Download to read offline

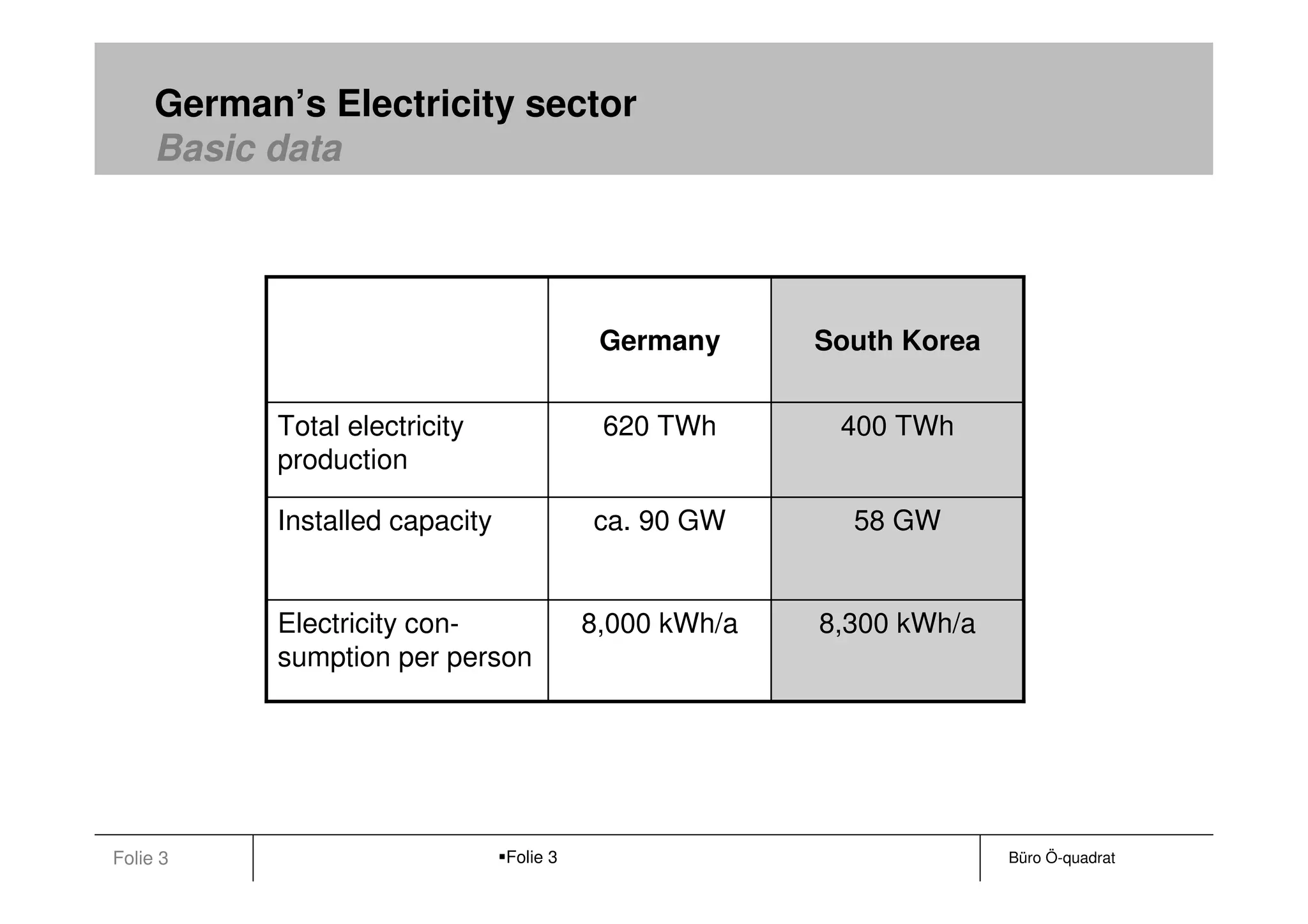

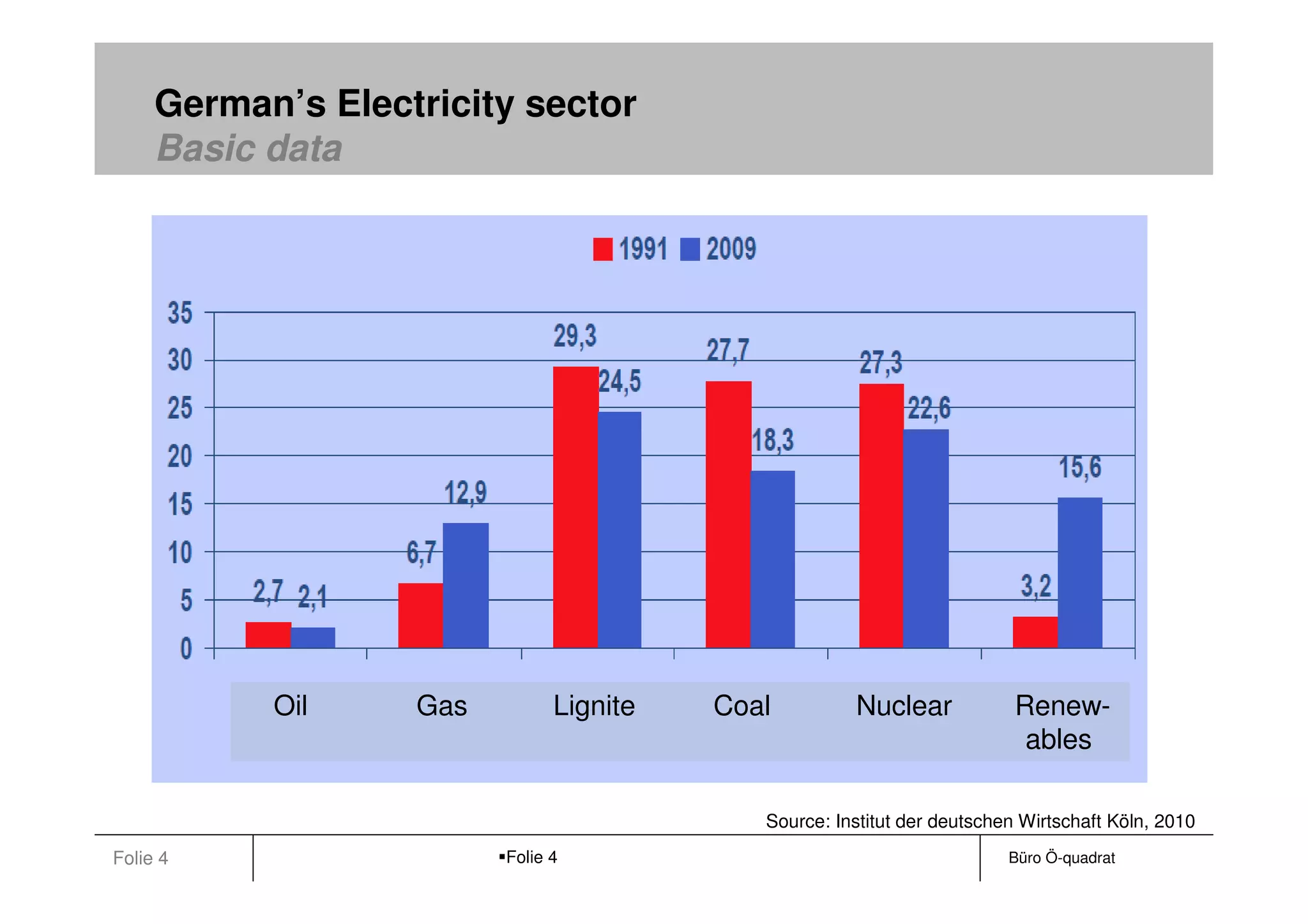

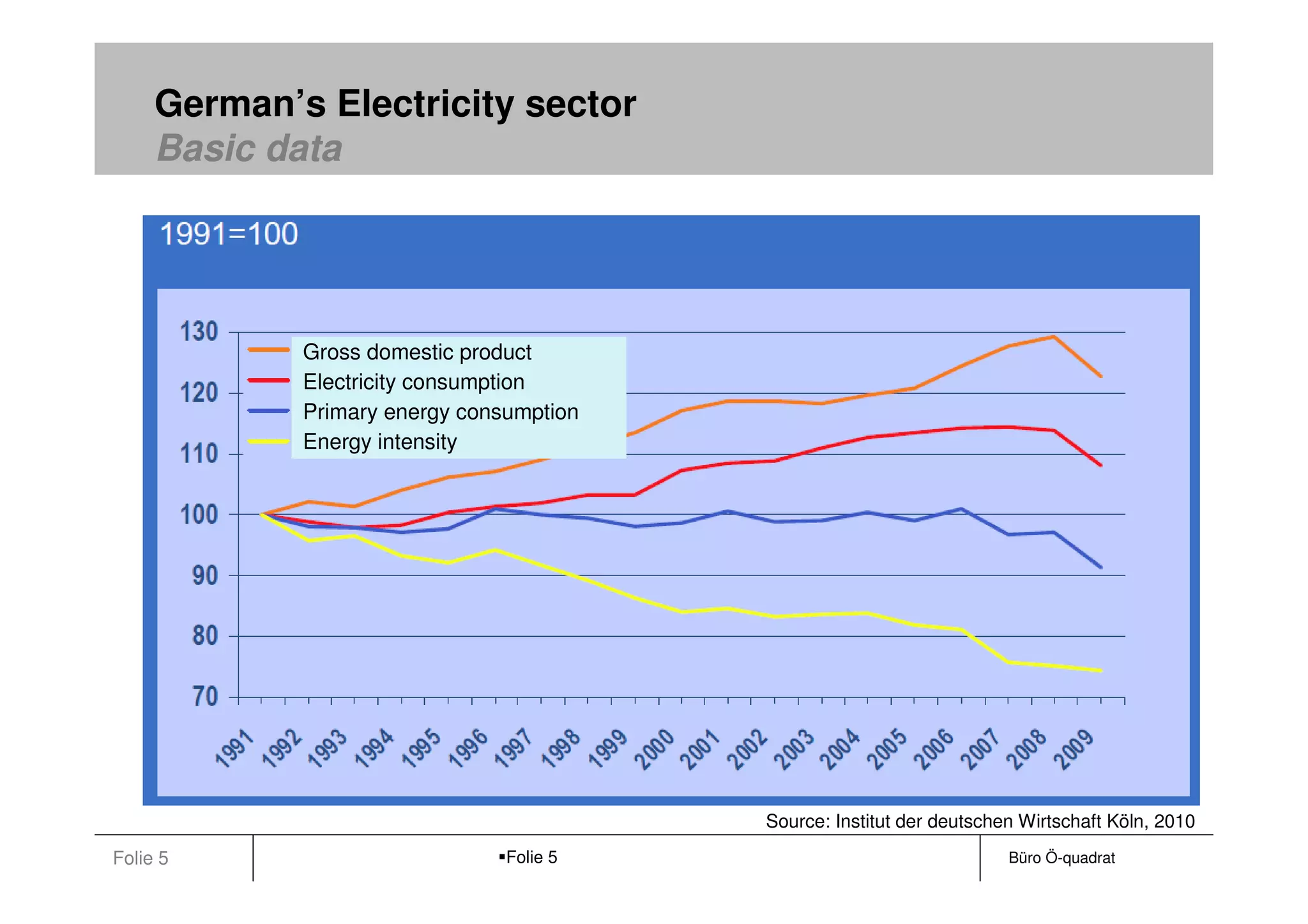

