Downloaded 12 times

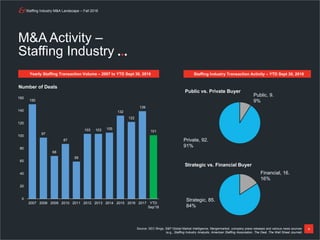

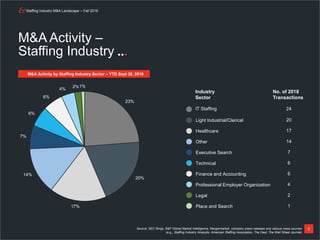

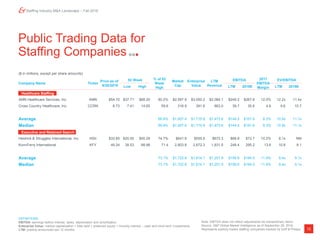

The document analyzes M&A activity in the staffing industry, noting that 101 transactions occurred in the first 9 months of 2018, with 92 unique private buyers completing acquisitions and strategic buyers accounting for 84% of deals. Professional staffing companies like IT, healthcare, and life sciences saw the most demand from buyers. The recovery environment has encouraged strong financial performance and ownership changes in the staffing industry through M&A and recapitalization transactions.