has lower volatility, beta, correlation, and maximum drawdown than the market. While it had negative returns on three of the S&P's best days, it was positive on two of the market's worst three days over the period.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 with lower annualized returns and volatility. However, it has experienced smaller drawdowns and has had positive performance on some of the market's worst days, showing it may provide a hedge in falling markets.

Stat Arb Performance

The document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. Some key points:

- The statistical arbitrage strategy has underperformed the S&P 500 since inception, with returns of -1.47% annualized vs -7.64% for the index.

- However, the strategy has significantly lower risk than the index, with annualized volatility of 8.44% vs 25.52% for the S&P 500.

- On its best days, the strategy has outperformed or kept pace with the S&P 500's gains, while on down days it has held up better or gained relative to sharp

What's hot (20)

Viewers also liked

FICCI's Voice - From the desk of Dr Didar Singh, SG, FICCI

FICCI's Voice - From the desk of Dr Didar Singh, SG, FICCIFederation of Indian Chambers of Commerce & Industry (FICCI)

The document discusses the results of FICCI's latest Business Confidence Survey. It finds that business confidence has declined significantly, with companies reporting moderate to substantially worse performance over the last six months and being not too optimistic about near term performance. The Overall Business Confidence Index declined to its lowest level in 17 quarters. Expectations for key indicators like sales, profits, investments, exports and employment are subdued. Access to credit also emerged as a major issue, with more companies reporting high credit costs and limited availability. Measures like improving infrastructure, expediting stalled projects, simplifying business policies and procedures, and interest rate cuts are suggested to revive growth.The Changing Landscape of Educational Standards in the Accountancy Profession

The Changing Landscape of Educational Standards in the Accountancy Profession International Federation of Accountants

This document discusses the International Accounting Education Standards Board's (IAESB) role in establishing standards for accounting education and professional development. The IAESB aims to strengthen the global accountancy profession through high-quality education standards, promoting adoption of International Education Standards, and monitoring implementation of standards. It also discusses emerging trends impacting accounting education, key stakeholders, the IES revision project, and consequences of revising the standards.FICCI Voice - May 2014

The document provides summaries of multiple topics discussed by FICCI (Federation of Indian Chambers of Commerce and Industry). It discusses inflation numbers in India increasing to 5.7% in March 2014 driven by fruits and vegetables. It also discusses the RBI maintaining interest rates and calls for more coordination between fiscal and monetary policy. Other topics covered include allowing evening trading in agricultural commodities, promoting IP awareness in India, India's IP laws being TRIPS compliant, requesting clearance of environmental projects during elections, and promoting tourism in India.

FICCI's Voice - May 2015

The document summarizes comments from FICCI (Federation of Indian Chambers of Commerce and Industry) on various economic issues in India:

1) FICCI welcomes the new foreign trade policy 2015-2020 and comments that it provides a roadmap to increase exports, employment, and ease of doing business.

2) FICCI expresses concern over falling exports in March 2015 and calls for steps to reverse the trend.

3) FICCI comments that while manufacturing growth was positive in 2014-2015, challenges like interest rates and infrastructure need addressing for continued growth.

4) FICCI signs a cooperation agreement with Turkey to establish forums to promote trade and investment between the two countries.

The Impact of Integrated Reporting

Presentation given by Graham Terry, senior executive, strategy and thought leadership, South African Institute of Chartered Accountants, during the International Federation of Accountants (IFAC) integrated reporting seminar, A Fundamental Shift in Corporate Reporting, November 14, 2012.

Robert Dacey, Chief Accountant Government Accountability Office USA - IFAC So...

Robert Dacey, Chief Accountant Government Accountability Office USA - IFAC So...International Federation of Accountants

The document summarizes long-term fiscal sustainability reporting in the U.S., including the timeline of reporting, types of projections provided, and illustrative charts and tables. Key developments include unaudited social insurance reporting starting in 1999, audited Statements of Social Insurance beginning in 2006, and comprehensive long-term fiscal projections reporting starting in 2010 on a unaudited basis and becoming audited in 2013. Projections provided include 75-year present values of receipts and spending, fiscal gaps, and alternative scenarios. Charts and tables illustrate historical and projected trends in receipts, spending, debt, and their composition through 2086 under current policy assumptions.Viewers also liked (6)

FICCI's Voice - From the desk of Dr Didar Singh, SG, FICCI

FICCI's Voice - From the desk of Dr Didar Singh, SG, FICCI

The Changing Landscape of Educational Standards in the Accountancy Profession

The Changing Landscape of Educational Standards in the Accountancy Profession

Robert Dacey, Chief Accountant Government Accountability Office USA - IFAC So...

Robert Dacey, Chief Accountant Government Accountability Office USA - IFAC So...

Similar to Stat Arb Performance

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index since inception on March 31, 2011. The statistical arbitrage strategy has underperformed the S&P 500 on a cumulative, annualized, and month-to-date basis. It has lower annualized volatility, beta, and maximum drawdown than the S&P 500. The best and worst days for the strategy differ from the S&P 500, with the strategy generating negative returns on some of the market's strongest up days and positive returns on some of its strongest down days.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 index from inception on March 31, 2011 through December 22, 2011. The statistical arbitrage strategy has underperformed the S&P 500 on a year-to-date, annualized, and maximum drawdown basis but has lower volatility and essentially no correlation to the stock market. It has also outperformed on the strategy's best and worst market days compared to the S&P 500.

Stat Arb Performance

The document summarizes the statistical arbitrage track record of a fund compared to the S&P 500 from inception on March 31, 2011 through December 8, 2011. The fund has underperformed the S&P 500 since inception with returns of -4.68% versus -6.90% for the S&P 500. The fund aims to achieve positive returns with lower risk than the market as evidenced by its lower beta, volatility, correlation and maximum drawdown compared to the S&P 500.