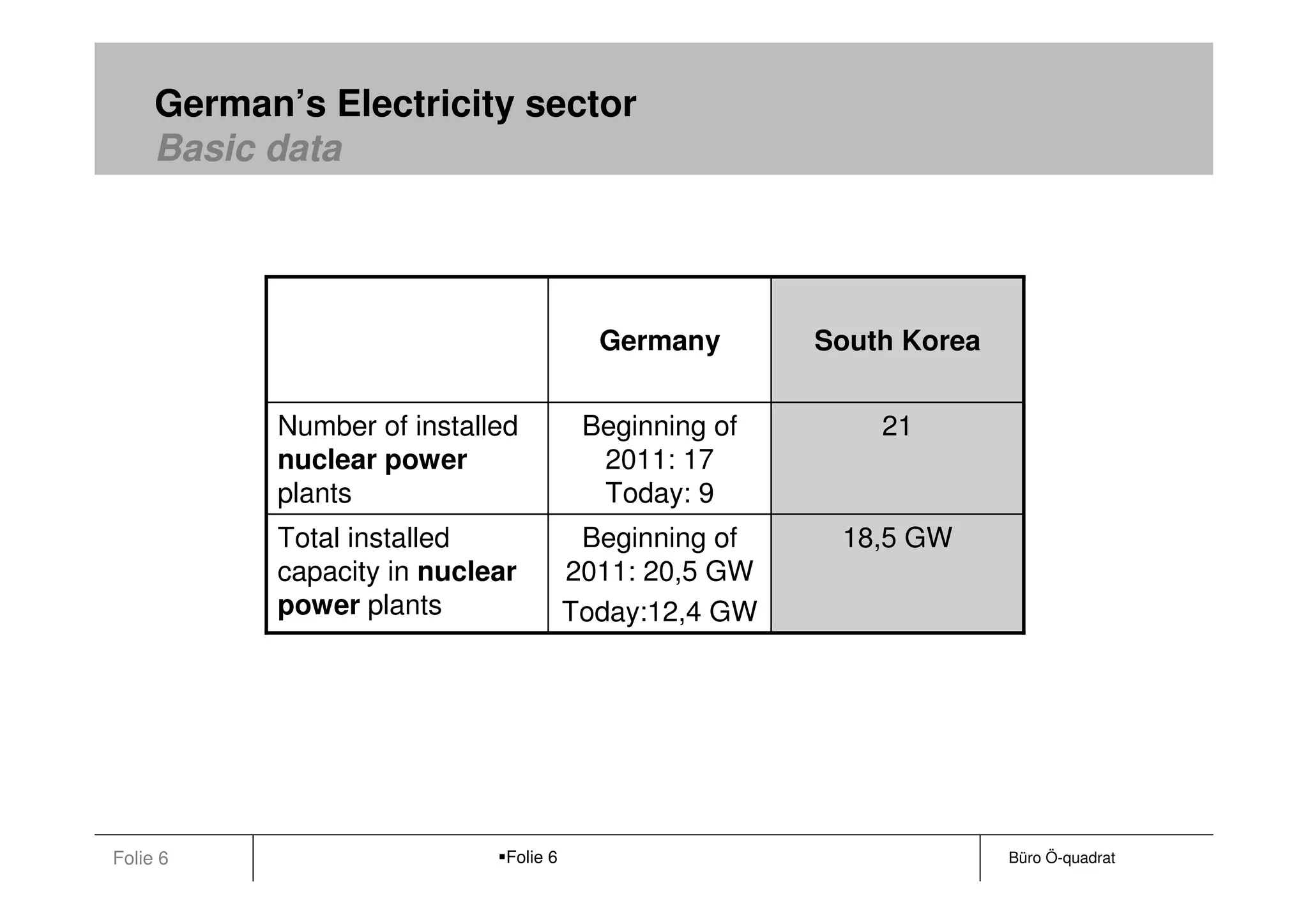

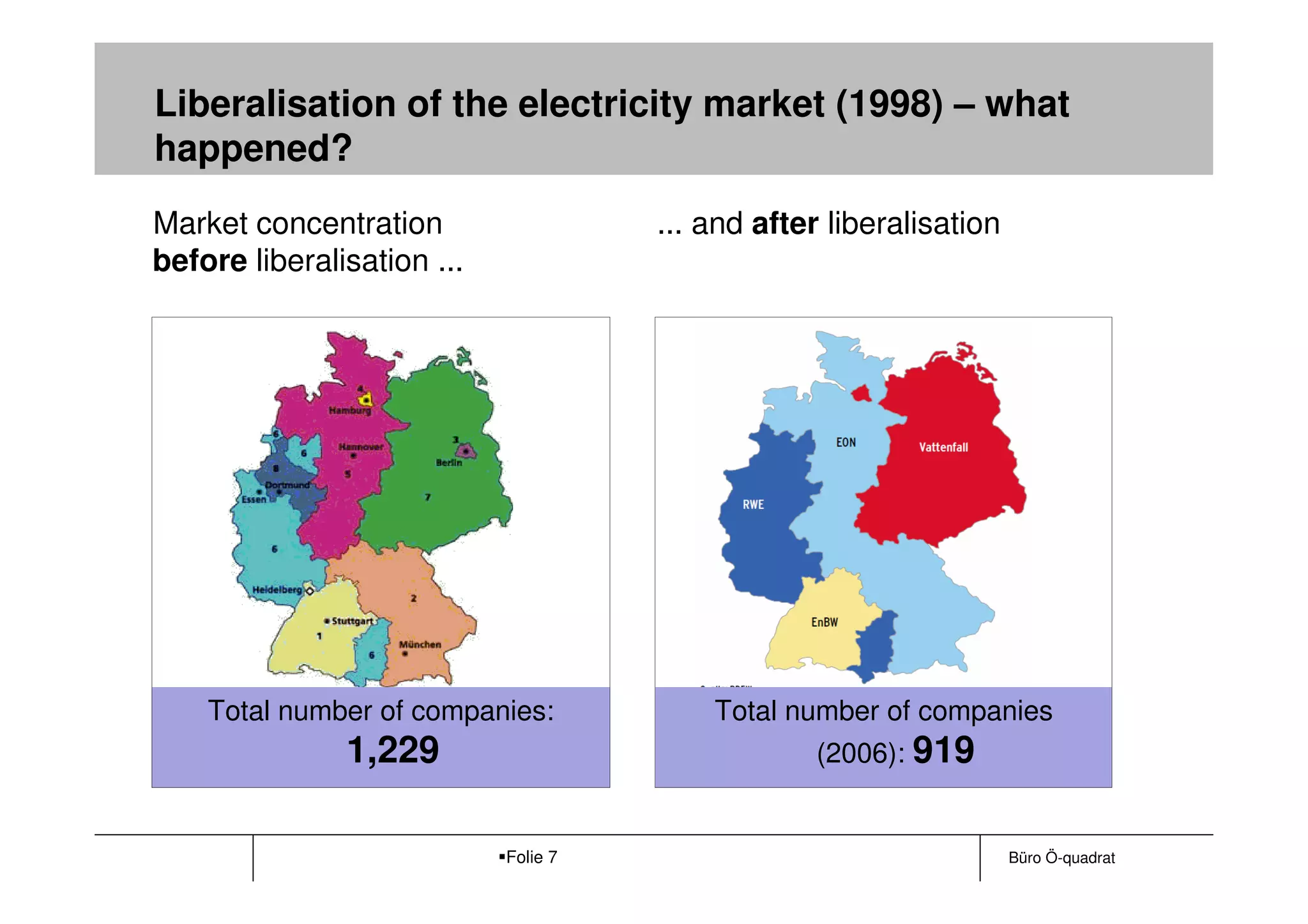

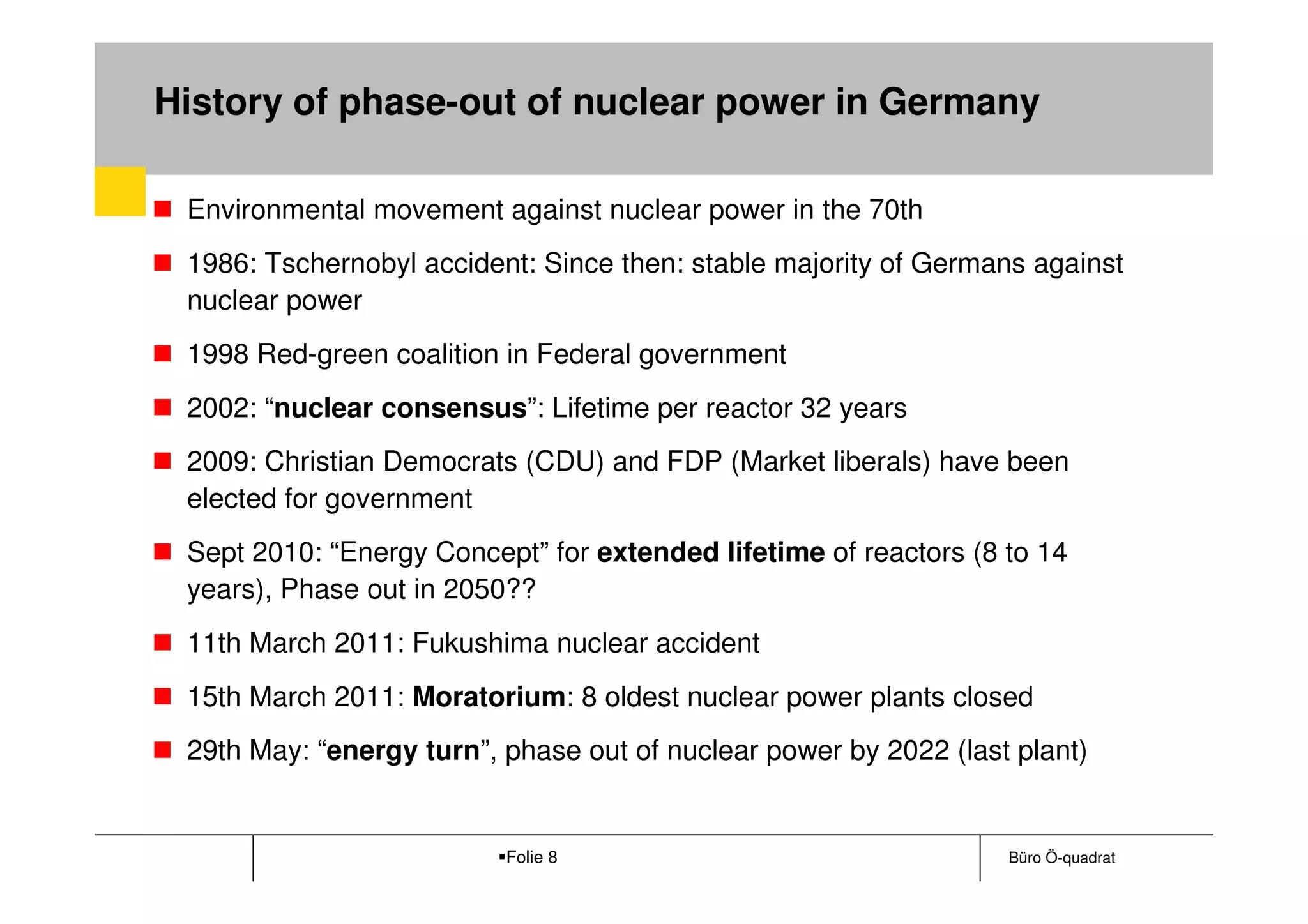

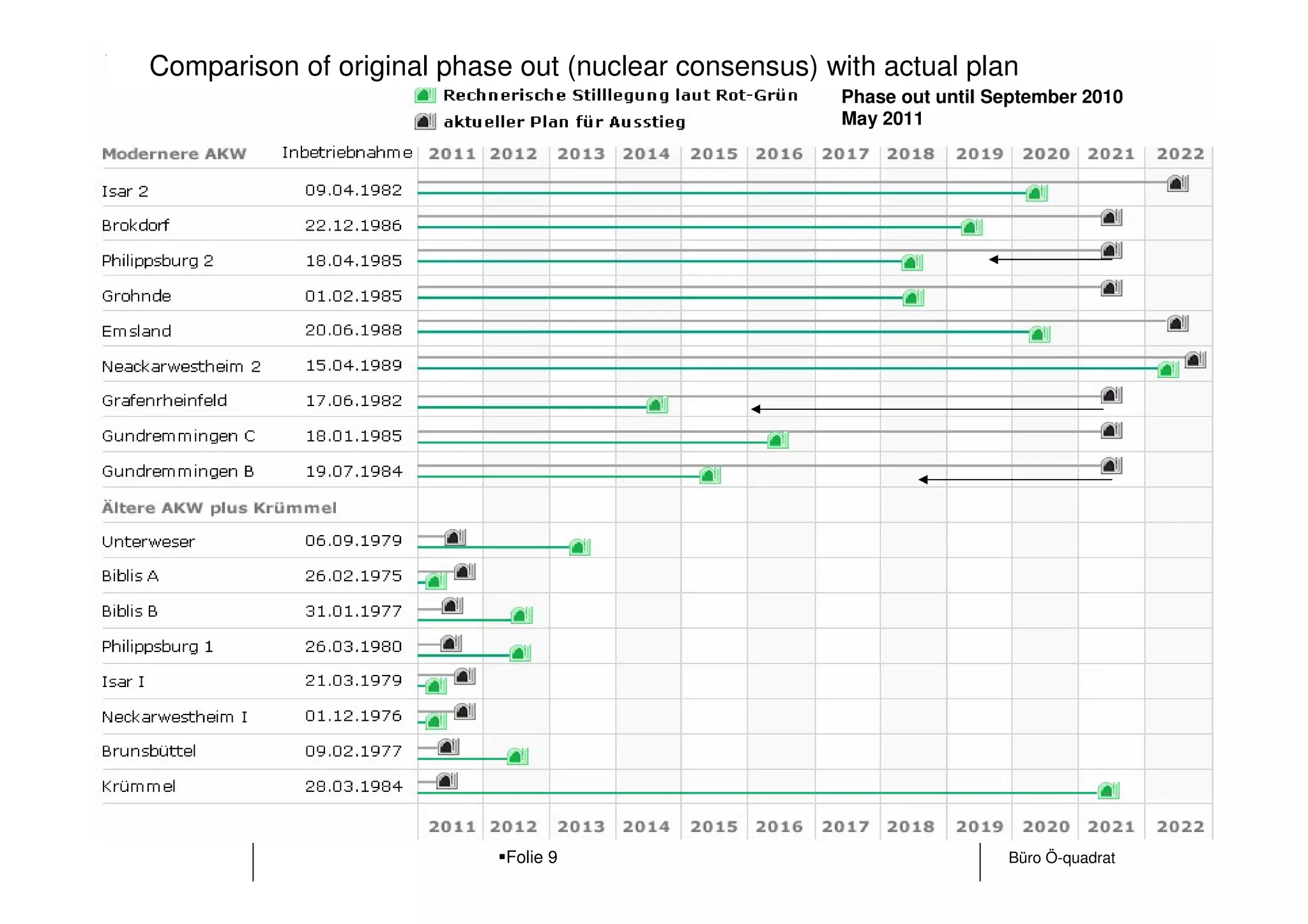

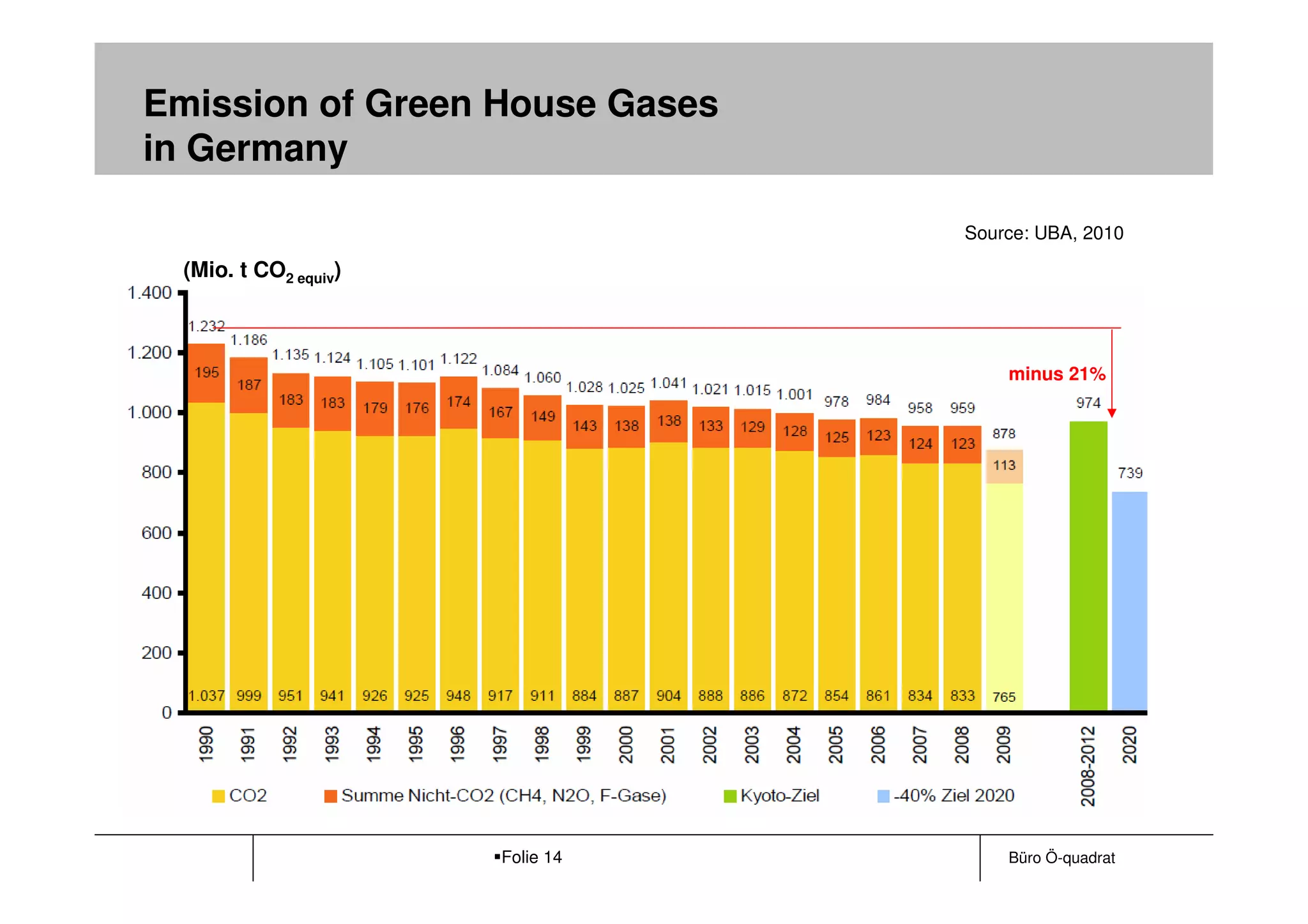

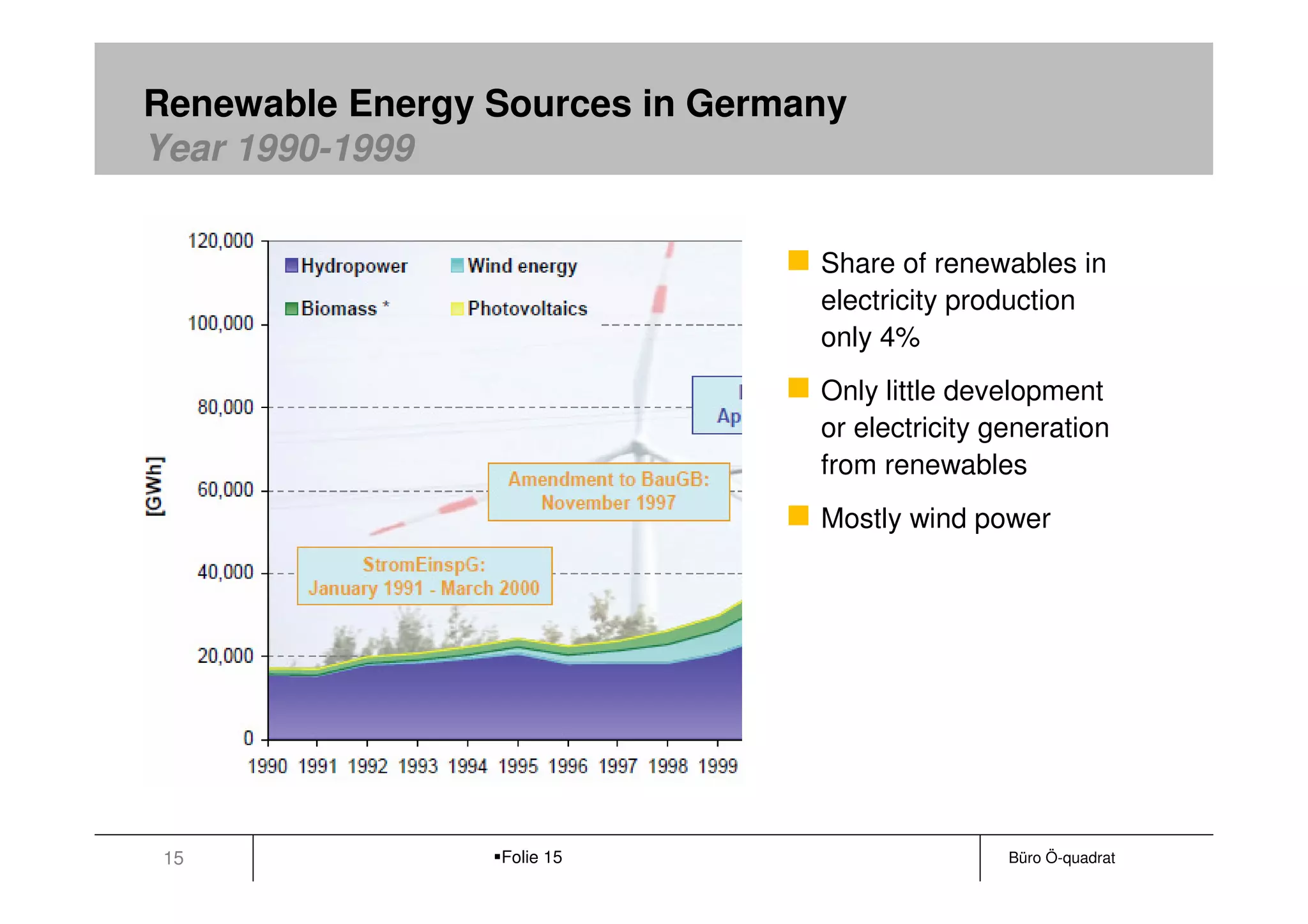

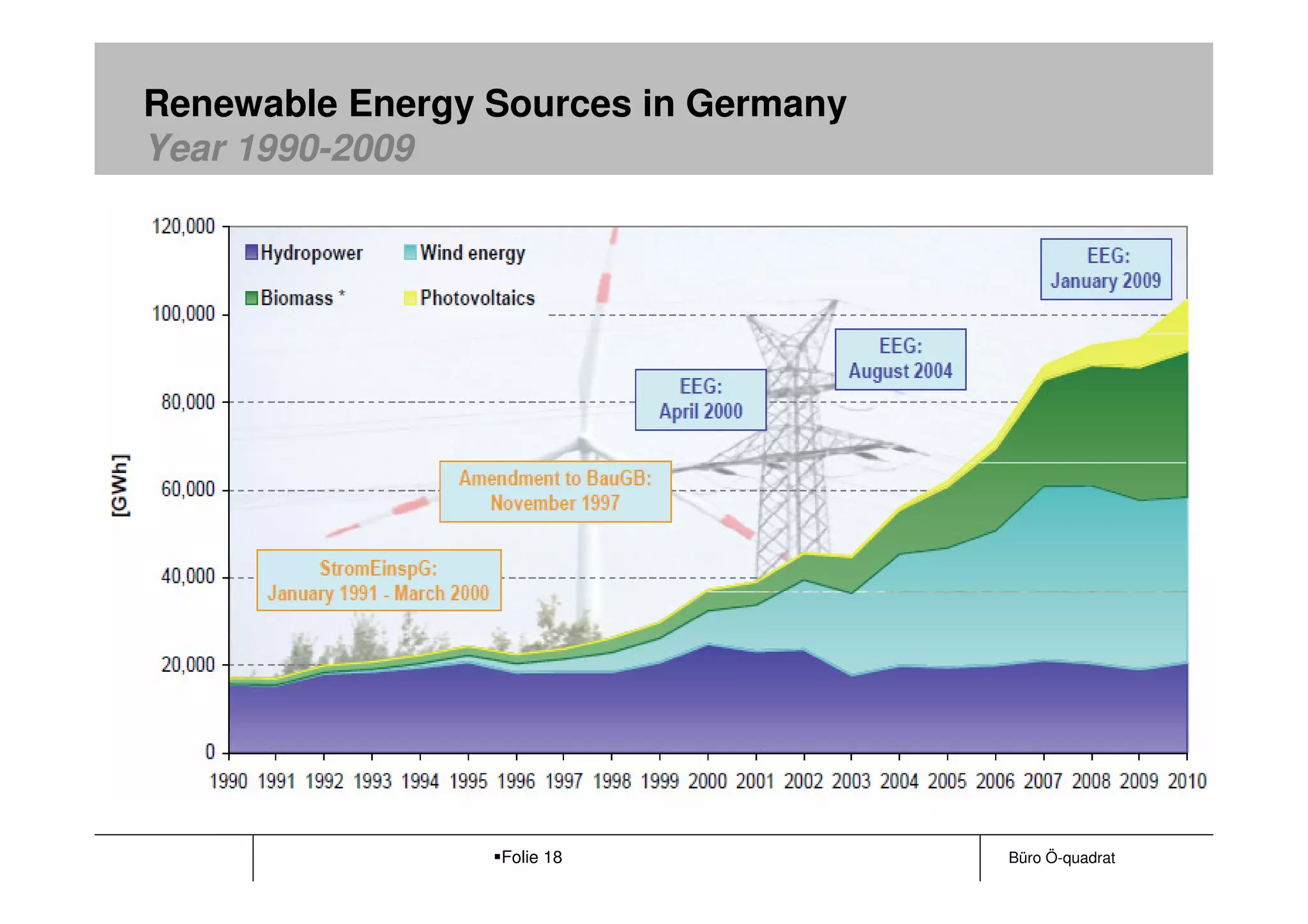

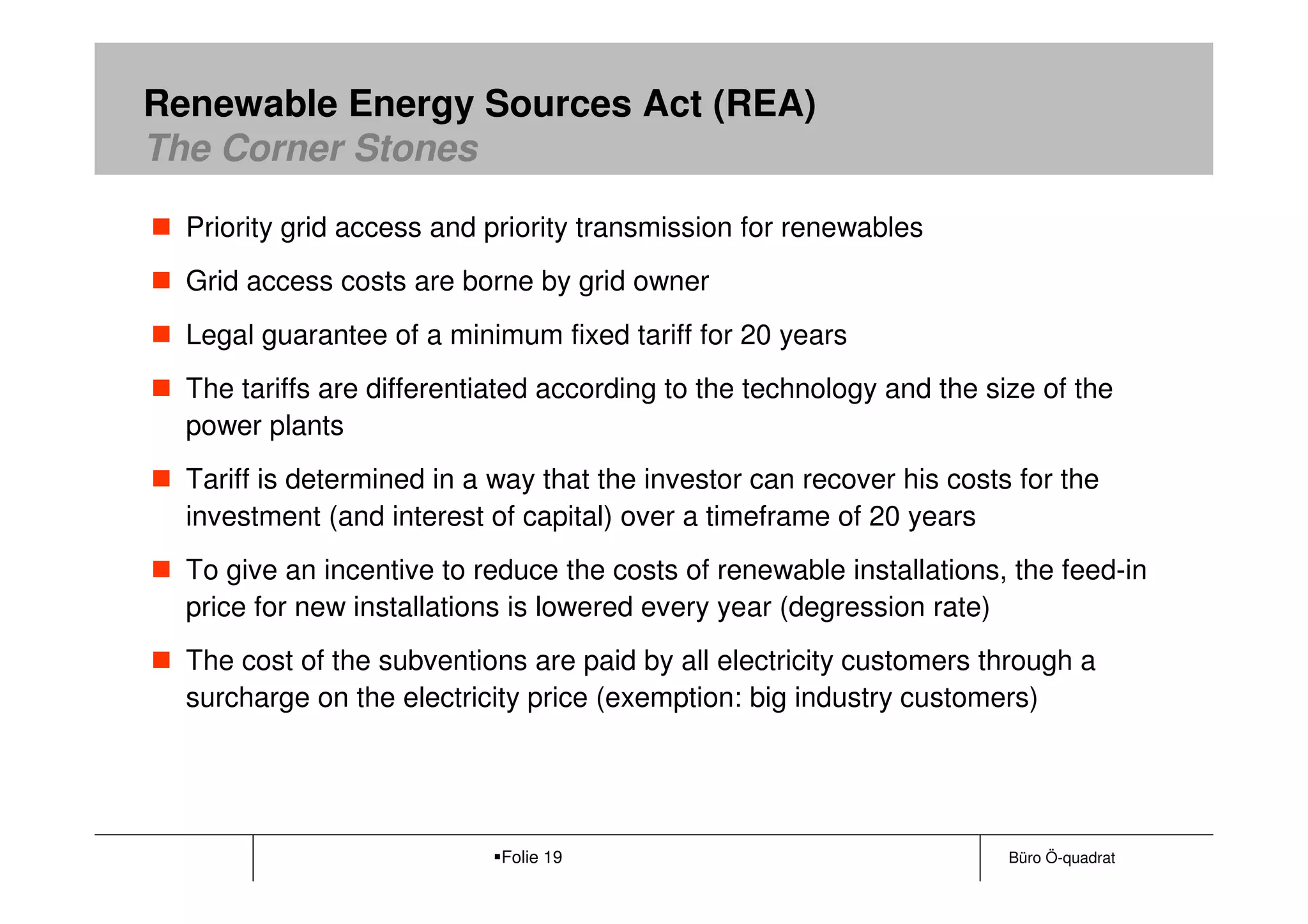

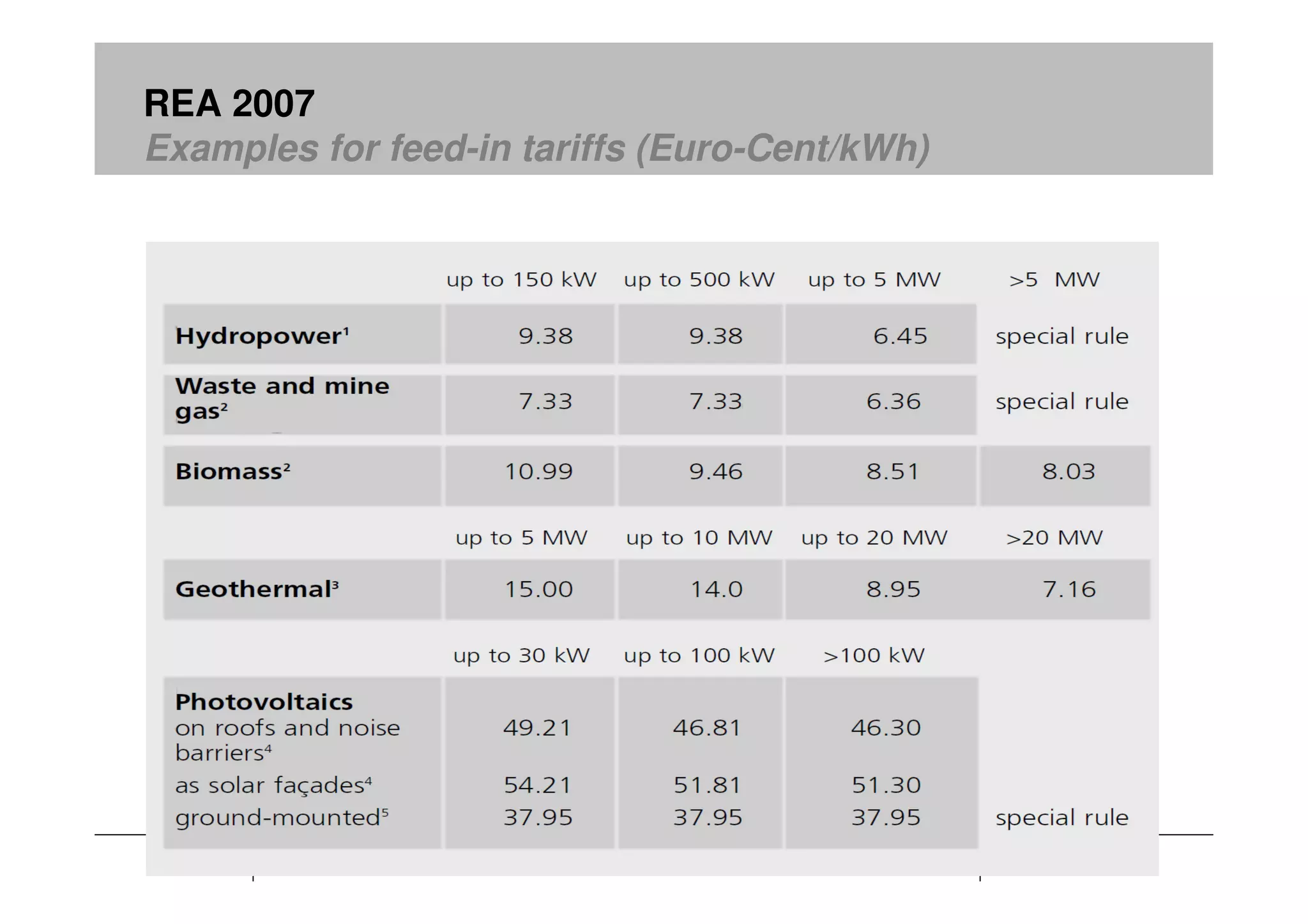