Stat Arb Performance

The document summarizes the statistical arbitrage track record of a fund called StatArb1 compared to the S&P 500 index from inception on March 31, 2011 through December 13, 2011. It shows that StatArb1 has underperformed the S&P 500 on all return metrics over this period, with lower annualized and monthly returns but also lower volatility, beta, correlation, and maximum drawdown compared to the S&P 500.

Stat Arb Performance

The statistical arbitrage strategy underperformed the S&P 500 index since inception in March 2011, with annualized returns of -6.74% compared to -11.70% for the S&P 500. In the past month and week, the strategy declined 0.37% and 0.28% respectively, outperforming the S&P 500's declines of 2.50% and 3.14%. The strategy has lower volatility, beta, correlation and maximum drawdown compared to the S&P 500.

Stat Arb Performance

The document summarizes the statistical arbitrage track record of a fund called StatArb1 compared to the S&P 500 index from inception on March 31, 2011 through December 28, 2011. It shows that StatArb1 has underperformed the S&P 500 on a return basis since inception but with lower annualized volatility, beta, correlation, and maximum drawdown, demonstrating lower risk. The best and worst three market days for both StatArb1 and the S&P 500 are also listed.

Stat Arb Performance

The statistical arbitrage strategy has outperformed the S&P 500 since inception on March 31, 2011, with returns of 0.92% compared to -9.18% for the S&P 500. The strategy has an annualized return of 1.95% and annualized volatility of 6.95%, much lower than the S&P 500's annualized return of -19.49% and volatility of 24.49%. While the strategy had its largest single day loss of -1.35%, it has had a maximum drawdown of only -3.84%, far lower than the S&P 500's maximum drawdown of -17.90%.

StatArb Performance

This document summarizes the performance of a statistical arbitrage fund (StatArb1) compared to the S&P 500 index from inception on March 30, 2012 through May 2, 2012. It shows that StatArb1 has lower returns than the S&P 500 since inception and month-to-date, but lower volatility, beta, and maximum drawdown, indicating it may be a less risky investment.

Stat Arb Performance

This document summarizes the performance of a statistical arbitrage strategy compared to the S&P 500 from inception on March 30, 2012 through April 30, 2012. The statistical arbitrage strategy has outperformed the S&P 500 over all time periods shown with lower volatility, beta, and maximum drawdown, though it has a positive correlation to the S&P 500.

Stat Arb Performance

This document provides the performance statistics of a statistical arbitrage strategy called StatArb1 compared to the S&P 500 index from inception on March 30, 2012 through April 27, 2012. It shows that StatArb1 has lower returns but significantly lower risk than the S&P 500 as measured by volatility, beta, correlation, and maximum drawdown.

Slides from PreSeed Academy #20 - Morten Poulsen (Speaker 2 of 3)

1. Plytix is a product information management platform that aims to minimize customer churn by focusing on achieving product-market fit before prematurely scaling.

2. The company tracks key performance indicators like a point-based "Point of Minimum Churn" score to measure customer engagement and retention on a monthly basis.

3. Plytix analyzes churn rates among customer cohorts that onboarded in different months to understand churn patterns and inform strategies to improve retention.

Similar to Stat Arb Performance (11)

Slides from PreSeed Academy #20 - Morten Poulsen (Speaker 2 of 3)

Slides from PreSeed Academy #20 - Morten Poulsen (Speaker 2 of 3)

Stat Arb Performance

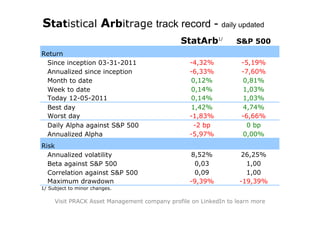

- 1. Statistical Arbitrage track record - daily updated StatArb1/ S&P 500 Return Since inception 03-31-2011 -4,32% -5,19% Annualized since inception -6,33% -7,60% Month to date 0,12% 0,81% Week to date 0,14% 1,03% Today 12-05-2011 0,14% 1,03% Best day 1,42% 4,74% Worst day -1,83% -6,66% Daily Alpha against S&P 500 -2 bp 0 bp Annualized Alpha -5,97% 0,00% Risk Annualized volatility 8,52% 26,25% Beta against S&P 500 0,03 1,00 Correlation against S&P 500 0,09 1,00 Maximum drawdown -9,39% -19,39% 1/ Subject to minor changes. Visit PRACK Asset Management company profile on LinkedIn to learn more

- 2. 0,80 0,85 0,90 0,95 1,00 1,05 31-Mar 10-Apr 20-Apr 30-Apr 10-May 20-May 30-May 9-Jun 19-Jun Daily Performance 29-Jun 9-Jul 19-Jul 29-Jul 8-Aug 18-Aug 28-Aug 7-Sep 17-Sep 27-Sep 7-Oct 17-Oct 27-Oct 6-Nov 16-Nov 26-Nov S&P 500 6-Dec StatArb 16-Dec 26-Dec Inception date=1 Statistical Arbitrage track record - daily updated

- 3. Statistical Arbitrage track record - daily updated S&P 500 StatArb Best 3 market days1/ 08-09-2011 4,74% -0,28% 08-11-2011 4,63% -0,49% 11-30-2011 4,33% -0,44% Worst 3 market days1/ 08-08-2011 -6,66% 0,39% 08-04-2011 -4,78% 0,74% 08-18-2011 -4,46% -1,35% 1/ since inception date 03-31-2011