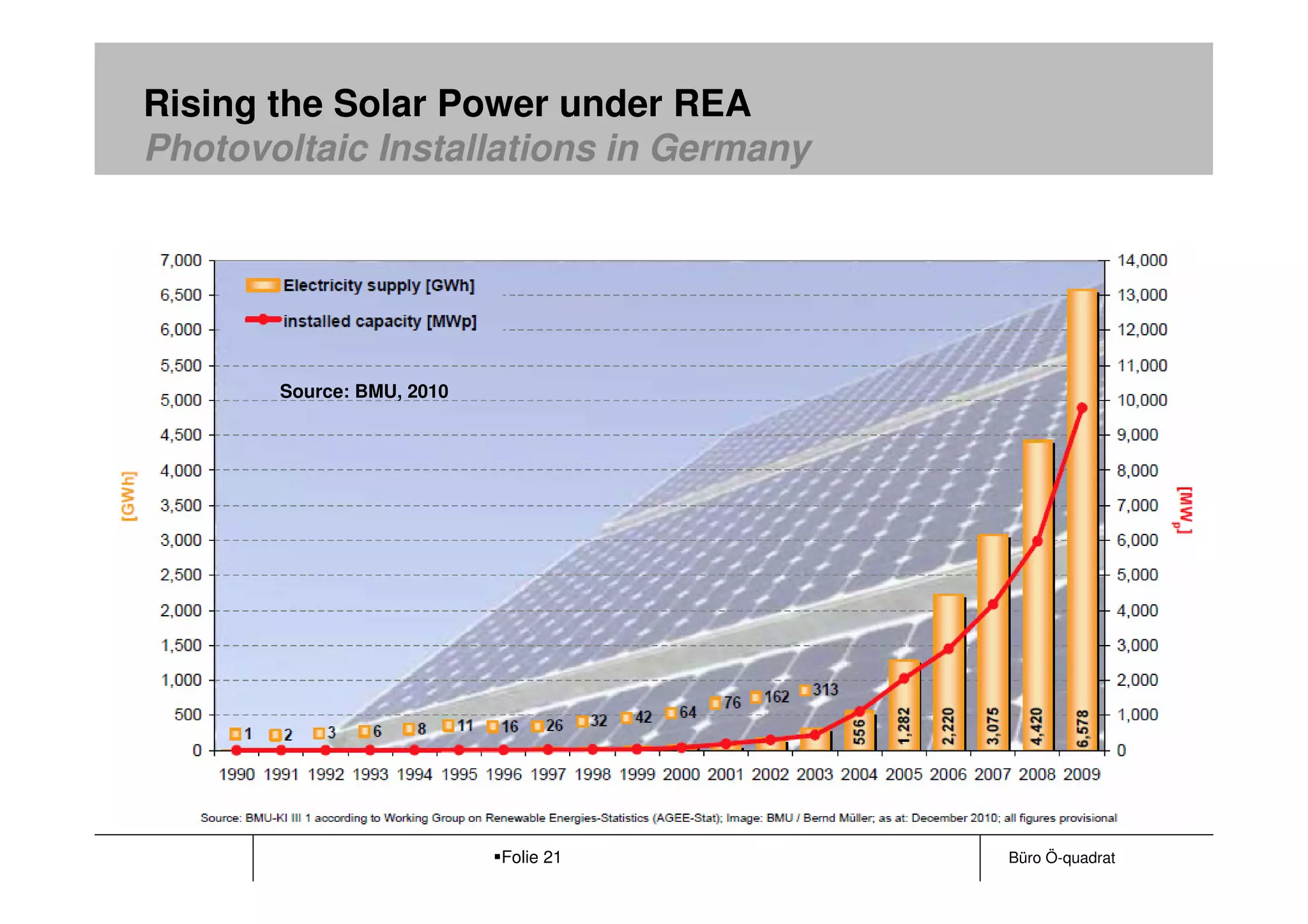

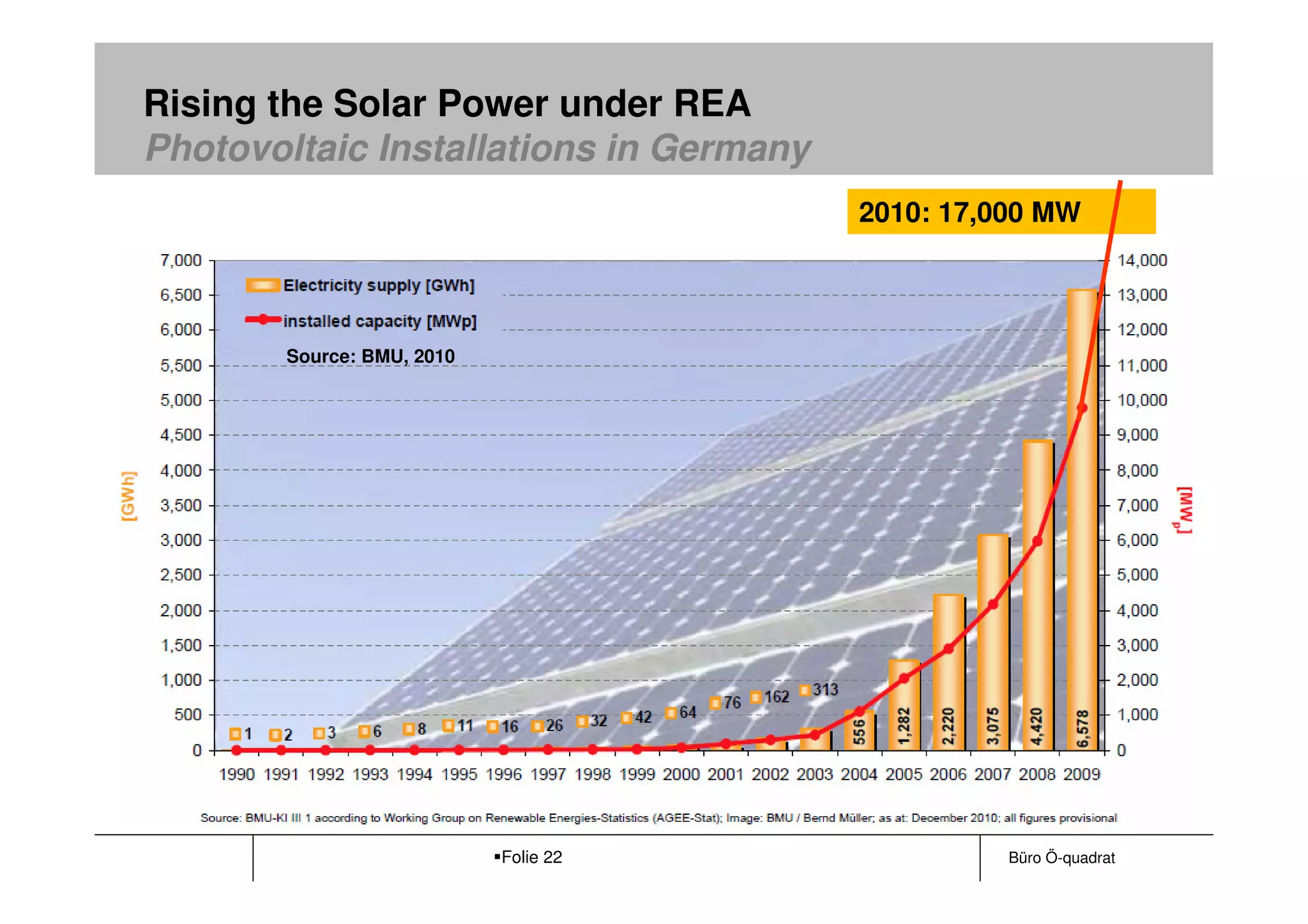

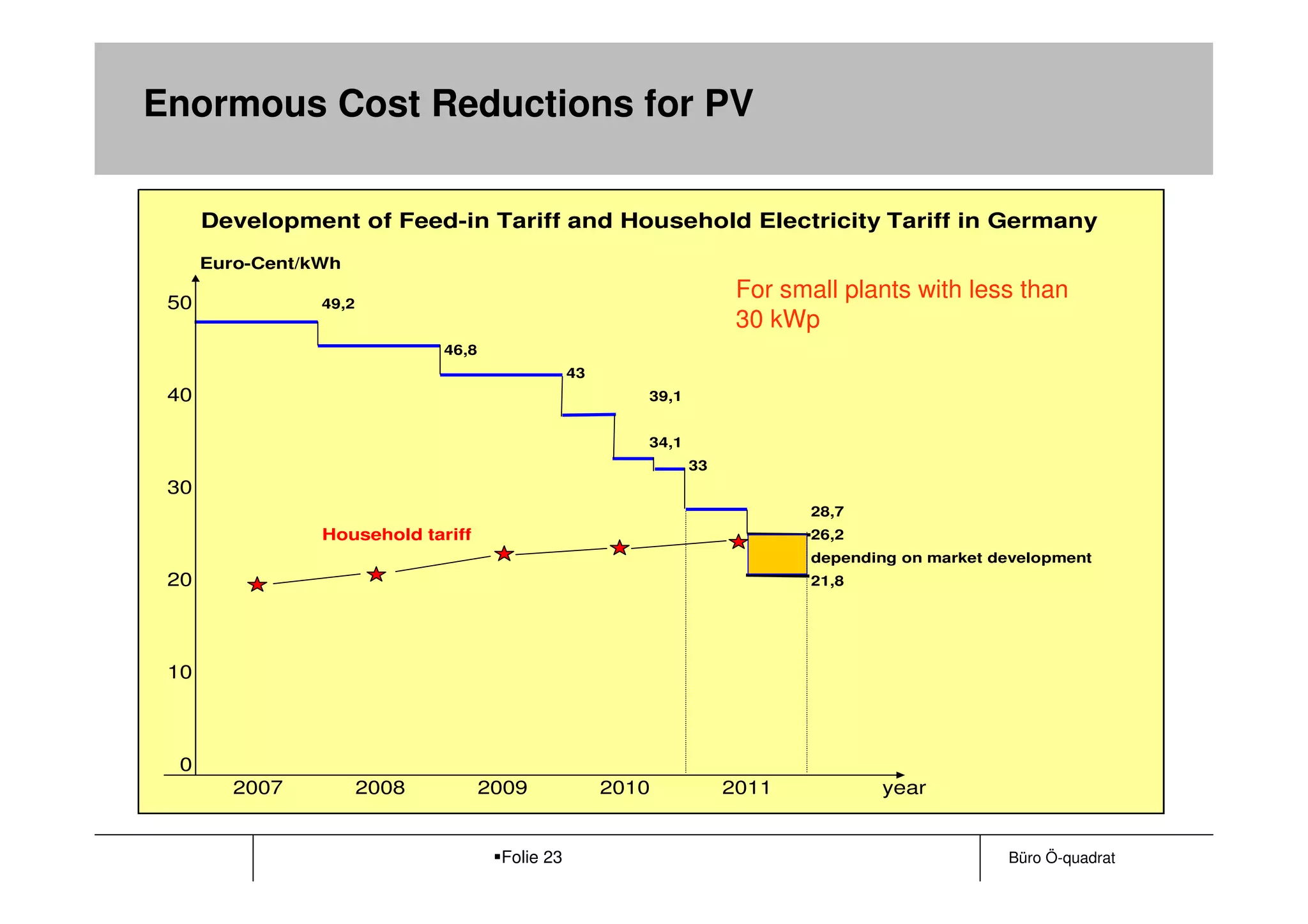

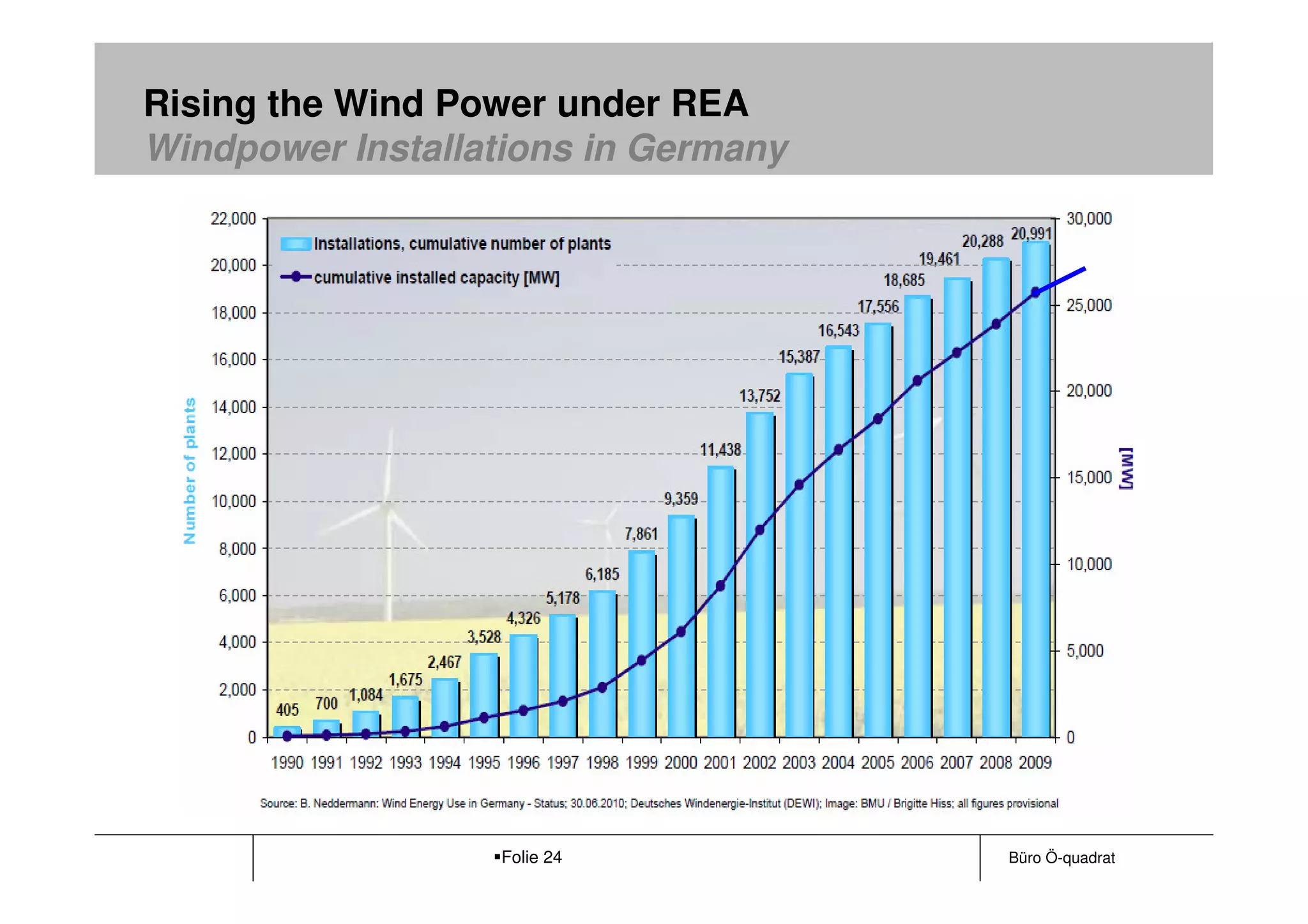

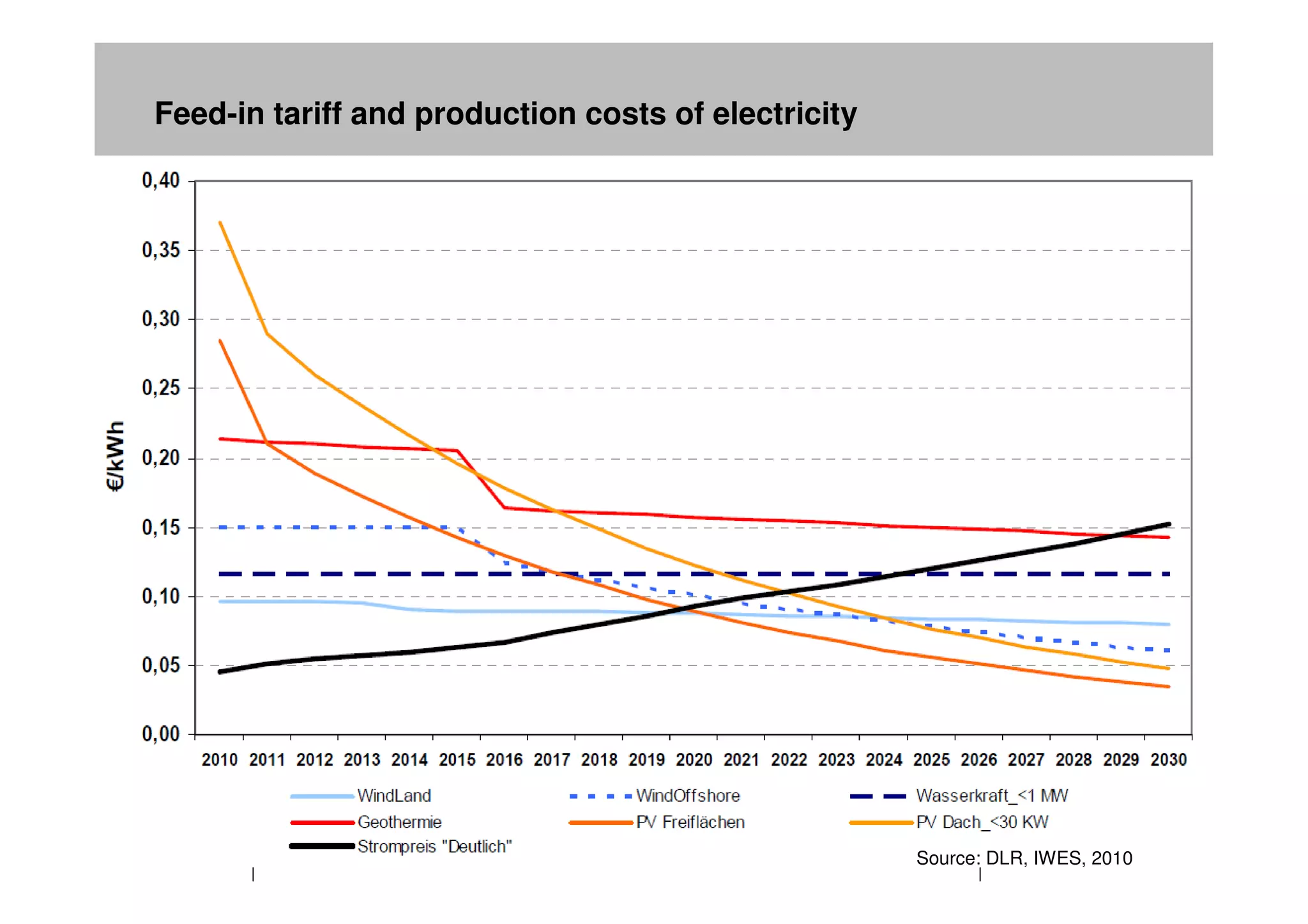

This document discusses Germany's phase out of nuclear energy and development of sustainable energy. It provides an overview of Germany's electricity sector and history of the nuclear phase out. Key reasons for closing nuclear reactors included risks of accidents, terrorism, waste storage, and proliferation. Germany set goals to reduce emissions 40% by 2020 and increase renewable energy to 35% of electricity by 2020. The Renewable Energy Act led to a renewable energy success story by establishing feed-in tariffs that guarantee prices for green energy producers. This incentivized growth of solar and other renewables in Germany.